PWR - Quanta Services: It Is Not A Good Time To Jump In After 6x In 5 Years

2023-12-14 09:14:56 ET

Summary

- Quanta Services has experienced significant growth in the past 5 years, but its financial metrics are subpar, warranting a hold rating.

- The company specializes in contracting services for various sectors, including infrastructure, energy, communications, and environmental services.

- Quanta Services has a substantial amount of long-term debt, but its debt levels are currently manageable, and it has no liquidity issues.

Investment Thesis

Quanta Services (PWR) has been on a tear in the last 5 years, going up almost 600% compared to S&P500´s 75% gain during the period. I wanted to see if it would still be a good time to invest in the company for the long term. Unfortunately, the company's financial metrics that I deem necessary for a good investment were subpar, and I would require a big pullback before I would consider taking on such risks. Therefore, I assign the company a hold rating.

Briefly on the Company

The company specializes in contracting services, including infrastructure, energy, communications, and environmental services. The company serves many different sectors, including utilities, private businesses, and governments.

The company builds and maintains power lines, communication networks, and pipes so that everything we do in our day-to-day lives is running smoothly.

Financials

As of Q3 ´23 , PWR had around $305m in cash and equivalents, against a whopping $3.9B in long-term debt. The debt figure increased in FY21 when the company acquired Blattner, a large and leading utility-scale renewable energy infrastructure solutions provider. That is quite a decent amount of debt, which will deter many investors from investing in the company. Leverage isn't all bad, especially if it is used correctly and acquisitions create value for everyone. So, is the debt at least manageable? The debt-assets ratio has increased, which makes sense because the debt levels have increased in recent years, however, it is still within the level that is considered acceptable, which is below 0.6. Debt-equity has also been decent even after the injection of debt. It has been under 1 all the time and anything under 1.5 I would consider manageable. Lastly, the interest rate coverage has come down substantially since FY18 due to the increase in debt and the annual interest expense on it. Many analysts consider an interest coverage ratio of 2x as healthy, while I think a 5x allows for the bad years of performance, and a higher chance of continuing to pay their interest expense through operating profits it makes, while 2x I feel is a little too close for comfort. Nevertheless, the company´s most recent interest coverage ratio is around 6, which passes even my conservative requirements. Below are these ratios with Q3 ´23 numbers also for reference.

{kind=link}

So, it looks like the debt on books is not an issue right now, as long as the management is going to start working on lowering the debt going forward instead of adding to it.

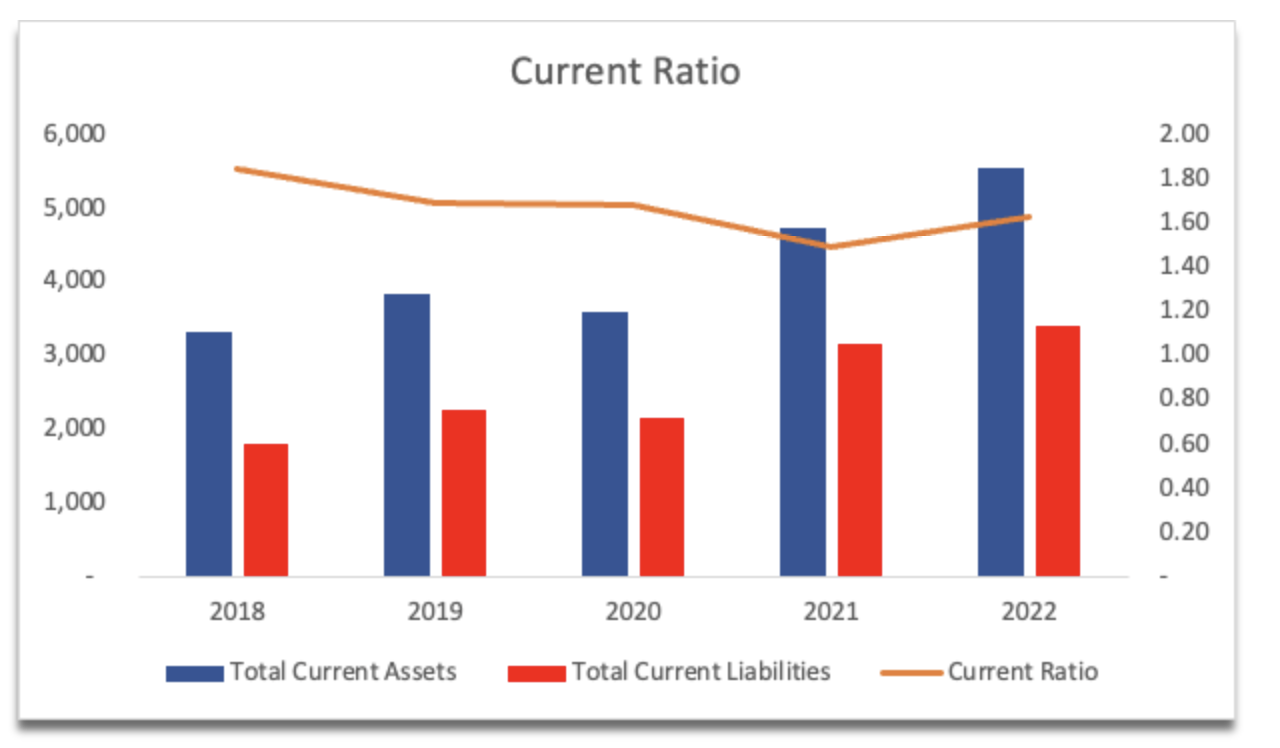

PWR´s current ratio has also been very healthy over the years, and in the most recent quarter, it stood at 1.6, which is right where I like to see it. Anything within 1.5-2.0 I consider to be efficient because the company has enough capital to cover its short-term obligations and still has a good amount left over for further growth of the company, so that is another plus for PWR. So, it is safe to say that the company has no liquidity issues.

{kind=link}

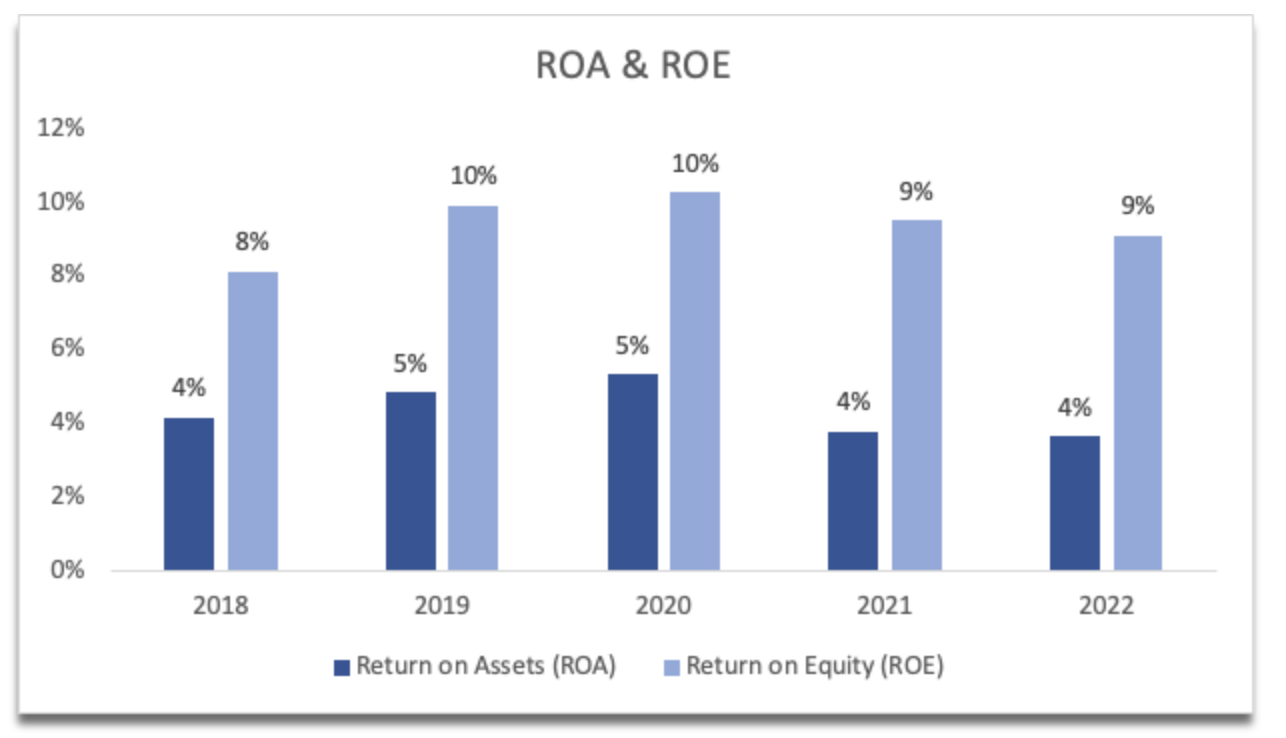

The following metrics are not as exciting but tell me a lot about how the company has been performing. PWR´s ROA and ROE have been trending slightly down since FY20, which can be attributed to the bottom line not increasing significantly over the same period while assets and shareholder equity have increased by much more. It seems that the management has not been very efficient with the company´s assets and shareholder equity in the last couple of years.

{kind=link}

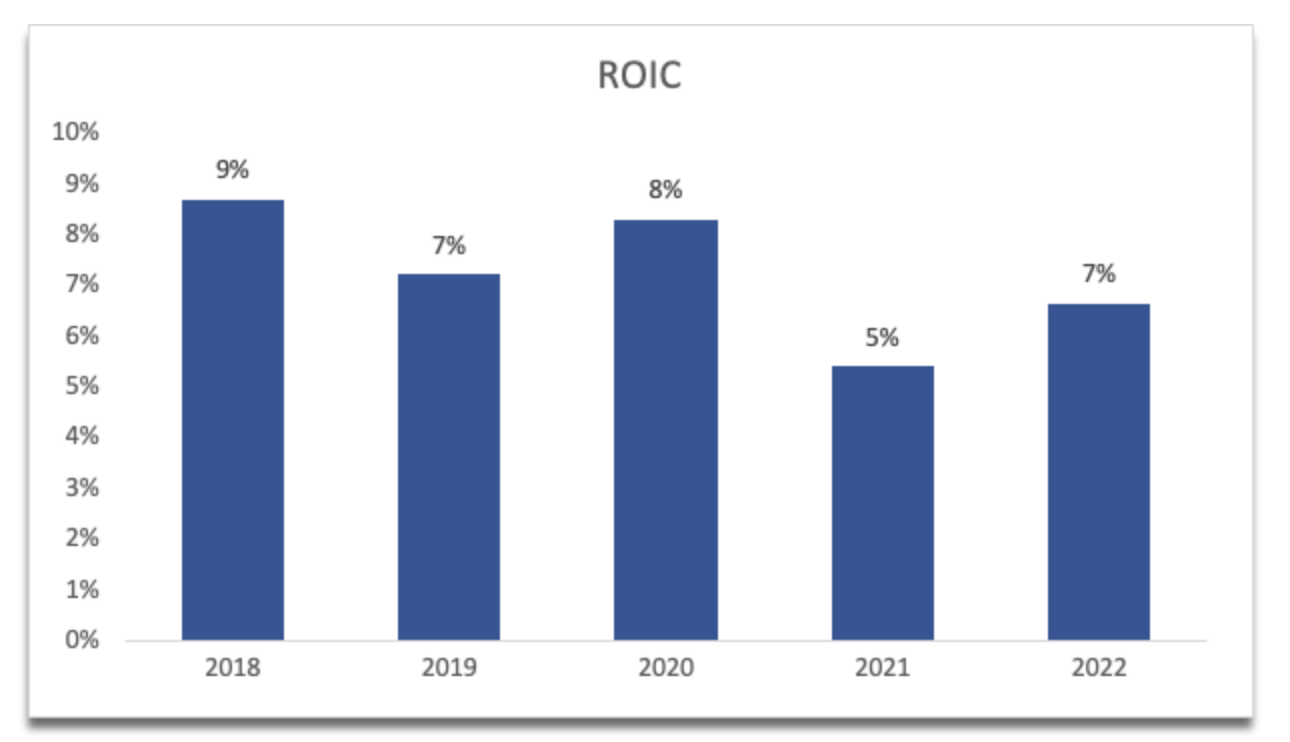

The same story can be said about the company´s ROIC, which I deem to be a very important metric for a long-term investment. Ever since FY20, it has been trending down, which means that the management is not allocating the capital very efficiently. It also coincides with the acquisition of Blattner. The company acquired all its assets, but the bottom line did not improve significantly, which to me sounds like the acquisition so far has not proven to be accretive. It´s only been a couple of years, so I won´t deem it a bad investment right now because the ROIC is coming back since the bottom in FY21. I like to see at least 10% from my investments, therefore, I would have to discount the company´s valuation a little more with a higher margin of safety later on.

{kind=link}

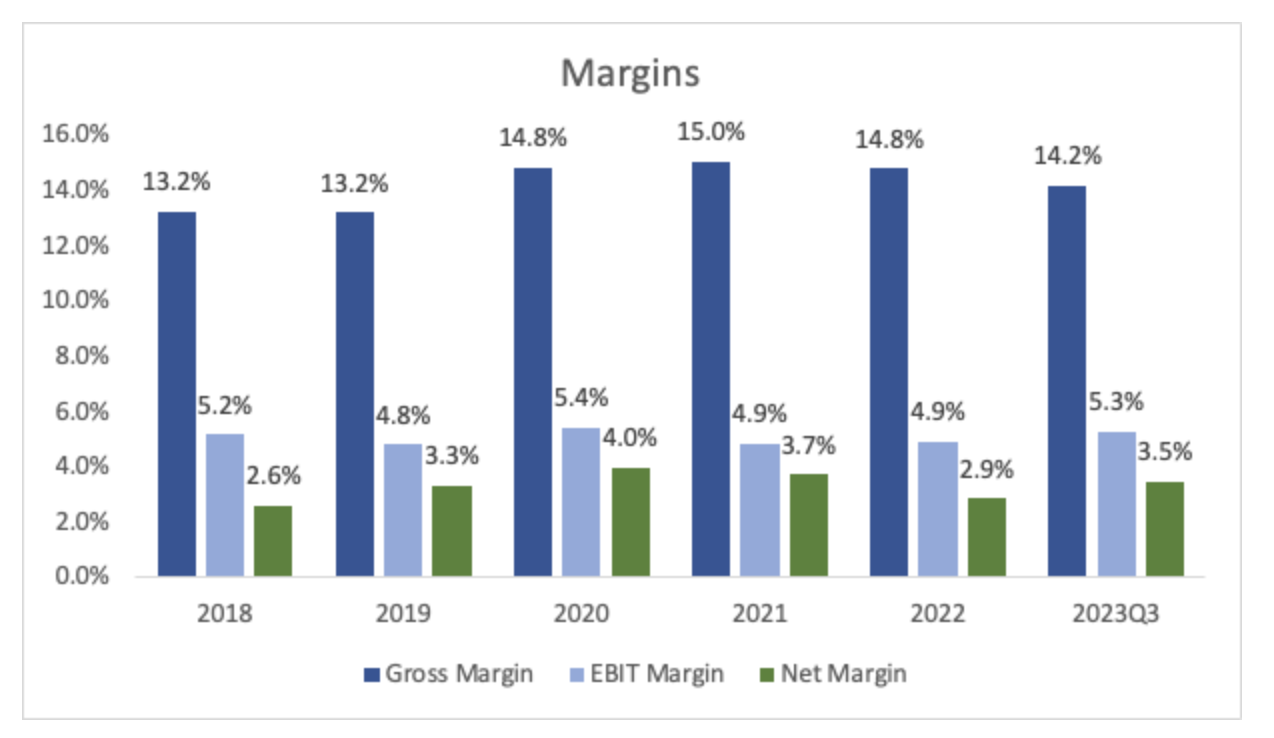

Speaking of efficiency, the company´s GAAP margins have taken a slight hit but have been relatively stable over the last few years, and in the latest quarter, it seems that the company managed to reduce operating expenses while gross margins have come down slightly y/y.

{kind=link}

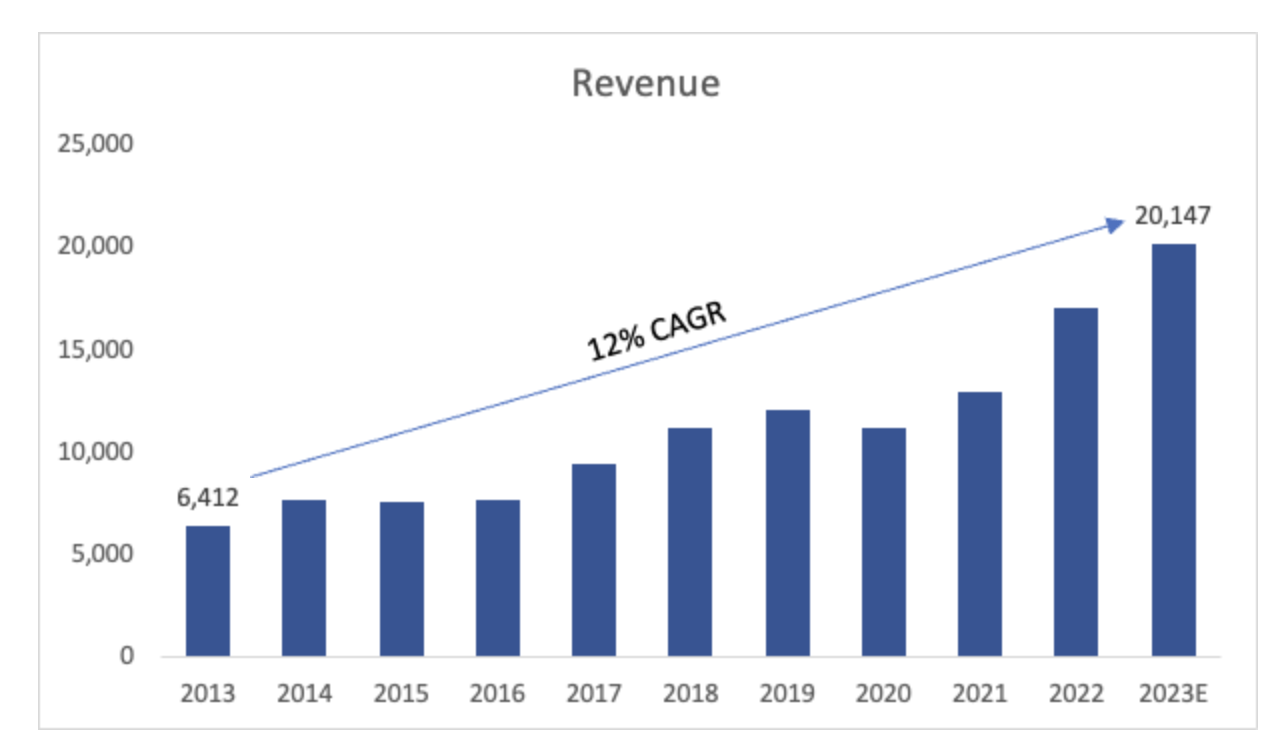

In terms of revenue, PWR managed around 11% CAGR over the last decade, with a 32% y/y from FY21 to FY22, which can be attributed to the acquisition of Blattner as the renewable energy sector saw a massive 107% increase in sales. In terms of FY23 guidance, the company sees around an 18% increase in sales y/y, which is a decent growth. I will be interested to see if this momentum continues in later years, however, I will be approaching my valuation with a conservative outlook rather than an optimistic one. That way I´ll get a larger margin of safety and a better risk/reward outcome.

{kind=link}

Overall, the company could be more attractive as an investment in my opinion. The high top-line growth is going to be attractive for many investors, however, if the company can’t grow its bottom line significantly with all these acquisitions and become more efficient and profitable then no amount of sales growth can make it a good investment to me.

Valuation

For revenue assumptions, I included the management´s outlook for FY23, as that is more than certain to be the growth. For the rest of the years, it is impossible to know until much later in the year, so I decided to go with a slightly conservative outlook. To cover my basis, I also included a conservative and an optimistic scenario. Below are those assumptions and their respective CAGRs.

{kind=link}

In terms of margins and EPS, I decided to be a little more optimistic and go with the company´s adjusted numbers as that is what the management believes is the "true value" of the company. Also, this way, I am giving the company a chance to be worth something close to its value right now, as you´ll see later on in the section. Below are those assumptions compared to the GAAP numbers of FY22.

{kind=link}

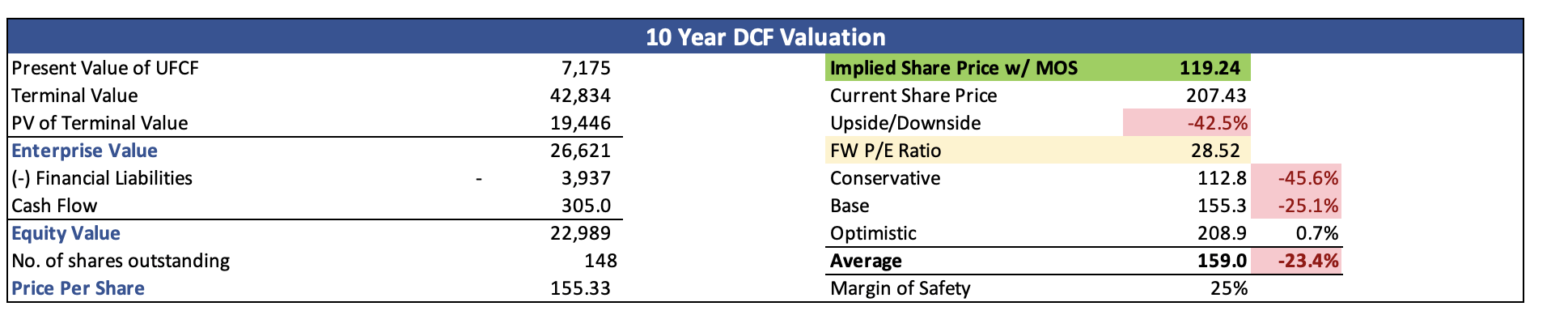

For the DCF analysis, I went with the company´s WACC of 8.2% as my discount rate and a 2.5% terminal growth rate. Also, important to note, that the company´s WACC is higher than its ROIC which means right now, the company is destroying value for its shareholders. On top of these estimates, I decided to add another 25% margin of safety because all the metrics I deem necessary are not adequate for me, so I would need a higher margin of safety to take on such risks.

With that said, Quanta Service´s intrinsic value and what I would be willing to pay for it is around $120 a share, which means the company is highly overvalued for me to commit any capital, as risk/reward is not enticing at this price.

{kind=link}

Closing Comments

Even with adjusted numbers, the company is nowhere near a good investment right now. It seems that investors are putting a high PE ratio on the company because of the recent sales growth acceleration. That doesn't mean that people won't make money going forward. What this means to me is that the company needs to maintain such growth to justify the valuation, and I don't think the top-line growth is enough for that, since the company is still not becoming more efficient over time and the recent acquisition so far is costing its profitability a little bit, but like I said, I won´t judge it too soon, since it may take a while longer to reap fruits of it. It also means that the company for me is more risky than the potential reward of investing my capital at this price. If the share price retreats closer to my PT or even below it, I would be willing to overlook the subpar ROIC and other efficiency metrics as at that point it would be worth the risk. Right now, I will set a price alert around my PT and revisit the company when it reports more earnings and see if anything has changed for the better.

For further details see:

Quanta Services: It Is Not A Good Time To Jump In After 6x In 5 Years