UNBLF - Q2 Coverage Round-Up: Top Picks For Q3 And Beyond

2023-06-30 09:36:05 ET

Summary

- July is upon us: time for investors to evaluate mid-year portfolio performance and consider potential re-balances.

- Discussing investment results, my biggest winning and losing positions in Q2, and my ratings for various stocks as we enter a new quarter.

- Top Picks going into Q3: Eni, CVS Health, and Unibail Rodamco.

I want to give readers an overview of my quarter-to-date coverage with this final June article. As we enter the back half of the year, July 4 th and the summer holidays are upon us. Time to relax and enjoy some time off from work, but also take a step back, evaluate mid-year portfolio performance, and consider a re-balance.

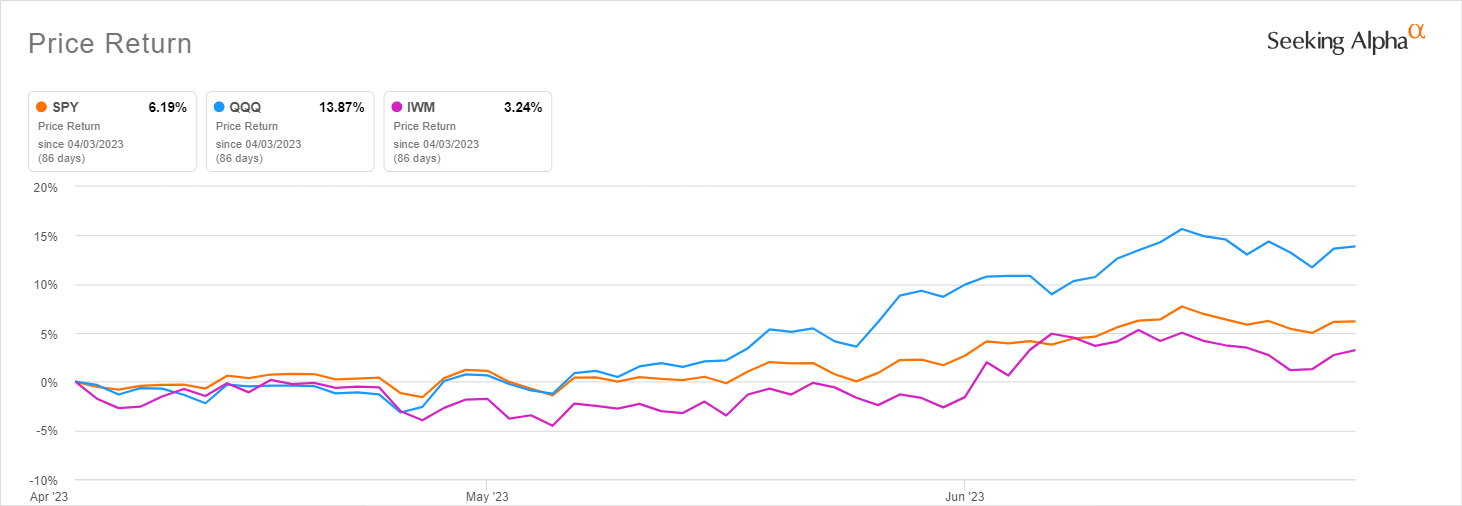

With most of the S&P500 YTD gains driven by a handful of mega-cap tech stocks, strategies that overperformed in 1Q23 continued to do well in the current quarter. Invesco's QQQ Trust ( QQQ ) is up by almost 14% in Q2, outperforming the S&P ( SPY ) by a wide margin and an even wider one of more than ten percentage points from the +3.2% for the Russell 2000 ( IWM ).

{kind=link}

Seeking Alpha

The results of companies like Apple ( AAPL ), up 51% for the year, might be driving the results, but such brilliant performance has nothing to do with top or bottom-line growth. I am not as excited as the general market by earning beats against lowered forecasts:

{kind=link}

Seeking Alpha

Stock gains are resulting in a rapid P/E ratio expansion, exacerbated by the negative YoY growth and against a macro outlook that is still deteriorating. The FED's record tightening cycle may have come to a halt in June, but it is too soon to imply that a pivot is coming next.

Against this backdrop, and with a personal performance much closer to IWM than the Nasdaq, I am undeterred in pursuing my current bucket strategy, which mixes global ETFs with DGI and High-Yield for individual stocks. I then have a "leftover" bin for top ideas that do not fit these two categories but with a limited allocation of up to 10% of total assets.

Winners and Losers

During the quarter, the biggest drag to portfolio performance was my short of Carvana ( CVNA ), which I shared with the community here . The timing on this one was as bad as it can get. The company reported marginally better profitability in 1Q23, and I expected the pop to be short-lived. However, debtholders' seem to continue accepting interest repayments with new principal instead of cash. The dissipating short-term liquidity risk allowed the company to kick the can further down the road on a new equity offering, triggering a short squeeze.

On a fundamental level, I still see Carvana as a doomed company. Positive adjusted EBITDA means nothing when interest payments exceed operating profits. Carvana will need debt relief sooner or later, which will only come at the expense of shareholders. At the same time, my failure was the inability to see that the market, for now, is unwilling to pull the plug on this one. Without a catalyst to the downside, the stock price was bound to recover due to the high short interest. I ate my losses at about $15 per share. Considering the subsequent price action, that seems to have been a wise decision, and for now, I do not see the right conditions to re-enter the short side of the trade.

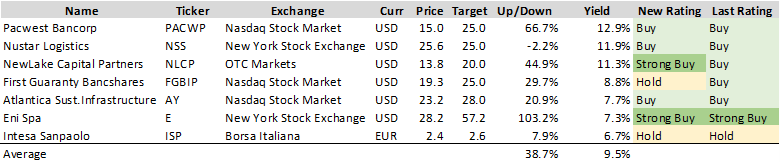

What worked well was, instead, my bullish view on PacWest ( PACW )( PACWP ), the beleaguered regional bank was caught in the perfect storm last March. Even with much-reduced profits going forward, I continue to see value in PacWest preferred shares. The bank should be able to continue covering its obligations. Even after a decent run-up from sub-$10, the shares still trade in the distressed range, yielding about 13%. Longer-term, the bull case is intact, and if the bank can clean up its balance sheet and reorganize towards community lending, I see chances for PACWP to recover towards par value. That means a 70% upside is still up for grabs while collecting the fat dividends. Regarding the ordinary shares, I suspect that part of the short crowd is in no rush to cover. A covered put option strategy could be profitable when viewing the upside as capped to TBVPS and high volatility persists.

Coverage into Q3

During the quarter, I shared several focused analyses on equities currently in my DGI and high-yield buckets. I also shared ideas on potential candidates that did not make the cut. Moving forward, I plan to gradually increase the stocks under continuous coverage to about 50-60 names, ideally evenly split between the DGI and the High Yield buckets. The article should serve the double purpose of providing readers with two lists of actionable ideas and a guidepost on whether the rating has changed from prior coverage on the ticker. For other stock ideas, such as special situations or deep value, there might or might not be a special-dedicated section as my coverage will likely be more sparse.

High Yield Bucket

Among high-yielding securities, seven focused analyses were published during the quarter. I have a current Buy/Strong Buy rating on five, including a Buy on renewables owner Atlantica Sustainable Infrastructure ( AY ) and NuStar Logistics baby bonds ( NSS ), and a Hold rating on the remaining two. In particular, I am downgrading my rating for First Guaranty Bancshares preferred shares ( FGBIP ) to Hold. While nothing is explicitly wrong with these shares that yield almost 9%, and I continue to own them, the risk/return profile for the other options seems better for new money. The problem is also that, back at the onset of viral market contagion across the regional banks, I expected the imbalance to self-correct, especially in the preferred shares space, within a short timeframe. This scenario, however, doesn't seem to be playing out as fast as expected.

{kind=link}

And Value For All

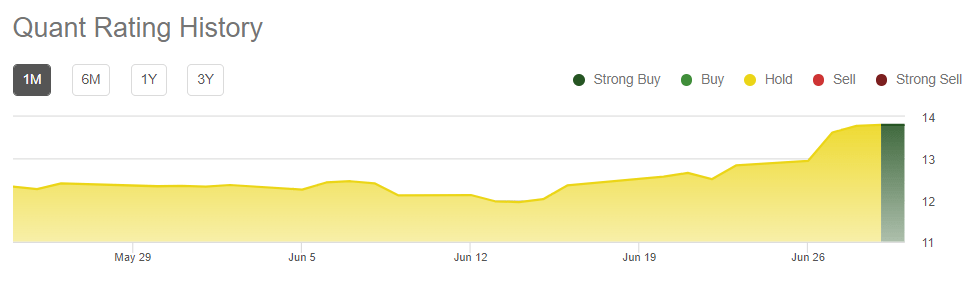

I am also moving to a Strong Buy rating on NewLake Capital Partners ( NLCP ) and expect to cover the stock with a new focused article in Q3, better detailing the reasons for my upgrade. The reason is also that technical indicators are improving rapidly. Readers can refer to Seeking Alpha Quant ratings, which have recently started to flash a double upgrade to Strong Buy:

{kind=link}

Seeking Alpha

DGI Bucket

I will strive to expand the coverage in the coming quarter, as there are currently only four names. I have more quality names in my DGI portfolio but have not written any analysis yet for the site, such as British Tobacco ( BTI ) and BlackRock ( BLK ). Of the four covered, I still have a Buy rating on three: CVS Health ( CVS ), Skyworks Solutions ( SWKS ), and Mid-America Apartment Communities ( MAA ), the same as when my focus analysis was released. I am not bullish on Leggett & Platt ( LEG ), and nothing has happened to materially alter any of these investment theses.

{kind=link}

And Value For All

CVS Health ((CVS)) offers the best risk/reward profile, primarily because of the considerable upside potential. Recently the stock re-tested its 52-week low but held, so the shares seem to have decent support at the current levels. While investors wait for the narrative to change, the stock provides a decent dividend and trades at ridiculously low multiples of 6x cash flow and 8x earnings.

Conclusion

Even with the NASDAQ continuing to surge in Q2 2023, I am sticking to my guns, diversifying exposure away from mega-cap tech stocks, to which most investors (including myself) are, in any case, highly exposed through passive funds.

My top pick in the high-yield space moving into Q3 is Eni ( E ), which could disproportionately benefit from rising oil prices driven by OPEC+ production cuts and steady demand. Eni is in great financial shape and poised to do well despite short-term macroeconomic weaknesses.

For DGI investors, I believe CVS Health is the most appealing prospect. Despite lacking a solid dividend growth track record (only 1-year growth), investors should focus on the future rather than historical data. I believe CVS will continue to increase its payout from now on.

A final special mention for a deep-value idea : shopping mall owner Unibail Rodamco ( URMCY )( UNBLF ) is worth a look. The thesis is simple: the company trades at half the valuation of its closest peers (despite equally worthy assets) because, in 2021, it decided to suspend dividends for three years and reduce leverage. We see the shares bound for a sharp re-rating, with an upside of 100%+, when Unibail finally reinstates its payout to shareholders by early 2024.

For further details see:

Q2 Coverage Round-Up: Top Picks For Q3 And Beyond