MBLY - Qualcomm: Underappreciated GARP Reiterating Buy

2023-12-21 23:47:47 ET

Summary

- Qualcomm's auto segment should power growth for the next decade.

- The Company's lucrative treasure trove of patents in connectivity should continue to ensure high-margin revenues for a long time.

- Its Snapdragon technology in partnership with Microsoft can find opportunities in the PC space.

- QCOM is an underappreciated and undervalued stock and a great bargain at this price.

I first recommended Qualcomm ( QCOM ) in March 2023, citing that Autos and IoT, its two other main stays would make up for the loss of revenue from Apple's ( AAPL ) iPhone business. I subsequently followed up with an article on the auto-tech industry, focusing on Qualcomm, Nvidia ( NVDA ), and Mobileye's ( MBLY ) massive auto pipelines to gain tremendously from the digitization of the car. The stock has moved up 32% this year to date, handily beating the index, and 15% since I recommended it. I believe there is still a lot of appreciation left and it's a fantastic GARP (Growth At a Reasonable Price) stock at $142. I'm re-iterating my buy recommendation.

First the good news, Apple stays on as a handset customer for an extra two years than originally planned, till FY 2027. Qualcomm's crown jewels of extensive, essential patents for wireless networks, such as a near-monopoly in 3G wireless networks, a large share of 4G patents, which contributed enough innovation to warrant earning royalties on virtually all 4G devices and a good portion of essential patents with 5G - ensure a lucrative stream of royalty revenue from most cell phones. Clearly, developing in-house modems is an enormously difficult undertaking and even the mighty Apple is still struggling to achieve the same levels of expertise and product quality that Qualcomm provides. While Apple's progress will encourage other handset makers to also develop in-house modems, especially technical powerhouse, Samsung Electronics Co. (SSNLF), I believe it is still at least a decade and billions away. And in the meantime, Qualcomm powers on with 6G development. The crown jewels continue to bolster and monetize the business.

Qualcomm's Revenue Segments

Based on Apple's decision to stay on with Qualcomm, I revised the revenue segments as below.

Qualcomm revenue segments (Qualcomm, Seeking Alpha, Fountainhead)

Qualcomm reports in two segments, QCT - equipment and services and QTL - licensing revenue, which is 84% and 16% of total sales respectively.

QTL

QTL had a terrible FY2023, dropping 17% from $7Bn to $5.8Bn mainly because of the massive drop in cell phone revenue of 22%. The cellphone industry had an inventory glut and severe indigestion from over-ordering due to the pandemic, which caused a lot of damage to licensing revenues as well, as customers drew down on inventory in FY2023 and ordered precious little. I expect a rebound in FY2024 of 14%, and then a modest growth of 8% going forward.

QCT

Phones - Handsets

Equipment sales to cell phone makers should rebound by 8% from the 22% drop in FY2023, but grow slower at 5% each year for both Android and I-Phones in FY2025 and FY2026. Cellphones are a saturated market and higher growth is unlikely to resume, over time there should be some weaning of demand from the likes of Huawei and other Chinese manufacturers also trying to build their own modems and chipsets, mitigated by new products such as the Snapdragon 8. Given Qualcomm's R&D spend of $9Bn and expected early lead in 6G, this will be a slow but steady grower for the next decade, even after Apple's loss from FY2027.

From CFO Ashish Palkhivala on the Q4-FY2023 earnings call.

QCT handset revenue forecast includes the benefit of normalization of Android channel inventory and higher demand due to the acceleration of flagship launches with our newly announced Snapdragon 8 Gen 3 mobile platform. Notably QCT handset forecast include sequential revenue growth of greater than 35% from Chinese OEMs. QCT IoT revenue forecast reflects the industry-wide cyclical factors we've previously discussed, including lower demand and elevated channel inventory.

Autos

The Auto segment, which is the growth engine, grew a whopping 36% from $1.4Bn to $1.9Bn in an otherwise dismal FY 2023. While it's a small 5% of revenues, 33% growth in the next three years should take it to $4.3Bn by FY2026 and 9% of total sales. I've outlined Qualcomm's auto strengths in the growth drivers section below.

IoT

IoT is the second largest segment in Qualcomm's portfolio and contributed almost $6Bn or 16% of Qualcomm's revenue. While Autos leads the growth charge, the IoT segment, which also dropped 17% last year on inventory drawdowns after growing 38% in the year prior, should remain a modest single-digit grower at 8% for the next 3 years.

Strengths and Growth Drivers

Auto

Auto is Qualcomm's growth engine.

Qualcomm has a large pipeline of $30Bn through 2030, larger than Nvidia's $14Bn and Mobileye's $22Bn. I expect the auto segment to grow from $1.9Bn to $4.3Bn by FY 2026, a CAGR of 33% in the next 3 years. The auto industry, as it moves towards autonomous driving, is an extremely difficult one to work in with its maze of regulations, emphasis on safety, adherence to stringent quality standards, and the time from pipeline to production, which sometimes stretches up to 7 years. ICE (Internal Combustion Engine) automakers have to make a paradigm shift embracing technology as the main driver and not looking at digitization partners as parts suppliers.

Qualcomm's main strengths are

- Its connectivity has decades of experience in the cell phone industry.

- It's focused on becoming the seamless, one-stop shop integrating ADAS, Infotainment, Car to Cloud services, and connectivity.

- Its massive capacity to scale and handle the complexity needed to manage different systems, stacks, and vendors.

- Building a better platform at scale - Qualcomm would be the digital chassis for traditional ICE automakers needing a new architecture at scale with product, connectivity, and services. Qualcomm would be the perfect auto partner from design to production.

- Unlike Mobil Eye, Qualcomm could take market share by being more flexible and building heterogeneous SoCs the way they did in phones and IoT.

Given the emphasis on technology and the high growth, Mobileye, Qualcomm's largest competitor is valued at a whopping 16x revenues. I don't believe the markets are valuing the strength of Qualcomm's $30Bn pipeline and 33% growth correctly and see this as an opportunity to buy.

Further, in FY-2023, amongst its competitors, Qualcomm's auto segment grew at 24% compared to an estimated 22% for Nvidia and 21% for Mobileye.

Licensing Revenue

Licensing revenue with a whopping EBT (earnings before taxes) margin ranging from 70 to 74% is the crown jewel of Qualcomm's portfolio. The licensing business of $6Bn, growing steadily in high single digits is around 16-17% of Qualcomm's total revenue but with margins over 70% goes straight to the bottom line. It has a virtual stranglehold in the cell phone connectivity market with mighty competitors like Apple unable to break out and make their own chips even after 5 years of trying. I believe this lucrative 5G royalty stream should continue for the next decade, and further down, the 6G networks rollout from 2030 should maintain the licensing revenue stream for the next decade. Even in the horrible fiscal 2023, with revenues down 19%, Qualcomm grew R&D spending from $8.2Bn to $8.8Bn, from 19% of revenues to 25%, clearly doubling down on their strength.

PCs, AI, and the move to ARM processing

- Microsoft's ( MSFT ) foray into AI is pushing on-device AI centerstage and Qualcomm is working with them to provide faster and more efficient chips.

- The PC market seems to be evolving into ARM-based architecture, which should benefit Qualcomm, perhaps ushering in a new era in PCs as Seeking Alpha contributor Bob O'Donnell suggests.

- Initially, revenues may not be significant, but if there is a paradigm shift over time, Qualcomm's capacity to scale similarly with cell phones and autos should definitely get them a decent share of this market and a new revenue stream.

- While it's too early to forecast revenues, Qualcomm's flagship Snapdragon can make inroads into the PC space. There are three main reasons why Qualcomm can get revenues from the PC market.

In CEO, Christiano Anon's own words on the Q4-2023 Earnings Call, emphasis mine:

On-device Gen AI is evolving in parallel with Gen AI in the cloud enabling entirely new use cases. We expect high-performance on-device AI to become a requirement over the next few years, driving content, units, or both . Our Snapdragon platform is highly differentiated from its competitors. First, we significantly increased the AI processing performance in power efficiency of our best-in-class NPU, CPU and GPU.

We also reached an important milestone in our expansion into PCs with the announcement of our Snapdragon X Elite platform. The Snapdragon X Elite includes our first implementation of the custom Oryon CPU, which exceeds the multi-threaded CPU performance of any x86 or ARM competitor in its class. It also matches the single-threaded CPU peak performance of the leading x86 CPU competitors at 70% less power.

In total AI performance of the Snapdragon X Elite across CPU, GPU and NPU is 75 tops, the highest in the industry.

Microsoft is redefining the entire Windows experience with the AI Copilot and the Snapdragon X Elite is built from the ground up for this opportunity. We look forward to PCs powered by Snapdragon X Elite from leading OEMs starting mid 2024 .

Risks

Qualcomm's licensing business grew at the expense of Nokia and other weak players at that time. It did become the technological leader in 3G, 4G, and 5G, earning billions in licensing revenues. However, current competitors include the $380Bn market cap Samsung with much better access to technology, and Apple, which will eventually make the breakthrough. Then there are Chinese competitors, funded and helped by their government, who want technological self-reliance.

There is a severe amount of pushback from customers like Apple, suing for licensing royalties to be based on component costs such as baseband and antennas and not the final cost of the device.

Lastly, while government regulators have been focusing on big tech, there is the risk of regulators trying to protect customers by reducing smartphone prices by reducing licensing fees.

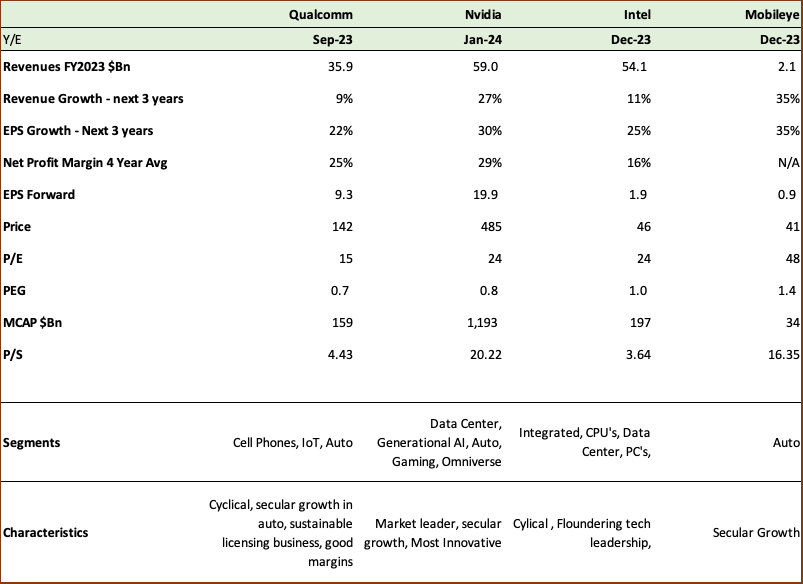

Competitors

Qualcomm's competitors (Qualcomm, Nvidia, Intel, Mobileye, Seeking Alpha, Fountainhead)

{kind=link}

Qualcomm stacks up well against Nvidia, Intel, and Mobileye, with the cheapest P/E and PEG ratios of 15 and 0.7. All four should have a better three years ahead with earnings growth ranging from 22% for Qualcomm to 25% for the beleaguered Intel ( INTC ), also coming off a horrible 2023. Mobileye and Nvidia, of course, will grow faster on the strength of auto and data center growth respectively. I also find Qualcomm's P/S very attractive at only 4.4, it's just a little above Intel's 3.6, a company with two years of revenue declines from $79Bn in 2021 to $54Bn in 2023, and under attack from several fronts. Qualcomm also should be valued much higher than Micron ( MU ), a cyclical at 3.8x sales.

Investment Case

Qualcomm has a lot of positives going for it, I own some and keep adding to my portfolio.

The licensing business is a highly lucrative treasure trove with enough defenses to last at least a decade. It has 70% margins and Qualcomm has been consistent with R&D spend even in down years to keep this segment in great shape.

The auto segment has a bright future with 33% growth. The cell phone business while growing slower is a large chunk of Qualcomm's revenues and will continue to grow in low single digits for at least another decade.

Qualcomm's earnings will grow faster at 22% than revenues of 9% in the next three years and at 15x forward earnings is a decent bargain. Besides, it has very strong margins at 26-28% for the equipment business and 70 to 74% for licensing in FY 2024.

Qualcomm Financial Analysis (Qualcomm, Seeking Alpha, Fountainhead)

I also made a sum of the parts scenario for Qualcomm; I don't believe my assumptions are unrealistic in the table below. Here goes:

Qualcomm sum of the parts (Qualcomm, Seeking Alpha, Fountainhead)

The QCT (equipment) business gets a companywide EBT margin of 26 to 28%, which is extremely good.

Auto - I took Mobileye's P/S of 16, Qualcomm is growing at 33% compared to Mobileye 35% and are around $2Bn in revenues; besides Qualcomm's pipeline of $30Bn is larger than Mobileye's $22Bn.

Licensing - I took a multiple of 16X - this is a very, very lucrative business with 70-74% EBT margins, and still grows at 8%. With Apple's failure and the continuous technological advances in connectivity such as 6G coming up, I believe this deserves a high multiple of 16. Comparatively, Arm Holdings plc ( ARM ) is valued at 23X sales.

IoT - A steady grower at 8%, assigned at 6x sales, also because of the high margins.

Cell Phones - The largest component at $20Bn in revenues, but assigned a low 4x sales, on par with Micron and Intel, which I believe is conservative since I do believe Qualcomm is a stronger company than both. Besides, Qualcomm is also one of the strongest competitors in cellphones connectivity with its licensing treasure trove.

Based on that, Qualcomm should have a market cap of $249Bn, and currently at $159, I believe it is undervalued by 57%.

For further details see:

Qualcomm: Underappreciated GARP, Reiterating Buy