XM - Qualtrics International: Great Growth Interesting Catalyst Create Enthusiasm

Summary

- Qualtrics International Inc.'s shares soared after management reported positive financials for the final quarter of 2022, and news broke that its largest shareholder is interested in selling its stake.

- This 71% stake in the company could have major ramifications for all parties involved, but the devil will be in the details.

- Qualtrics International is growing really well and bottom line results are improving, but the uncertainty and the price of the firm make me more neutral on the business for now.

Buying into rapidly growing technology companies can be a great way to generate strong returns. It can also be a great way to lose a lot of money. But add into the picture the fact that you might now have an interesting catalyst, and the picture becomes far more complicated. One company that fits this description is Qualtrics International Inc. ( XM ).

While revenue growth for the company has been fantastic over the past few years, and that trend looks set to continue for 2023, profits and cash flows have been a bit of a problem. The good news is that, if you make certain adjustments, you can see where value is being added. But on top of this, we now have a scenario where the company's largest shareholder is looking to divest of its ownership in the firm. Depending on how things go, this could result in greater autonomy by management while also freeing up cash for the seller. But the bigger question that shareholders have is what the end result might be for them.

All things considered, I would say that recent developments favor investors in the company. But this does not necessarily mean that the company makes for a good opportunity for all investors.

Great growth and an interesting catalyst

Operationally speaking, Qualtrics International is set up as a software enterprise that's dedicated to what it calls "experience management," often abbreviated as "XM." Through its XM Platform, the company helps organizations both design and improve the experiences that build loyalty with their customers, turn employees into ambassadors, increase the love of the products these organizations produce, and more. To be clear, management refers to experienced management as the business discipline of helping organizations connect with their customers and employees. The company's platform has four core experiences that it makes available to its customers through the software that it provides.

The first of these is called CustomerXM. This particular offering aims to decrease churn, increase engagement, and expand customer lifetime value by listening to customers across all sales and other channels and utilizing their feedback to create additional value. For instance, the software will track the entire customer journey across a company's platform, collect data on pain points, provide access to the business of reviews from customers, and more, all with the aim of finding ways to reduce those pain points. The EmployeeXM product does something similar, but with employees. For instance, the offering can help with conducting performance assessments, measuring employee engagement, keeping track of things like work anniversaries and parental leave periods, and even assisting with recruiting and onboarding activities when it comes to new talent.

ProductXM helps its customers to design products that people love, to decrease the time to market, and to increase the profitability of organizations by uncovering and acting on user needs, desires, and expectations. This particular offering helps to find broken product experiences and fix them, whether that involves pricing strategies, packaging, concept testing, or others. And finally, we have BrandXM, which helps to create more loyal followers, promote customer acquisition, and increase in organization's market share by making sure that the brand in question resonates with target customers. The platform does this, and other things, largely through keeping track of key performance indicators and other insights on a real-time basis.

There are some other services that the company has launched over time. DesignXM, for instance, helps to uncover the products, services, and experiences that the market might want next by looking at market research, looking at design, and more. Meanwhile, XM Services provides expert-designed programs centered around things like advisory services and executive reporting.

{kind=link}

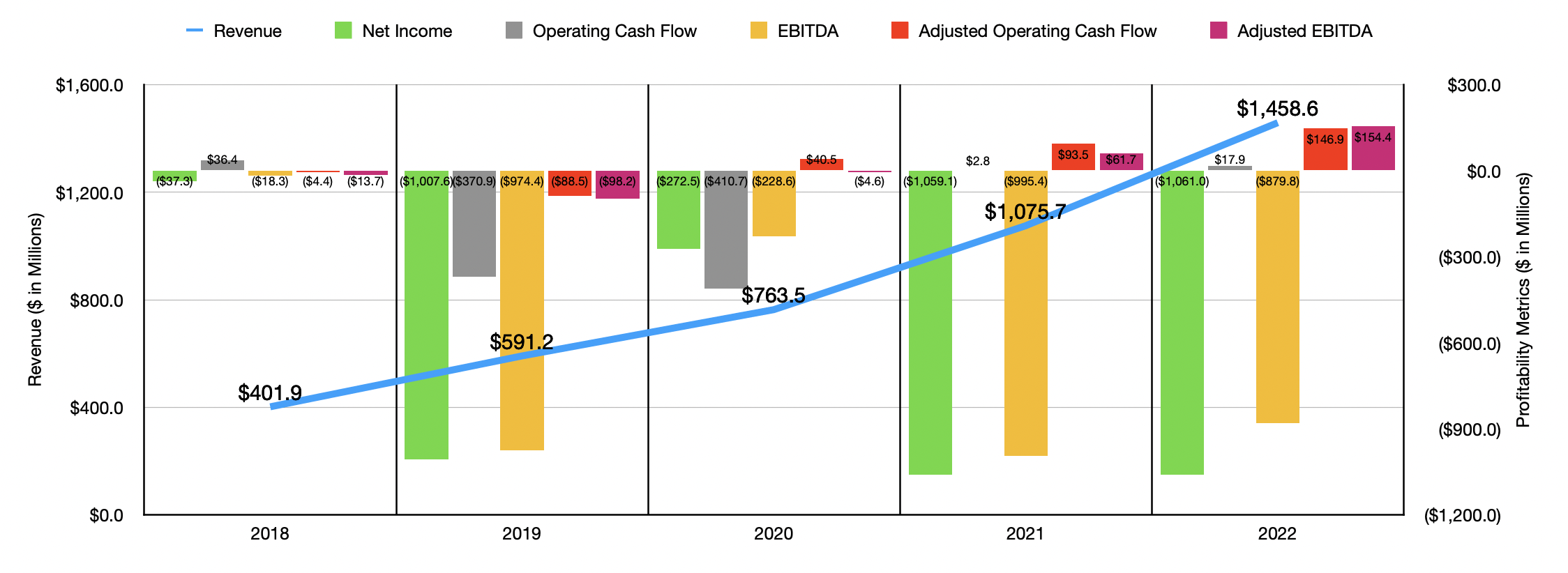

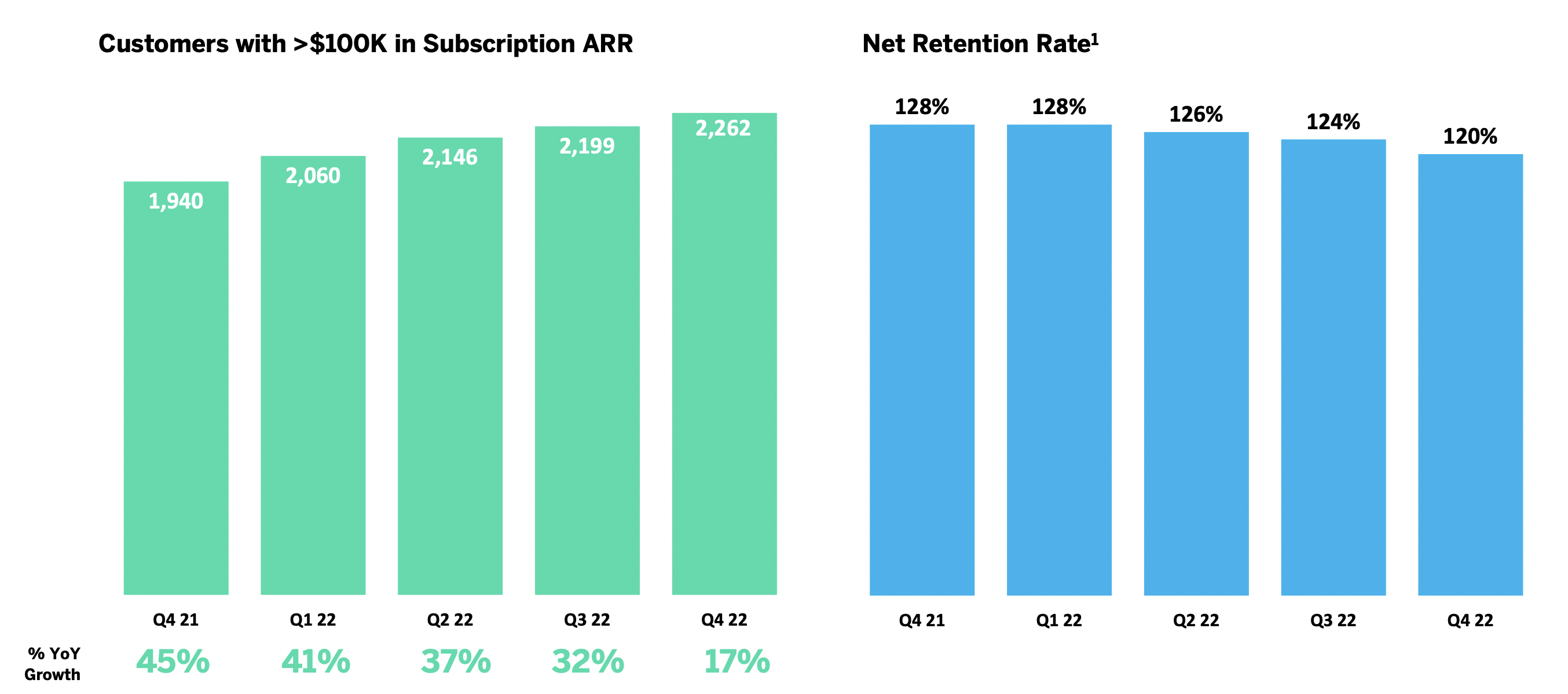

Over the past five years, the management team at Qualtrics International has done a great job growing the company. Sales went from $401.9 million in 2018 to $1.46 billion in 2022. The increase of 35.6% from $1.08 billion in 2021 to the aforementioned 2022 figure came largely due to a rise in the number of large customers. Large customers are those responsible for over $100,000 in annual recurring revenue associated with the company's subscriptions. At the end of the final quarter of 2021, this number came out to 1,940. By the end of 2022, this number had grown to 2,262. For context, as recently as the end of 2019, the company had only 1,026 large customers.

{kind=link}

On the bottom line, though, the picture has been quite volatile. With the exception of the 2020 fiscal year, when the company reported a net loss of $272.5 million, each year from 2018 through 2022 has been worse for the company from a profitability perspective. The firm went from a loss of $37.3 million in 2018 to a loss of $1.06 billion in 2022. This shouldn't be surprising for those who are familiar with rapidly growing firms. Growth requires a lot of talent and other resources, making it an incredibly expensive endeavor.

The good news is that other profitability metrics aren't so bad. After seeing operating cash flows hit negative $410.7 million in 2020, that picture has improved year after year. In 2021, it was positive to the tune of $2.8 million. Last year, it totaled $17.9 million. If we adjust for changes in working capital, the picture would look even better, with the metric improving year over year since 2019. That year, the company had a net outflow of $88.5 million. By 2022, the number had grown to $146.9 million.

Something that is a bit tricky is EBITDA. As you can see in the initial chart in this article, this number is also significantly negative. But if you remove stock-based compensation from the equation, you start to see a trend whereby the metric went from an all-time low of negative $98.2 million in 2019 to a high of $154.4 million last year. This better helps to demonstrate what kind of cash the company is generating. At the same time, an argument could be made that not paying employees with stock-based compensation means that you have to pay them with actual cash. And that does not come cheap.

{kind=link}

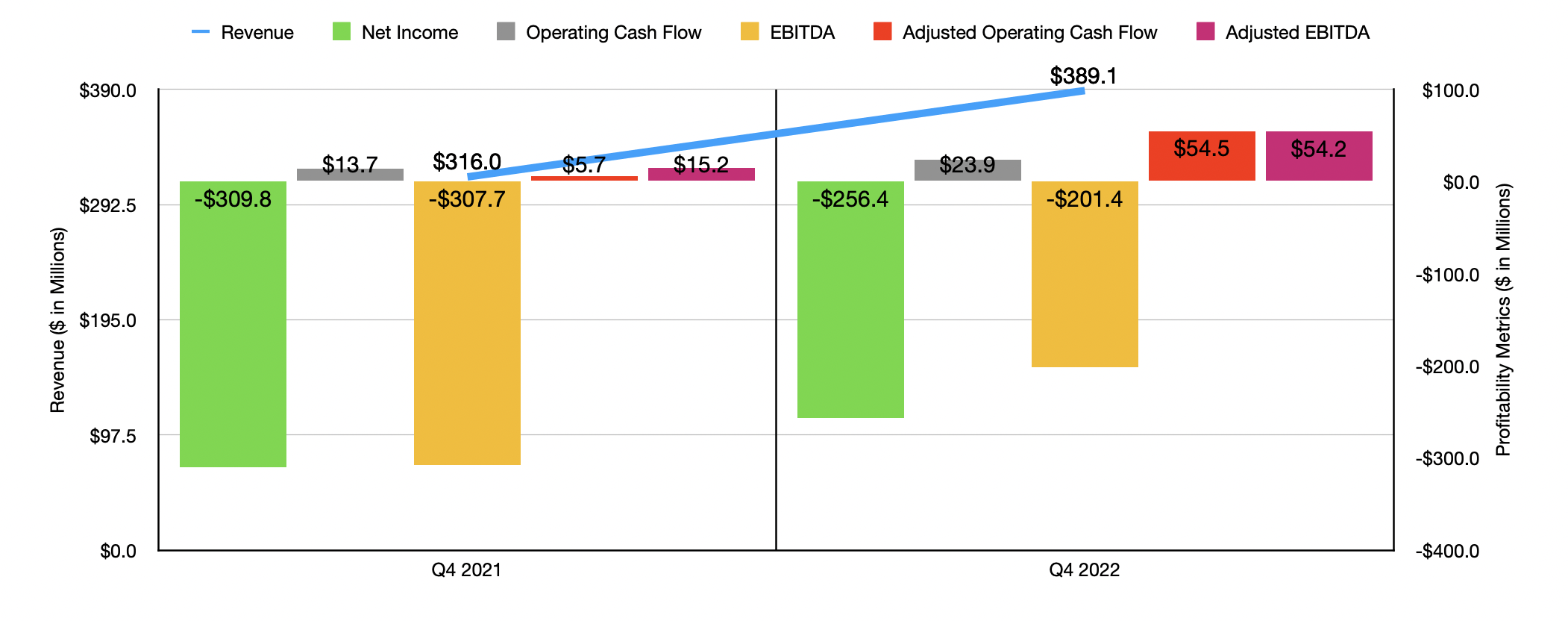

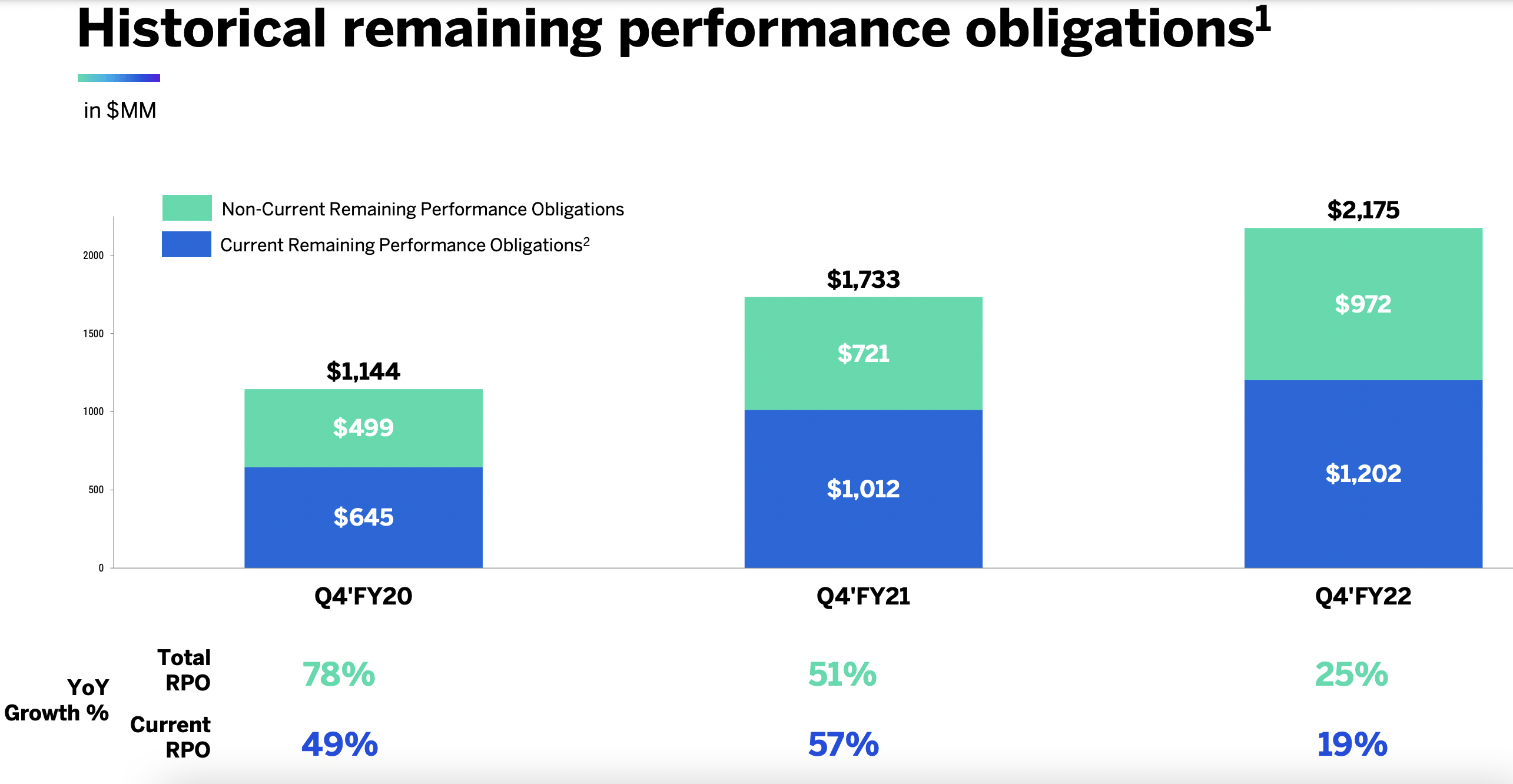

On January 26th, shares of Qualtrics International roared higher, closing up 32.9%. Some of this move higher may stem from the fact that, on January 25th, management announced positive results for the final quarter of its 2022 fiscal year. Sales of $389.1 million came in higher than the $316 million reported at the same time one year earlier. They also beat analysts' expectations by nearly $8 million. Adjusted earnings per share, meanwhile, came in at $0.03, beating what analysts anticipated to the tune of $0.01 per share. As you can see in the chart above, other profitability metrics for the company also fared better year-over-year. Most notably, we have the cash flow figures of the firm. Adjusted operating cash flow totaled $54.5 million. This is compared to the $5.7 million reported one year earlier. A similar year-over-year improvement can be seen when looking at adjusted EBITDA, which rose from $15.2 million to $54.2 million. Meanwhile, in the image below, you can see that the company also reported for the quarter remaining performance obligations, often referred to as backlog, of nearly $2.18 billion. This also represents a significant improvement compared to the same time last year, with year-over-year growth totaling 25%.

{kind=link}

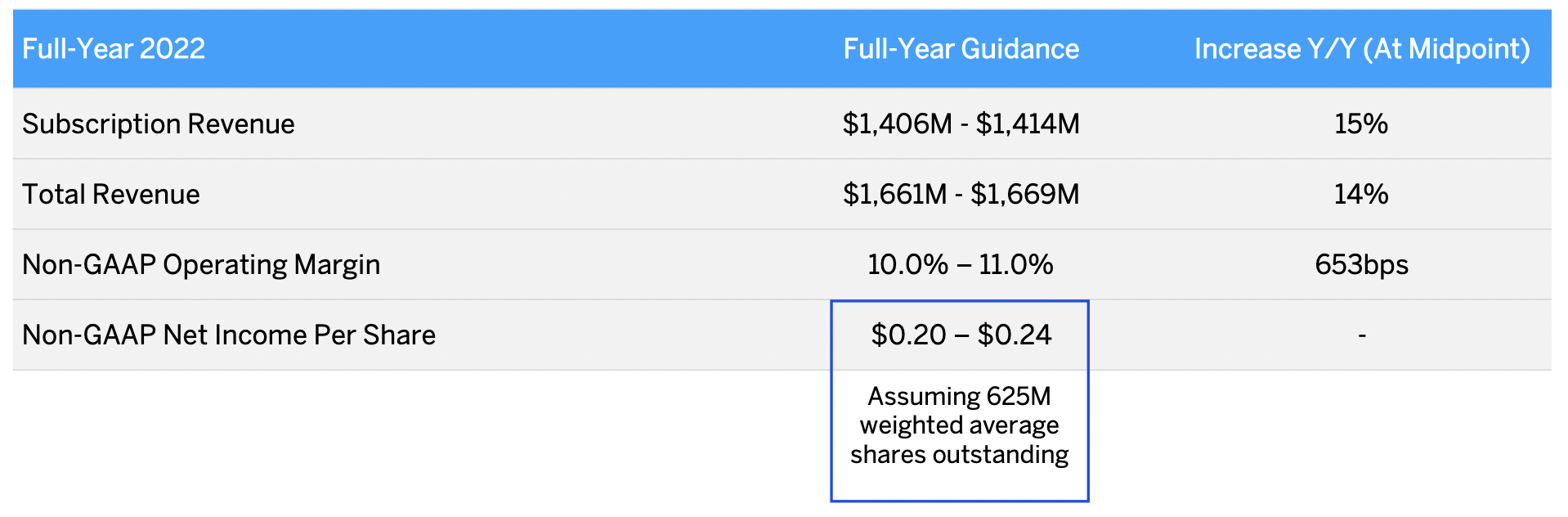

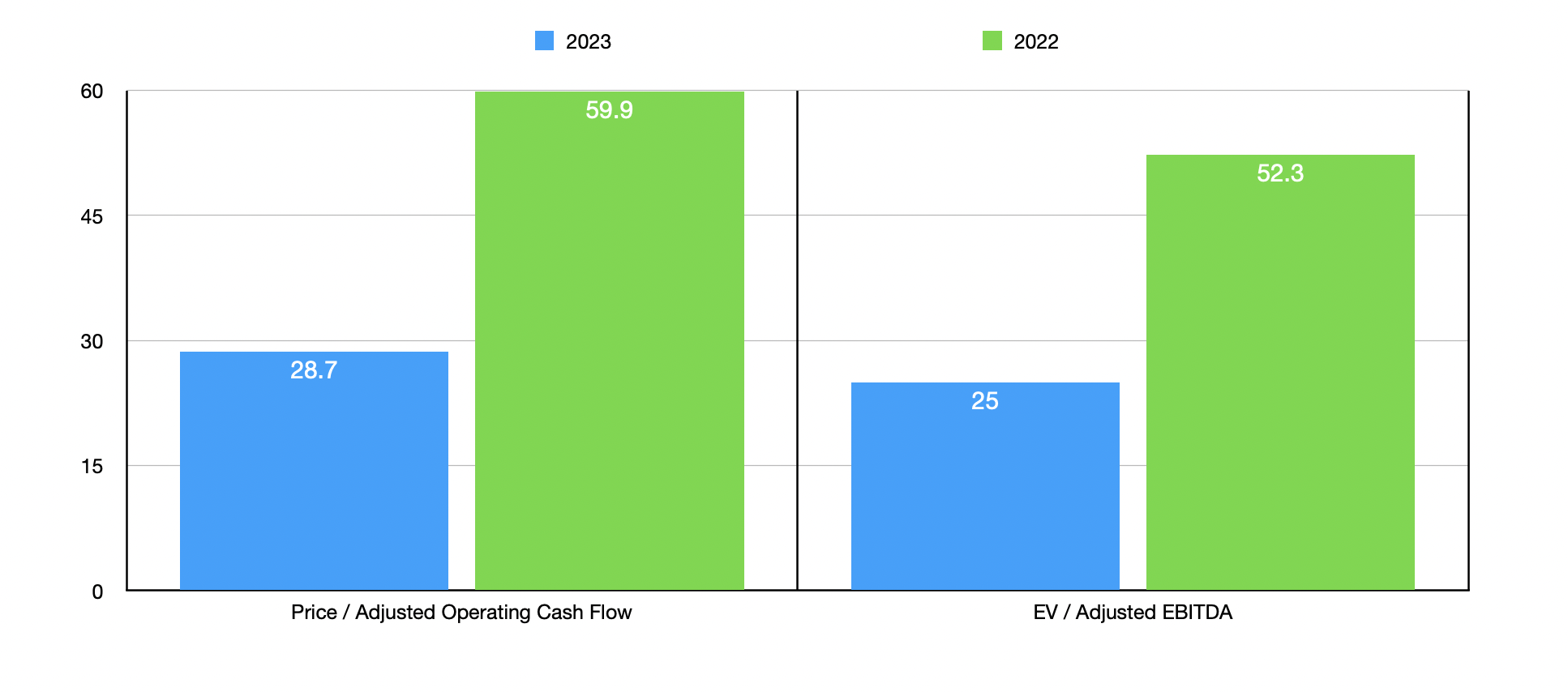

In terms of valuing the company, though, the picture is a bit complicated. Really the only way to value the company is to use the positive cash flow numbers that we have. For 2023, management has said that revenue should come in at between $1.66 billion and $1.67 billion, with the subscription revenue for the company coming in at around $1.41 billion. The company also said that its non-GAAP operating margin should be somewhere between 10% and 11%. If we make certain adjustments there, we should get adjusted operating cash flow for the company of $307.1 million for the year, while getting $322.8 million is a decent estimate for adjusted EBITDA.

Based on these figures, the company is trading at a forward price to adjusted operating cash flow multiple of 28.7 and at a forward EV to EBITDA multiple of 25. By comparison, if we use the data from 2022, these multiples would be 59.9 and 52.3, respectively.

{kind=link}

While the forward-looking numbers aren't awful for such a rapidly growing company, they require an investor to bet on management's guidance for the future. Coming up short on this could prove problematic and would likely result in significant downside for investors. But for better or worse, this or at least some of it may be offset by a different catalyst the company is experiencing.

On January 26th, SAP SE ( SAP ) announced its latest quarterly results. During that time, the company also said that it was exploring a sale of its 71% stake in Qualtrics International. This is in addition to its decision to let go of around 3,000 employees with the aim of saving hundreds of millions of dollars annually. This stake in Qualtrics International is currently worth around $6.25 billion. For shareholders and SAP, it can free up some cash that management might use for other things. As for investors in Qualtrics International, there is the potential, depending on how the transaction is done and whether it's one purchaser or many, for the company to have even greater autonomy and, as a result, to intensify its growth initiatives. It could even theoretically lead to a purchase of the entire business. But at the end of the day, the devil will be in the details there, and we are left wondering until more information comes out.

{kind=link}

Takeaway

Based on the data provided, Qualtrics International strikes me as a rapidly growing company that does have a great deal of potential. The firm currently operates in a market that management estimates to be worth around $60 billion. Growth in the number of large customers is pushing revenue higher and some of the cash flow numbers, while far from perfect, are improving for the enterprise as well. The market likely has been optimistic about the company's recent financial performance.

But the real catalyst seems to have been the news that SAP is likely to sell off its ownership in Qualtrics International Inc. Depending on how that goes could mean a great deal for shareholders. But it also creates additional uncertainty which, when added to how shares are already priced, makes Qualtrics International Inc. a bit rich for my blood.

For further details see:

Qualtrics International: Great Growth, Interesting Catalyst Create Enthusiasm