DE - Q3 Earnings Torpedoed CNH Industrial: Time To Buy

2023-11-09 09:53:25 ET

Summary

- CNH Industrial's stock dropped by as much as 12% following its Q3 earnings report, presenting a potential investment opportunity.

- The company's financials showed a decrease in net sales and a margin deterioration, leading to a lowering of its financial guidance.

- Investors may want to buy the dip and position themselves for the next equipment replacement cycle.

Introduction

My best investments so far have been the ones where a quality stock suddenly dropped due to temporary concerns. Well, I believe CNH Industrial ( CNHI ) offers us such an opportunity after it dropped as much as 12% following its Q3 earnings .

Summary of Previous Coverage

All year long, agricultural and farming machinery stocks have underperformed the market due to several indicators showing the peak of the current cycle.

While I believe this is true and, as we will see in a moment, it obtains confirmation from what CNH Industrial just released, I also think we should not overlook some structural tailwinds the industry will benefit from as time goes by.

In particular, I want to recall the three main trends I pointed out when I initiated my coverage of the stock: increasing world population, scarcity of arable land, scarcity of skilled labor force.

This paints the picture for a growing need for food coupled with more productive technologies that increase acre output and substitute, partially or totally, skilled workers. In other words, the need for precision agriculture machinery and autonomous solutions will be growing in the next decade.

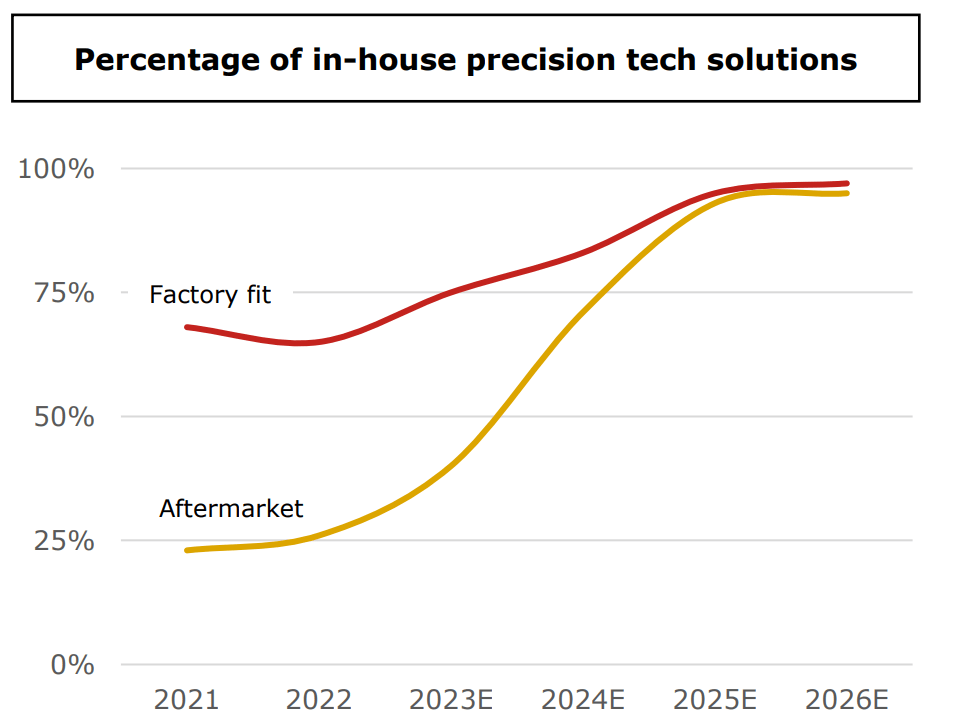

CNH Industrial, thanks to the Raven acquisition, is moving quickly to increase its in-house precision tech solutions, as shown below.

{kind=link}

CNH Industrial was my industry pick in 2022 because of a simple reason. Leaving aside the benefit from having spun-off Iveco ( IVCGF ), its on-highway business, I thought last year's environment was the right one for those companies that usually are the second largest leader in their industry. The reasoning behind this was rather simple and we can summarize it in this way: with a surge in machinery demand, the industry leader - Deere ( DE ), in this case - could not fulfill all of it in a reasonable time. This leads customers who are in a hurry and need new equipment to turn to the second available option. Therefore, I forecasted an outflow of demand from Deere's bucket into CNH Industrial's and AGCO's ( AGCO ). However, I thought CNH Industrial would perform a bit better than AGCO because it was starting from a better operating efficiency. While AGCO just recently reached double-digit margins, CNH Industrial was faster at taking advantage of last year's situation and sped up its margin growth . In particular, it took advantage of its larger penetration of North America compared to AGCO.

As 2023 kicked in, I started expecting a more normalized market, and I thus started taking advantage of weakness in the industry to introduce Deere into my portfolio . This was because, once this cycle settles and we start preparing for the next one, I want to own the industry leader and its premium products which lead to premium prices and margins. In August, I also picked up some more shares of CNH Industrial because of its interesting valuation.

Q3 Earnings

Let's get to the point of this article. The third-quarter report swept through the stock like a raging tornado. It's not often we see a 12% drop in one day on a well-established and profitable company. Let's see what happened.

First of all, the report started with a warning sign. Before it even highlighted its main financials, CNH Industrial pointed out that they operated "amid softer demand in certain product categories and South America". Not a good sign.

The second concern comes from the fifth point of the report, where the company announced an "immediate restructuring program to be followed by a thorough review of SG&A cost structure". In other words: the company is worried its margins won't hold up. Again, not a confidence-inspiring statement.

The main highlights are as follows:

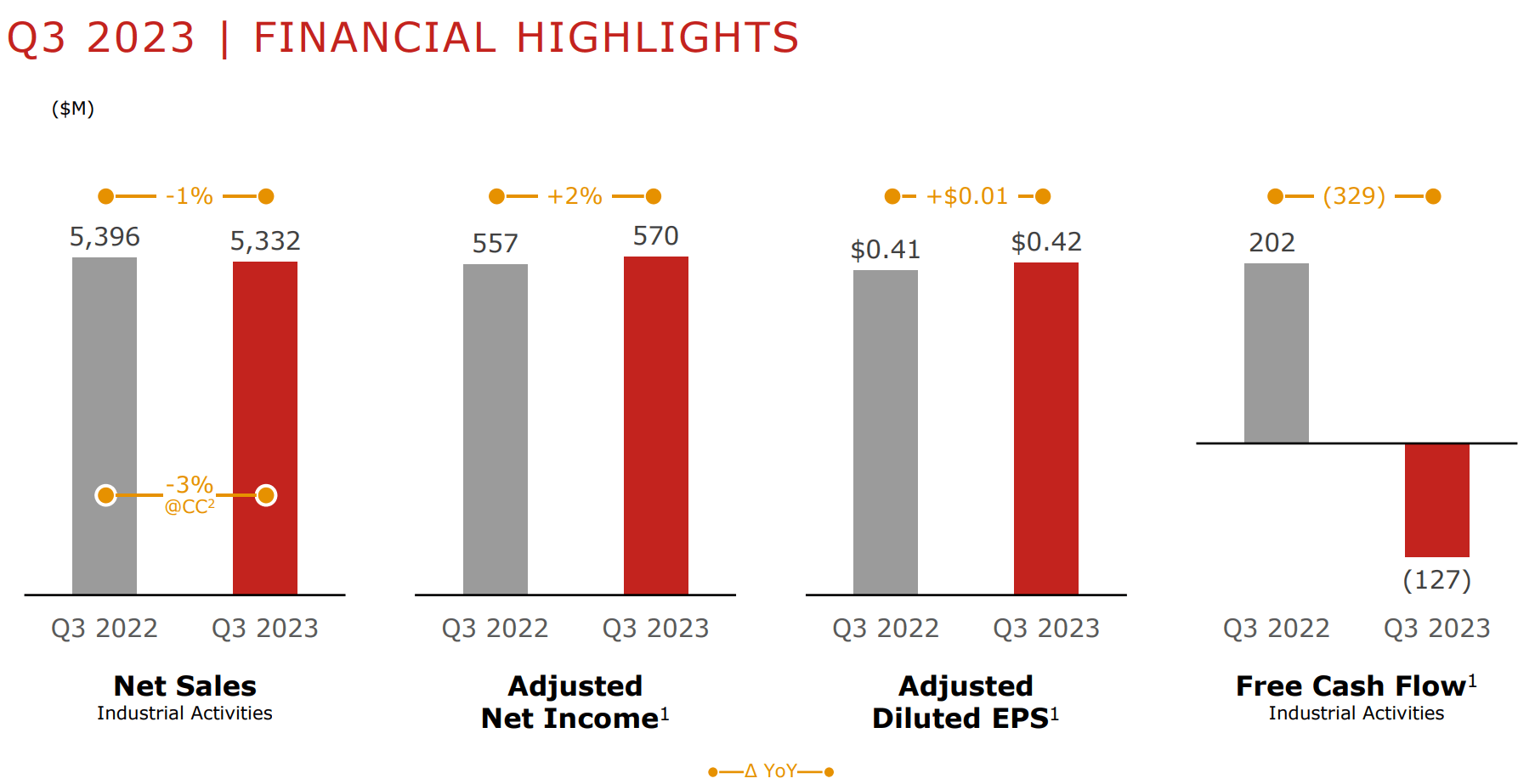

- Consolidated revenue of $6 billion (+2%) with net sales from industrial activities down 1% to $5.3 billion. This is a miss by $220 million.

- Adj. EBIT of industrial activities down 2% YoY to $657 million, with a margin deterioration of 10 bps to 12.3%.

- Net income up 2% to $570 million.

- Diluted EPS of $0.42 up $0.01 YoY, which is a slight miss of just $0.01 compared to analysts' forecasts.

- Free cash flow shows a positive increase to $202 million.

{kind=link}

As far as this increase in cash flow goes, we should not be deceived. Towards the end of the cycle, unfinished products decrease as they are delivered to customers and the company sees a reduction in accounts receivables, which means customers owe less money to the company because they have paid for their vehicles. In Q3 2022, the change in accounts receivables was -$316 million, now it is -$222 million. This creates a $100 million increase in cash from operations. At the same time, this is balanced by an increase in accounts payable because suppliers are going to be paid soon. The real difference comes then from the change in other net operating assets, which is the difference between the operating assets of the company and its operating liabilities. In this quarter this item reports $256 million vs. -$53 million in Q3 2022. Out of the $329 million increase in FCF, $309 came from this.

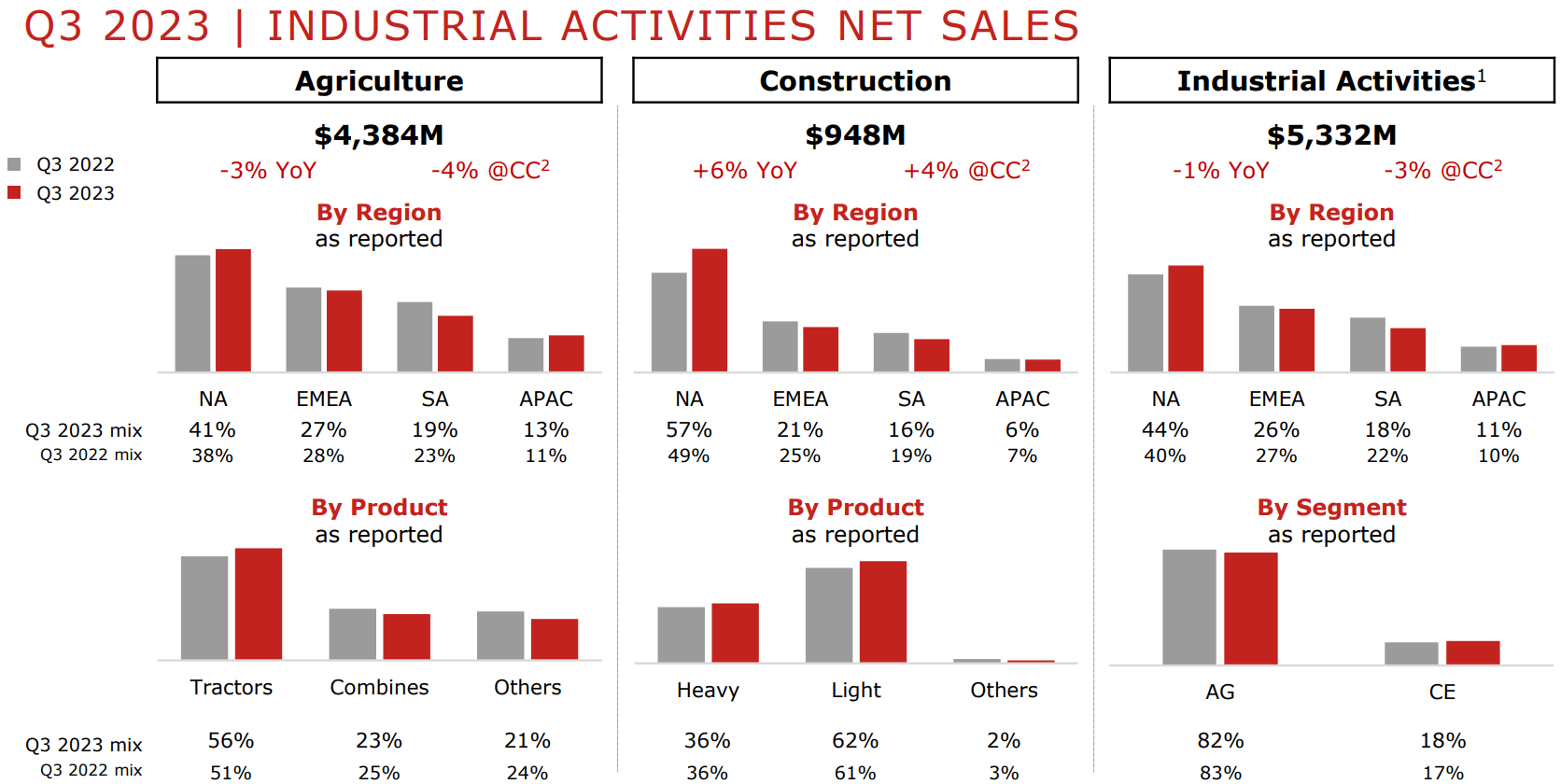

Now, let's move back to the top line and look at net sales of industrial activities. North America is still holding up and it has increased its weight on the overall mix (41% in this recent quarter). This, per se, is not bad news, since the continent is the one where CNH Industrial enjoys its highest margins. However, what is more concerning is the environment in South America, where government spending has slowed down (especially in Brazil), hitting one of CNH Industrial's largest markets.

{kind=link}

As many may know, CNH Industrial has two main branches: agriculture and construction. The former is 4x the size of the latter and it has the higher margins, too. However, CNH Industrial has committed itself to growing its construction business and making it a lucrative branch, too. As we can see, construction did grow more than agriculture across its different products, with the North American region still showing strength.

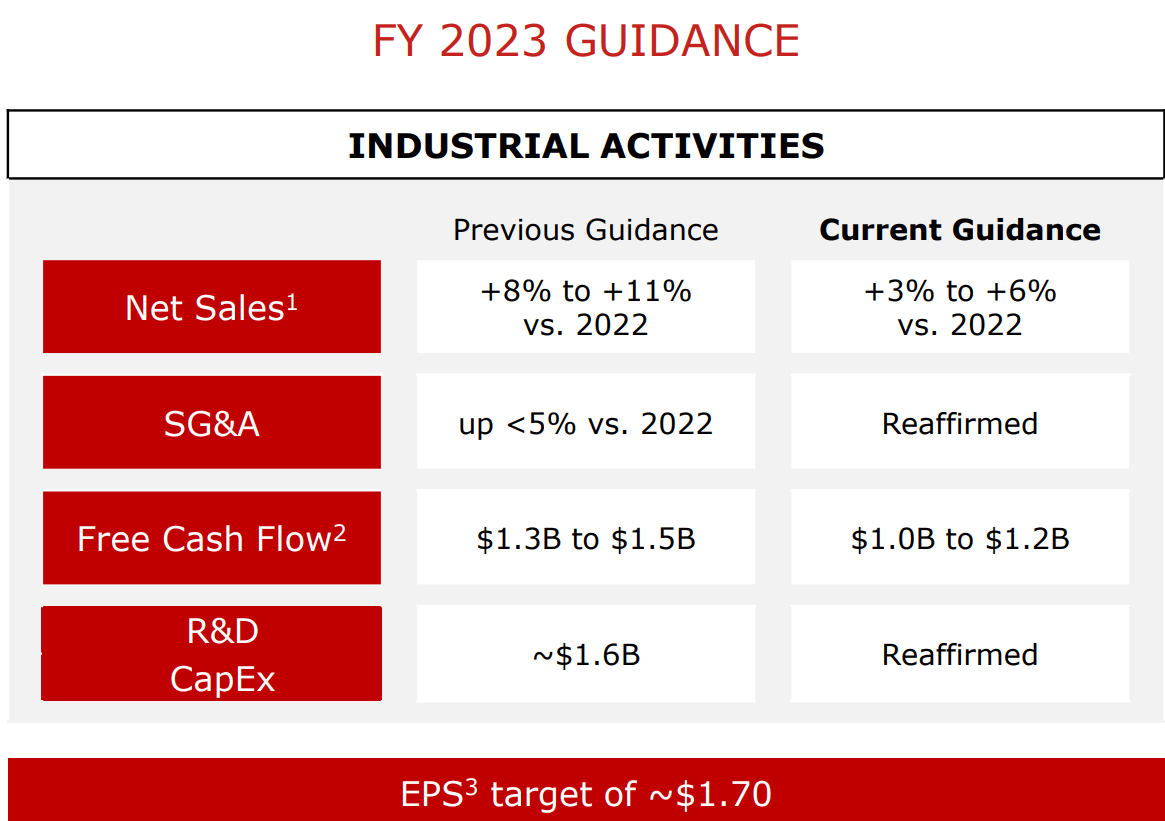

What actually concerned investors was when CNH Industrial updated its financial guidance, lowering it as follows:

{kind=link}

As we can see, net sales are now expected to grow at a moderate pace between 3% and 6%, while just a few months ago the company's guidance forecasted net sales growth between 8% and 11%.

This is why Scott Wine, the company's CEO, announced CNH Industrial is initiating an immediate restructuring program "to achieve a 5% reduction in salaried workforce cost to be substantially completed by year end".

In fact, Oddone Incisa, CFO of CNH Industrial, had to disclose that "as demand slowed, we produced around 20% fewer low horsepower tractors [...] while on our high horsepower tractors, production was up 13%". Small ag is the first to slow down because small tractors are easier to build and to deliver. Large ag equipment takes longer to build. But, eventually, large ag will see the impact of decreasing economic conditions. The company thus has to brace itself for impact.

However, though this news is not pleasant, we must also consider how they were, in a certain way, warranted and expected. The cycle must come to a close and a new cycle needs to be prepared. Usually, cycle after cycle, CNH Industrial has come out stronger and larger. Therefore, this could be the right time to start a position and take advantage of weak data coming in every day.

Milan Exchange Delisting

CNH Industrial also disclosed that its delisting from the Milan stock exchange has been approved and will be effective from January 2, 2024. This will make CNH Industrial a stock traded only in New York. This means CNH's common shares will continue to be listed on Milan until December 29, 2023.

The single listing should actually increase liquidity for the stock and streamline financial reporting. Moreover, CNH Industrial was added to the Russell 1000 in June, another positive fact for the stock.

Together with the delisting announcement, CNH Industrial also approved a new share buyback program under which the company will repurchase up to $1 billion worth of its common shares between November 8, 2023 and March 1, 2024. This program should assist with volatility arising from the delisting. The program will involve share repurchases up to €400M to be executed in Milan by year-end, while the remaining funds will be used to execute the program on the NYSE.

This program alone is worth around 7.4% of CNH Industrial's current market cap and this proves how meaningful it should be.

In addition, such a massive program shows how CNH Industrial's management is confident the company now trades below intrinsic value, as Mr. Wine said during the last earnings call .

Now, even though the company has not talked about this, I am inclined to think that, once the company will be listed only on the NYSE, it will soon thereafter change its dividend policy, shifting from an annual dividend to a quarterly one, in line with North American standards. This could make the stock even more appealing for investors.

Valuation

Looking at CNH Industrial's valuation metrics on SA, we immediately spot how this stock doesn't have high expectations baked in. Its current valuation grade is a B, with a fwd PE of 5.8 graded with an A+, a fwd EV/EBIT of 12.6 graded with a B and a fwd P/FCF of 6.1 graded with an A-. In every case, we are talking about a discount to the sector average of 62% considering its PE ratio, a discount of 15% considering the EV/EBIT ratio, and a 51% discount from the perspective of the P/FCF ratio.

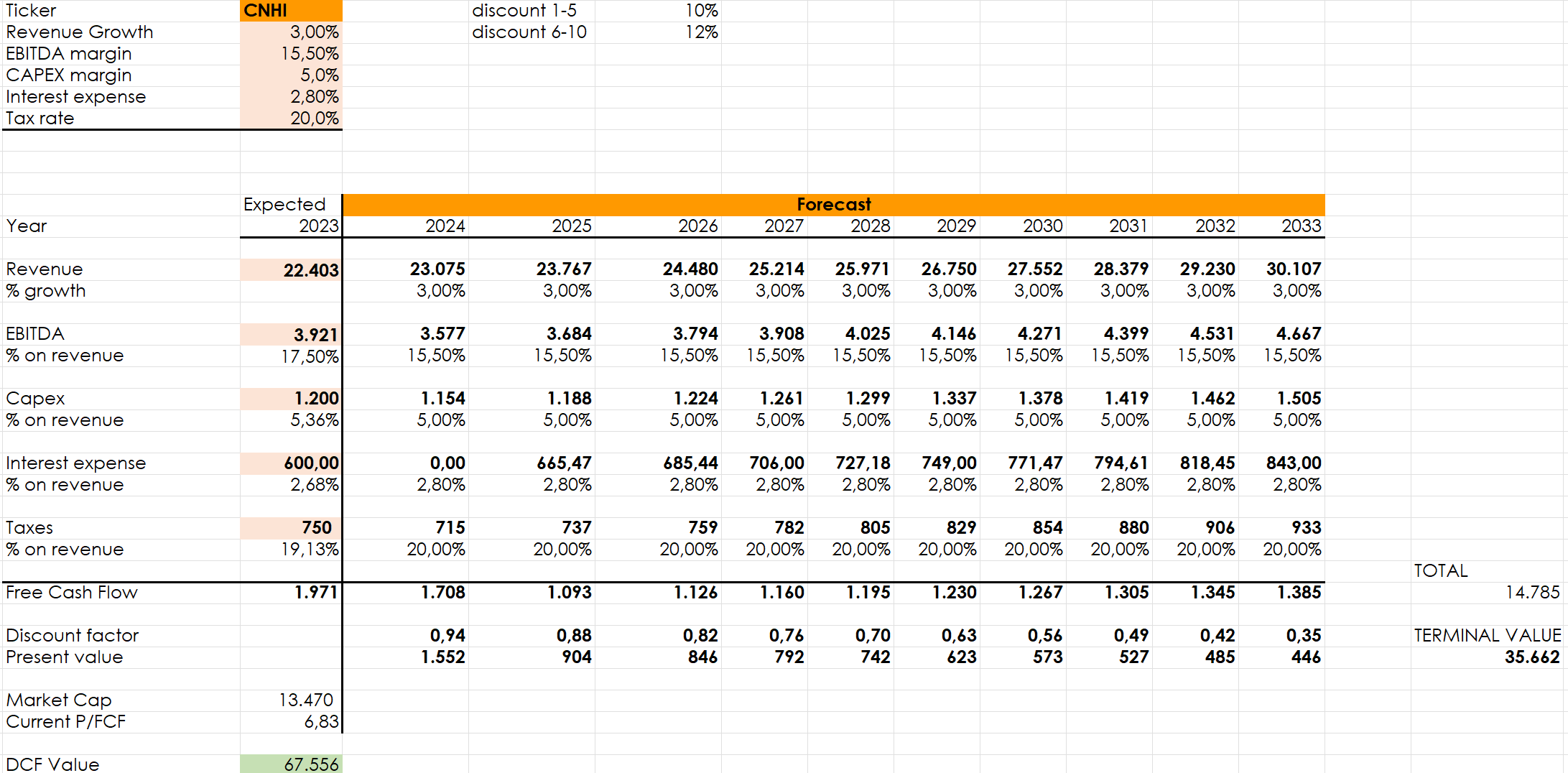

If I run some numbers in my discounted cash flow model, even though I significantly discount future cash flows, I still get the stock is highly undervalued. Expecting an average revenue growth around 3% for the next 10 years and an EBITDA margin of 15.50%, if I discount CNH Industrial's future expected cash flows by 10% for the first five years and by 12% for the next five years, I get a present value of total cash flows of $67 billion, while the stock is currently trading at a market cap of $13.5 billion.

One can be as conservative as possible and cut this valuation in half, but it would still show we are looking at a nice opportunity with plenty of upside.

{kind=link}

The discount is here. However, what can make us help decide whether to invest or not in CNH Industrial? First of all, one has to be bullish on the industry. Secondly, one has to be confident about the direction the company is going and how its management is leading the company towards its goals.

I personally think the company is undergoing temporary turmoil which is quite normal during its cycles. However, I think it has been executing well, quarter after quarter, taking advantage of extreme market conditions. And I also think the company could be close to a price where a double becomes more and more likely. This is why I rate the stock as a strong buy.

For further details see:

Q3 Earnings Torpedoed CNH Industrial: Time To Buy