FSNUY - Quest Diagnostics: Market Overreaction Creates Investment Opportunity

2023-12-08 07:22:17 ET

Summary

- Quest Diagnostics is a global leader in diagnostic testing, information, and services, providing diverse products to a broad clientele.

- The company capitalized on COVID-19 testing to boost earnings. However, post-pandemic, the decline in revenues deterred investors, resulting in poor stock performance.

- My analysis shows that the prevailing negativity around the stock is overstated and the stock might be poised for a reversal.

- At its current price, the stock presents a favorable short to medium-term investment opportunity with a potential 19% increase.

Quest Diagnostics (DGX) recent volatility stemming from the decline in Covid-19 testing revenue appears to have stabilized. The company's strong financial position, consistent and defensive earnings outlook, coupled with an attractive dividend policy, position it as a compelling investment opportunity for investors seeking large-cap value and defensive stocks.

Company's Overview

Quest Diagnostics is a global provider of diagnostic testing, information, and services. Specializing in a variety of diagnostic information services, the company serves a diverse clientele, including patients, clinicians, hospitals, health plans, employers, and accountable care organizations. Quest Diagnostics provides comprehensive healthcare solutions through its network of laboratories, patient service centers, and professionals, while also offering information technology solutions and risk assessment services for the life insurance industry.

Business highlights

To drive business growth, the company implemented strategic initiatives. Specifically, I highlight the following:

Growth Focus

DGX is growth-focused, achieved through acquisitions of existing business and through launching new products. By leveraging strategic acquisitions, the company achieved a 2% revenue increase in 2022 . In addition, In 2023, the company launched several new products including a blood-based test for predicting Alzheimer's disease progression, a new prostate cancer test, and a home fertility test for women. This strategy of acquisitions and products launches will provide the company with new pipelines for growth.

Genomic Medicine

Aligning itself with the evolving trend in healthcare, the company embarked on a Genomic Medicine initiative in 2020 through the acquisition of Blueprint Genetics. This commitment persisted in 2022 with the strategic hiring of two vice presidents specializing in biomedical engineering, molecular genomics, and oncology. Genomic Medicine is poised to revolutionize healthcare operations, and the market is projected to expand tenfold between 2022 and 2028 . This strategic move will bolster the company's competitive standing and unlock fresh avenues for growth.

Diversification

Furthermore, the company's diverse product portfolio, clientele, and global presence not only mitigate operational risk but also contribute to its overall business strength.

Financials

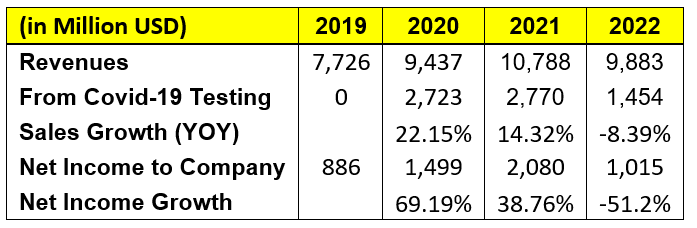

In 2022, the company's net profit decreased by almost 50%, primarily attributed to declining demand for Covid-19 testing. After reaching a peak of $2.72B in 2021, Covid-19 testing revenues plummeted to $1.45B in 2022, with an anticipated further drop to $220M by the end of 2023 (as per the company's third-quarter 2023 news release).

{kind=link}

Company Data, Author

Post-pandemic, the remarkable revenue growth observed in 2020 and 2021 is unlikely to recur. Future revenue is anticipated to stem from new product offerings and organic growth rates unaffected by the pandemic. Excluding Covid-19 testing income, the company achieved a 2.63% compound annual growth rate from 2017 to 2022.

{kind=link}

Company Data, Author

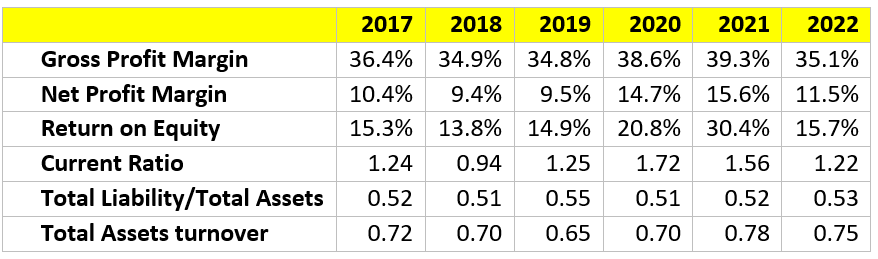

A brief overview of the company's historical performance reveals that key profitability indicators—gross profit margin, net profit margin, and return on equity—exhibited exceptional values in 2020 and 2021. However, in 2022, these metrics reverted to their pre-pandemic average levels. The company's liquidity and solvency positions, measured by current ratio and total liability/total assets respectively, have remained healthy over recent years. Additionally, the company's efficiency in managing its assets, gauged by total assets turnover, has also maintained stability.

{kind=link}

Seeking Alpha, Author

The table above demonstrates the company's sustained and robust financial position.

Stock Performance

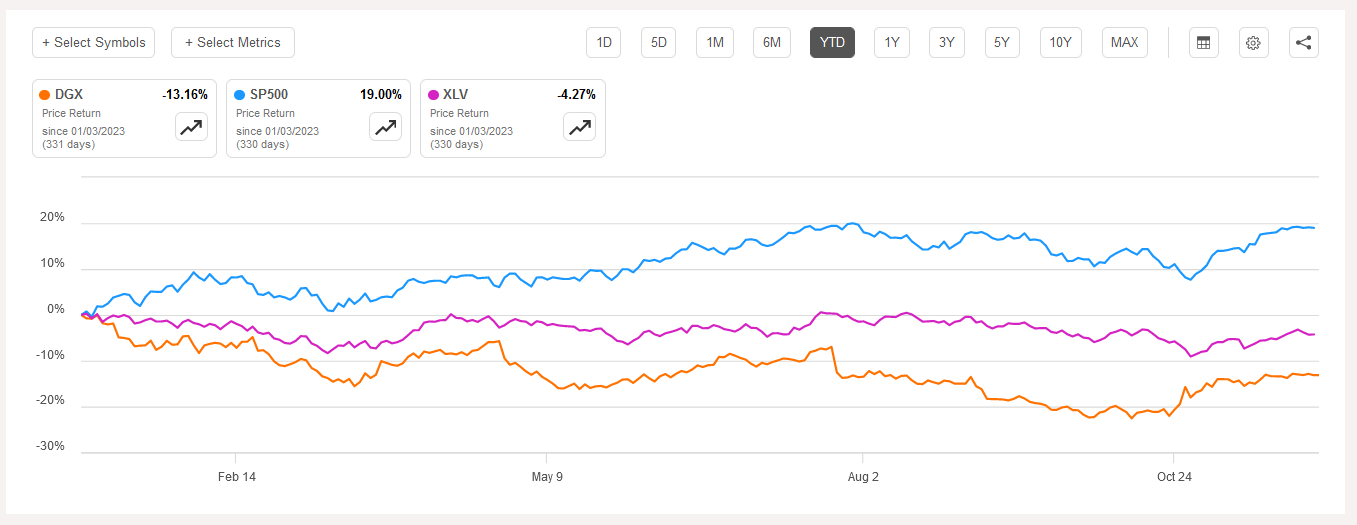

The recent stock performance has been dismal compared to the overall market, reflecting a lack of investor enthusiasm. Year-to-date, the stock declined by 12%, contrasting with the S&P 500's 19% increase and the Health Care Select Sector ETF ( XLV ) which only dropped by 4%

{kind=link}

Seeking Alpha

In my view, the decline in stock performance is primarily attributed to decreased revenue and earnings. However, beyond company-specific factors, broader issues within the healthcare sector are prompting investors to limit their exposure. This includes proposed government regulations aiming to cut budgets for existing healthcare programs or renegotiate costs with providers, posing a significant concern with potential lasting effects on pricing power and sector dynamics. Nevertheless, I believe that large providers, such as Quest Diagnostics, can navigate these challenges by optimizing operations to cut costs and innovating new products and services to enhance profit margins.

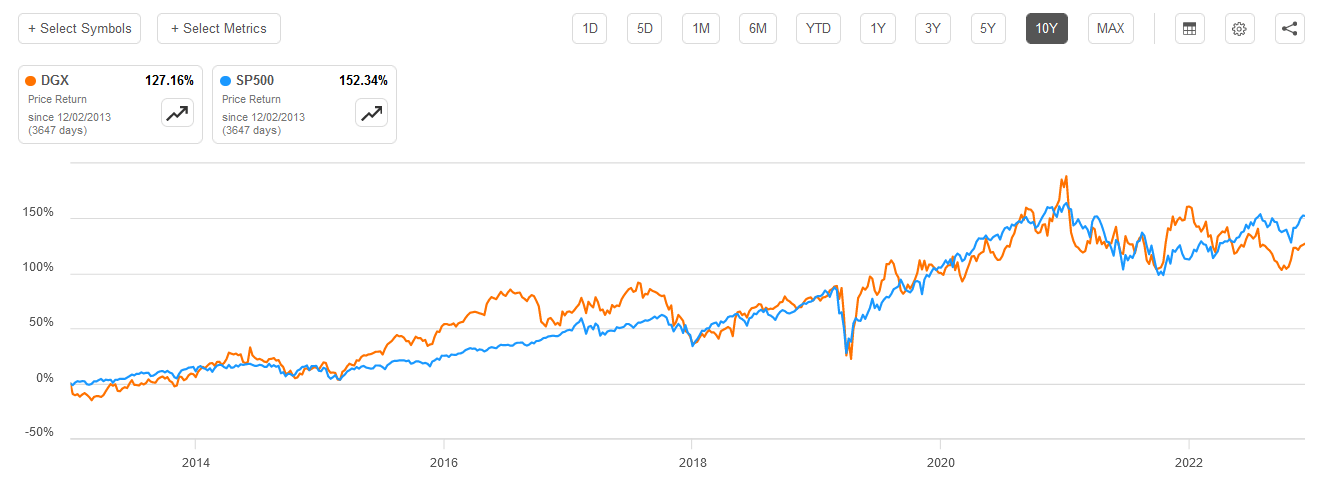

While the recent performance of DGX stock compared to the S&P 500 has been less than optimal, examining the past 10 years reveals a historical pattern of the stock closely tracking the index. Periods of out-performance alternate with periods of under-performance. Applying this historical analogy to the current trend suggests the stock is poised for a reversal.

{kind=link}

Seeking Alpha

Comparative Analysis

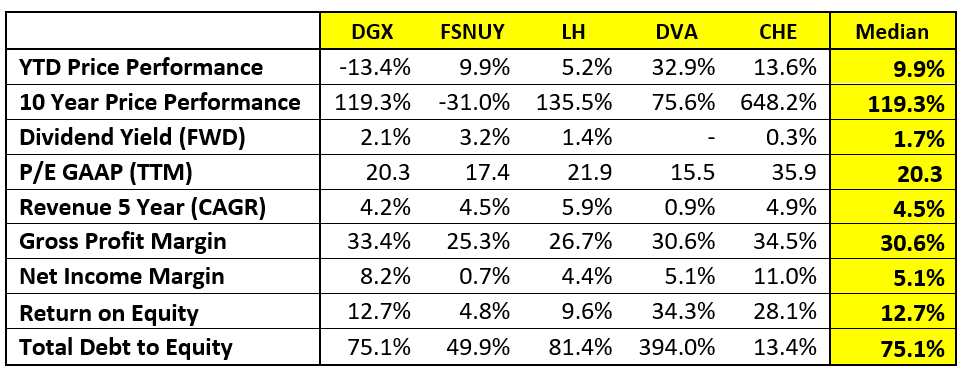

For comparative analysis, I examined four companies in the healthcare services industry:

- Fresenius SE & Co. ( OTCPK:FSNUY ): Offers products and services for dialysis, hospitals, and outpatient medical care. Market Cap $17.40B.

- Laboratory Corporation of America Holdings ( LH ): Operates as a life sciences company, providing essential information for medical decisions. Market Cap $18.06B.

- DaVita Inc ( DVA ): Provides kidney dialysis services for patients with chronic kidney failure in the United States. Market Cap $9.08B.

- Chemed Corporation ( CHE ): Offers hospice and palliative care services primarily in the United States. Market Cap $8.67B."

Reviewing the table below, DGX stock exhibits the weakest year-to-date price performance. However, its 10-year performance aligns with peers. The company maintains a high dividend policy, while its P/E ((TTM)) falls within the peer range. The 5-year revenue growth is slightly below the median, yet both gross profit margin and net income margin outperform the median, with return on equity at the median. Total debt to equity remains within the peer range.

{kind=link}

Seeking Alpha

The table above indicates that Quest Diagnostics' reported financial figures align with those reported by its competitors.

Stock Valuation

The graph below depicts DGX's historical P/E ratio. Excluding the abnormal revenue period from 2021 to 2022 due to Covid-19 testing, the P/E ratio generally ranged between 15 and 20. The current forward P/E ratio stands at an estimated 15.5x , notably lower than historical values, indicating the potential for a stock price increase based on current earnings estimates

{kind=link}

Seeking Alpha

Discounted Cash Flow Model

To determine the firm's fair value, I discounted the future free cash flow to the firm (FCFF) using the weighted average cost of capital ((WACC)).

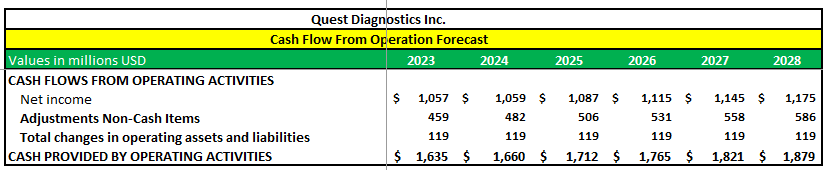

In my revenue forecast, I excluded income from COVID-19 Testing as it is not expected to be material in the future. The base case scenario for revenue growth is 2.6%, reflecting a conservative rate equivalent to the compounded annual growth rate of revenues (excluding COVID-19 testing) between 2017 and 2022. Operating expenses are expected to grow in line with sales, and non-operating expenses will follow the same growth rate observed over the last 9 years. The average tax rate is assumed to be 25%.

Seeking Alpha, Author

For Cash Flow from Operating Activities ((CFO)), items directly linked to sales will grow at the same rate as sales, while other elements are assumed to remain constant.

{kind=link}

Seeking Alpha, Author

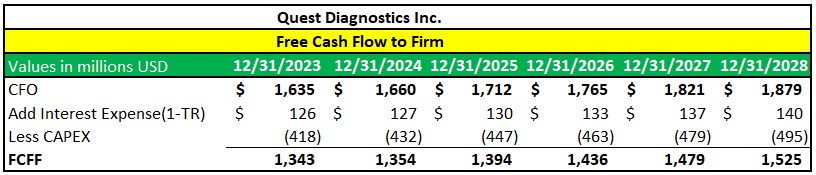

FCFF is given by:

FCFF = CFO + Interest(1-Tax Rate) – CAPEX

{kind=link}

Seeking Alpha, Author

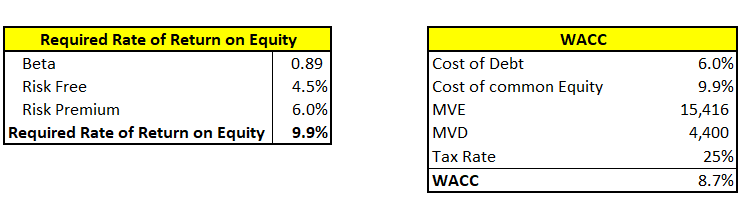

I used Capital Asset Pricing Model to calculate the required rate of return on equity.

{kind=link}

Seeking Alpha, Author

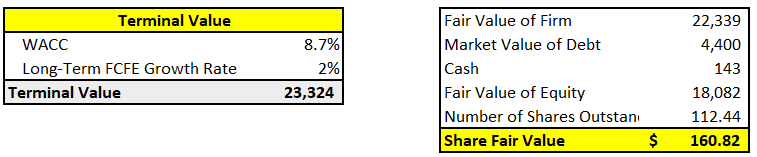

Assuming a long-term FCFF growth rate of 2%, the fair value of the stock is $160.77. This fair value represents a 19% potential growth from the $135 current market price.

{kind=link}

Seeking Alpha, Author

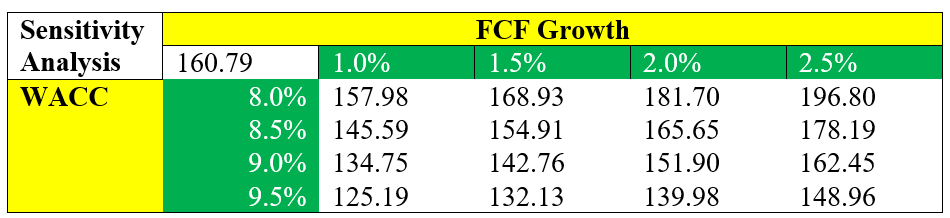

Running a sensitivity analysis by changing the FCFF growth rate and the WACC values, we find that the stock price ranges between $125.19 and $196.80.

{kind=link}

Author

Risk Factors

Companies in the healthcare industry typically face unique challenges due to the extensive regulations that they are subject to. Macroeconomic factors such as a slowing economy, high inflation, and high interest rates could adversely impact the company’s bottom line. Additionally, the following risk factors specific to Quest Diagnostics may affect the company’s ability to drive future revenue growth:

1. In their 2022 annual report, the company highlighted that the consolidation of health insurance plans has resulted in fewer, larger plans with significant bargaining power, negatively impacting the company's pricing power and consequently their profit margin.

2. Government budget reductions in healthcare are a potential risk. The U.S. government, in efforts to address its fiscal budget deficit concerns, may consider cutting healthcare spending, impacting the entire sector, including Quest Diagnostics.

3. Anticipated positive health effects from new weight-loss drugs like Ozempic and Wegovy from Novo Nordisk ( NVO ) and Mounjaro from Eli Lilly ( LLY ) could potentially reduce the demand for healthcare services."

Bottom Line

Quest Diagnostics leveraged the pandemic with COVID-19 testing, but post-pandemic, the loss of this revenue led to a decline in stock value, deterring investors. However, a deeper analysis reveals a financially sound company with future growth prospects. The stock appears undervalued, with a fair value of $160.53, suggesting a 19% potential increase. Therefore, I recommend a buy rating.

For further details see:

Quest Diagnostics: Market Overreaction Creates Investment Opportunity