QDPL - QDPL Could Be Better Than JEPI In Some Ways

2023-07-12 22:43:19 ET

Summary

- The Pacer Metaurus US Large Cap Dividend Multiplier 400 ETF aims to offer a dividend yield equivalent to 400% of the S&P 500's yield, using strategic futures contracts trading.

- The fund's approach differs from JEPI's covered calls strategy, allowing investors to benefit from dividend hikes and maintain a significant portion of the S&P 500's upside.

- While JEPI might perform better in a bear market or if companies cut dividends, QDPL could outperform in a prolonged bull market with substantial dividend growth.

Pacer Metaurus US Large Cap Dividend Multiplier 400 ETF ( QDPL ) is a quite less known ETF that has some very interesting and unique qualities that might interest many people, especially investors of JEPI ( JEPI ) because it has a very similar goal but a very different way of accomplishing this goal while offering some additional benefits as well. One could actually say that this fun is undiscovered. Even on Seeking Alpha this ETF has only 145 followers as of the time of writing this article. Maybe after reading this article, the ETF will catch attention of more people because it's certainly worth a look.

I think this fund might be even better than JEPI in some ways after considering its pros and cons as I will explain below and compare the two funds in their different approaches.

This fund invests directly in S&P 500 futures so its composite, sector loadings, weights and other qualities mimic that of S&P 500. Basically you get exposure to the exact same stocks as you would if you were investing into S&P 500 index with the exact same weights.

QDPL's goal is to pay a dividend yield that is equivalent to 400% of the dividend yield of S&P 500 by strategic trading of futures contracts. For example when S&P 500 has a yield of 2%, this fund is shooting to have a yield of 8%. This is similar to JEPI offering a higher yield by selling covered calls but there are also differences between two approaches.

First, let's see what QDPL does and how it quadruples the dividend yield of S&P 500. It uses a vehicle called Dividend Futures which are cash-settled contracts that allow the purchaser of the said future contract to take advantage of expected future dividend payments before its payment date. There are quarterly and annual dividend futures which allow investors to trade dividends before they are even paid. Since we don't know for sure how much dividend will be paid in advance, dividend futures trade like an asset with bid-ask spreads based on investors and traders placing their bets. At the end of the year, all dividends paid during the year are added to the settlement price of the future. If dividends paid at the end of the year are higher than expected (and priced in) in the beginning of the year, the holder of the dividend futures contract makes additional money. If the dividends are cut or come in less than originally priced in, they can actually lose money but they can simply roll their contracts.

Historically S&P 500 dividends have grown by about 6% annually while annual futures contracts typically imply a dividend growth rate of 0% to 4%. In fact it's very rare for them to imply a higher dividend growth rate than 5%. Moreover, in the last 10+ years, futures contracts never implied a higher dividend growth than the one that actually occurred.

Having given all this information, how does the fund take advantage of this? The fund holds cash as collateral and buys annual dividend futures, rolling them up as they come. Below is a quote from fund's materials :

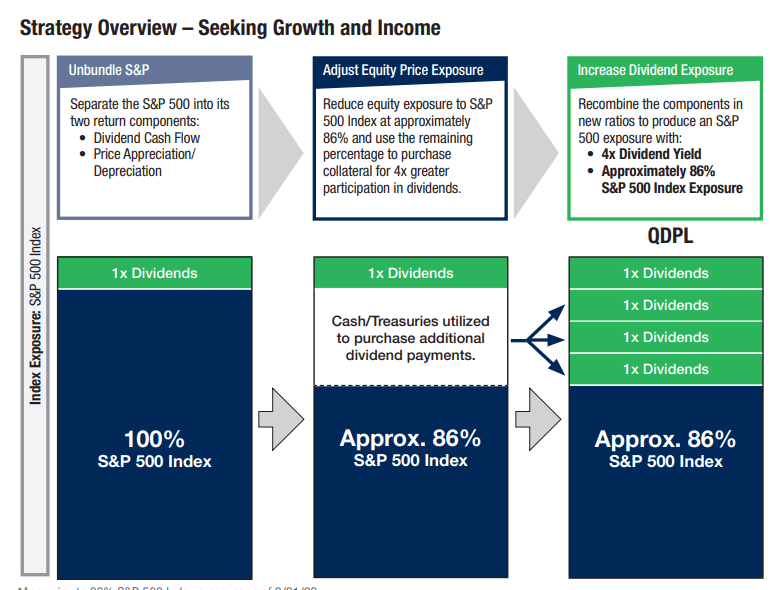

The fund utilizes the dividend multiplier strategy to reallocate capital between an index’s dividend cash flow and potential price appreciation/depreciation. By holding 4 times the dividend component, including dividend futures and equity investment, the fund aims to provide cash distributions equal to 400% of the S&P 500’s ordinary yield in exchange for modestly lower exposure (approximately 88%) to the S&P 500 Index performance. As of 12/31/2022, the fund's indicated yield is 7.45% vs. only 1.7% from S&P 500. At the same time, the 1-year beta is 0.9.

The fund does not use leverage so it's beta comes below 1.0. Basically the fund gives up 14% of S&P 500's growth in exchange for 4x its dividends. For every 1% that S&P 500 gains, this fund is expected to gain 0.86% so it's not totally giving up all upside either. For example, if S&P grows 10% in a year, this fund is expected to gain 8.6%.

QDPL's strategy overview (Pacer ETFs)

{kind=link}

Comparing QDPL to JEPI

How does this compare to JEPI? Let us list the positives first.

JEPI sells covered calls which caps almost all upside. We don't know exactly what price point JEPI sells its calls because it utilizes ELNs (equity-linked note) which don't come with a lot of transparency. We can still have a good estimate though because we can see how JEPI's NAV moves when the stock index moves higher. For example last January S&P 500 was up 7.38% while JEPI's NAV only rose 1.07% which tells me that JEPI's covered calls were sold at a strike price very close to the money at the beginning of the month. This means upside will be very limited.

What did QDPL do during the same period? It rose 6.88%. It basically kept 93% of S&P 500's upside while offering 4x its dividend yield.

How about long term? The fund has been around just a little over a year but during this time its total return was very comparable to the return of S&P 500.

The second positive of QDPL over JEPI is that it will allow investors to benefit from dividend hikes. JEPI's dividend payments and dividend yield mostly depend on how much it can generate from covered calls because only a small portion of its total dividends come from dividend payments it receives from its holdings. JEPI's dividend yield also depends heavily on VIX because VIX pretty much dictates how much the fund can earn from selling monthly options. QDPL is different because it can not only take advantage of dividend hikes but it can also multiply the effects of them since the fund multiplies its dividends by 400% using dividend futures contracts. Below is a chart of SPY's dividend history just to give a general idea about what kind of dividend growth investors can expect in the long run.

But there are also areas where JEPI excels. Although QDPL's beta is much lower than that of the stock index, JEPI's beta is even lower than QDPL's. This is partially because of JEPI's intentional stock selections and partly due to covered calls it sells. Keep in mind though that beta works both ways and it limits both upside and downside for funds so while JEPI is likely to see more protection during a bear market it is also likely to see a much slower recovery on the way up. Since the markets tend to go up far more often than they go down, a low beta might actually be a disadvantage because the average bull market lasts about 6-7 years while the average bear market only lasts about 10 months and low beta provides tailwinds during a bear market and headwinds during a bull market.

Here is where JEPI might excel against QDPL though. If companies start cutting dividends like they did in 2008, QDPL's dividend will also get a cut. In fact, if SPY's dividend yield drops from 2% to 1%, QDPL's yield could drop from 8% to 4%. JEPI probably won't see a sharp decline like that because it doesn't rely on dividend payments. In fact, in an environment like that, VIX would likely be higher and JEPI would likely generate higher than average yields.

This advantage might not last long though because if we are in a market where dividends are being cut all over the place, S&P 500 would also see a price decline and its forward yield could still rise or at least stabilize.

Another advantage of JEPI is that its approach is less complicated and most investors understand how it works so they might feel more comfortable putting their money in JEPI. QDPL's approach is pretty advanced to say the least and many people might not fully understand how it works and they might simply choose not to invest in it. Then again, one could also make the counter argument that JEPI's reliance on third-party ELN's to generate yield is not exactly transparent either because we don't know the exact details of it such as strike prices or expiration dates of the options being sold.

To be honest, I wouldn't want you to pick one or the other because there is room for several stocks and funds in a well-diversified portfolio. You can buy and hold both and get good results from both in the long run. I just believe there are certain areas where QDPL might be more likely to outperform JEPI because it offers a similar dividend yield without giving up all upside and it also takes advantage of dividend growth in a way JEPI doesn't. In a prolonged bull market that comes with plenty of dividend growth, QDPL would certainly outperform but we don't know what kind of market lays ahead of us either.

I am personally buying and holding both but I plan on adding more funds to QDPL than JEPI in the next 12 months.

For further details see:

QDPL Could Be Better Than JEPI In Some Ways