QABSY - Qantas Is Not The Long Term Buy It Appears

2023-04-03 08:30:58 ET

Summary

- Qantas is Australia's leading airline and has benefited from a return of air travel, lack of competition, and government support.

- Delayed investment in new planes has temporarily improved earnings yet an estimated spend of $28 b USD on plans over a decade will soon start to drag on earnings.

- Local competition is returning just as consumer trust in Qantas has plummeted while China reopening business has disappointed so far.

- Despite an attractive valuation of 6.5 times earnings, we believe that tailwinds are temporary and long term earnings will revert to pre-COVID averages.

- We rate Qantas a hold with a negative bias.

Introduction

Qantas ( QABSY ) is Australia's dominant airline which has benefitted greatly from reopening following COVID controls. Record earnings have been achieved in an environment with muted competition.

In this report, we first explain the recent record profits.

Then we examine the several headwinds that loom in the short and longer term for Qantas including:

- Falling Australian consumer spending due to sharply higher mortgage rates.

- Delayed capex in new planes will need to accelerate sharply as average plan age approaches 15 years. This will drag on earnings for many years.

- Competition is re-emerging post COVID just as consumer trust in Qantas has plummeted due to wide spread operational issues.

- Chinese air capacity has not returned to pre-COVID levels and this may continue for far longer than many analysts expect.

Looking at the longer term view of Qantas the recent profit performance is well above average. Thus the current valuation of 6.5 times current earnings is actually fair value because current earnings are unstainable. Costs will increase due to Capex and margins may suffer as competition expands.

Short term earnings over the next 6 months might be strong, but if you have a longer term view, we would be tempted to take our gains.

Thus we rate Qantas a hold with a negative bias for the longer term.

Note: Qantas is actually an acronym and should be rendered QANTAS (Queensland and Northern Territory Aerial Services) but we will use Seeking Alpha's convention of Qantas for this report.

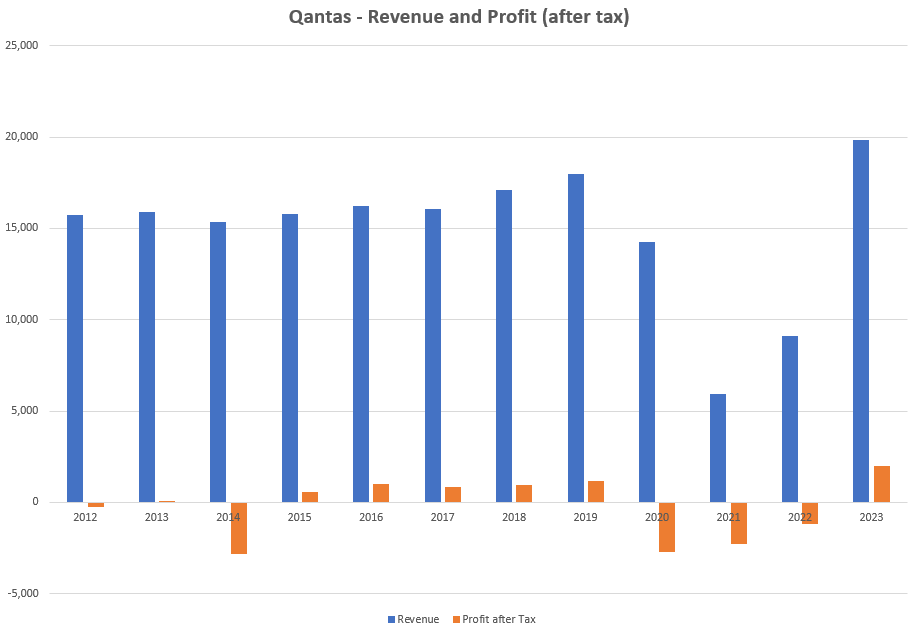

Reopening helps Qantas to record profits.

Many analysts on Seeking Alpha have made the bull case for Qantas. Earnings of $1 b AUD for the last 6 months of 2022 have smashed records. Australian financial years run to June 30, so we have annualized the first six months of 2023 to provide a rough and rosy estimate for full-year 2023 earnings.

Full re-opening has been a truly exceptional time for Qantas.

{kind=link}

Pre-COVID both revenue and earnings had grown at single digit rates, and even then, quite unevenly. Full year revenues will likely get close to $20 B AUD when previous records were almost $18 B AUD. If air fares remain elevated, then profits might reach $2 B AUD, almost double the 2019 record.

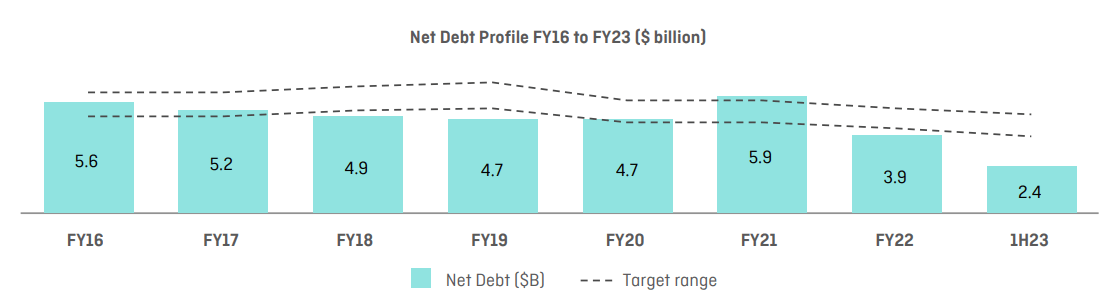

During COVID and revenue plunged and losses mounted. Yet Qantas was fortunate to receive $2 b AUD in government support and wage subsidies. This combined with a capital raise of $1.4 b AUD and a pause in replacing planes (more on that later), has kept debt levels on a gentle steady decline.

{kind=link}

Strong yields from higher than average ticket prices were a key reason for strong profitability. This is unlikely to remain sustainable and increased capacity from Virgin Australia, Rex Airlines and Bonza. More on that later.

Still, a final positive benefit of COVID times is tax losses. At Dec 31, 2022 Qantas still had deferred tax assets of $614 m AUD which at current usage rates of around $400 m a year, might last 18-24 months.

Overall, Qantas is flying in clear skies right now. But clouds lie ahead.

Australian consumers under pressure.

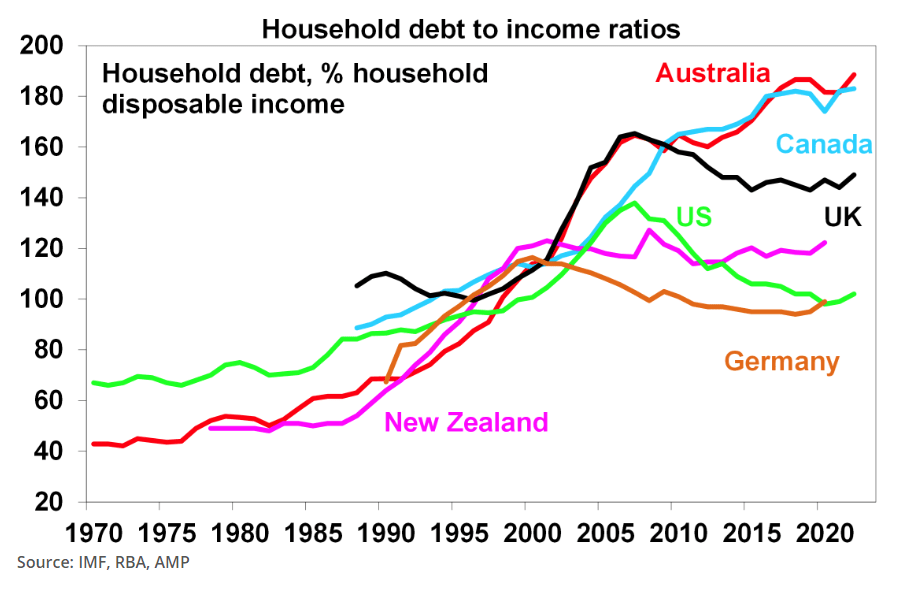

Unlike the United States, about 85-90% of Australians have floating rate mortgages. Mortgage rates have spiked from about 2% to around 6.5%. This is bad news given Australia has a high household debt to income ratio.

{kind=link}

Consumer confidence has collapsed, beaten only by the depths of national COVID lockdown scare of early 2020.

{kind=link}

Forecasters are divided on when rates might ease with the majority forecasting 2024 . National Australia Bank puts recession risk at 45% .

Airline travel is a very discretionary item for spending and it is hard to forecast strong growth given the risk of recession.

Capex has been delayed and will be costly.

Running airlines is challenging and costly. Planes need to be replaced on a regular basis as part of normal operations. For many decades Qantas was famous for operational excellence and average plane age was 8-9 years.

As most proud Australians will know, Qantas was famously name-checked in Rainman for having never lost a plane to a crash in 123 years of operation.

Recent management however has a cost cutting approach and average plane age is now 14.7 years. A string of incidents in December 2022 with 5 planes turning around in a single week, and although none crashed, it left many wondering.

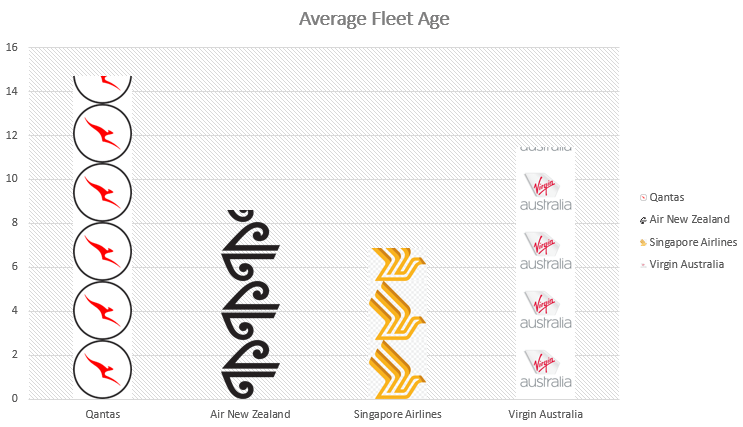

For Qantas' peer group, here is the data on average fleet age .

{kind=link}

Qantas at 14.7 years is far higher than even Virgin's 11.5 years. Average age has drifted higher under CEO Alan Joyce, who started in 2008, but delayed spending has really accelerated in the last 8 years. Flying on older planes is more costly using up to 25% more fuel and maintenance costs are higher.

Guardian

The Australian Financial Review estimated that Qantas needed to spend $28 B USD over the next decade just to maintain current capacity. That's $2.8 B USD a year, or close to $4.1 b AUD annually just to stand still. It would take much more to expand capacity.

Qantas announced a recommencement of plane purchases but this will only address perhaps half the models in service. This cost will start to reappear from late 2023 when the Qantas order for 40 x Airbus A321XLRs begins to be delivered. Despite the orders announced in May 2022, several models of planes such as the A330 have not yet announced a replacement strategy. This may yet cost $9 B USD over a decade.

A delay in orders might be conservative management during COVID, but stock investors should understand how this juices returns in the short term. In the long term the drag on profits and debt levels will be obvious.

Bottom-line: Qantas will need to accelerate spending to keep planes in the air.

Customer satisfaction plummets.

There is an old saying from Dutch Politician Johan Thorbecke :

Trust arrives on foot and departs on horseback.

For many in 2022, trust in Qantas departed on passenger jet.

Qantas and its discount airline subsidiary Jetstar had some of the worst cancellation and rates in Australia in 2022. In addition there was a spike in lost luggage, flight delays and a website that crashed on a regular basis. Cumulatively, this all damaged the Qantas brand.

In fact, the Australian consumer protection regulator, the ACCC reported that:

The ACCC received 1,740 contacts involving Qantas in 2021-22, the most of any company and 68% higher than the previous year.

The ACCC even publicly warned Qantas:

Needs to do more to adequately invest in its systems, processes and people to dramatically improve its customer services and customer dispute resolution."

The Roy Morgan survey of consumer attitudes to the most trusted Australian businesses showed Qantas plummeting from 9th to 40th in the December 2022 quarter. Only a year ago Qantas was 6th.

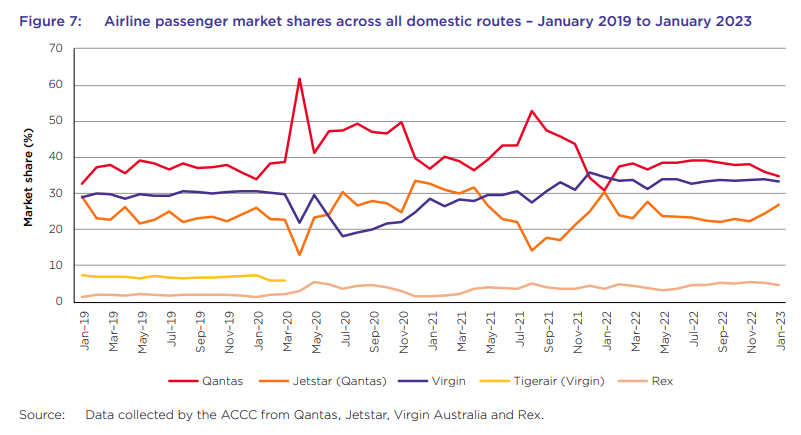

So far this has not led to a decline in Qantas market share. It's often hard to find an alternative on some routes because Qantas and Jetstar combined have about 2/3 of the market. In 2022 most airlines were also capacity constrained, but that is starting to change.

{kind=link}

In 2023 competition is increasing as Virgin Australia increased flights and micro competitor Rex Airlines took market share on trunk routes. A small new airline called Bonza airlines also launched in January 2023.

In this analyst's opinion the Australian market is not large enough to support 2 full-scale airlines at consistently profitable levels. Virgin Australia always struggled to achieve a consistent profit and folded early in the COVID stoppage of 2020. Virgin Australia was bought by Bain Capital in bankruptcy and will soon be listed via an IPO .

Even in good times Qantas was doing just OK on an inconsistent basis.

Virgin Australia is not yet back to pre-COVID capacity but it's expanding and along with small competitors Rex and Bonza increasing capacity, things have finally started improving for consumers as the figure below shows.

{kind=link}

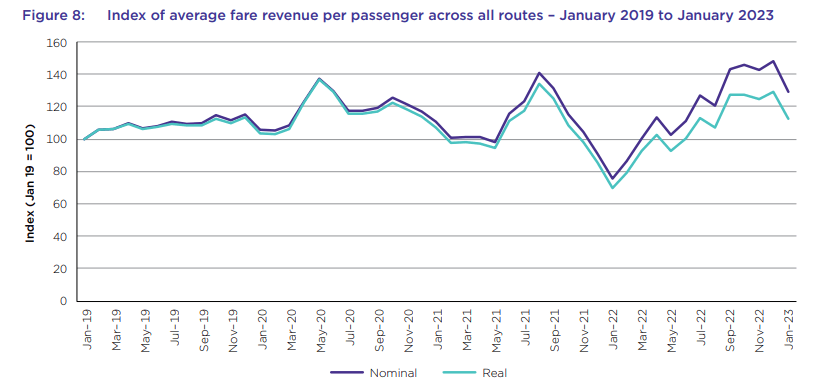

This increased capacity has already led to a decline in revenue per passenger from a peak in November 2022.

Bottom-line: A collapse in trust has many regular travelers ready and keen to try alternatives.

China re-opening has disappointed so far.

The return of travel to China will be positive for Qantas, but not quite the immediate boom some expect. Issues exist for supply and demand.

Supply: Capacity is hampered by a lack of staff.

Qantas will struggle to increase capacity to China quickly having already struggled with staffing capacity issues in late 2022. Issues remain and Qantas is still trying to recruit employees as a leaked email to former staff in February 2023 showed. The goal for international capacity to be back to 80% by June 2023. This means flights to China will likely still be missing for some time.

Qantas has still not yet announced a return to direct flights to Shanghai or Beijing and is only flying to Hong Kong at present. This might be due to capacity issues, but given the high ticket prices in the market, it is just as likely that government approvals from the Chinese end are still lacking.

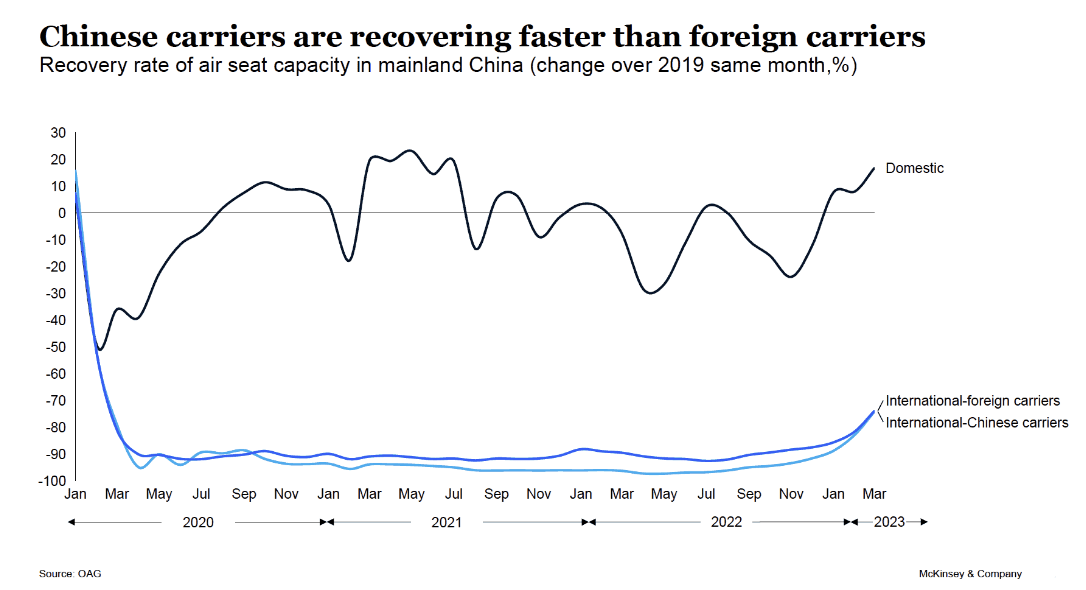

Demand: Chinese international travel is returning, but only slowly.

The expected boom in international travel has so far not eventuated. The reasons could be a lack of flights, a delay in route approvals, a new preference for local travel and a weak local economy are all contributors.

{kind=link}

Perhaps this analyst is too cynical, but we find it easy to believe that the government is delaying the return of international carriers to Chinese skies to enable Chinese airlines to make bumper profits due to limited competition.

Bloomberg Intelligence estimates that Chinese international travel will only return to 45% of 2019 levels by the end of 2023. That's well short of a boom.

Clear skies are temporary for Qantas.

If you look at the long term history of Qantas' financial performance then we can see a range of $300-500 m AUD per annum is more likely long term than current inflated levels. Even at this rate, consistency is unlikely. This implies an earnings multiple of around 14-20 rather than the temporary boost delivering a seemingly cheap multiple of 6-8 times earnings.

When investing in airlines, never forget the old joke based on a kernel of truth.

How do you make a small fortune in airlines? Start with a large fortune!

Don't be fooled by Qantas' profits made during a period when competitors were weak, consumers were ebullient at their COVID release, ticket prices were 2-3 times normal levels due to a lack of capacity, and investment in new planes had slowed to a crawl.

Normal business conditions are returning, consumer spending is slowing and the airline business has a well-earned reputation as a tough game .

Further, it's hard to see Qantas can grow from here.

Qantas valuation is fair but far from attractive and towards the top of the investable range. Consider taking profits if you are sitting on paper gains.

We rate Qantas a hold with a negative bias.

For further details see:

Qantas Is Not The Long Term Buy It Appears