PWR - Quanta Services: Poised To Benefit From Trillions In Infrastructure Spending

2023-12-14 05:08:23 ET

Summary

- Quanta Services is a growth stock with outstanding growth potential in the energy and communications infrastructure industry.

- It has a strong history of revenue growth, beating industry averages in revenue, EBITDA, and EPS growth.

- PWR has a backlog of over $30 billion and expects to see significant growth in the green energy transition and the aging utility workforce.

Thesis

Although modestly overvalued, Quanta Services, Inc. ( PWR ) is a growth stock that has delivered outstanding growth since mid-2020. Its potential reflects the trillions of dollars that will go into energy and communications infrastructure over the next decade.

About Quanta

The company provides what it calls "specialized infrastructure solutions to the utility, renewable energy, communications, pipeline, and energy industries."

Its services include designing, installing, repairing, and maintaining energy and communications infrastructure. It has operations in the United States, Canada, Australia, and other international markets.

At the close of trading on Wednesday, December 13, 2023, it had a market cap of $29.31 billion, based on a share price of $210.28.

The company was formed in 1997 when founder John Colson assembled four companies into one. It has since gone on to acquire more than 200 other firms. On its website , the company reports that it purposefully retains "the unique, decentralized model that has made us Quanta from day one." It began trading publicly the following year.

Competition

The company reports in its 10-K for 2022 that it operates in highly competitive markets. In addition, there are few barriers to entry into some of its industries, and some of its subcontractors may become skilled enough to compete with it.

Seeking Alpha names AECOM ( ACM ), EMCOR Group, Inc. ( EME ), Stantec Inc. ( STN ), WillScot Mobile Mini Holdings Corp. ( WSC ), and APi Group Corporation ( APG ) as publicly traded competitors. All have significantly smaller market caps than Quanta.

It has an enterprise value of $33.26 billion; the next largest is AECOM at $14.24 billion.

Scanning through its November 2023 investor presentation , several other competitive advantages appear or are implied:

- It calls itself the largest and preferred employer of craft-skilled labor in the industry.

- Expertise in recruiting and training tradespeople and others needed in the industry.

- Deep customer relationships, as evidenced by the fact that roughly 90% of its 2022 revenue came from "repeatable and sustainable activity." It added that many of its customers have been with it for decades.

- Having acquired so many other firms in the past 20 years, it has expertise in purchasing other companies.

- Liquidity: At the end of the third quarter, it had $305 million in cash and equivalents, as well as an investment-grade credit rating.

Growth

First, Quanta has a strong history of revenue growth, which has averaged 13.06% per year (YoY), which is 35.54% greater than the industrials sector median. On a forward basis, it is expected to deliver a growth average of 9.96% per year over the next five years, which is 95.53% more than the sector.

Turning to EBITDA, the company has outpaced the industry by 1.49% over the past half-decade. On a forward basis, EBITDA is expected to beat the industry median by 39.51% over the same period.

Third, EPS diluted growth, year-over-year, has averaged 14.52%, making it a whopping 223.80% higher than the industrials median over the past five years. Diluted EPS growth, forward basis, is estimated at 18.98%, 2.5% above the sector forecast.

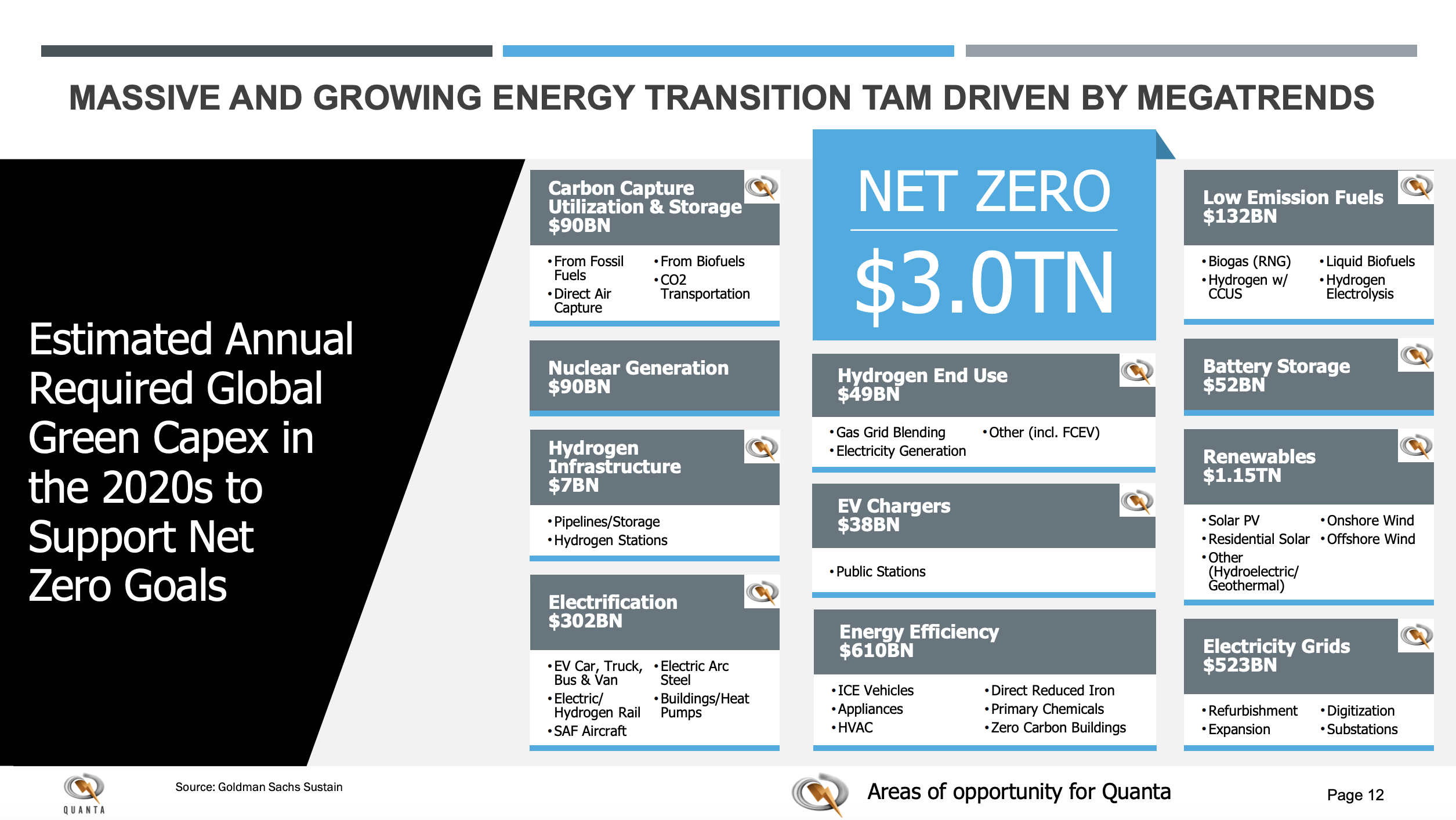

In its investor presentation, the company pointed to a massive growth opportunity in just the green energy transition:

{kind=link}

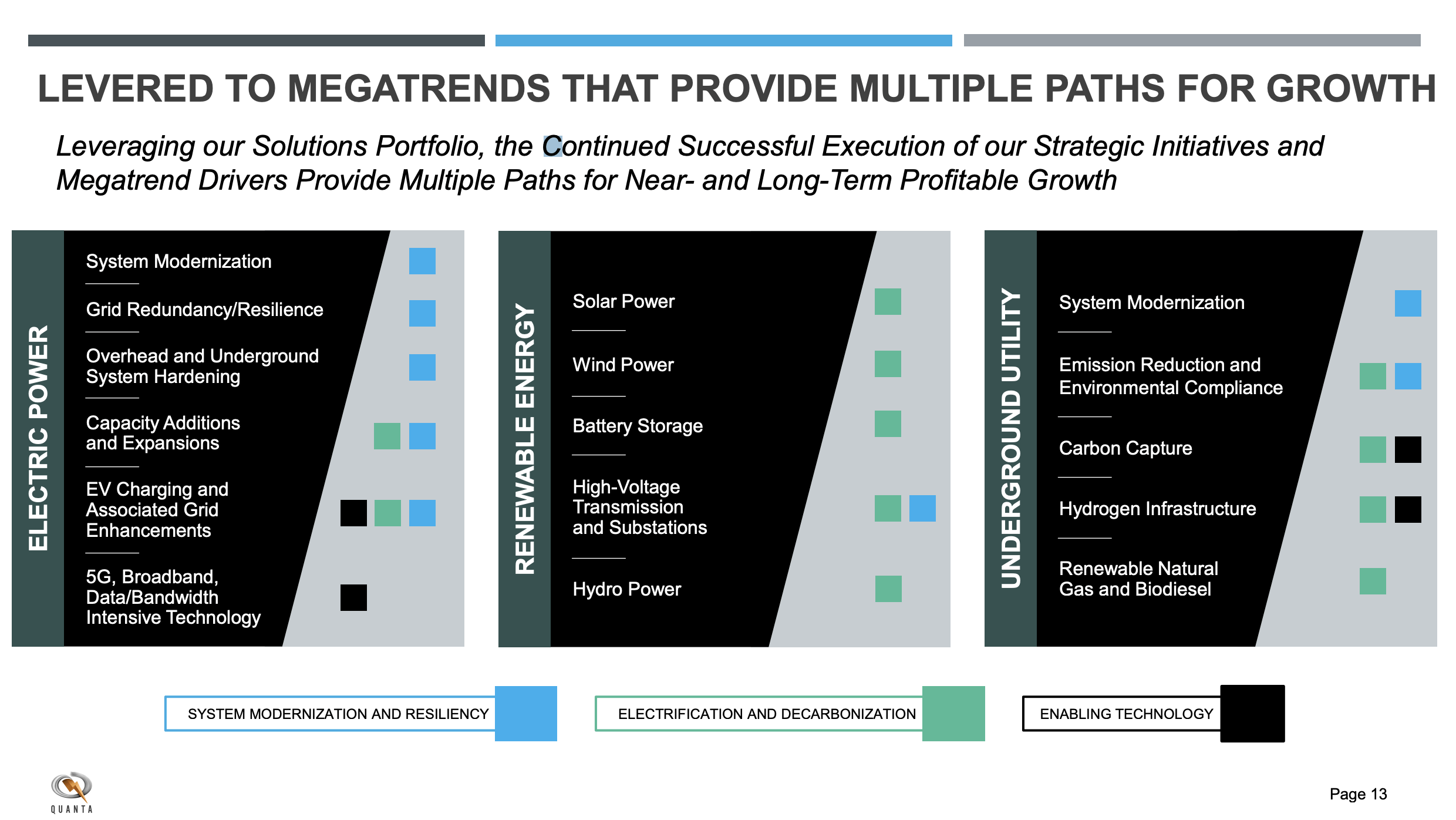

More broadly, it sees several trends that should help growth in both the short and long terms:

{kind=link}

It also sees a major growth opportunity in the aging utility workforce, because electric and gas utilities will outsource more of their skilled labor needs to companies like Quanta.

In its Q3-2023 earnings presentation , it reported having a total backlog of more than $30 billion for the first time.

In conjunction with the third quarter results, it offered guidance for the full year ending on December 31:

- Revenue between $20.1 billion and $20.4 billion, up from 2022 revenue of $17.1 billion.

- Net income attributable to common stock: between $729 million and $759 million, up from $696.4 million last year.

- Diluted earnings per share attributable to common stock: $4.90 to $5.10, compared with $4.69 per share in 2022.

- EBITDA: between $1.74 billion and $1.79 billion, up from $1.628 billion last year.

Margins

To capitalize on these opportunities, Quanta will require margins that provide free cash flow for internal and acquired growth, as well as pay its dividend. On a TTM basis, it has a gross margin of 12.99%, an operating margin of 5.47%, and a profit margin of 3.57%.

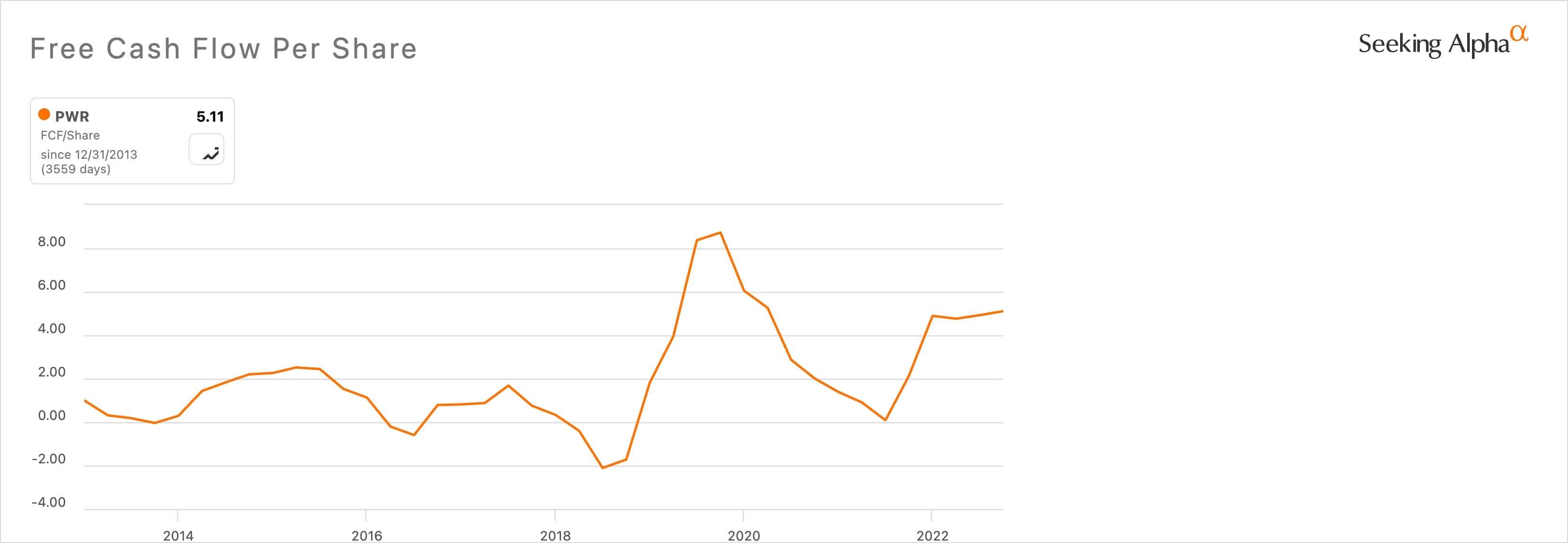

Nothing too impressive there, but still, free cash flow [TTM] is $5.11 per share, more than double its average between 2010 and 2020. However, the growth in FCF hasn't been smooth:

{kind=link}

In the November 2023 presentation, Quanta listed several margin improvement initiatives. They include exiting some international operations to focus on North America and Australia, identifying areas for margin improvement in its Underground Utility & Infrastructure segment, and what it calls "Strategic initiatives to improve margins and returns across the portfolio."

Management and strategy

Chief Executive Officer Duke Austin joined the company in 2009 and held several senior positions before stepping into the corner office in 2016. He has led Quanta during its rapid growth over the past seven years.

Jayshree Desai has been the Chief Financial Officer since 2020. Prior to that, she held senior financial and executive roles at several energy companies.

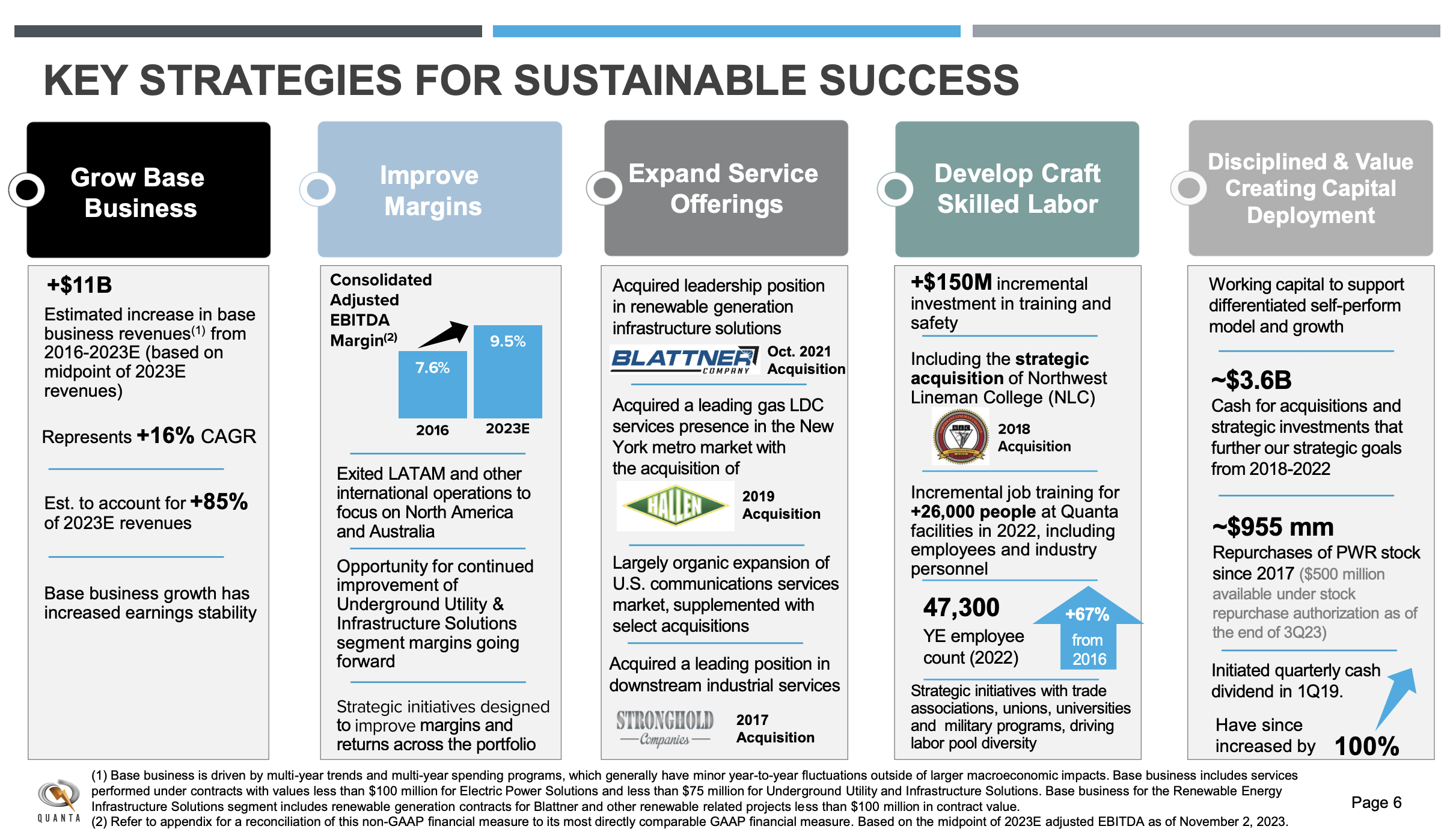

Turning to strategy, the company articulated that in the November 2023 presentation:

{kind=link}

Overall, it aims to deliver 5% to 8% organic revenue CAGR and double-digit returns on invested capital.

Valuation

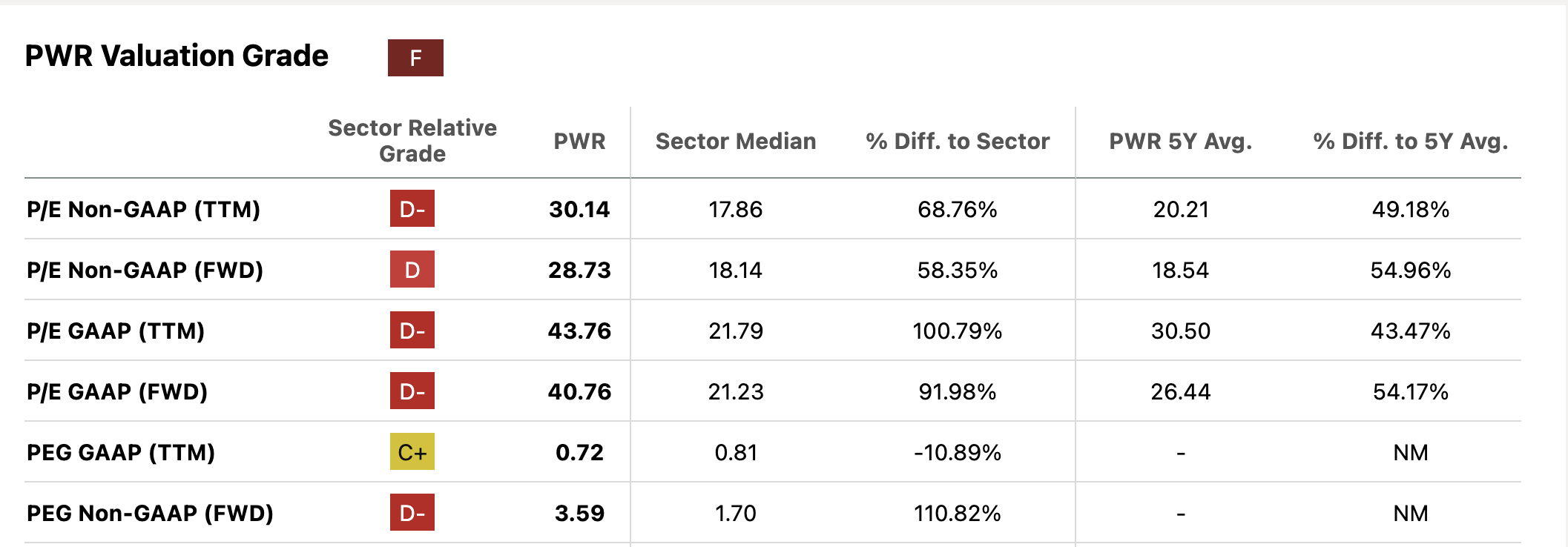

Quanta gets an extreme valuation from the Seeking Alpha system, and it isn't the good extreme:

{kind=link}

Looking at the P/E in more detail, the share price grew from a low of $36.16 on July 9, 2020, to $210.28 on December 13, 2023. That's an average annual growth rate of 60.5%.

Over roughly the same period, earnings per share grew from $0.52 per share in Q2-2020 to $1.83 per share in Q3-2023. That's an average increase of 46.4% per year over the past three and a half years.

That difference of 14.1% per year over the course of roughly three and a half years tells us the stock is overvalued, although perhaps not so excessively as the Seeking Alpha grade suggests.

What if we bring in the growth of EBITDA, through the forward PEG ratio? PEG non-GAAP ratio of 3.57 implies an annual growth rate of 8.1%. Given the EPS growth rate of 46.4%, that seems quite modest. Increasing the growth rate to 15%, which seems more appropriate, produces a PEG ratio of 1.92. That's 32.14% above the sector median of 1.70, but less dramatically higher.

The same story comes from the price-to-sales ratio of 1.47, which is 8.22% above the sector median of 1.36.

As this 10-year price chart shows, the capital gains have been strong and relatively steady since 2020.

Technically, the 200-day moving average crossed above the 50-day moving average on November 17, and the price has continued steadily upward since then. Still, as it nears the previous high, there's a possibility the price will dip again. That would provide better value and perhaps a margin of safety.

Given the ratios and charting, I consider Quanta to be 15% to 20% overvalued, which would make fair value a price between $168.22 and $178.74.

However, there are few stocks that offer the kind of growth seen in Quanta, so there is a lot of competition among investors. For long-term investors, say three years or more, the current price isn't an unreasonable amount to pay for the expected growth. Still, patience should be the keyword, as another dip may occur in the not-too-distant future.

Other perspectives: Wall Street analysts give the firm a Buy rating, with an average score of 4.37 and Quant analysts have a hold rating and a score of 3.17. Seeking Alpha analysts have it a sell rating score of 2.00; however, of the four SA ratings this year, three were Buys, and one was a Sell.

Dividends

Quanta pays a dividend, which gets Seeking Alpha grades of A+ for safety, B- for growth, F for yield, and D+ for dividend consistency. That F reflects a yield of just 0.18%, or $0.36 per year, with a low payout ratio of 4.70%.

Risks

According to its 10-K, its risks include operational hazards, physical risks associated with climate change, an inability to recruit for its labor-intensive business, failure to make good on acquisitions, and the availability/price of fuel, materials, or equipment.

On the regulatory and compliance side, Quanta may be affected by new requirements, work stoppages by its unionized workforce, and failure to comply with environmental laws and regulations.

Financial risks include access to funding, debt problems, cash flow to service that debt, and an inability to get surety bonds or bank guarantees.

Conclusion

Quanta Services is a strong player in an industry that will see trillions of dollars invested to build and upgrade essential infrastructure. It appears to have the growth opportunities, profitability, management and strategies it needs to keep growing more quickly than the market as a whole.

I consider it to be overvalued by 15% to 20%, but understand that investors may have to, or be willing to, pay a premium to get this kind of growth.

Despite the overvaluation, I see it as a promising growth stock going forward and rate it a Buy.

For further details see:

Quanta Services: Poised To Benefit From Trillions In Infrastructure Spending