QABSY - Qantas Airways Stock Is Taking Off: Massive Potential For Long-Term Growth

Summary

- Qantas Airways is recovering nicely from the COVID slump.

- The stock is deeply undervalued, leaving plenty of room for stock growth.

- Qantas is likely to experience strong multi-year growth as travel demand increases.

In my continuing quest to find stocks with strong long-term growth potential, I came upon Qantas Airways ( QABSY ). Qantas Airways operates as the largest domestic and international airline in Australia with a fleet of 322 aircraft as of the end of FY22 . The company's low valuation and strong expected growth has the potential to drive the stock for above-average gains over multiple years.

Like other airlines, Qantas experienced a rough patch during the COVID pandemic that significantly suppressed air travel. However, the company has been recovering in FY23 and is currently seeing increased demand for travel. This is a positive catalyst that can drive growth for Qantas for the foreseeable future.

Air Travel Outlook in Australia

Air Service Australia (the country's air traffic management) expects domestic air travel in Australia to recover to pre-pandemic levels by the second half of 2023. However, international travel is expected to take longer as significant increases in fuel prices and travel prices for longer trips have reduced demand.

One key point regarding tourism in Australia is the re-opening of China. Prior to the COVID pandemic, China arrivals were the largest group of inbound travelers into Australia before COVID. This includes many students from China. The relaxing of China's COVID restrictions can be a strong catalyst in 2023 and beyond. It is expected to take months for the amount of China to Australia travelers to return to pre-pandemic levels. This gradual increase in travelers should provide a steady increase in growth for Qantas.

Qantas is forecasting a strong international recovery through mid-2023. Qantas expects international capacity to increase to 82% of 2019 levels by the company's fiscal Q4 which begins in April 2023. The recovery is being supported by the return of Qantas' Airbus A-380s from storage and heavy maintenance and the delivery of Boeing 787-9 aircraft.

Given the steady increases in travel domestically and internationally, Qantas is likely to achieve strong growth in FY23 and FY24 as the airline returns to pre-pandemic levels.

Low, Attractive Valuation

Qantas trades with a deep, low valuation with a forward PE of 6.7, PEG of 0.12, and a forward EV/EBITDA of 3.63. This is much lower than the sector median forward PE of 17.58, PEG of 1.65, and forward EV/EBITDA of 11.2.

These are very low valuation metrics. Of course, the airlines typically trade with below-average valuations due to the cyclical nature of the business, the sensitivity to higher fuel costs, and the negative impact from the pandemic. However, Qantas' valuation makes for an attractive entry point for the post-pandemic recovery in my opinion.

The forward looking valuation metrics are taking into account a profitable year for Qantas for FY23. The company is expected to achieve EPS of $3.39 for FY23 which ends in June 2023. This profitable year follows three unprofitable years due to the negative aspects of the pandemic.

Strong Expected Growth

The recovery from the pandemic is expected to allow Qantas to achieve revenue growth of 48% and EBITDA growth of 120% for FY23. At the same time, CapEx is expected to grow at about 20%. Qantas is also expected to grow EPS at an average annual pace of 57% over the next 3 to 5 years.

This growth is likely to drive the stock higher for above-average gains from the low valuation starting point.

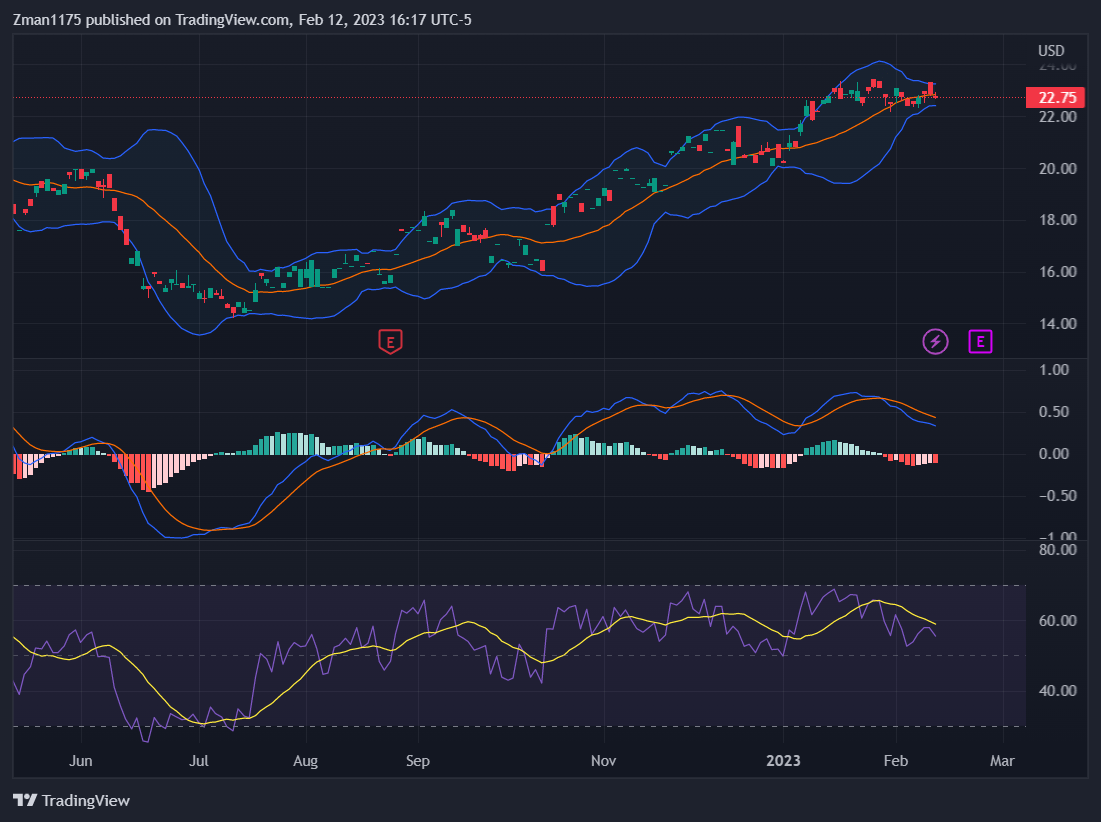

Technical Perspective

{kind=link}

The daily chart above shows Qantas's positive stock momentum. It looks like the price is declining a bit from a near overbought condition. However, I don't see any reason why the stock would sell off significantly right now. This is probably just a natural minor pullback on profit taking.

The MACD in the middle of the chart and the RSI at the bottom have been choppy. So, I would put more emphasis on the strong price action since the beginning of FY23 in July 2022. The price action is reflecting the recovery in the Australian airline industry, which is expected to continue. So, the stock is likely to continue rising along with the industry's recovery.

Seeking Alpha Ratings

{kind=link}

Seeking Alpha has a 'strong buy' quant rating for Qantas. Stocks with strong buy quant ratings have been back tested and shown to significantly outperform the S&P 500 ( SPY ) over the long-term. You can see that the factor grades are all high for Qantas, which is what is driving the strong buy rating.

The Risks for Qantas

Like other airlines, Qantas is highly sensitive to fuel prices. Fuel costs are a major expense. Therefore, any significant spikes in fuel prices could narrow Qantas' profit margins and lower the company's earnings performance.

Another spike in COVID or another disease could lead to future travel restrictions or make people less willing to travel. China could revert back to strict travel restrictions, which could lead to a drop in international travelers to Australia.

Long-Term Outlook for Qantas

The company is expected to report earnings for the 1st half of FY23 on February 23, 2023. The company reports earnings twice per year as an Australian company. I would expect the report to be positive as air travel has picked up and fuel prices have declined from the highs in 2022. Investors could consider getting into the stock before earnings in anticipation of a positive report and future guidance or wait to see what is said for a more conservative approach.

Analysts have a one-year price target of $30 for the stock, representing 32% upside from the current price. This looks reasonable as the valuation is attractively low, leaving plenty of room for upside appreciation. The high expected double-digit growth is likely to drive the stock for above-average gains.

The price target of $30 would take the PE to 8.8 based on the expected EPS of $3.39 for FY23. This would still be a low valuation. So, the price target actually looks conservative in my view.

For further details see:

Qantas Airways Stock Is Taking Off: Massive Potential For Long-Term Growth