NX - Quanex Building Products: Trading In-Line With Peers

2023-05-14 04:15:34 ET

Summary

- Quanex faces uncertainty due to high-interest rates and a slowing economy.

- The dividend yield is too low for this interest rate environment, and the company has not grown it in three years.

- The stock may revisit its 52-week lows when the market volatility returns.

Quanex Building Products ( NX ) plays in a competitive market with much pricing pressure and a lack of a moat. The company faces short-term uncertainty due to a slowing economy, and much may depend on the direction of the interest rates in the second half of 2023. The company has a good balance sheet but offers a low dividend yield and has failed to raise its dividend over the past three years. The company is cheaply valued but trades in line with its peers. Any near-term increase in market volatility due to further slowing of the economy or the debt-ceiling debate may offer a better entry point for this stock.

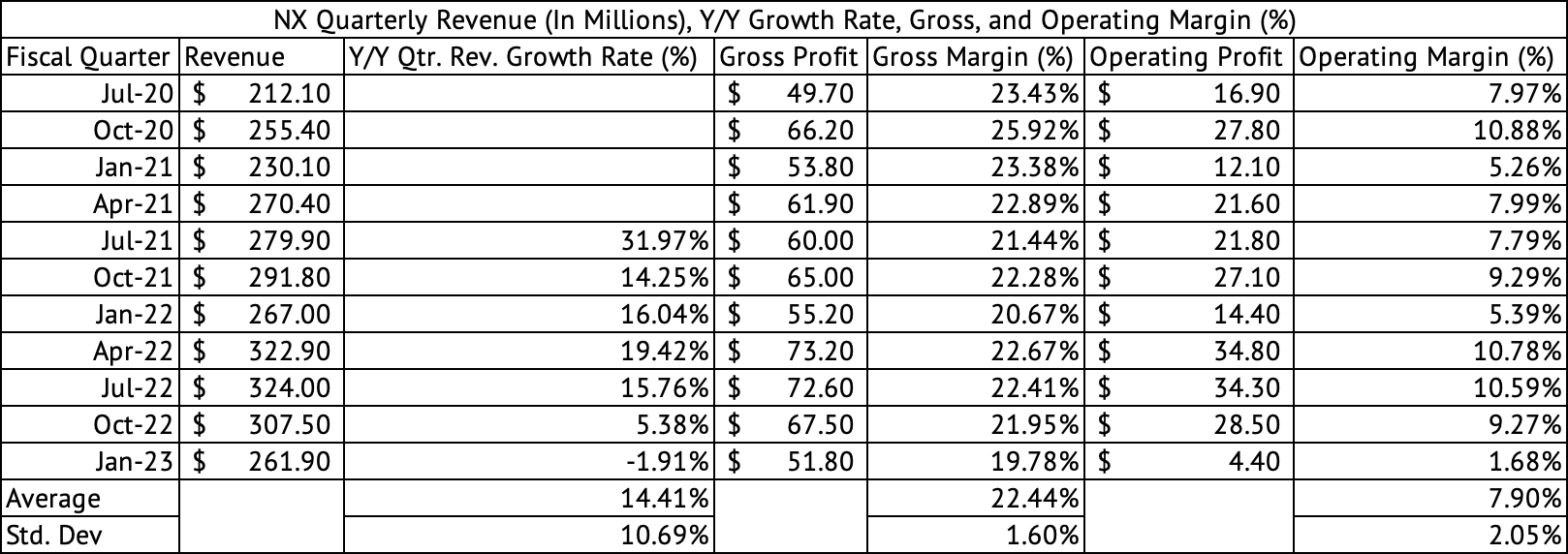

Declining Revenue

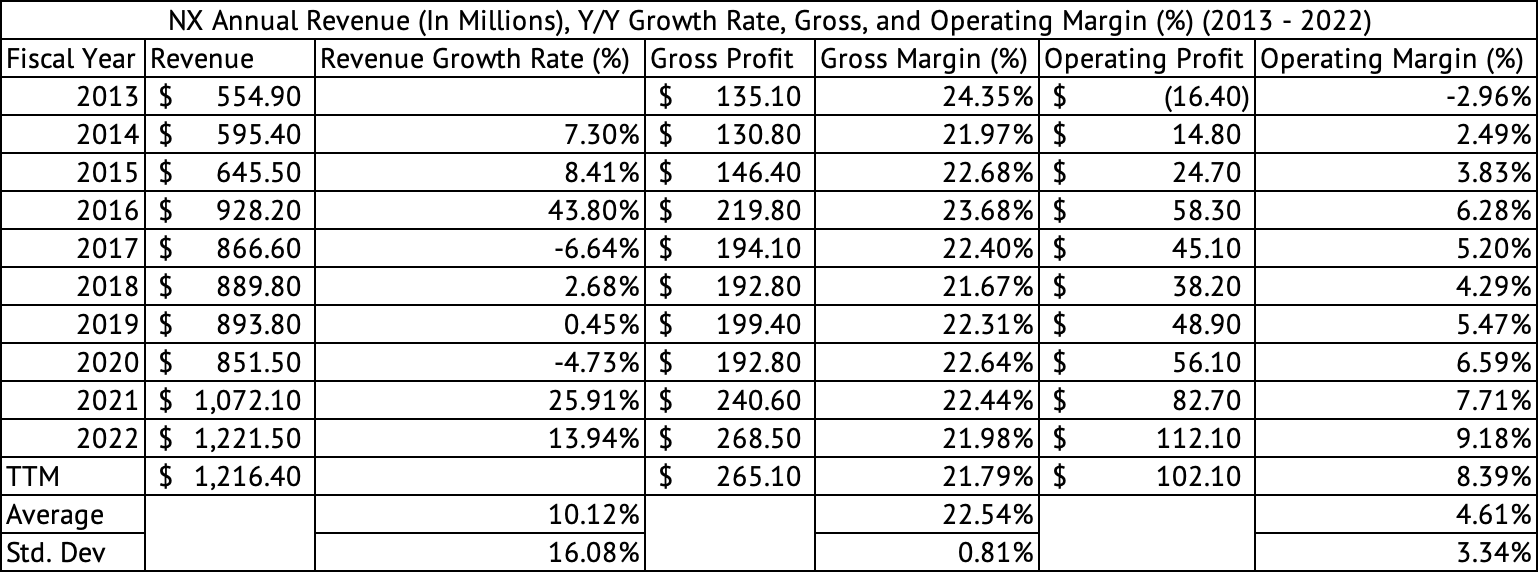

The company saw its revenue decline by 1.9% y/y in the quarter ending January 2023 (Exhibit 1) . Its gross margins for the quarter declined below 20%, reaching 19.7% compared to its average of 22.4% since July 2020. The company has averaged a gross margin of 22.5% over the past decade, with a low standard deviation of 81 basis points (Exhibit 2) .

Exhibit 1:

Quanex Building Products Quarterly Revenue, Gross, Operating Profit, and Margins (%) (Seeking Alpha, Author Compilation)

{kind=link}

Exhibit 2:

Quanex Building Products Annual Revenue, Gross, Operating Profit, and Margins (%) (Seeking Alpha, Author Compilation)

{kind=link}

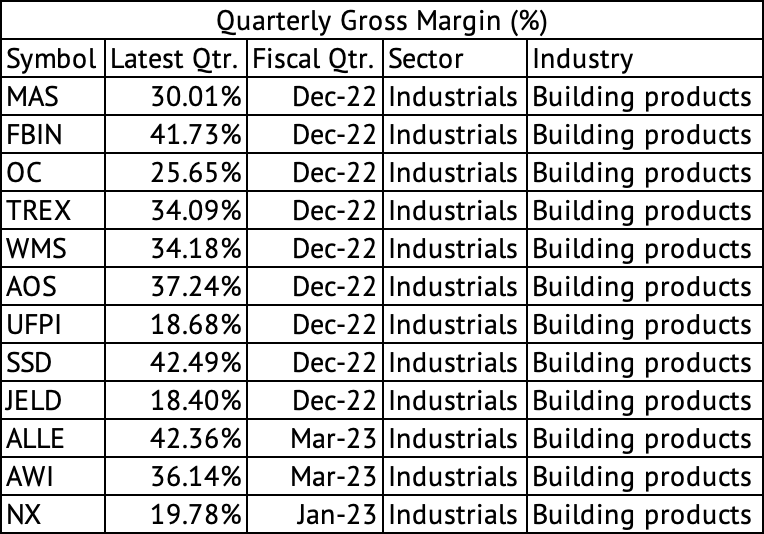

In my recent analysis, I rated both JELD-WEN Holding ( JELD ) and UFP Industries ( UFPI ) a hold. The company's gross margins are much closer to JELD-WEN Holdings and UFP Industries, which had 18.4% and 18.6% in gross margins, respectively, in the most recent quarters (Exhibit 3) . However, given its high debt load, JELD-WEN Holding may be the weakest company in the lot.

Exhibit 3:

Quarterly Gross Margins of Building Products Companies (Seeking Alpha, Author Compilation)

{kind=link}

The company is scheduled to report its Q2 earnings on June 2 . The consensus estimate is for the company to report $270.43 million in sales for the quarter, which would be a q/q increase but a decline of nearly 16% from its April 2022 quarter. But, the company is coming off of solid revenue growth in 2021 and 2022, making for tough comparisons in 2023.

Investors should expect further moderation in growth and a return to normalcy (low-single-digit growth) over the long term. A sluggish economy and high-interest rates have increased the risk of a further decrease in revenue in 2023. The direction and the level of interest rates in the U.S. is unclear. If inflation continues to soften, but the economy weakens dramatically with an increase in the unemployment rate, the Federal Reserve may be forced to cut rates and may provide a much-needed boost to the housing sector.

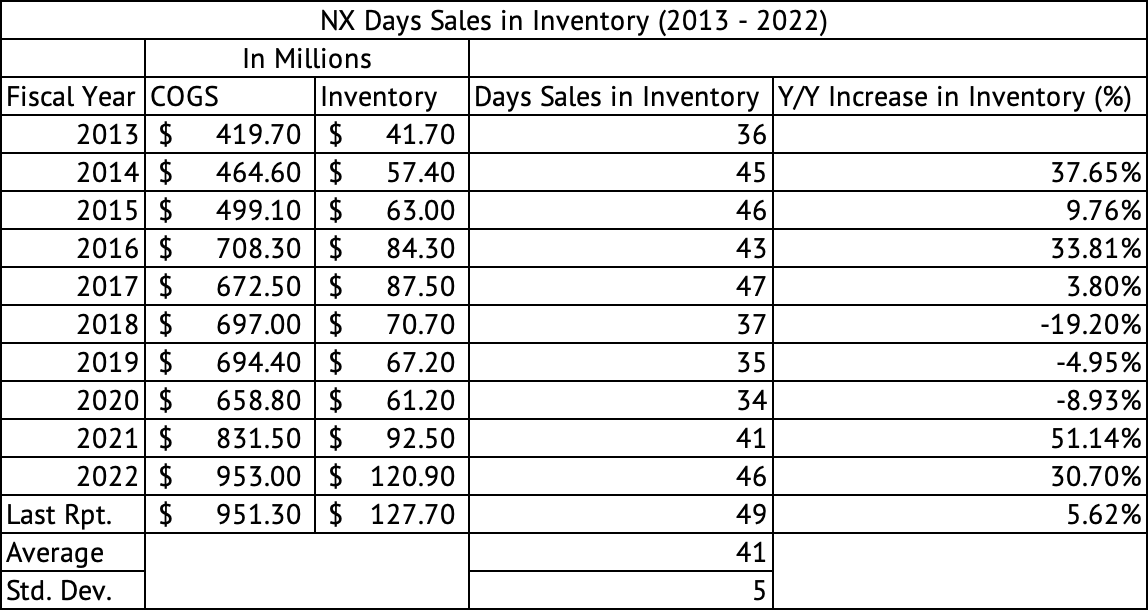

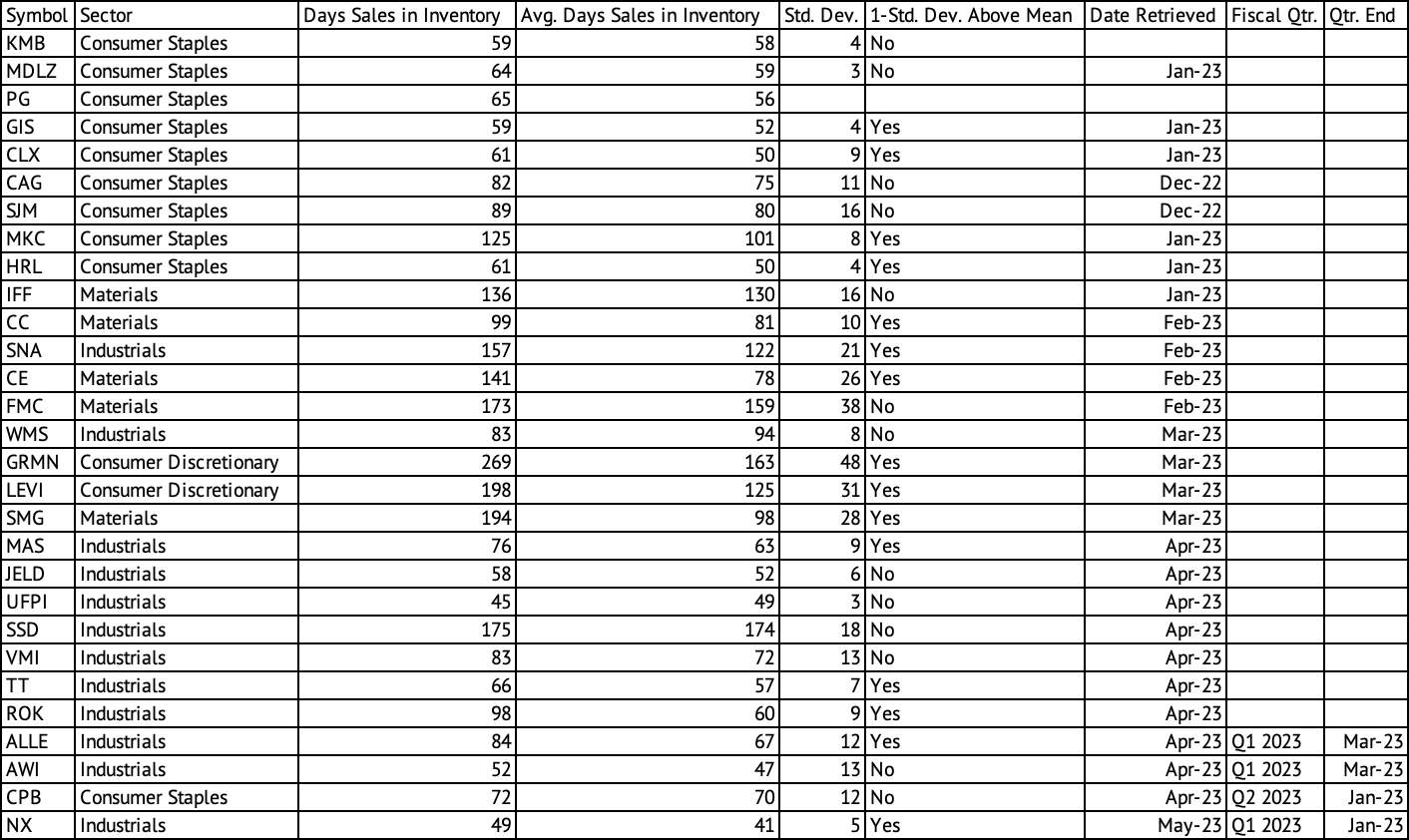

High inventory costs

Quanex's carrying cost of inventory has increased since 2022. As of Q1 2023, which ended in January, the company carried about 49 days of inventory compared to its average of 41 days with a standard deviation of 5 during the past decade (Exhibit 4) . The company's current inventory carrying costs exceed one standard deviation from its mean. These higher-than-average costs may take a while to work through. But, their inventory costs have likely peaked. They may provide tailwinds to their cash flows in the coming quarters.

Exhibit 4:

Quanex Building Products Day's Sales in Inventory (Seeking Alpha, Author Calculations)

{kind=link}

Many companies across various sectors of the economy have experienced high inventory-carrying costs (Exhibit 5) . Still, at the same time, these same companies did not anticipate the dramatic slowdown in business when consumers pivoted from spending on products to services. The overall economic downturn will cause additional concern as the U.S. GDP grew at a 1.1% rate in Q1 2023 compared to a 2.6% rate in Q4 2022. The Atlanta Fed's GDPNow forecast a somewhat optimistic 2.7% for Q2 2023 as of May 8, 2023.

Exhibit 5:

Day's Sales in Inventory Across Consumer Staples, Consumer Discretionary, and Industrial Companies (Seeking Alpha, Author Calculations)

{kind=link}

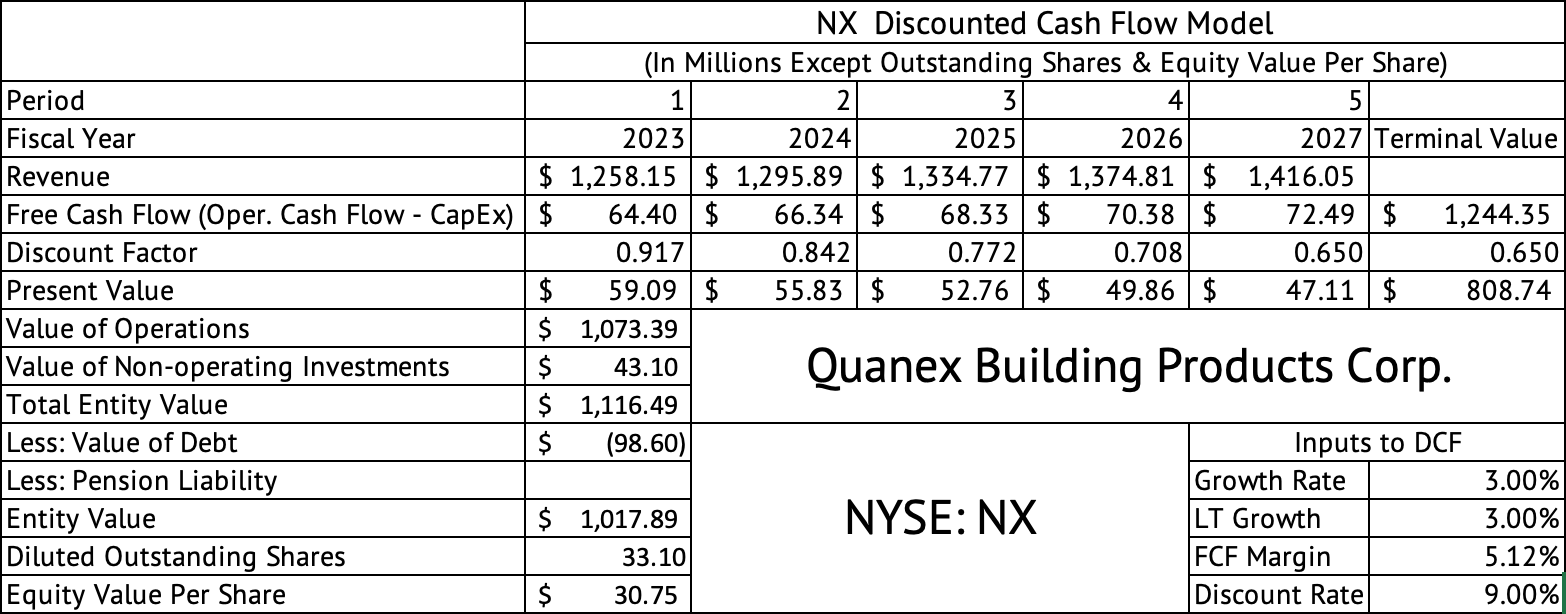

Stock may be undervalued for a reason

Quanex is undervalued by every measure. It trades at a forward PE ratio of 11.3x compared to the sector median of 18x. It trades at a forward price-to-sales ratio of 0.5x. The stock trades at $20. A discounted cash flow model estimates the per-share equity value at $30 (Exhibit 6) . This model assumes a growth rate of 3%, a free cash flow (operating cash - CapEx) margin of 5.1%, and a discount rate of 9%. The free cash flow margin used in the model is its average over the past decade.

Exhibit 6:

Quanex Building Products Discounted Cash Flow Model (Seeking Alpha, Author Calculations)

{kind=link}

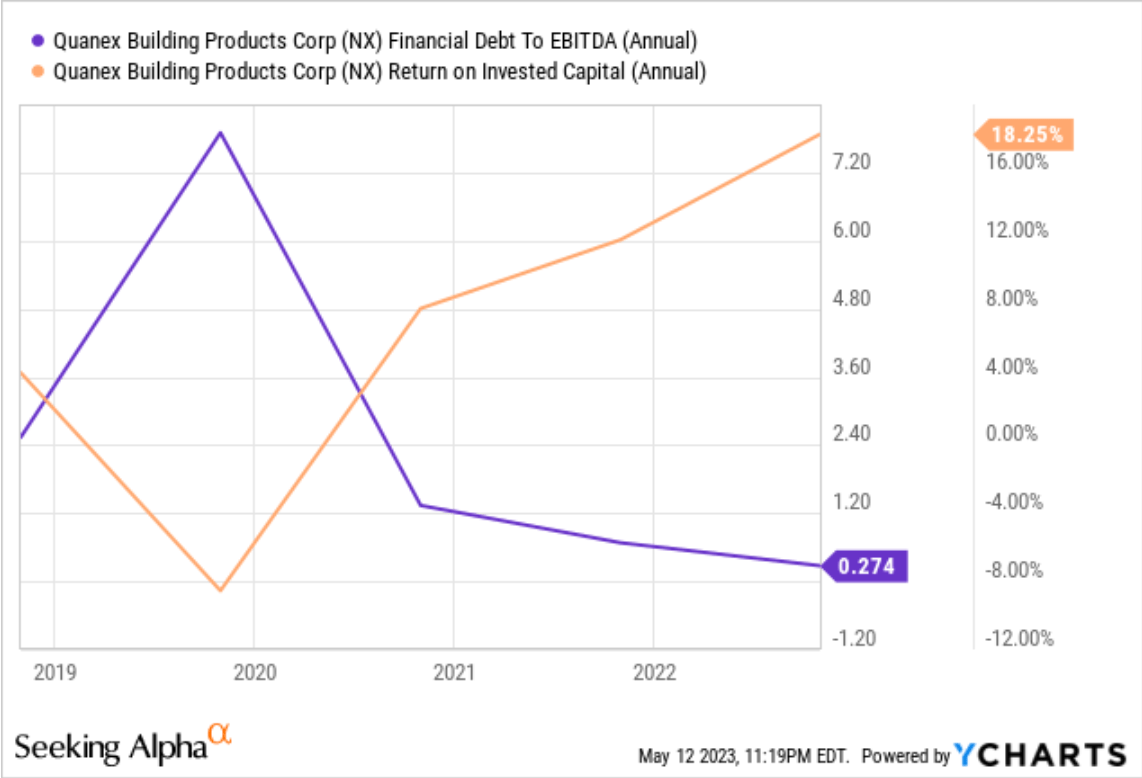

The company has a low debt-to-EBITDA ratio of 0.27x (Exhibit 7) . It has total debt of $98.6 million and a net debt of $55.5 million. The company generated a good return on invested capital of 18%, far exceeding its cost of capital. But the question remains can the company consistently generate good returns in every economy? The answer is probably no; a recession may take a toll on the company's revenue and profitability, adversely affecting its returns. That may be the primary reason why the stock is cheaply valued.

Exhibit 7:

Quanex Building Products Debt-to-EBITDA Ratio and ROIC (Seeking Alpha)

{kind=link}

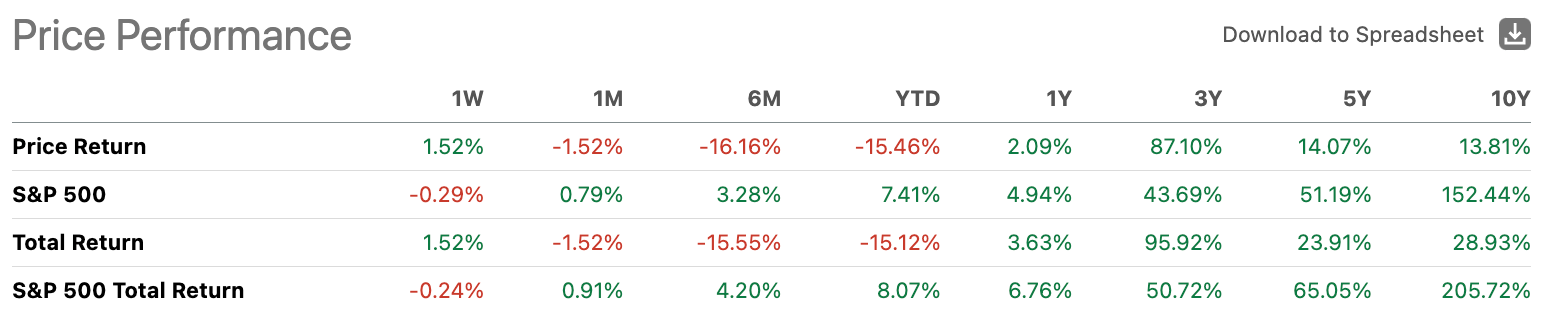

The company has admitted, based on research done by a third-party firm , that the market for windows in the residential remodeling & replacement market is projected to grow at a 2% pace in 2023. Similarly, the demand for cabinets is projected to slow in 2023. The company is susceptible to uneven cash flows due to its dependency on the repair and remodel market, which is subject to changes in consumer spending. The last three years were good for the company, and the good times may be ending with a return to anemic growth rates. Over the past three years, the company has had a total return of 95% compared to the 50% return for the S&P 500 Index ( SP500 ) (Exhibit 8) . Over the past year, the company has fallen behind the S&P 500 Index with a total return of 3.6% compared to 6.7% for the S&P 500 Index.

Exhibit 8:

{kind=link}

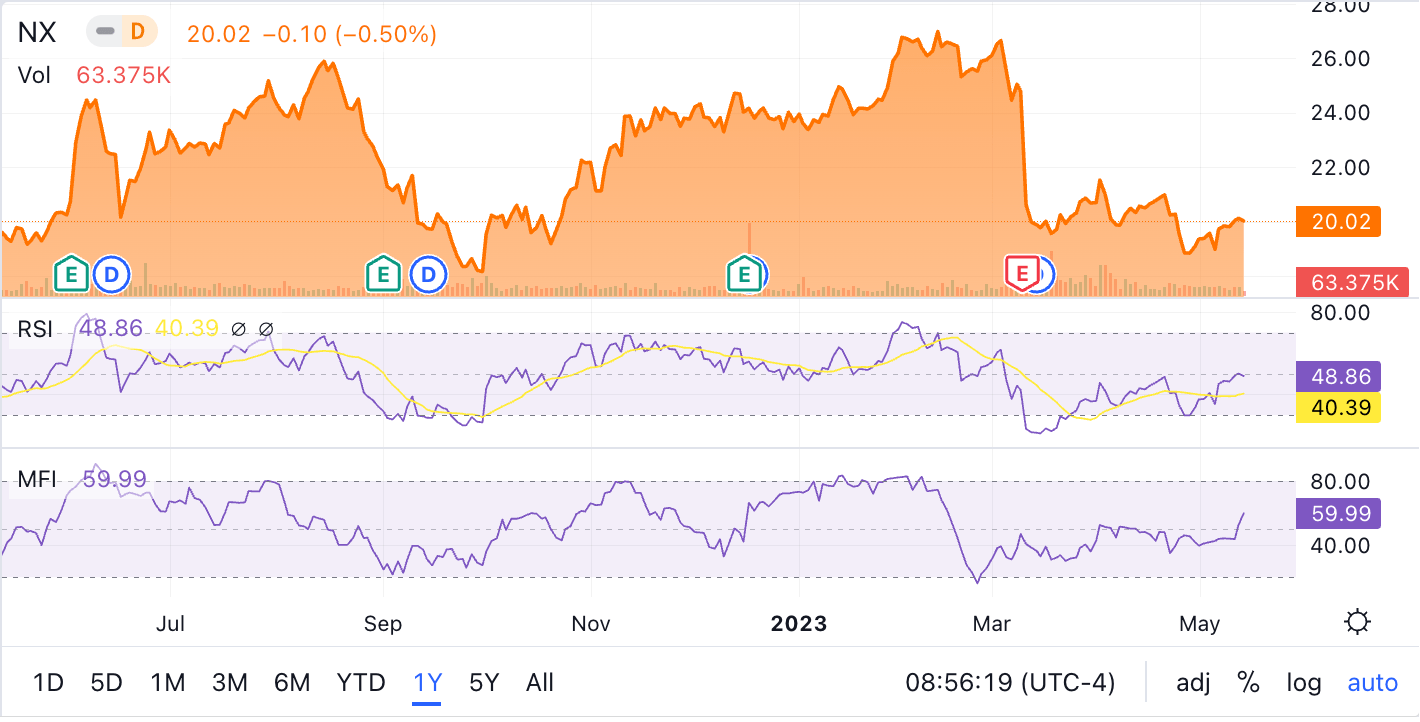

The stock has come under heavy selling pressure over the past three months, with a decline of 23% . The RSI and MFI technical indicators show that the stock may have bottomed in March (Exhibit 9) . Buying opportunities in the stock may emerge soon if the market's volatility increases due to the economic uncertainty and the stand-off over debt-ceiling increase. The S&P VIX Index ( VIX ) is currently at 17, which may be too subdued given the market uncertainties.

Exhibit 9:

Quanex Building Products RSI and MFI Technical Indicators (Seeking Alpha)

{kind=link}

Low dividend yield

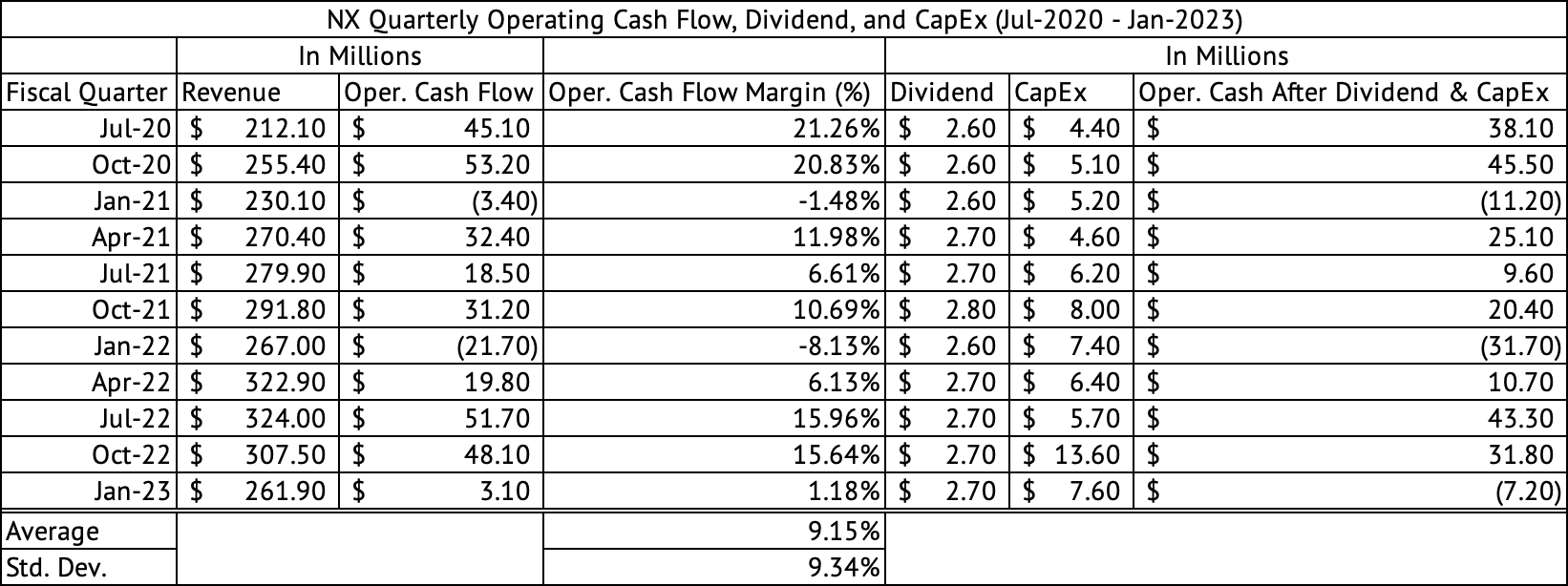

The dividend yield is another reason not to own the stock or add to existing holdings. The stock has a dividend yield of 1.6%. Unfortunately, this low yield is in line with the sector median. The Vanguard Industrials Index ETF ( VIS ) and the Vanguard S&P 500 Index ETF ( VOO ) have lower yields of 1.1% and 1.2%, respectively. The company's payout ratio is 12.7%, a conservative figure. The company paid $10.8 million in total dividends over the past twelve months while generating $122 million in operating cash flow (Exhibit 10) .

Exhibit 10:

Quanex Building Products Operating Cash Flow (Seeking Alpha, Author Compilation)

{kind=link}

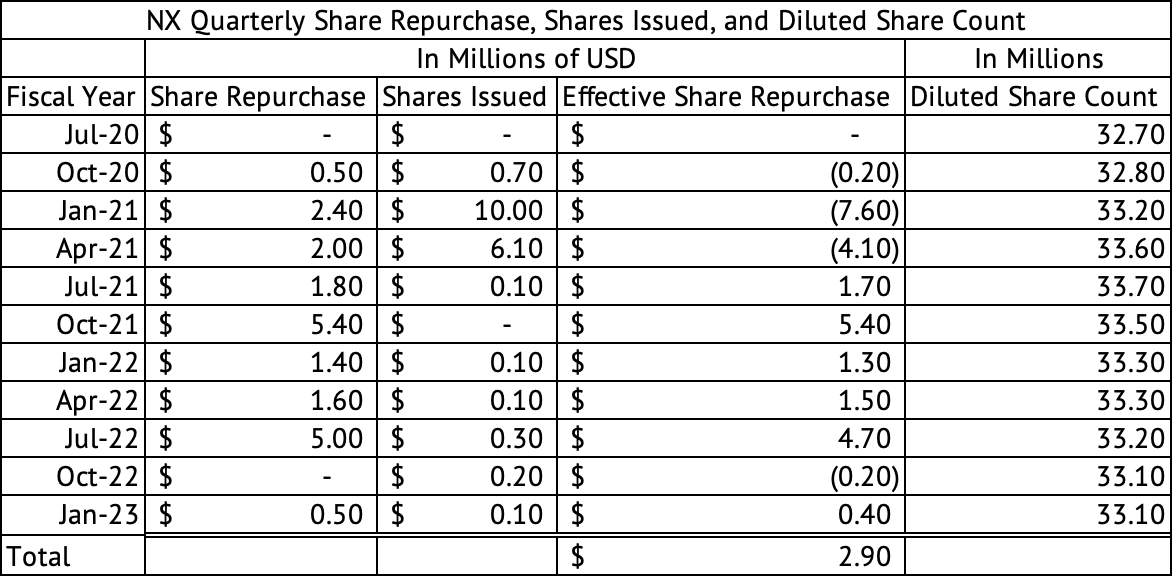

The company has averaged $95 million in operating cash flow since 2018. The company's dividend is safe in a recession but has not grown over the past three years. It has the resources to increase its dividend, but may prioritize share buybacks over a dividend increase. Since July 2020, the company has repurchased $2.9 million of its shares (Exhibit 11) . But, its diluted share count has increased from 32.7 million to 33.1 million, an increase of 0.4 million over the same period.

Exhibit 11:

Quanex Building Products Share Repurchases and Issuances (Seeking Alpha, Author Calculations)

{kind=link}

Quanex has a good balance sheet, but its growth prospects have turned negative due to the high-interest rates and uncertain economic conditions. The company's dividend yield is too low compared to higher yields offered by other stocks and the "risk-free" U.S. Treasuries. The stock's valuation is comparable to its peers and may indicate that the markets expect poor financial growth and performance in 2023. The building products segment overall may require lower interest rates to boost sales. Given the stock's low dividend yield, a slowing economy, and the debt-ceiling fight in the U.S. Congress, it may be best for the market volatility to return before buying.

For further details see:

Quanex Building Products: Trading In-Line With Peers