TNRSF - Q1 2023 Earnings Preview: An Important Day For Schlumberger

2023-04-19 07:30:00 ET

Summary

- The management team at Schlumberger Limited is expected to announce results for the first quarter of the company's 2023 fiscal year soon.

- Leading up to that point, analysts have high expectations, but these may not be unrealistic.

- The firm is also healthy and affordable at this time, which makes me feel bullish about SLB stock.

Over the past year or so, many companies that are dedicated in some capacity to the energy sector have thrived. This makes sense when you consider just how high the prices of oil and, up until recently, natural gas, have been. One of the companies that have benefited and look set to continue benefiting from current market conditions is Schlumberger Limited ( SLB ). Although management has been transitioning the company to focus on more digital and other technology-oriented operations, the company still does generate the largest portion of its revenue from things such as well construction and similar activities. It is true, however, that we are dealing with rapidly changing and uncertain market conditions. This does create some uncertainty when it comes to the company's prospects as an investment opportunity.

The good news for investors is that they will soon have a good look at exactly how the company has been performing as of late. This is because, in the next few days, management will be reporting financial results covering the first quarter of the company's 2023 fiscal year. Leading up to that time, there are some things that investors would be wise to keep a close eye on. These are aspects of the company and its performance that will go a long way toward determining how healthy the company is and how the market perceives it to be over the next few months.

Schlumberger Q1 earnings - What to keep an eye on

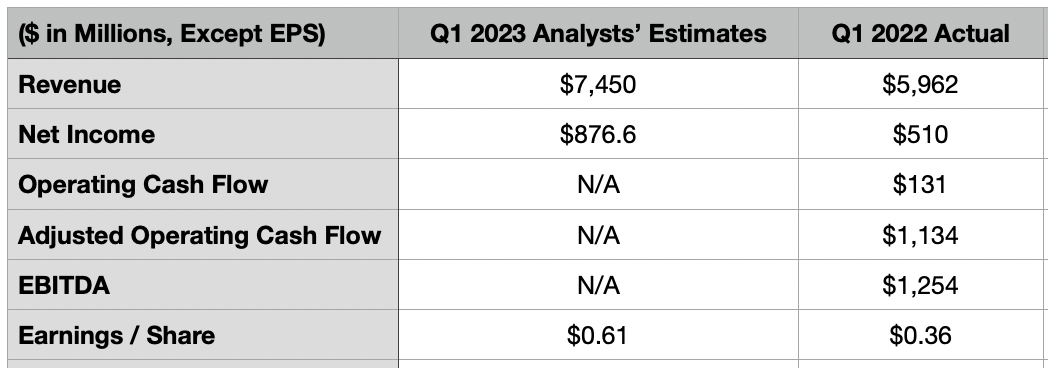

Before the market opens on April 21st, the management team at Schlumberger is expected to announce financial results covering the first quarter of the company's 2023 fiscal year. Leading up to that time, there are some expectations that analysts have already set for the business. These will be top of mind when the company reports. For starters, revenue is expected to come in at $7.45 billion. If this comes to fruition, it will translate to a year-over-year increase of 25% compared to the $5.96 billion the company reported one year earlier.

{kind=link}

Such a significant increase for such a large company in a mature industry may seem unrealistic. But there are likely a few drivers behind this upside. In 2022 , the company was still very much focused on activities like well construction, production systems, and reservoir performance. But in its annual report, it describes itself as a global technology company that helps to drive energy innovation. Although one could argue that technology is at the center of what the business does, few would agree that it is, today, a technology enterprise. Rather, it is a business that aspires to become one.

Along this vein, management is working to achieve significant growth on the digital and integration side of the enterprise. During 2022, $3.73 billion of the company's revenue came from these activities. That was 13.2% higher than the $3.29 billion generated one year earlier. I don't expect this to be the fastest-growing portion of the business. But I do believe that any growth that it achieves will have a significant positive impact on the company's bottom line. I say this because, even though the Digital & Integration segment of the firm accounts for only 13.1% of the company's revenue, it is responsible for 26.2% of its pre-tax income.

The fastest-growing portion of the company, at least for now, would likely be the Well Construction segment. For those not familiar, this is the part of the company that focuses on combining all of the resources at its disposal in order to optimize well placement and performance, maximize drilling efficiency, and improve wellbore assurance. In 2022, this segment generated revenue of $11.40 billion. That was 30.9% higher than the $8.71 billion it generated only one year earlier. At the end of the day, a good portion of the company's business is related to drilling activities. When focusing on the US alone, the picture has been quite bullish. In the first three months of this year, for instance, an estimated 2,985 wells were drilled across the country. That compares to the 2,362 that were drilled the same time one year earlier. Meanwhile, completions totaled 3,004. That's up from the 2,421 that were completed the same time last year. Naturally, this would prove bullish for a company such as Schlumberger.

On the bottom line, analysts believe that the company will report earnings per share of $0.61. This would represent a significant improvement over the $0.36 per share that the company reported one year earlier. Given the number of shares the company currently has outstanding, this would translate to net income of $876.6 million. That's materially higher than the $510 million reported one year earlier. None of this would surprise me. As I mentioned already, the Digital & Integration segment is likely to post attractive growth year over year and the high margins it offers should be beneficial for the enterprise. On top of this, the firm operates in a space that, at the moment, has a high level of demand for what it can provide. This gives the company pricing power the likes of which it did not have a few years ago.

{kind=link}

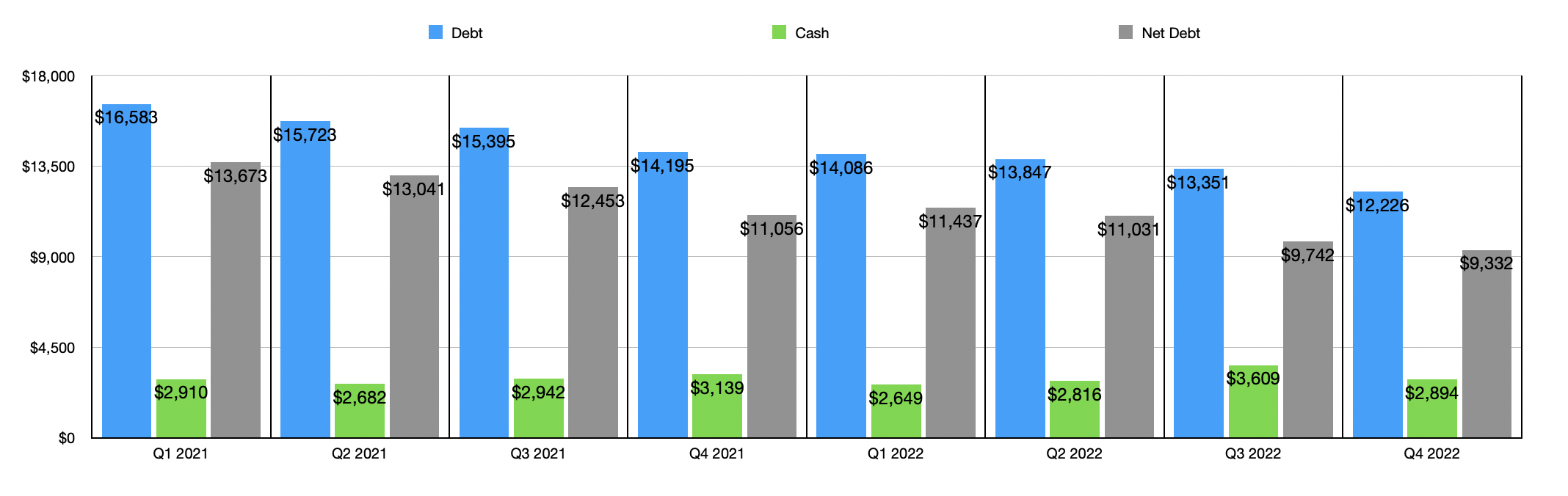

Outside of what analysts expect, there are some other items that investors should be paying attention to. For instance, there are other cash flow metrics that are important. For context, in the first quarter of 2022, the company generated operating cash flow of $131 million. If we adjust for changes in working capital, that number balloons to $1.13 billion. And on top of that, EBITDA for the enterprise was $1.25 billion. All of these would be incredibly important. Another important metric will be leverage. As you can see in the chart above, management has done well to reduce the company's overall leverage. Back in the first quarter of 2021, for instance, the enterprise had net debt of $13.67 billion. Thanks to the strong cash flows that management achieved, combined with a share increase of 47 million units, the company has been able to reduce debt, on a net basis, to $9.33 billion as of the end of the 2022 fiscal year. If profits are slated to increase for the first quarter, cash flows will likely come in strong as well. I wouldn't be surprised to see net debt fall further, especially given that interest rates are comfortably higher than they were a year earlier.

{kind=link}

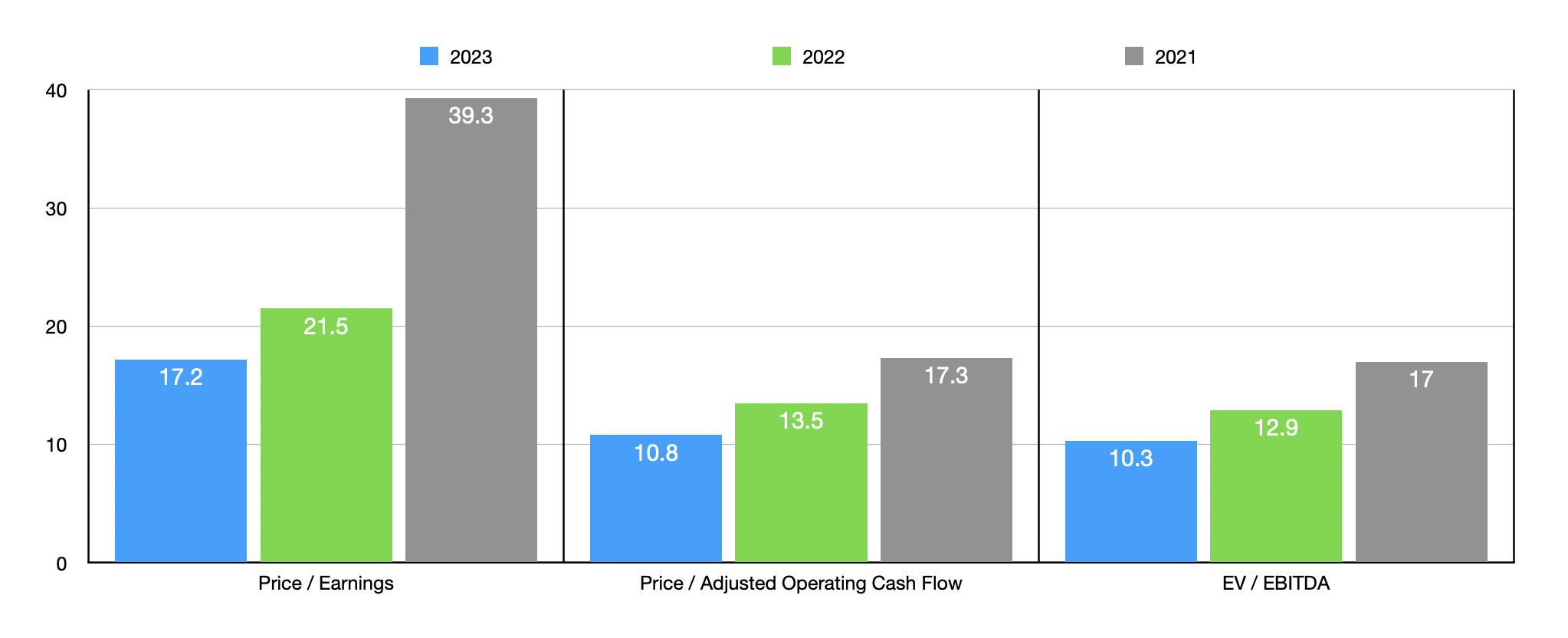

Of course, those who are looking to buy stock in the company should continue to pay attention to its valuation. In the chart above, you can see how the company is priced using data from 2021 and 2022, as well as estimates for the 2023 fiscal year. So long as financial performance does not revert back to what it was in 2021, shares look attractively priced in my opinion. This is especially true on a forward basis. Using the data from 2022, I decided to compare the company to five similar firms. In the table below, you can see how this works out. On a price-to-earnings basis, two of the three companies ended up being cheaper than Schlumberger. Using the price to operating cash flow approach, I found out that our prospect was the cheapest of the group. And finally, using the EV to EBITDA approach, I found out that three of the five companies were cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Schlumberger Limited |

| 21.5 |

| 13.5 |

| 12.9 |

| Baker Hughes ( BKR ) |

| 89.8 |

| 15.3 |

| 25.3 |

| Halliburton ( HAL ) |

| 19.3 |

| 13.6 |

| 10.5 |

| Tenaris S.A. ( TS ) |

| 6.8 |

| 14.8 |

| 4.4 |

| NOV Inc. ( NOV ) |

| 47.9 |

| 30.7 |

| 13.1 |

| ChampionX ( CHX ) |

| 37.7 |

| 14.2 |

| 12.3 |

Takeaway

Leading up to earnings, I can understand why investors might be a bit cautious. Economic conditions are certainly questionable. Having said that, I think that Schlumberger will find itself in a good position. Revenue, profits, and cash flows are all likely to rise materially year over year. Although it is true that the stock looks more or less fairly valued compared to similar firms, I do think it looks affordable on an absolute basis. Due to these factors, I have no problem rating the company a ‘buy’ at this time to reflect my view that it should outperform the broader market for the foreseeable future.

For further details see:

Q1 2023 Earnings Preview: An Important Day For Schlumberger