PWR - Quanta: Valuation Is Off The Grid

2023-10-02 09:43:27 ET

Summary

- Quanta Services has a strategy of constant acquisitions leading to good long-term growth.

- The company has a diverse portfolio of energy infrastructure solutions and a well-diversified client base as a result of constant acquisitions.

- The stock price has rallied significantly in the past years - after the rally, my DCF model estimates the stock to be overvalued, constituting my sell rating.

Quanta Services ( PWR ) provides energy infrastructure solutions. The company has had a strategy revolving around constant acquisitions, boosting the company's long-term growth to a very good level. After a massive stock price run, though, I believe the stock is currently overvalued; I have a sell rating at the current price.

The Company

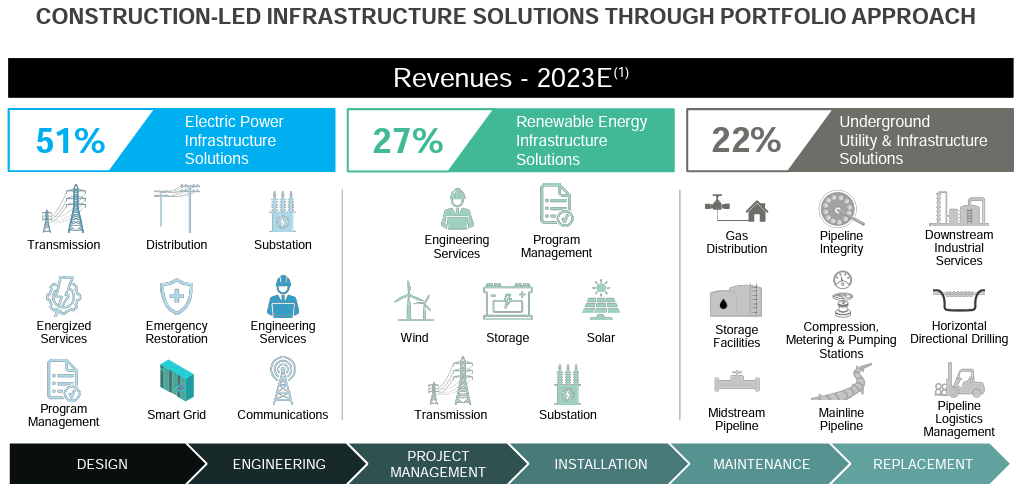

Quanta focuses on energy infrastructure solutions. As the company has acquired multiple businesses over the company's history, Quanta's offering has widened into a very diverse portfolio of services and products. Currently, the company's split between different segments is the following:

Quanta's Segments & Offering (Quanta August 10th Investor Presentation)

{kind=link}

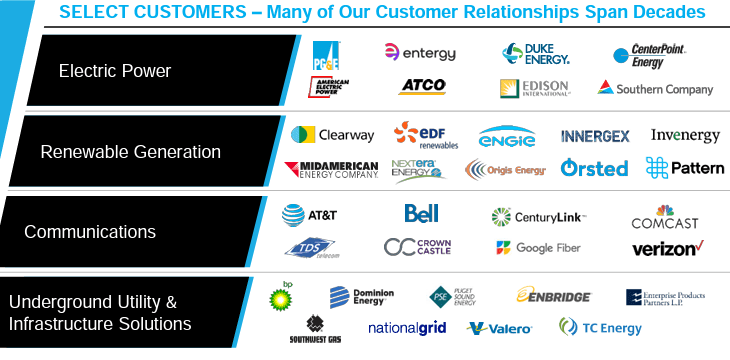

The company has significantly large customers, ranging from PG&E (PCG) to AT&T (T):

Quanta's Client Base (Quanta August 10th Investor Presentation)

{kind=link}

The top 10 customers only account for 36% of Quanta's revenues, signifying a well-diversified client base.

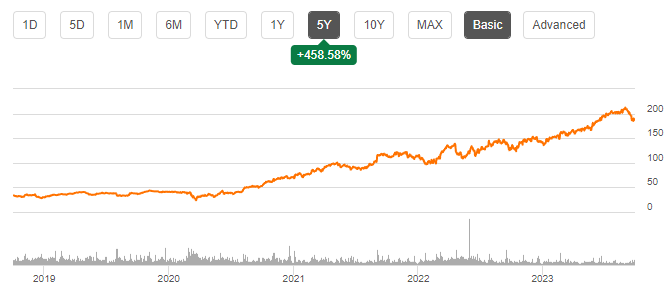

The stock price has seen a massive run as in its last five years the price has appreciated by over five-fold:

{kind=link}

The company does pay out a dividend in addition, but the amount is very small - currently, Quanta's dividend yield stands at 0.17%.

Financials

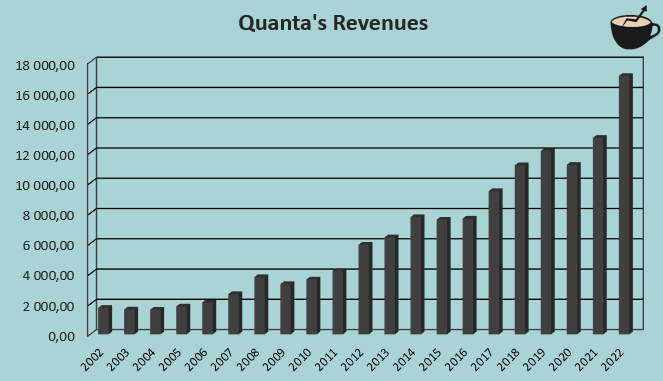

As a result of the company's constant acquisitions, Quanta has achieved a compounded annual growth rate of 12.1% from 2002 to 2022 after starting the strategy revolving around acquisitions in 2010:

{kind=link}

The growth has still been quite valuable - although the growth is due to extensive acquisitions, the company has managed to decrease the company's outstanding share count from 2010; cash flows have been sufficient to finance the acquisitions.

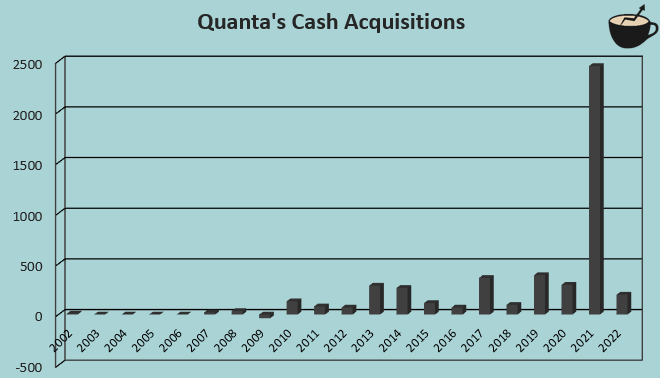

As mentioned, Quanta's cash acquisitions have been quite constant beginning in 2010 - the company has had acquisitions well above $100 million in most years, with a large acquisition of Blattner made in 2021 representing a larger sum:

{kind=link}

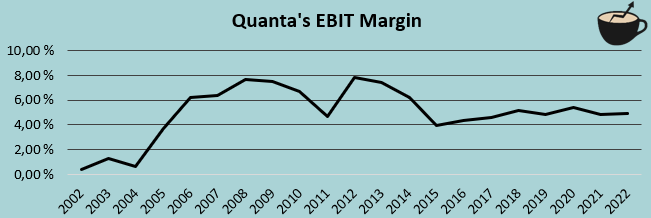

Quanta's EBIT margin has had an average of 5.0% in the company's history from 2002 to 2022:

{kind=link}

With trailing numbers , the margin stands precisely at the average of 5.0%. The company has initiatives to improve the margin in the coming years to a rate that's above Quanta's long-term average, though. For example, the management sees room for margin expansion in the renewables segment as discussed in the company's Q2 earnings call , representing 27% of Quanta's business.

Quanta has some long-term debt on the company's balance sheet . Currently, the company has around $4.2 billion of long-term debt, of which $40 million is in the current portion and the overwhelming majority in the long-term portion. I believe the amount of debt should be safe for Quanta and a good way of getting relatively cheap financing - compared to the company's market capitalization of around $27.2 billion, the amount of debt is at a quite modest level. On the other side of the balance sheet, Quanta has a cash balance of $362 million and a significant receivables balance of $5.4 billion.

Valuation

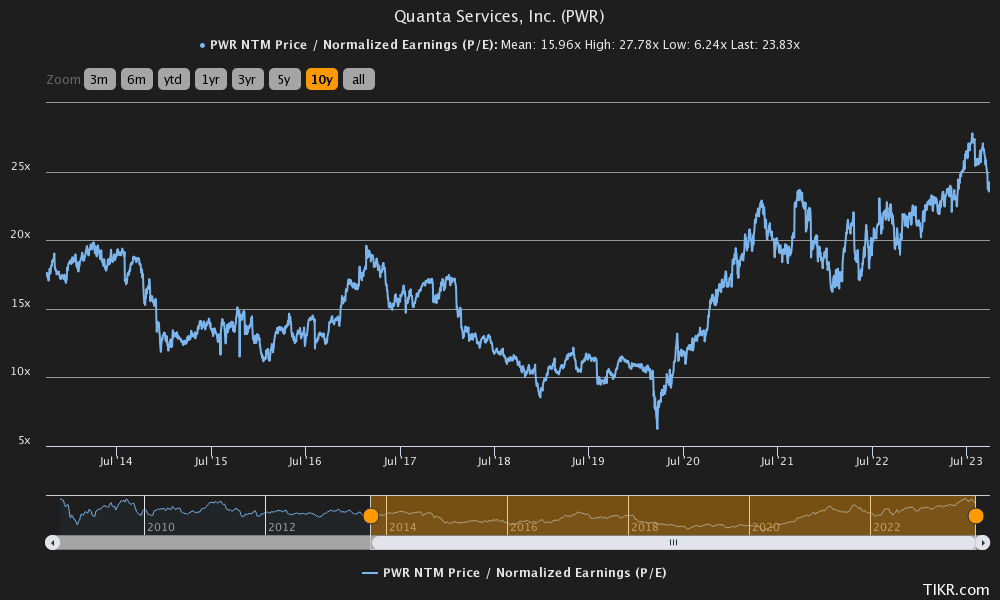

After the massive stock run in the past years, Quanta trades at a forward price-to-earnings ratio of 23.8, around 49% above the stock's ten-year average of 16.0:

{kind=link}

The higher ratio compared to Quanta's history seems quite extraordinary - interest rates have risen significantly, in theory raising investors' required rate of return. To further analyze the valuation, I constructed a discounted cash flow model in my usual manner.

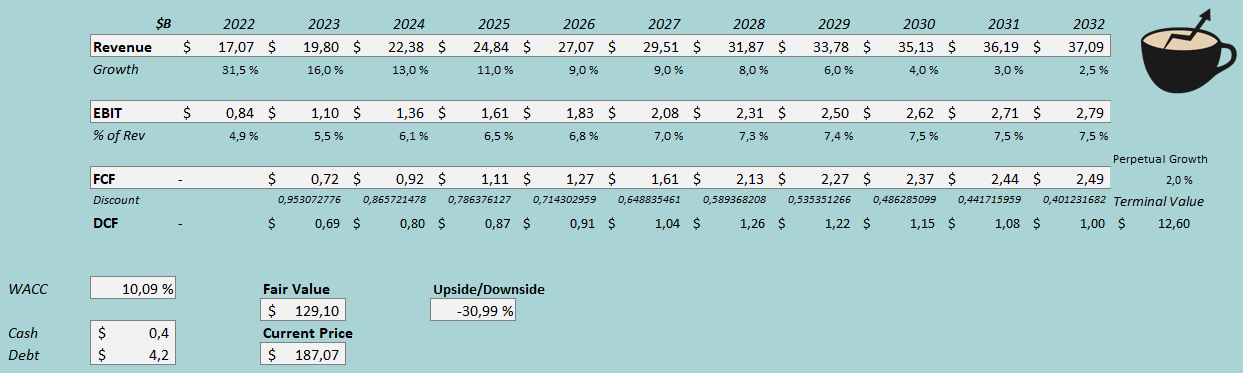

In the DCF model, I estimate a growth of 16% for 2023 - the growth represents the middle point of Quanta's management's current guidance. After the year, I have a growth of 13% for 2024. The rate slows down slightly in the years after 2025 and takes larger steps down after 2028 into a perpetual growth rate of 2%. The CAGR estimate of 10.0% from 2023 to 2028 takes into account a continuing flow of acquisitions for Quanta. After the years, I estimate acquisitions to slow down significantly, but in turn, improve free cash flow significantly - contrary to my usual modeling, I consider further acquisitions in the DCF model.

Quanta's management seems to have plans for margin expansion - in the DCF model, I estimate an EBIT margin of 5.5% for 2023, 0.6 percentage points above 2022. Going further, I estimate further margin leverage as a result of acquisition synergies, a larger scale of operations, and the improving margin of the renewables segment - I estimate the EBIT margin to scale in steps into a figure of 7.5%, achieved in 2030. For the cash flows, I estimate the conversion from earnings to free cash flow to be quite poor in the coming years as I price in acquisitions into the cash flows. The cash flows improve significantly in 2028, though, as I estimate the acquisitions to slow down in the year.

The mentioned estimates along with a cost of capital craft the following DCF model scenario with a fair value estimate of $129.10, around 31% below the current price:

{kind=link}

The average weighted cost of capital used is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In Q2, Quanta had $48 million in interest expenses. Annualized, the company's interest rate comes up to 4.56%. I estimate the company's long-term debt-to-equity ratio to stay quite near the current level, at an estimated 15%.

For the risk-free rate on the cost of equity side, I use the United States' 10-year bond yield of 4.58% . The equity risk premium of 5.91% is Professor Aswath Damodaran's latest estimate for the US made in July. Yahoo Finance estimates Quanta's beta to be 1.08 . Finally, I add a small liquidity premium of 0.3% crafting a cost of equity figure of 11.26% and a WACC of 10.09%.

Takeaway

Utility companies can be quite complicated to do a valuation on - the DCF model relies on assumptions about future acquisitions in addition to organic performance. The beta figure could also be significantly lower as the figure often is for utilities companies, lowering the cost of equity significantly in the future. I believe the DCF model represents moderate estimates for Quanta's performance, but the company could very well surprise the estimates to the positive or negative side; I am open to rating changes as the company continues on its path. For the time being, I have a sell rating.

For further details see:

Quanta: Valuation Is Off The Grid