QLYS - Qualys: Take Your Profits Now

2023-11-29 09:46:32 ET

Summary

- QLYS has surged 20% since earnings, hitting all-time highs.

- It is now priced for expansion of 5-year revenue growth yet management is guiding us to its lowest annual growth rate in history.

- Four different valuation models suggest downside of between 9-18%.

- We rate QLYS stock a SELL at current levels.

Overview

Qualys Inc (QLYS) provides IT security solutions to over half of Fortune Global 500 companies. Their share price has jumped 20% since announcing earnings in early November and is trading at another all-time high. As cybersecurity specialists, Qualys is riding one of the strongest macro themes in the market. The recent run-up in price was an understandable response to yet another beat on both top and bottom lines, maintaining their status as the most profitable of their peers.

But dig into the details and we find evidence that price has overshot fair value by quite some margin. The current price assumes growth will accelerate from historical rates, yet net new client numbers are stagnant and their preferred measure of revenue growth for existing clients has been falling since 2022. Most importantly, management themselves are guiding down our expectations of future revenue growth.

Four different valuation models indicate the stock is overvalued by 9-18%. Moreover, the primary factors that most influence QLYS share price are all trading at levels that have historically been sensible short-term exit points.

Qualys has overrun fair value on several occasions in the past ten years and has pulled back each time. This report contends that we're witnessing the most extreme period of overvaluation in its history.

Qualys has a well-regarded product suite and will continue to grow over time, but our view is there will be better entry points in the future. Take your profits now. We rate QLYS stock a SELL at current levels.

A Well-Received Earnings Report

Let's set the scene with their recent earnings update from early November.

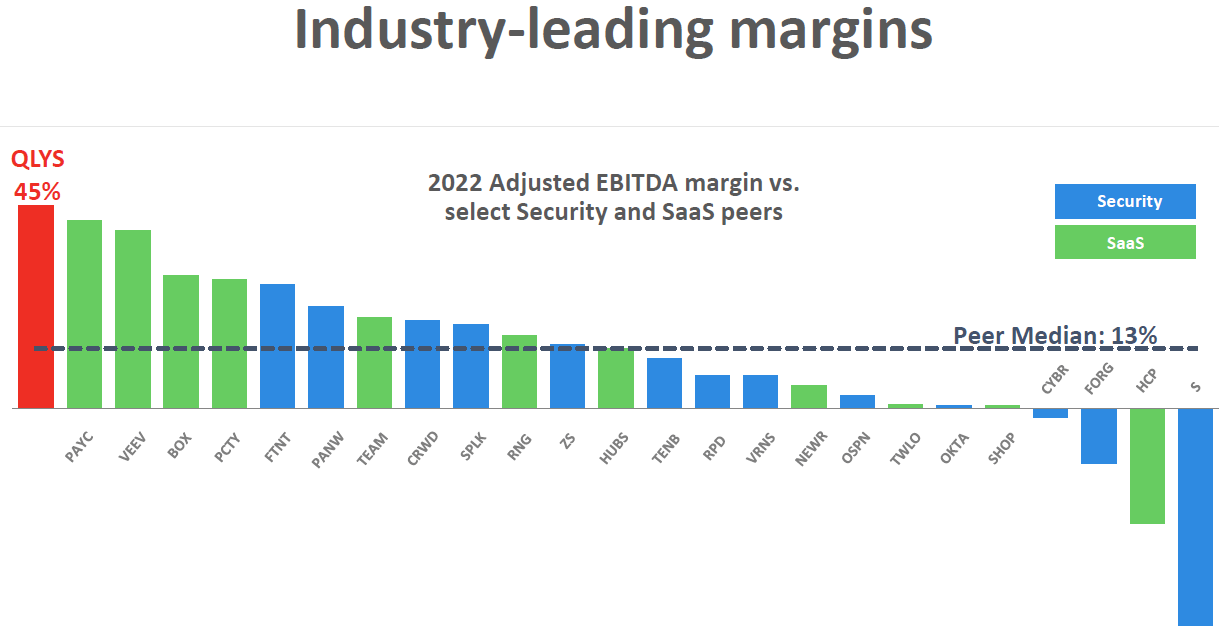

On the revenue side, Qualys reported $142 million - a minor $1 million beat. On the earnings side, they reported EPS of $1.51 - a huge $0.38 beat. These numbers help to maintain their status as the most profitable of their peers.

QLYS Peer EBITDA Margins (QLYS Q3 2023 Earnings Presentation)

{kind=link}

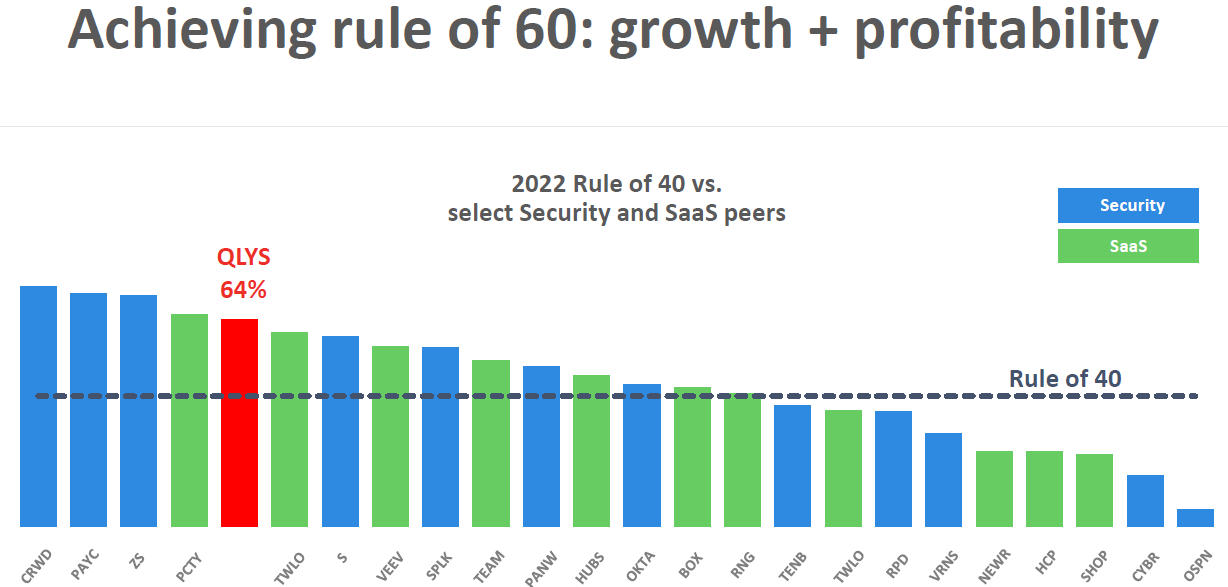

Perhaps more notably, it lands them in a group of companies delivering growth and profitability margins that sum to over 60%. The more common 'Rule of 40' is discussed at length in this excellent article and shows companies passing this screen have delivered extraordinary value for shareholders over many years. Rarefied air indeed.

Rule of 40 Chart (QLYS Q3 2023 Earnings Presentation)

{kind=link}

Adding to the good news, QLYS continued share buybacks during the quarter, delivering yet more value to shareholders, and confirmed there is more to come.

There are no credit risks to note. QLYS is sitting below the industry median for the Debt/Equity Ratio; and because of the interest income generated on their cash balance, they have no interest cost to cover on the debt they do have.

On the back of this earnings update, 15 of the 22 analysts covering QLYS increased their 12-month price targets.

So what's not to like? Let's dive in.

The 'Sell' Case

Revenue side

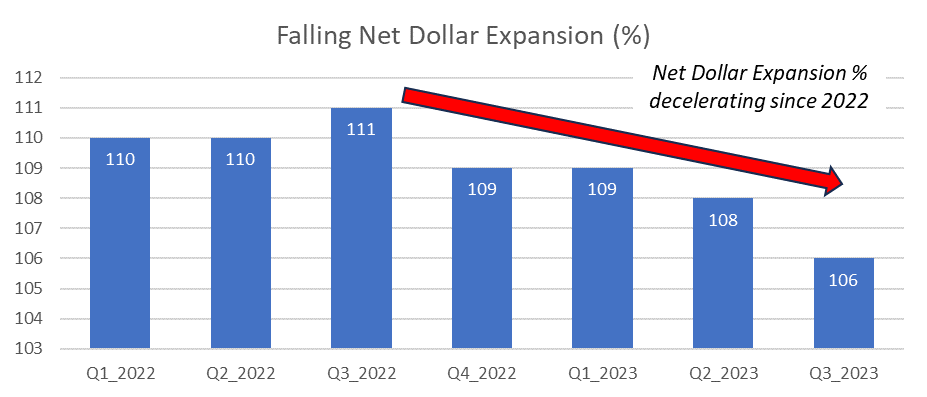

Revenue growth from existing customers is decelerating, as per Qualys' preferred measure of 'net dollar expansion' (percentage change in revenue over the period plus upsells). Anything above 100% signals growth from existing customers; under is contraction. As per the chart below, the uplift from existing customers has been trending down since the high in 2022. It is still positive, but the trend is unmistakable. CFO Joo Mi Kim stated this is likely due to customer budget constraints and they " believe ongoing budget scrutiny will linger for the foreseeable future ". My read on this comment is they are not expecting any uptick in this measure any time soon.

Net Dollar Expansion % (FactorRank analysis based on past earnings transcripts)

{kind=link}

As well as revenue challenges from existing customers, QLYS is not winning new customers, as per CFO Kim's comment during the earnings call - "new growth remains challenging... our customer count is kind of flat". In explaining this lack of growth, management cited challenging macro conditions and the "underinvestment that we had this year" in sales and marketing.

So are they doing anything about this underinvestment in sales? CFO Kim is expecting an "acceleration in sales and marketing investments" in 2024, but Qualys has an unused 2023 budget in this area that could be used immediately.

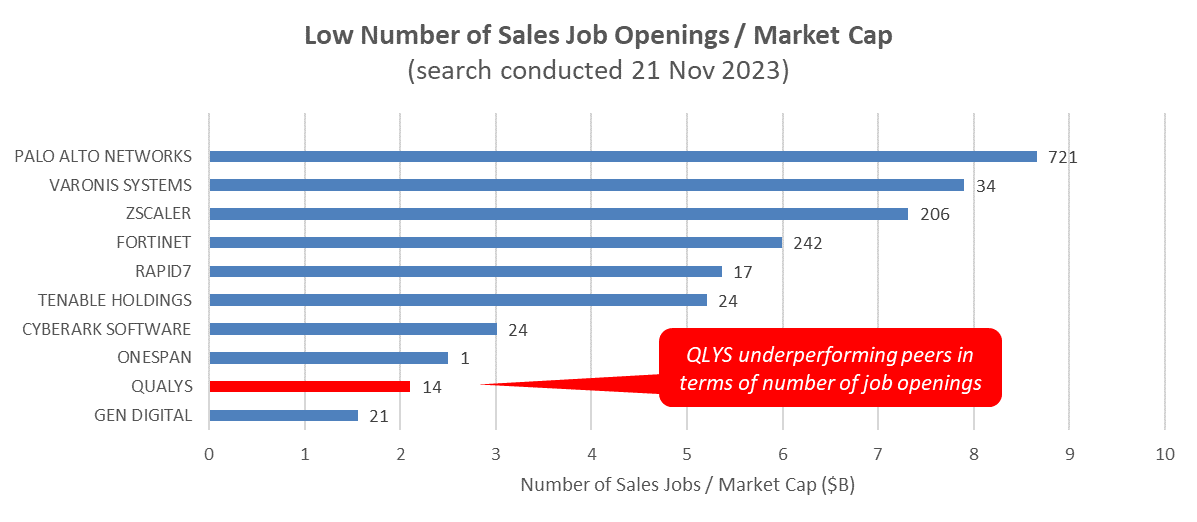

To get some insight into Qualys' focus on sales growth I had a quick look at their sales job openings against their peers in the 'security software' sector. On this measure (which I accept is pretty blunt) QLYS has the second lowest number of sales job openings as a percentage of market cap. To the extent that the market cap embodies future growth expectations, it appears QLYS is continuing to underinvest in sales and marketing.

Sales Job Openings as % of Market Cap (FactorRank analysis based on jobs posted on company websites)

{kind=link}

Given the onboarding time for new hires and 'extended sales cycles' that CFO Kim cited in Q2, it could be some quarters before we see a meaningful tick-up in new customer numbers.

In the meantime, CFO Kim is guiding fourth-quarter revenue expectations down to an annual growth rate of 10% to 11%. When was the last time QLYS delivered revenue growth this low? Never! I looked at 10 years of history and the next lowest was Q4 2020 when they delivered a very COVID-impacted 12%.

In an environment where global cybersecurity industry growth is trending above 12% , falling revenue guidance suggests real macro challenges for QLYS customers, higher-rated competition ( Tenable , CrowdStrike ) for Qualys, and ultimately margin compression. This guidance is not factored into the price, in our opinion. As per our later valuation analyses, the current price assumes an expansion of historical revenue growth rates, not a contraction.

Earnings side

The EPS beat was strong, but we argue the outperformance was not from revenue surprises or good expense management. The primary drivers of their EPS beat were light operating expenditures from their underinvestment in sales and marketing, an accounting change that delivered a lower expected tax rate, and a slightly lower share count from buybacks. Other than buybacks, these are one-time items.

With sales investment expected to increase next year, it's unlikely we'll see more EPS beats like this without a re-acceleration of revenue growth. But as we've seen, guidance for revenue growth is down, not up.

Market Response

Analysts have responded by increasing their target price, but the disconnect between the QLYS price and analyst consensus is now the most extreme in its history. Previous extremes such as this have been sensible points to exit.

The market, however, continues to push the price higher. The current price now assumes not just a continuation of sales growth from the past five years, but an expansion . This is not the guidance we're getting from management. Something must give - either guidance reverses or price drops. History suggests the latter.

The 'BUY' Case

Notwithstanding the views discussed in The Sell Case , there are several possible catalysts that could generate new business for Qualys and underpin a reversal in revenue guidance. This sector is, after all, one of the strongest macro plays in the market.

Management cited budgetary constraints as one of the primary reasons for deceleration in net dollar expansion. To the extent this is interest rate driven, a period of falling rates may trigger a recovery. However, Wall St remains divided when that will be.

An increase in the volume of cyber events may force companies to adopt detection and remediation capabilities sooner than they've budgeted for. According to Deloitte, 22% of executives have already experienced at least one cyber event targeting their financial data. As this number grows so will the readiness to invest in protection.

In the meantime, data privacy laws may force companies to spend anyway. Europe is leading the charge here, with their data privacy laws ((GDPR)) regarded as the ' gold standard ' for the regulation of data protection. In place since 2018, the laws impose massive fines on companies for data breaches, the largest (so far) being Meta at $1.3 billion . As more businesses look to protect themselves from data breaches (and potential fines), they may conclude that despite budgetary constraints it makes sense to invest in appropriate IT security capabilities and find budget savings elsewhere.

Even without an increase in direct sales, growth of the 'Partner' channel (aka introducing brokers) may help to re-accelerate sales growth. However, we note that at this stage the contribution to revenue from this channel was flat QoQ.

In summary, our view is that all these upside risks will play out over time. The question is which companies will win - the competition is fierce for both talent and customers.

That said, after a period of consolidation we expect QLYS to continue its growth trajectory. But in the meantime, it has overrun fair value.

Valuation Summary

Fair Value Comparison Across Valuation Models (FactorRank analysis)

QLYS is trading well above fair value levels implied by four different valuation models.

Factor valuation implies a 9% downside with the four leading factors trading at levels that have previously been sensible short-term exit points.

DCF valuation implies an 11% downside using revenue growth projections provided by QLYS guidance.

Against peers, QLYS is trading higher than its 5-year averages despite lower forward guidance; relative peer valuation implies almost a 12% downside from here.

Street valuation implies an 18% downside, the lowest level in history and the first time there are more analysts with 'sell' vs 'buy' ratings.

On this basis, we rate QLYS stock a SELL at current levels.

The following sections in this report discuss each of these valuation models in more detail.

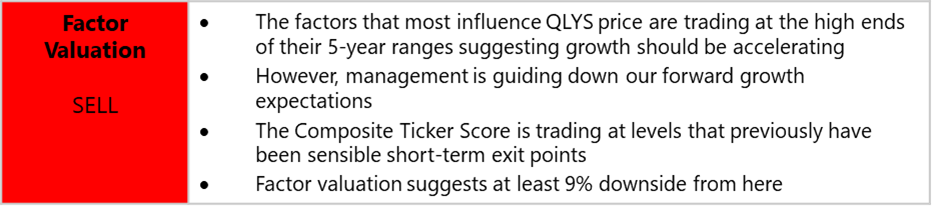

Factor Valuation

Factor Valuation Summary (FactorRank analysis)

{kind=link}

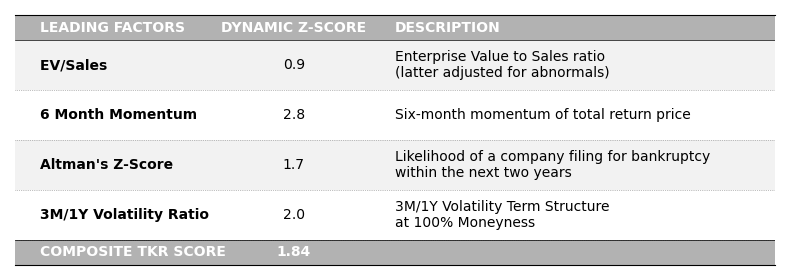

We analysed 34 different factors to determine the top four (table below) that most influence QLYS share price. It's interesting to see Altman's Z-score and 3M/1Y Volatility Ratio in the mix as these don't often make lists of leading factors.

All four factors are trading at high Dynamic Z-Scores, levels that have previously shown to be sensible short-term exit points. For brevity, the individual factor charts are not shown in this report but are available on request.

QLYS Leading Factors (FactorRank analysis)

{kind=link}

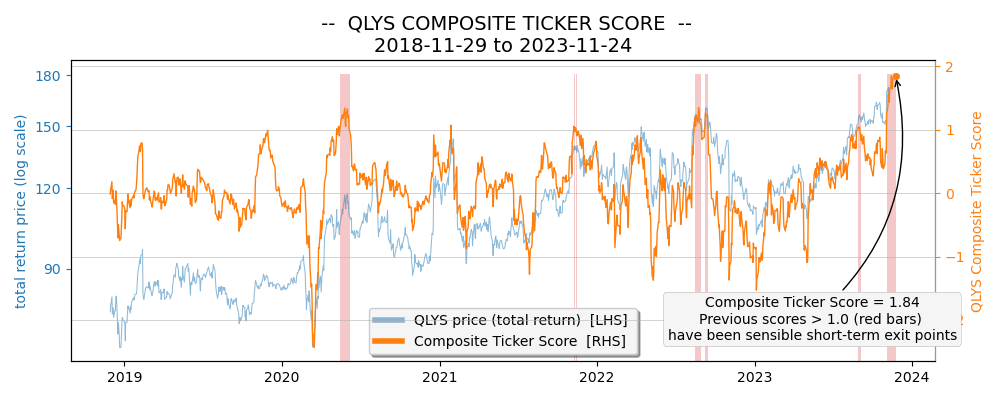

When we combine these four factors into a Composite Ticker Score (orange line below) we can see that previous scores above 1.0 (red bars) have generally been sensible short-term exit points. At the time of writing, we're sitting at +1.8 which is compelling support for the SELL investment thesis.

QLYS Composite Ticker Score (FactorRank analysis)

{kind=link}

The only fundamental factor in our list of Leading Factors is EV/Sales. Looking at the table below, we can see that the average 5-year multiple on EV/Sales is 10.4. At the time of writing, we're sitting at 11.5. If the multiple returns to 10.4 the implied share price is $163.43, or a fall of 9.4%.

Factor-Based Implied Share Price (FactorRank analysis)

{kind=link}

However, Qualys management is guiding us towards even lower sales growth than the past 5 years, so we can expect even more downside. On this basis, we assign a 'SELL' rating to the Factor Valuation component of the analysis.

DCF Valuation

DCF Valuation Summary (FactorRank analysis)

{kind=link}

Our discounted cash flow analysis generates an equity value of $160.60, or 11% downside from the current price. We use the following assumption set to arrive at this outcome:

- Forward annual revenue growth of 10.5% (mid-point of QLYS guidance)

- Future tax rate of 21% (as per QLYS guidance)

- Operating expenses (as a percentage of sales) increases five percentage points (from 55% to 60%) due to QLYS' stated expectation of higher investment in sales and marketing

- Terminal value calculation uses the EV/Sales ratio as this is one of the primary factors influencing QLYS stock price

- Terminal value multiple falls from 10x (5-year average) to 9x to reflect QLYS expectations of lower future growth and increasing competition

- WACC of 12.5%

With 11% downside, we assign a 'SELL' rating to the DCF Valuation component of the analysis.

Relative Peer Valuation

Relative Peer Valuation Summary (FactorRank analysis)

{kind=link}

Peer group members are from the same industry, show strong correlation and/or cointegration, and have good data quality. The peers for this analysis are QLYS, CRWD, CYBR, MSFT, NOW, ORCL, PANW, RPD, TENB, VRNS, and ZS.

Across both metrics analyzed, QLYS is trading higher than its 5-year average relative to peers:

Historical Range Chart (FactorRank analysis based on peer data)

A quick interpretation of this range chart using forward EV/Sales ratio (bottom line) as an example: During the past 5 years QLYS traded at a 3% premium to peers on this measure; during this period it ranged between a 28% discount and a 51% premium to peers; it is currently trading at an 11% premium after lifting 8 percentage points.

Given management is guiding down our future revenue expectations the best outcome we can hope for is a return to the 5-year average EV/Sales multiple of 8.6 (table below).

Relative Value-Based Implied Share Price (FactorRank analysis based on peer data)

{kind=link}

Using forward EV/Sales as a guide, we get an implied share price of $159.31, or a fall of 11.7%. On this basis, we assign a 'SELL' score to the Relative Peer Valuation component of the analysis.

Street Valuation

Street Valuation Summary (FactorRank analysis)

{kind=link}

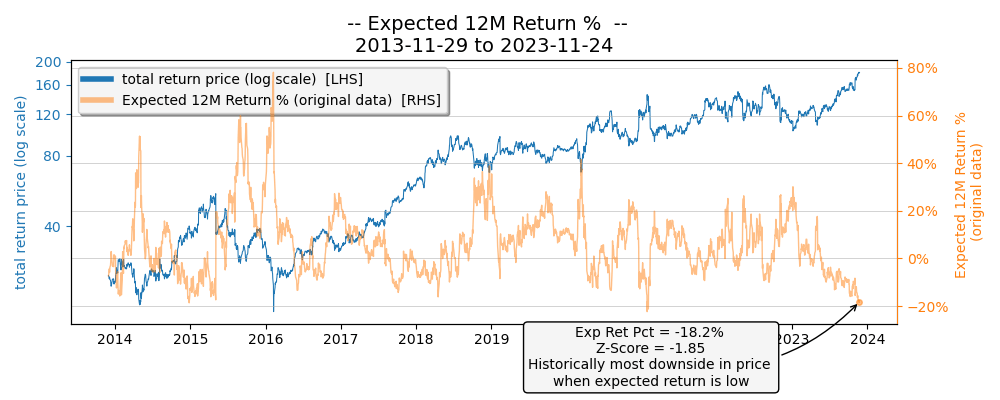

17 analysts have updated their target prices and ratings since QLYS reported Q3 earnings. At the time of writing, we are witnessing two 'firsts' for QLYS:

- Expected 12M return data suggests at least 18% downside which is the lowest expected return in the company's history.

- This is the first time in the company's history that there are more analysts with sell than buy ratings.

As the chart below shows, previous downside extremes of this metric (orange line) have been sensible short-term exit points.

On this basis, we assign a 'SELL' rating to the Street Valuation component of the analysis.

QLYS Expected 12M Return % (FactorRank analysis based on analyst target prices)

{kind=link}

Final Thoughts

Qualys is clearly a strong company offering a well-regarded product to a customer base that knows they need a solution. They are riding a theme that is one of the strongest macro plays in the market. Despite, or perhaps because of this strength, they are currently overvalued - the most overvalued in their history. Previous instances of overvaluation have resulted in periods of pull-back. We contend this is another of those periods, and that there will be better entry points in the future. We rate QLYS a Sell at current levels.

For further details see:

Qualys: Take Your Profits Now