SSNLF - Qualcomm: This Is Clearly Not The Bottom

2023-05-17 09:00:00 ET

Summary

- The semiconductor and personal devices demand destruction is not over yet and is likely to continue for the next few quarters, based on QCOM, INTC, AMD, and AAPL's recent earnings call.

- QCOM's recent FQ2'23 performance and FQ3'23 guidance appear underwhelming as well, significantly worsened by the growing long-term debts at elevated interest rates.

- Combined with the deteriorating balance sheet, the stock may further retrace to its previous July 2020 support level of $95.

- Even then, investors may only add if it consequently matches or lowers their dollar cost averages, since the economic downturn may only end by 2024, if not 2025.

- Nonetheless, its partnership with various OEMs bodes well for its long-term recovery, since Androids comprise up to 49.9% of the global smartphone market share in Q1'23.

The QCOM Investment Thesis Is Only For The Patient

We have been previously bullish about QUALCOMM Incorporated's ( QCOM ) long-term prospects, as highlighted in our article here . While our opinion remains the same, we suppose the optimism about the automotive and industrial end markets must be tempered a little, since the semi-chip correction has yet to end.

Notably, the consumer demand for personal devices remains impacted, with Intel's ( INTC ) top and bottom lines still underperforming in the latest quarter. Even Micron Technology ( MU ) has reported significant inventory write-downs , with Samsung ( SSNLF ) and SK Hynix likely experiencing record-high inventory levels for memory chips.

Even one of the most enduring smartphone brands, Apple Inc. ( AAPL ), has faced a deceleration in smart device sales in FQ2'23, with product net sales of $73.92B ( -23.3% QoQ / -4.5% YoY) against the previous cadence in FQ2'22 ( -25.8% QoQ / +7.65% YoY).

As a result, it is unsurprising that QCOM's FQ2'23 results have been impacted, with revenues of $9.27B (-2% QoQ/ -16.9% YoY) and adj EPS of $2.15 (-9.2% QoQ/ -33% YoY).

Notably, most of the revenue decline is attributed to the handset segment at $6.1B (+6% QoQ/ -16.8% YoY), though consumer demand for the automotive at $447M (-1.9% QoQ/ +20.4% YoY) and IoT at $1.39B (-17.2% QoQ/ -26.6% YoY) has also declined by the latest quarter.

However, QCOM investors need not fret yet, since its Average Selling Prices remain stable, with gross margins still intact at 55.2% in FQ2'23, against the 56.5% reported over the last twelve months [LTM] and 57.8% in FY2022.

In addition, the chip company continues to invest in its capabilities despite the downturn, with Research & Development expenses of $2.21B (inline QoQ/ +8.8% YoY) in FQ2'23, only slightly moderated from the FQ2'22 cadence (-5.1% QoQ/ +14% YoY). We suppose these efforts may ensure that it emerges stronger once the macroeconomic outlook normalizes, likely by 2025, if not earlier in 2024.

Meanwhile, investors must also note that QCOM has increased its reliance on long-term debts to $15.48B (inline QoQ/ +26.9% YoY) by the latest quarter, naturally triggering an elevated annualized interest expense of $716M (+46.1% YoY).

Due to the Fed's continuous hikes thus far, we may see a further increase in its expenses ahead, especially since the chip company recently secured loans of $700M at a fixed interest rate of 5.40% through 2033 and $1.2B at 6% through 2053. This is naturally alarming, compared to the historical interest rate cadence of between 2.50% and 4.73%.

QCOM's balance sheet has also deteriorated to $6.67B of cash/ short-term investments (-18.9% QoQ/ -42.2% YoY), likely worsened by the sustained share repurchases of $3.7B (-13.9% sequentially) and dividend payout of $3.35B (+9.4% sequentially) in the LTM. Then again, with an EBITDA of $14.48B in the LTM (inline sequentially), we reckon that the chip company may remain well-capitalized in the intermediate term.

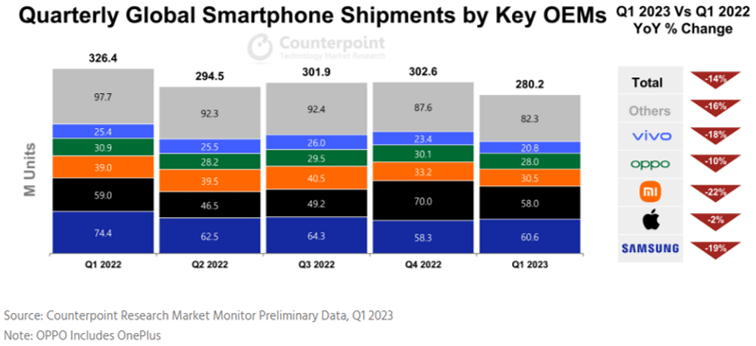

Android OEMs Shipment Globally

{kind=link}

In addition, QCOM's partnership with Android OEMs bodes well for the recovery of its top and bottom line in the long term, since Samsung continues to command the largest share at 60.6M units (+3.9% QoQ/ -18.5% YoY) in the global smartphone market by Q1'23.

This is on top of Vivo, Oppo, and Xiaomi delivering a total of 79.3M units (-8.5% QoQ/ -16.7% YoY), compared to AAPL's 58M (-17.1% QoQ/ -1.6% YoY) at the same time. Therefore, since the chip company supplies its Snapdragon 8 Gen 2 mobile platform for the flagship models of all four OEMs mentioned above, investors need not fret since this headwind is only temporary, with most tech/ semiconductor companies/ OEMs similarly impacted.

Meanwhile, QCOM still offers underwhelming forward guidance , with FQ3'23 revenues of $8.5B at the midpoint (-8.3% QoQ/ -22.2% YoY) and adj EPS of $1.80 at the midpoint (-16.2% QoQ/ -39.1% YoY). The main culprit notably remains with QCT, at revenues of $7.2B (-9.3% QoQ/ -23.1% YoY) and to a smaller extent, QTL revenues of $1.25B (-3.1% QoQ/ -17.2% YoY).

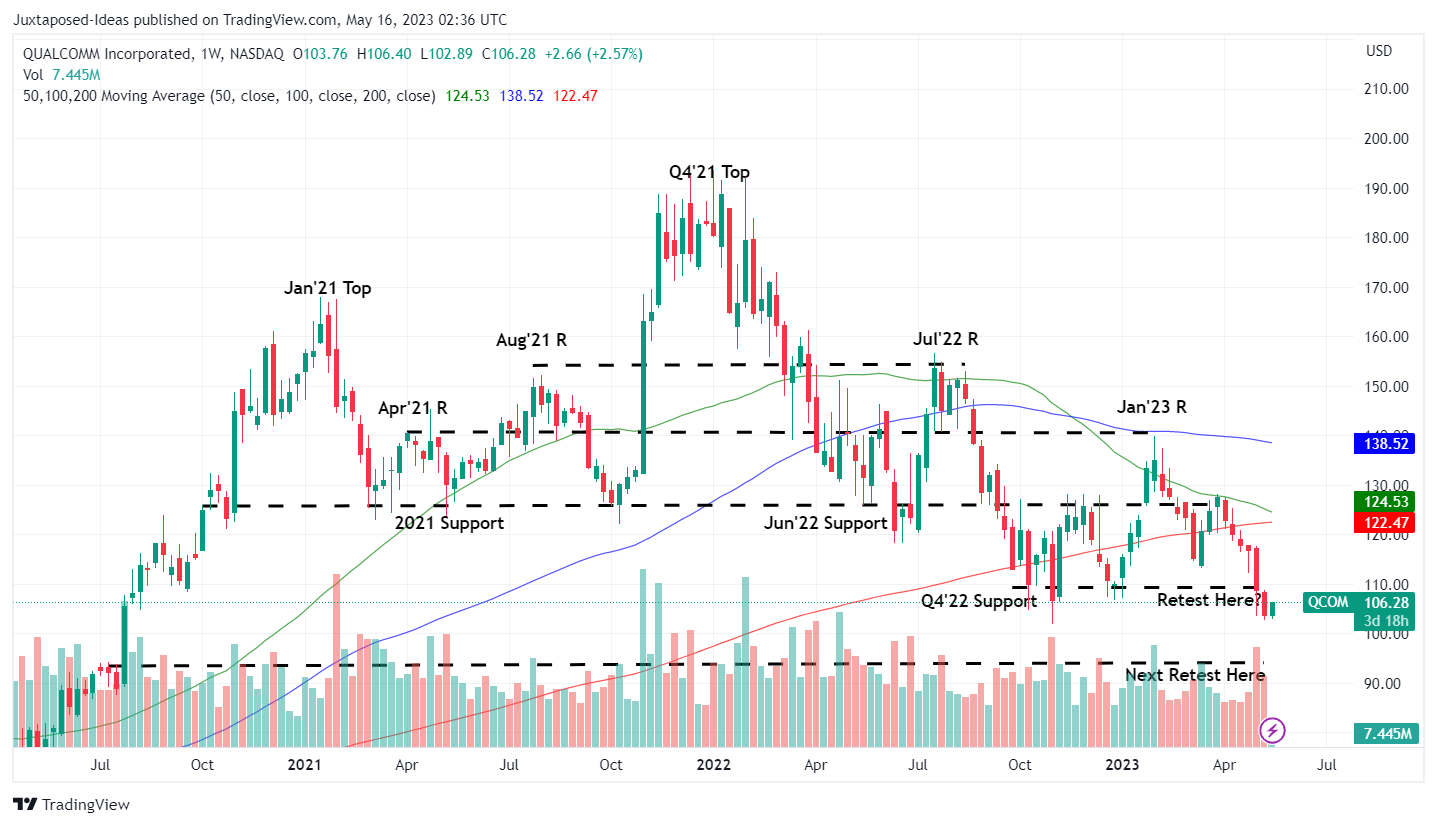

QCOM 3Y Stock Price

{kind=link}

Given these numbers, it is unsurprising that the QCOM stock is already testing the previous Q4'22 support of $110s. As a result, we do not recommend anyone to add the stock at this perceived dip yet, due to the potential underperformance from these levels.

Assuming that the current support is breached, we may see another retest of the July 2020 level of $95, depending on the market sentiments then. Investors may be well advised to wait for those levels for an improved margin of safety.

Nonetheless, we must highlight that QCOM is only suitable for those with long-term trajectory, since the handset, automotive, and IoT markets are still undergoing demand corrections, with the peak recessionary fears likely putting further downward pressure on discretionary and corporate spending, elongating the replacement cycles.

As a result, while we continue to rate the stock as a Buy, investors may only do so if it consequently matches or lowers their dollar cost averages, since the economic downturn is only starting.

For further details see:

Qualcomm: This Is Clearly Not The Bottom