FTDS - Q3 2023 Global Market Outlook Update: Slowly Slowing

2023-06-28 03:20:00 ET

Summary

- Headline inflation has peaked in most regions. The biggest contributor is the decline in energy prices.

- Core inflation in Europe has largely been driven by the second-round effects of last year’s big increases in oil and gas prices.

- Megacap stocks are once again dominating the performance of the U.S. equity market. This time it is driven by excitement around generative artificial intelligence technologies such as ChatGPT.

- Malaise is the best description of the UK economy. GDP has barely grown over the past year and is still lower than before the pandemic in 2019.

- Domestic spending in Japan is starting to pick up, with the reopening gathering some steam and inbound tourism returning.

A character in Ernest Hemingway’s novel The Sun Also Rises , when asked how he went bankrupt, answers “gradually, then suddenly.” This is a good description of the U.S. economic outlook.

Forward-looking recession indicators such as the inverted yield curve, tighter bank lending standards , weak manufacturing activity and depressed consumer confidence readings are all flashing warning signs. Meanwhile, measures of real economic activity such as jobs growth and household spending are only gradually moderating.

Most of the other major economies are also slowing and at risk from aggressive central bank tightening. Growth in the eurozone is buckling under a steep decline in bank lending, and persistent inflation is forcing the Bank of England to tighten further despite the lack of UK economic growth.

China’s growth impulse is faltering following the post-pandemic lockdown surge. Japan remains an outlier, where monetary policy is still ultra-accommodative and gross domestic product ((GDP)) growth is likely to remain above trend.

This creeping slowdown in the United States seems likely to persist for a few more months. Households still have around $500 billion in excess savings built up during the pandemic, corporate profits are stabilizing, and housing indicators such as the National Association of Home Builders index have bounced off lows. Manufacturing output could receive a temporary boost as inventories are rebuilt from currently low levels.

The stresses from tight U.S. Federal Reserve (Fed) policy are apparent from the regional bank collapses earlier in the year and rising delinquency rates for credit cards and automobile loans. Standard and Poor’s reported that corporate bankruptcies for the year to May are the highest since 2010. 1

The uneven economic data means that a further Fed rate hike cannot be ruled out. We think the 500 basis points of tightening so far is enough to bring inflation back to target and significantly slow the economy. Further Fed tightening, in our view, will increase the risk of recession.

A recession in the United States seems probable over the next 12-18 months. The tipping point will likely come when corporate profit pressures force firms into austerity measures such as layoffs and capital expenditure delays, and households - having exhausted pandemic savings - respond by cutting back on discretionary spending.

The industry consensus, as surveyed by Reuters in June, has a recession starting in the final quarter of 2023. This is possible, but we suspect that the gradual and uneven pace of the downturn could delay the recession until sometime in 2024.

A later recession should be a milder recession for the simple reason that by 2024 inflation should have fallen by enough to allow the Fed to ease aggressively. A recession that starts in 2023 while inflation is still above the Fed’s target would limit the pace of easing.

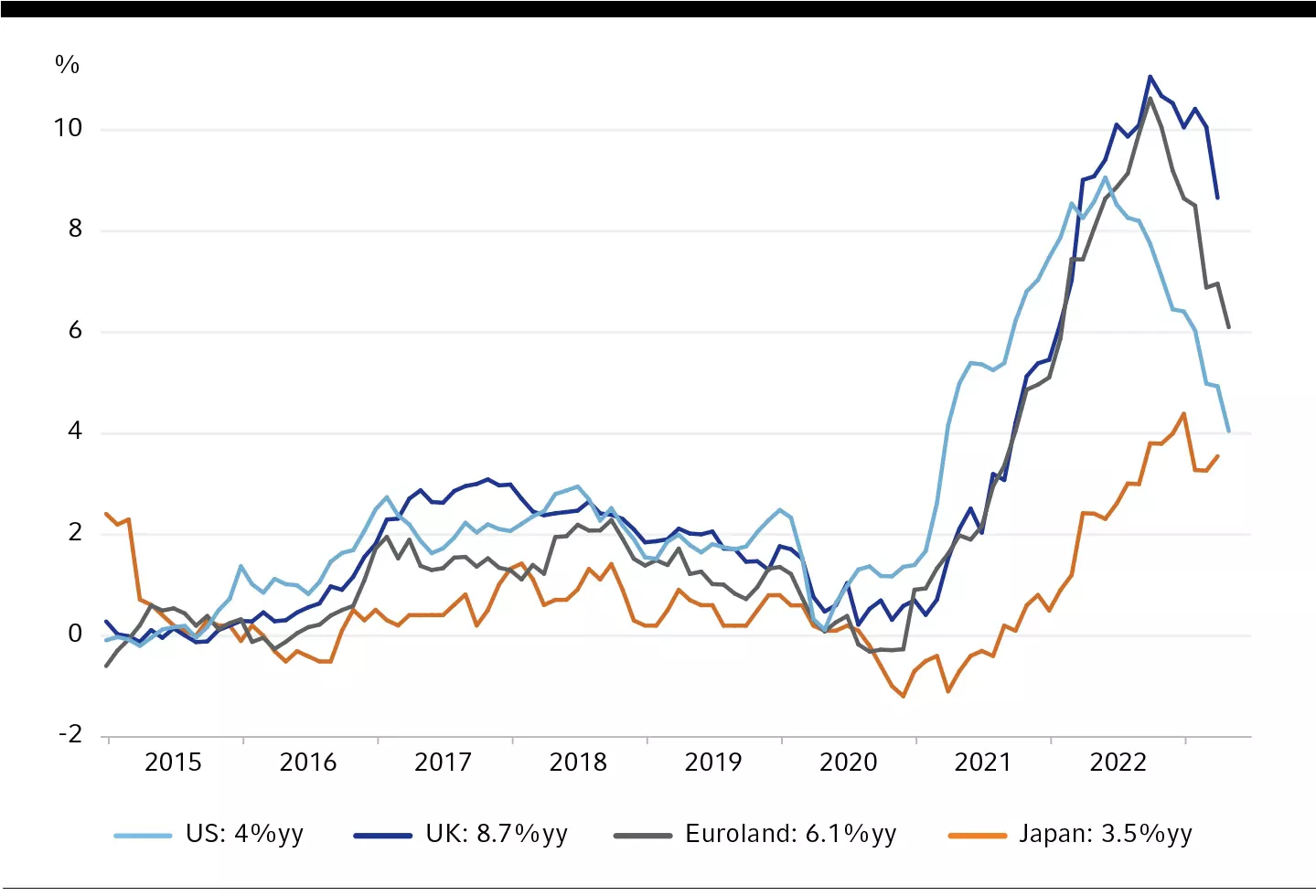

U.S. is leading the inflation decline

Headline inflation has peaked in most regions. The biggest contributor is the decline in energy prices, with oil prices down from $130 per barrel just after Russia’s invasion of Ukraine to $70 per barrel in mid-June.

Core inflation, which excludes food and energy, is proving stickier, but it has begun to turn lower in the United States. This trend should persist as supply bottlenecks clear and as rental and used car prices continue to normalize lower.

The main barrier to inflation returning to the Fed’s 2% target is the nearly 6% growth in wages . This is falling only gradually but should trend lower as the heat comes out of the labor market.

Core inflation in Europe has largely been driven by the second-round effects of last year’s big increases in oil and gas prices. Energy inflation has flipped from a high of 44% early last year to negative 2% in the 12 months to May 2023. We expect this should drive a significant decline in core inflation in coming months.

UK core inflation, however, is likely to lag the declines in the U.S. and Europe. Wages are still rising and the labor market remains tight due to falling participation rates and worker skills shortages resulting from Brexit.

The message from inflation trends is that the Fed is close to finished with rate hikes, and the European Central Bank (ECB) may soon be finished if, as we expect, core inflation starts trending lower. The Bank of England ((BOE)), however, has the most challenging task with core inflation yet to peak.

Futures markets have priced more than 100 basis points of further BOE tightening by early 2024. This may be an overestimate given that the overall economy is barely growing, but the BOE is likely to be the last major central bank to pause rate hikes.

Global Inflation Rates Have Peaked In Major Economies

{kind=link}

Source: Refinitiv® DataStream®, as of May 23, 2023. yy = year-over-year, which means comparing results from a time in one year to the same time in the prior year.

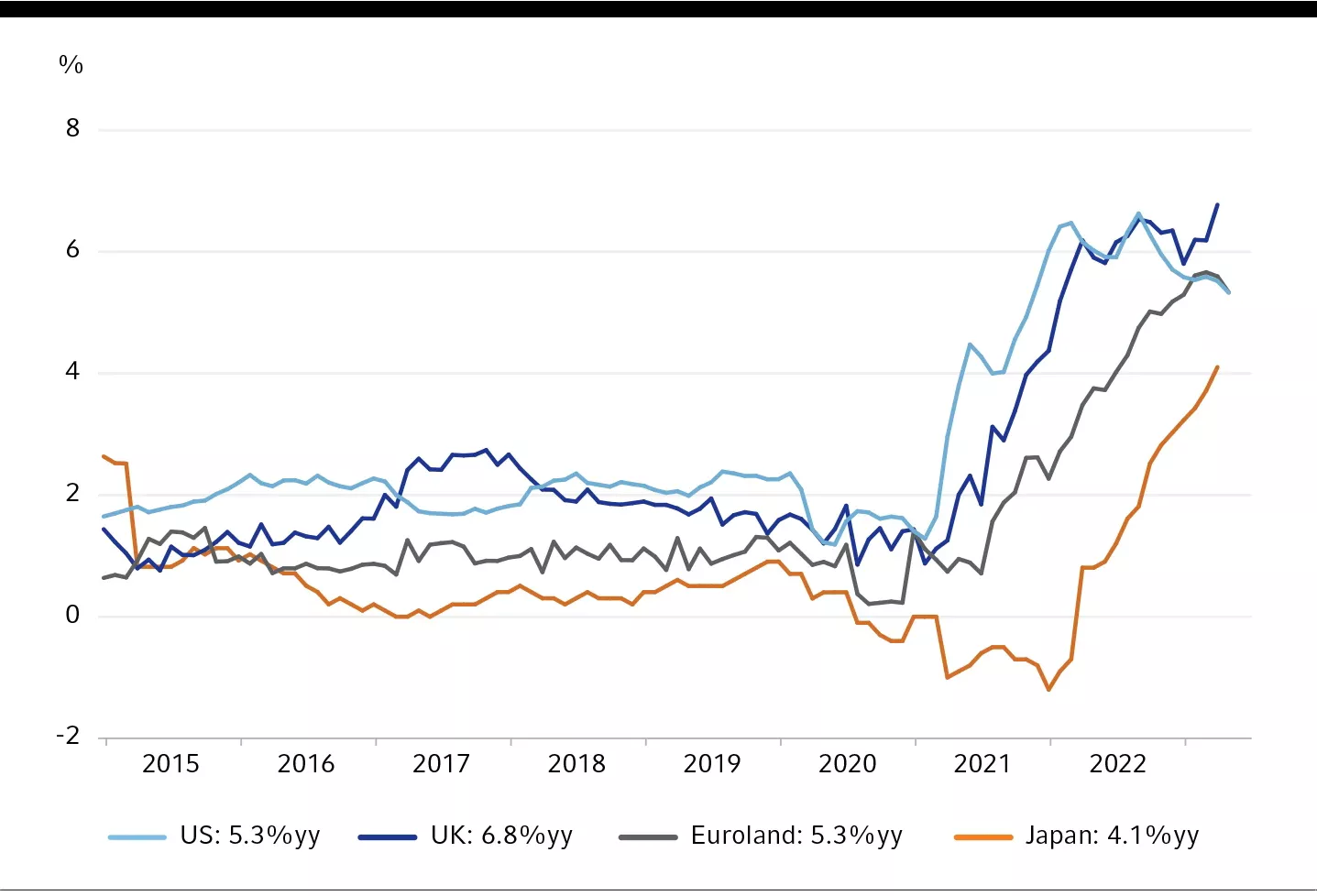

Global “Core” Inflation Rates Are Proving Stickier

{kind=link}

Source: Refinitiv® DataStream®, as of May 23, 2023.

AI excitement is building

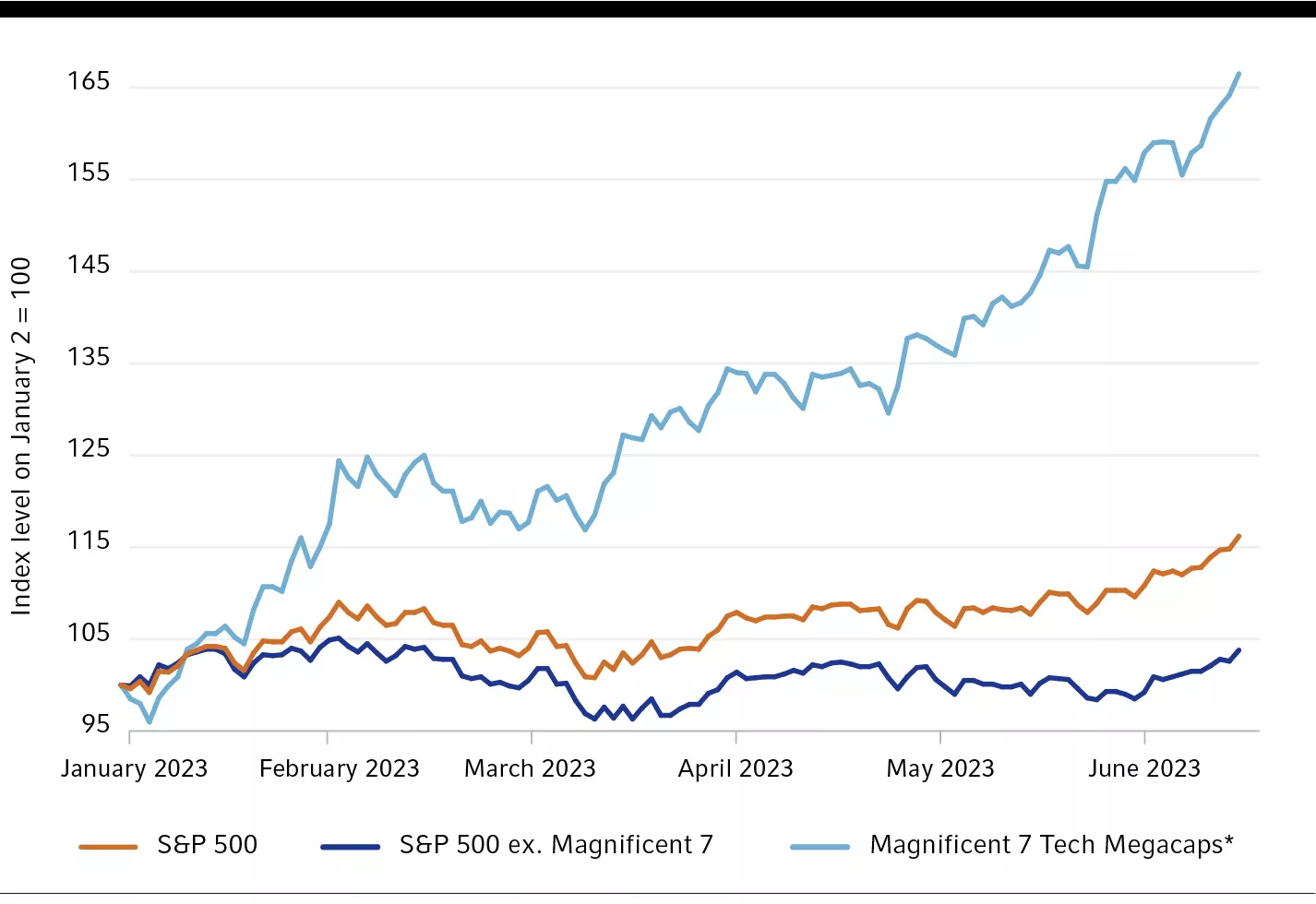

Megacap stocks are once again dominating the performance of the U.S. equity market . This time it is driven by excitement around generative artificial intelligence technologies such as ChatGPT.

The year-to-date return of the top seven technology stocks through June 15 has been 65%. Nvidia ( NVDA ) has posted a 190% return and Apple’s market capitalization now exceeds that of the entire small-cap Russell 2000® Index.

The S&P 500 has returned 16.2% so far this year. However, excluding the magnificent seven, the return has been just 3.8%.

ChatGPT’s release late last year triggered a wave of predictions about how transformative the new generative artificial intelligence technology will be. Goldman Sachs thinks AI could lift U.S. labor productiviy growth by 1.5% per annum over the next decade and boost corporate profit margins by 400 basis points.These forecasts are speculative, but it’s hard not to be excited by the potential of AI. The effects of AI could occur faster than in previous technological revolutions such as the introduction of electricity, roads and the internet. These previous episodes depended on scale and network effects to become transformative. Use of AI, by contrast, is increasing quickly and the effects on growth and productivity may occur in years rather than decades.Identifying the investment winners and losers from AI is not clear-cut. AI runs on computer processing power and data, so specialized chipmakers are likely to be beneficiaries, as well as companies that have access to large amounts of computing power, cloud storage and data.

There are also likely to be losers as existing technologies are rendered obsolete. Another issue is whether AI will produce the monopoly power and profits that the current tech giants enjoy from networking effects and scale economies. The gains may end up more evenly shared between the users and creators of AI. There is also the question of whether AI will turn into a speculative mania in the manner of the 1990s tech bubble. The gains for companies such as Nvidia and Meta this year can in part be explained by large increases in their earnings expectations.

Aggressive Fed tightening and the risk of recession are likely to keep the lid on AI euphoria for now. The return of low interest rates and easy money in the next cycle could be the trigger for an episode of speculative excess. AI is still in its infancy and will be one of the key investment themes to monitor going forward.

Technology mega-cap stocks have dominated u.s. Market returns

{kind=link}

Source: Refinitiv® DataStream®, Russell Investments' calculations, last observation as of June 15, 2023. *The Magnificent 7 is comprised of Apple, Meta Platforms, Alphabet (Google), Amazon, Tesla, Nvidia, and Microsoft.

Regional snapshots

United States

We are negative on the U.S. economic outlook. Restrictive monetary policy and weak leading economic indicators point to a slowdown. The Fed is nearing its peak for the federal funds rate after hiking by 5 percentage points over the past 14 months.

Policy is restrictive, the FOMC (Federal Open Market Committee) members are cognizant of the lags until the full impact of their past moves are felt, banks are tightening credit standards, and the Fed staff is forecasting a recession.It is possible that Chair Jerome Powell could still hike one or two more times this year. He has repeatedly emphasized that letting inflation become entrenched would be a bigger mistake than overtightening and causing a recession.

The Fed creates risk for markets when it is emphasizing high interest rates and seeking weaker economic growth to win its fight against inflation. The downgrade cycle in S&P 500 consensus earnings estimates bottomed out in April as stronger big bank results and mega cap tech fundamentals stabilized on cost cutting and expected artificial intelligence tailwinds.

U.S. earnings growth would likely fall 10 to 15% in a recession, creating downside risk to equity prices and Treasury yields as the Fed eventually lowers interest rates more aggressively than currently priced. Market psychology is optimistic - but not euphoric.

Our outlook for U.S. equity markets is cautious due to expensive valuations and a deteriorating business cycle. However, without evidence that investors have become fully euphoric, markets could potentially still melt higher in the near term.

Eurozone

After escaping recession over the winter, the outlook is turning more negative. Technically, it can be argued that the recession has already arrived, given that GDP growth was reported as negative in both Q4 2022 and Q1 2023. The labor market remains tight, with unemployment the lowest since the euro was established and the growth of wages accelerating.

The ECB does not think the region is in recession, as it lifted the deposit rate to 3.5% in June and signaled that another hike is likely in July. President Christine Lagarde has a constructive view on the outlook.

Our take is that the eurozone economy is starting to buckle under the strain of the monetary tightening so far. Lending growth has collapsed, and the credit impulse is the most negative since the 2007-08 financial crisis.

We also think that headline and core inflation are set to decline rapidly in coming months. Energy prices have an outsized impact on European inflation, and the energy Consumer Price Index ((CPI)) has fallen 1.8% over the past 12 months after surging 44% in the year to March 2022.

The fading recovery in China is another challenge for the eurozone. China is an important export market for the region’s industrial and luxury goods.

Near term, the continued hawkishness of the ECB is supportive for the euro, which is still cheap on a purchasing-power parity basis. However, the risk of a policy mistake by the ECB could put downward pressure on the currency over the medium term.

Eurozone equities have performed broadly in line with U.S. equities so far this year, but will soon face the cycle challenges of tight monetary policy and recession risk.

United Kingdom

Malaise is the best description of the UK economy. GDP has barely grown over the past year and is still lower than before the pandemic in 2019. Core inflation continues to move higher, hitting 6.8% in April. The unemployment rate has edged up slightly, but at 3.8% is still at levels last seen in the 1970s.

The combination of sluggish growth, rising inflation and a tight labor market points to an economy that is constrained on the supply side. The UK has had a smaller post-pandemic recovery in labor market participation than the U.S. or the eurozone.

Sickness and early retirement explain much of the labor-supply gap. Brexit has also had an impact in terms of skills mismatch, with European workers often not easily replaced.

The persistence of inflation has forced the Bank of England back to a hawkish stance. The base rate was lifted by 50 basis points to 5.0% in June and market expectations are for a peak of over 6% by early 2024.

We doubt that policy can be tightened that much without the economy buckling and look for a lower peak. Holders of popular two-year fixed-rate mortgages already face the prospect of refinancing from rates just over 1% in 2021 to near 6% currently.

A hawkish BOE should continue to support the British pound. Large-cap UK equities offer good value but could face headwinds due to their relatively large exposure to health, financials and consumer staples and small exposure to technology firms. UK gilts appear attractive with the 10-year yield at 4.4%.

Japan

Domestic spending in Japan is starting to pick up, with the reopening gathering some steam and inbound tourism returning. Wage growth continues to edge higher, and the stickier parts of inflation (i.e., services inflation) is approaching the Bank of Japan’s 2% inflation target.

The trade balance with the rest of the world is also improving, in part due to the decline in the oil price (Japan being a net oil importer), which should eventually reduce the pressure on the Japanese yen.

We expect that the Bank of Japan will amend its yield-curve control program by the end of the year, either by increasing the band around the 10-year target or changing the target tenure to a shorter date.

These dynamics should see a strengthening of the Japanese yen. The yen should benefit if global equity markets turn down and we enter a risk-off environment through the rest of the year.

China

The Chinese economy is decelerating after a strong first quarter. Consumption remains the key focus this year, and the data continues to indicate the Chinese consumer is cautious.

The excess savings in China are lower than in the developed world and are less likely to be spent, given these savings were accumulated without the support of fiscal stimulus.

Chinese property developers continue to see elevated credit spreads, and the recovery in the property market has been slow. There has been a bit of additional stimulus provided for electric vehicles, and we expect there will be more stimulus before the year ends (particularly for the property sector).

Monetary policy is likely to remain very accommodative, given inflation in China is currently running below 1% year-on-year. We maintain our view that 2023 GDP growth is likely to be around 5%.

The Chinese yuan is unlikely to strengthen until we see signs that the Federal Reserve and other developed central banks are close to cutting interest rates. Chinese equities look relatively cheap and have given back a significant amount of the gains since the government lifted pandemic restrictions.

Canada

A historic surge in immigration has supported consumption and overall economic growth and played a crucial role in stabilizing housing. This helped prompt the Bank of Canada (BoC) to hike its target rate in June after being on a conditional pause for most of the year.

Market probabilities indicate that one more rate hike is possible, raising the target rate to 5.0%, double its estimated neutral rate of 2.5%. A 5% policy rate is very restrictive, and despite recent housing developments, households are vulnerable if rates stay elevated.

Insolvencies, credit card balances, and usage of home equity lines are rising. These indicate that stress is mounting. Meanwhile, the labor market is loosening. The Canadian economy lost jobs in May, the first time since August 2022, and job vacancies have declined.

Weakening employment trends will eventually weigh on housing and consumer behavior and put downward pressure on inflation. We think a recession is the likely outcome over the next 12 months.

However, the BoC may be patient, and wait for confirmation that the economy is no longer operating in excess demand and that inflation is trending lower sustainably before easing monetary policy.

Australia/New Zealand

The Australian economy continues to slow, but the probability of a recession remains lower than for countries in the Northern Hemisphere. Immigration levels are high, which will support economic activity.

However, the increase in interest rates and the expiration of many fixed-rate mortgages over the last three months will further slow household spending. The labor market is very tight but should ease through this year as forward-looking indicators of labor demand are softening and labor supply is increasing.

The Reserve Bank of Australia has indicated that further interest rate increases may be required, given concerns about sticky inflation and very weak productivity (which increases unit labor costs). We think the Australian dollar has upside given our expectations of better economic growth and narrowing interest rate differentials.

New Zealand will experience a significant tightening of household finances, as many fixed-rate mortgages reset to much higher rates following the Reserve Bank of New Zealand’s (RBNZ) aggressive tightening. We think that recession risk in New Zealand is higher than for Australia.

The recent budget provides some support, with the fiscal impulse for 2024 larger than most economists had expected. Similarly, a pick-up in net migration is helpful, although it is a smaller impulse relative to Australia.

After lifting rates by more than most developed central banks, the RBNZ has pulled back its guidance on the need for future rate hikes. We expect its hiking cycle is now over.

Another consideration is the general election in October. Opinion polls have tightened at mid-year, and the incumbent Labour party has regained the lead.

Asset-class preferences

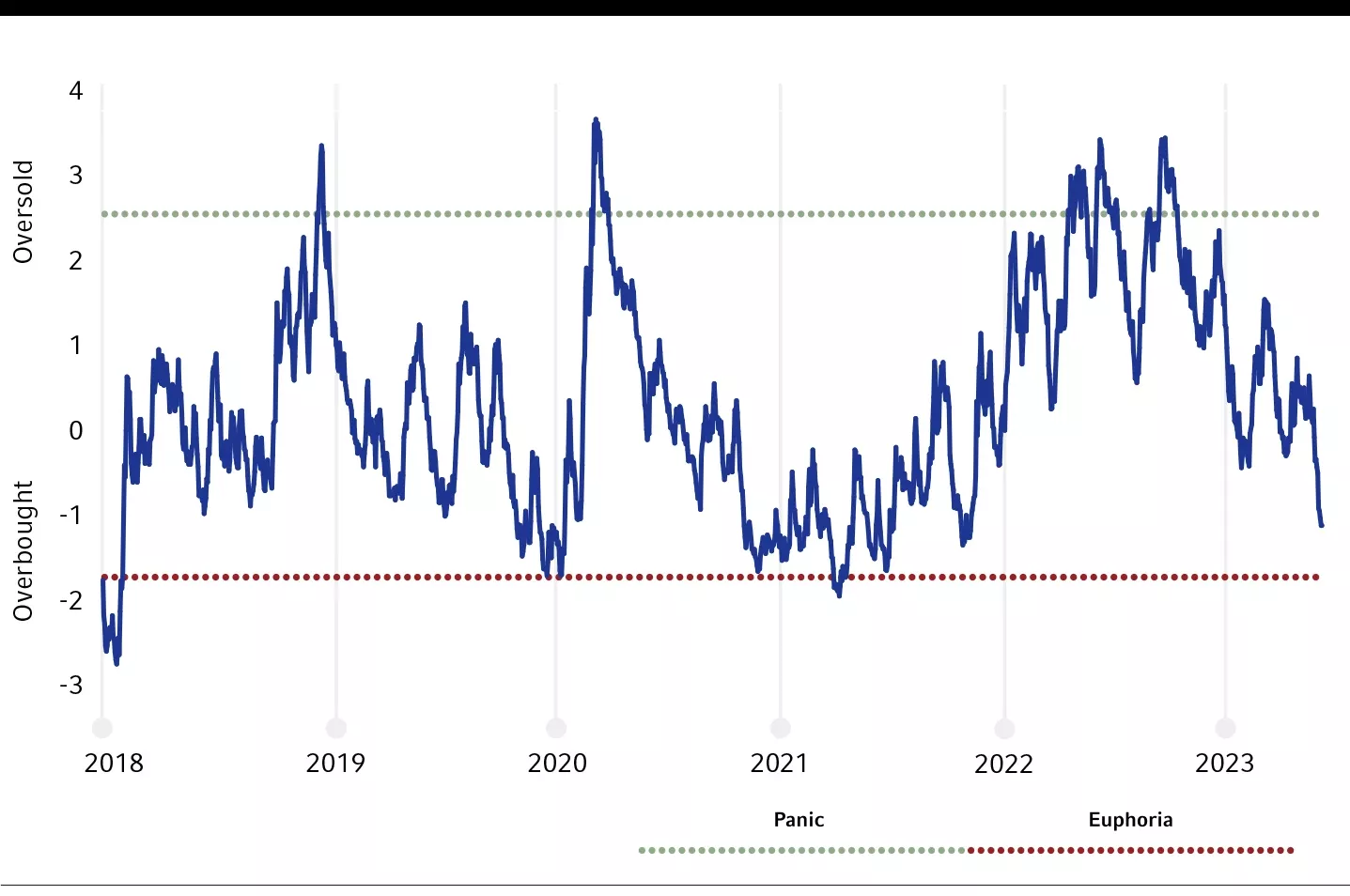

The gradual and uneven slowdown in the United States creates a complicated environment for financial markets. Our cycle, value and sentiment framework is cautious on the one-year ahead outlook for the S&P 500.

Valuation is expensive and the cycle is a headwind based on our view of recession risks. Our proprietary sentiment index is now slightly overbought after being oversold at the beginning of the year.

Markets, however, could melt upward over the next few months if investors begin to speculate (wrongly, in our view) that the resilience in the economic data suggests that a recession might be avoided.

Another complicating factor is the growing enthusiasm for stocks linked to artificial intelligence ((AI)). Almost all the S&P 500 gains so far this year have been delivered by stocks linked to AI.

This narrow leadership creates a risk that the gains could be quickly unwound if recession fears prick the AI hype. But there is also the possibility that investor appetite for AI-themed vehicles offsets cycle headwinds. On balance, we expect the cycle pressures to create downside equity risks, but AI mania is difficult to predict.

Our CVS framework provides us with a positive outlook for U.S. government bonds. 10-year yields near 3.8% are good value, recession risks provide cycle support and contrarian sentiment is also supportive with futures data showing that most speculative investors are positioned for yields to rise further. Bonds provide strong diversification potential for portfolios.

Composite contrarian indicator: Investor sentiment appears directionally overbought, but not yet euphoric

{kind=link}

Source: Russell Investments. Last observation is -1.23 Standard Deviations, as of June 14, 2023. The Composite Contrarian Indicator for investor sentiment is measured in standard deviations above or below a neutral level. Positive numeric scores correspond to signs of investor pessimism, while negative numeric scores correspond to signs of investor optimism.

Specifically, we have the following assessments at mid-year 2023:

- Equities have limited upside with recession risk on the horizon. Although non-U.S. developed equities are cheaper than U.S. equities, we have a neutral preference until the Fed become less hawkish and the U.S. dollar weakens significantly.

- Within equities, we prefer the quality factor, which tracks stocks that have low debt and stable earnings growth. These stocks typically show good relative performance during periods of economic slowdown. Quality stocks are relatively cheap at mid-year compared to the rest of the market.

- Emerging market ((EM)) equities have underperformed developed markets so far this year. This has been despite the weaker U.S. dollar, which usually is a trigger for EM to outperform. Concerns about China’s economy have been a headwind, and these worries seem unlikely to lift over the near term. For now, a neutral stance is warranted.

- High yield spreads are below their long-term average and investment grade credit spreads are close to their long-term averages. The poor cycle outlook is a challenge with default rates rising as U.S. recession probabilities increase.

- Government bond valuations look increasingly attractive. U.S., UK and German bonds offer reasonable value. Japanese bonds, however, are still expensive with the Bank of Japan holding to the 50-basis point yield limit. It is likely that the U.S. yield curve can steepen in coming months. The spread between 2-year and 10-year bond yields is close to an extreme. The yield curve tends to steepen after the Fed has completed raising interest rates and markets start looking toward monetary easing.

- Real assets: REITs (real-estate investment trusts) continue to have more attractive valuations relative to infrastructure and global equities. REITs should perform well when interest rates fall, given that real estate fundamentals appear reasonably healthy. Commodities face headwinds from the lackluster Chinese economy, particularly the poor outlook for infrastructure and construction activity. Oil prices have failed to rise following successive announcements of supply cuts by petroleum-exporting countries, and prices are unlikely to recover as global growth continues to slow. The supports for gold prices are unwinding as inflation declines and real interest rates increase.

- The U.S. dollar ((USD)) has trended lower over the past month as investors speculate the Fed is nearing the end of rate hikes. It could weaken further if markets become confident that a recession can be avoided, given the counter-cyclical nature of the dollar. The Japanese yen is attractive from a cycle, value, and sentiment perspective. At 142 versus the USD, it is significantly undervalued relative to its purchasing power parity valuation of 92. Japanese inflation pressures mean the Bank of Japan is set to eventually move away from its yield curve control monetary policy. Positioning data show that many investors expect further yen weakness.

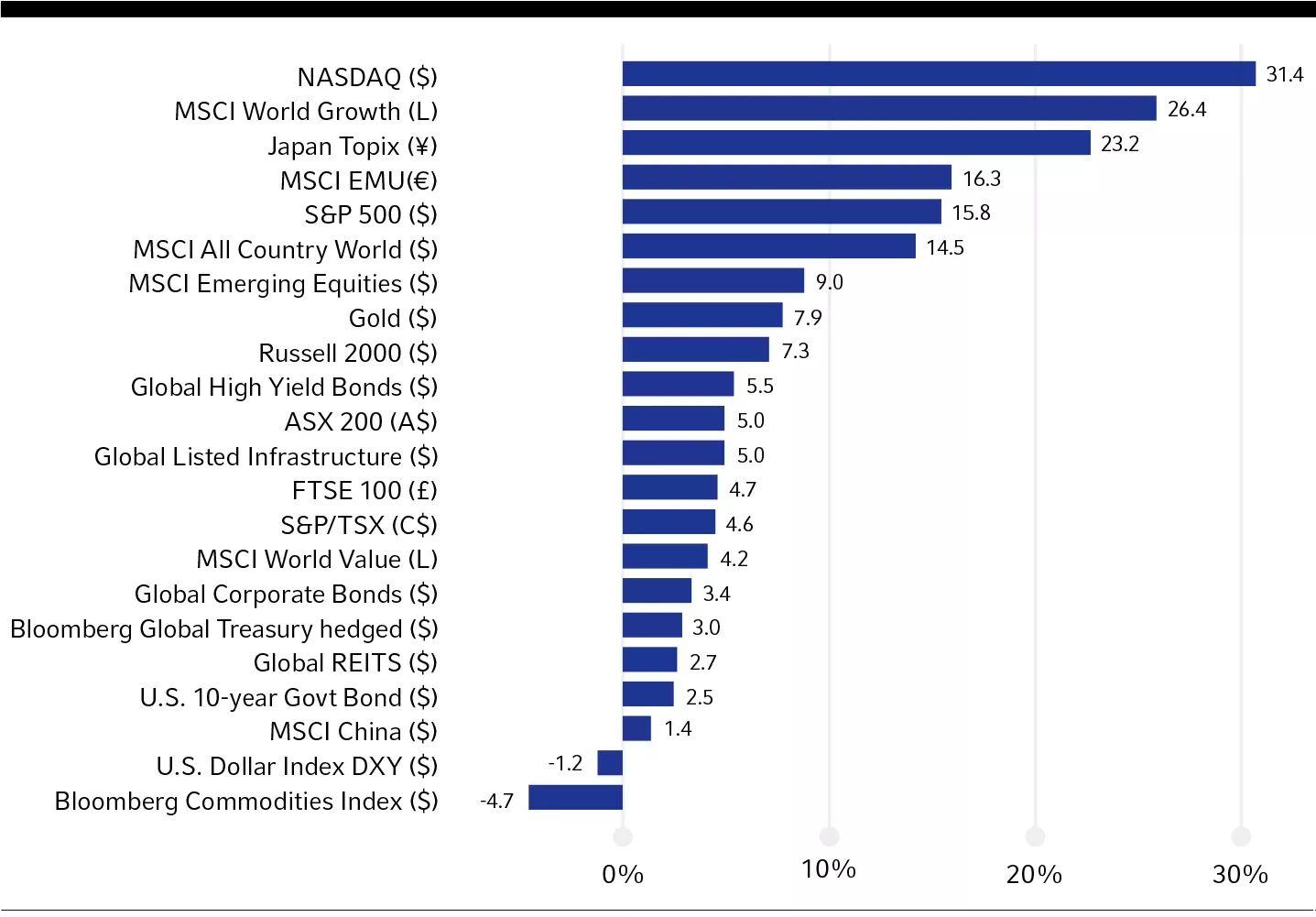

Asset Performance Since The Beginning Of 2023

{kind=link}

Source: Refinitiv® DataStream®, as of June 16, 2023. EMU = European Economic and Monetary Union.

1 US corporate bankruptcies tick up in May; year-to-date total highest since 2010

Disclosures

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. The information, analysis, and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

This material is not an offer, solicitation or recommendation to purchase any security.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment. The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

The information, analysis and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual entity.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the "FTSE RUSSELL" brand.

The Russell logo is a trademark and service mark of Russell Investments.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an "as is" basis without warranty.

The views in this Global Market Outlook report are subject to change at any time based upon market or other conditions and are current as of June 26, 2023. While all material is deemed to be reliable, accuracy and completeness cannot be guaranteed.

2023 Global Market Outlook - Q3 update

UNI-12254

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Q3 2023 Global Market Outlook Update: Slowly Slowing