DGX - Quest Diagnostics: Q2 Earnings Reveal Promising Growth Trends Despite Dwindling COVID Testing Revenues

2023-08-15 02:37:34 ET

Summary

- Quest Diagnostics has a strong Q2 with a slight beat on EPS and revenue. Quest’s base business appears to be recovering from the pandemic and pulled in $2.30B in revenue.

- Despite fading COVID-related revenue, Quest updated their full-year 2023 revenues to $9.12B -$9.22B.

- The post-COVID labor market is posing challenges, including high turnover and elevated labor costs. As a result, I have downgraded my conviction level from 5/5 to 4/5.

- I intend to take advantage of the ticker’s lackluster performance and will look to add to my dormant DGX position below my Buy Threshold.

Quest Diagnostics (DGX) recently reported their Q2 earnings with a slight beat on EPS and revenue. Quest’s base business appears to be recovering from the pandemic and pulled in $2.30B in revenue, up 9.5% year-over-year. Although COVID-related revenues have faded, the company was encouraged enough to update their full-year 2023 revenues to $9.12B -$9.22B. Despite the beat on earnings and upgraded guidance, the market has let DGX continue to trade in a year-long pennant formation that has become a purgatory for the ticker. I intend to take advantage of the ticker’s lackluster performance and will look to add to my dormant DGX position below my Buy Threshold.

I intend to provide a brief overview of the company’s Q3 earnings. In addition, I discuss some of Quest’s growth opportunities as well as some of the ticker’s leading downside risks. Finally, I reveal my plan for managing my DGX position.

Q2 Earnings Overview

Quest Diagnostics reported strong Q2 performance in their base business, with nearly double-digit revenue growth year-over-year. This growth was driven by collaborations with health plans, hospitals, and physicians, as people returned to healthcare services. Notably, revenue from health system customers grew by almost 10% , and operational improvements were achieved despite employee turnover challenges .

The company reported their total adjusted operating margin improved meaningfully, rising over 170 basis points compared to Q1. Despite a decline of around $80M in COVID-related revenue, the company demonstrated positive margin growth.

Quest emphasized its strategic focus on meeting changing customer needs, predominantly in clinical arenas such as molecular genomics and oncology. The company’s acquisitions also played a vital role in driving growth. The company introduced Genetic Insights , their consumer genetics health test, and underlined their commitment to advanced diagnostics, including Alzheimer's blood tests and oncology testing for enduring or recurrent cancer.

Quest Diagnostics Genetic Insights (Quest Diagnostics)

{kind=link}

Quest also discussed how their M&A strategy focused on traditional hospital outreach purchases and tuck-in lab agreements is in a position to boost earnings. In addition, their decision to employ automation and AI through their Invigorate program added to operational enhancements, comprising automated microbiology solutions and AI-enabled data collection.

Financials

In terms of financials, Quest Diagnostics reported consolidated revenues of $2.34B in Q2, with their base business revenues growing 9.5% to $2.3B while the company’s COVID-19 testing revenues declined. Diagnostic Information Services revenues fell as a result of lower COVID-19 testing revenue, but robust growth was seen in the base business. Total base testing volumes increased by 7.4% , and labor to improve profitability yielded an expanded adjusted operating margin.

Looking ahead, Quest upgraded their guidance for 2023, raising base business revenue expectations. Quest expects their revenue balance along with an adjusted EPS distribution in the second half. The company aimed for an adjusted operating margin of approximately 16.5% for the full year.

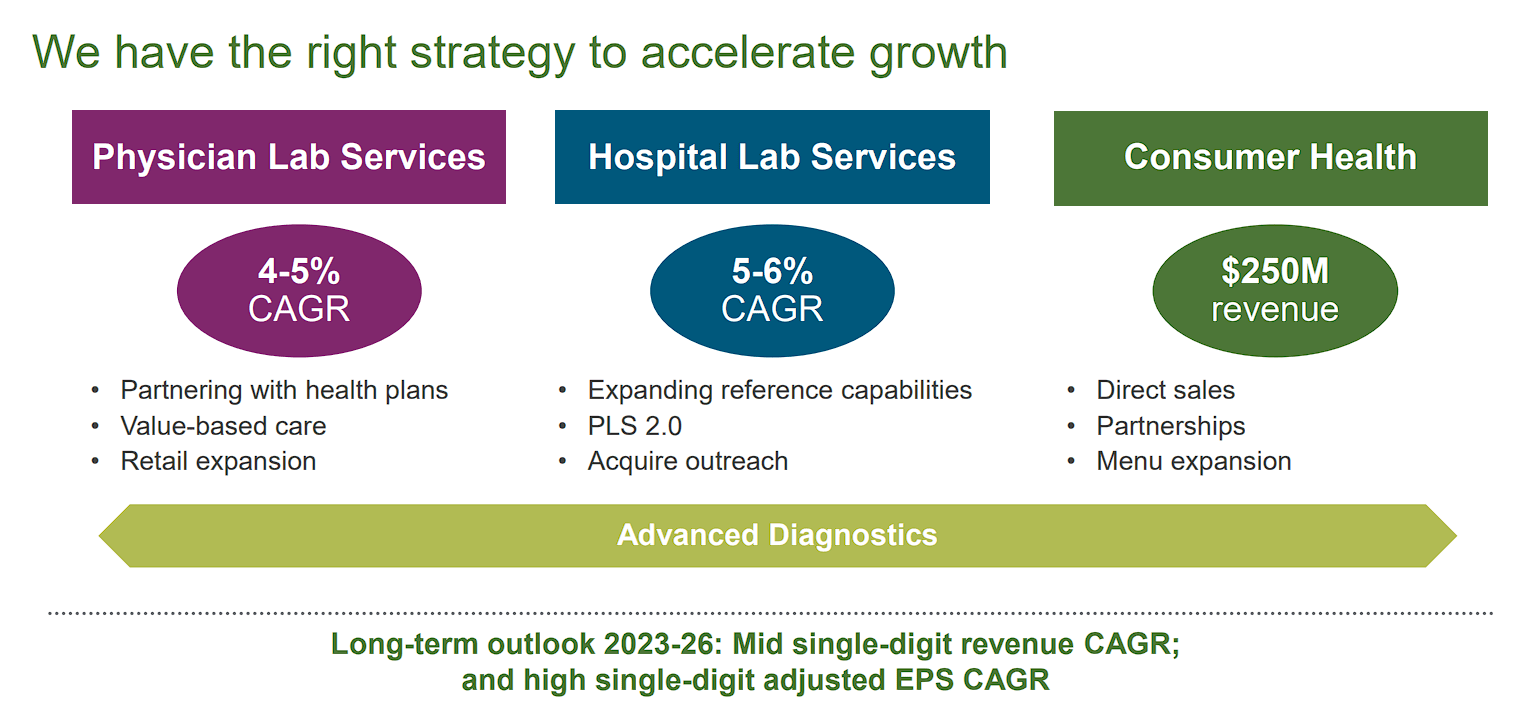

Finding Growth

Listening to Quest’s earnings call, it is clear that the company is attempting to obtain extra growth by claiming market share gain while trying to create demand for the company’s services in physician lab services, hospital lab services, and consumer health. The company believes they will work with commercial payers and utilize value-based programs to direct requisitions to Quest and thwart physician leakage to out-of-network labs.

Quest Diagnostics Growth (Quest Diagnostics)

{kind=link}

In addition, the company expects that they will continue to make investments in molecular genomics, oncology, Alzheimer's portfolio tests, and CIT. Moreover, Quest is not ruling out additional M&A and making deals to secure supplementary growth opportunities.

The company expects “mid-single-digit CAGR and high single-digit adjusted EPS CAGR between 2023 and 2026.”

Downside Risk

Although Quest appears to be dealing with the COVID transition pretty well, the impact of the post-COVID labor market is posing challenges including high turnover and elevated labor costs. Obviously, the higher turnover rates will impact productivity and the labor costs will hit the company’s margins. So, it is possible we see an elevated SG&A in the coming quarters and possibly some fluctuations in margins.

I don’t believe these issues will have a huge impact on the company’s performance, however, their earnings reports might not be as attractive with problematic fluctuations that are at the mercy of the labor market. As a result, I am changing my conviction level for DGX from 5 out of 5, down to 4 out of 5. I am still bullish… but, I am going to be more selective with my additions.

My Takeaway

Well, the primary takeaway is that Quest was able to quickly offset the expected decline in COVID testing revenues, with their base business and acquisitions. This quick change in the line from handling a massive amount of COVID tests to quickly returning to standard operations is quite impressive. This almost seamless change is notable because it was a major concern for some analysts as some of the COVID-related companies have struggled to make the transition back. Still, the company doesn’t really have many levers to pull to extract substantial growth in the coming years. Plus, the issues with the labor market might create some foot-dragging amongst investors, so DGX investors should not expect the ticker to hit all-time highs in the near future.

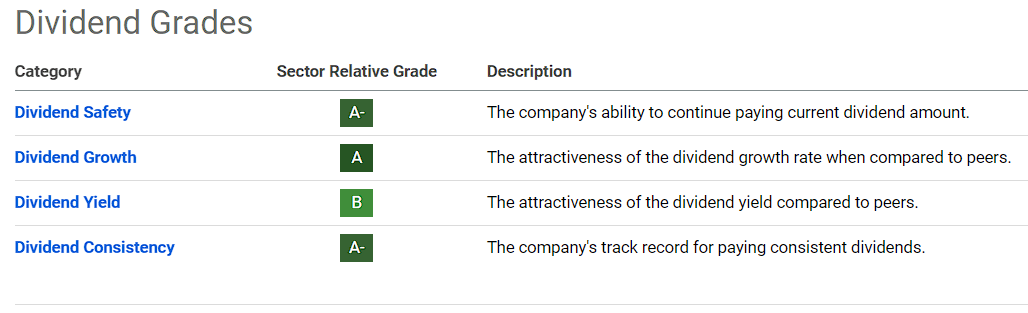

On the other hand, the ticker’s dividend is still really healthy with a $0.71 quarterly dividend and 11 years of dividend growth.

DGX Dividend Grades (Seeking Alpha)

{kind=link}

Therefore, I am more than comfortable with waiting and accumulating shares while we wait for the company to navigate the current labor environment and find some additional growth opportunities.

My Plan

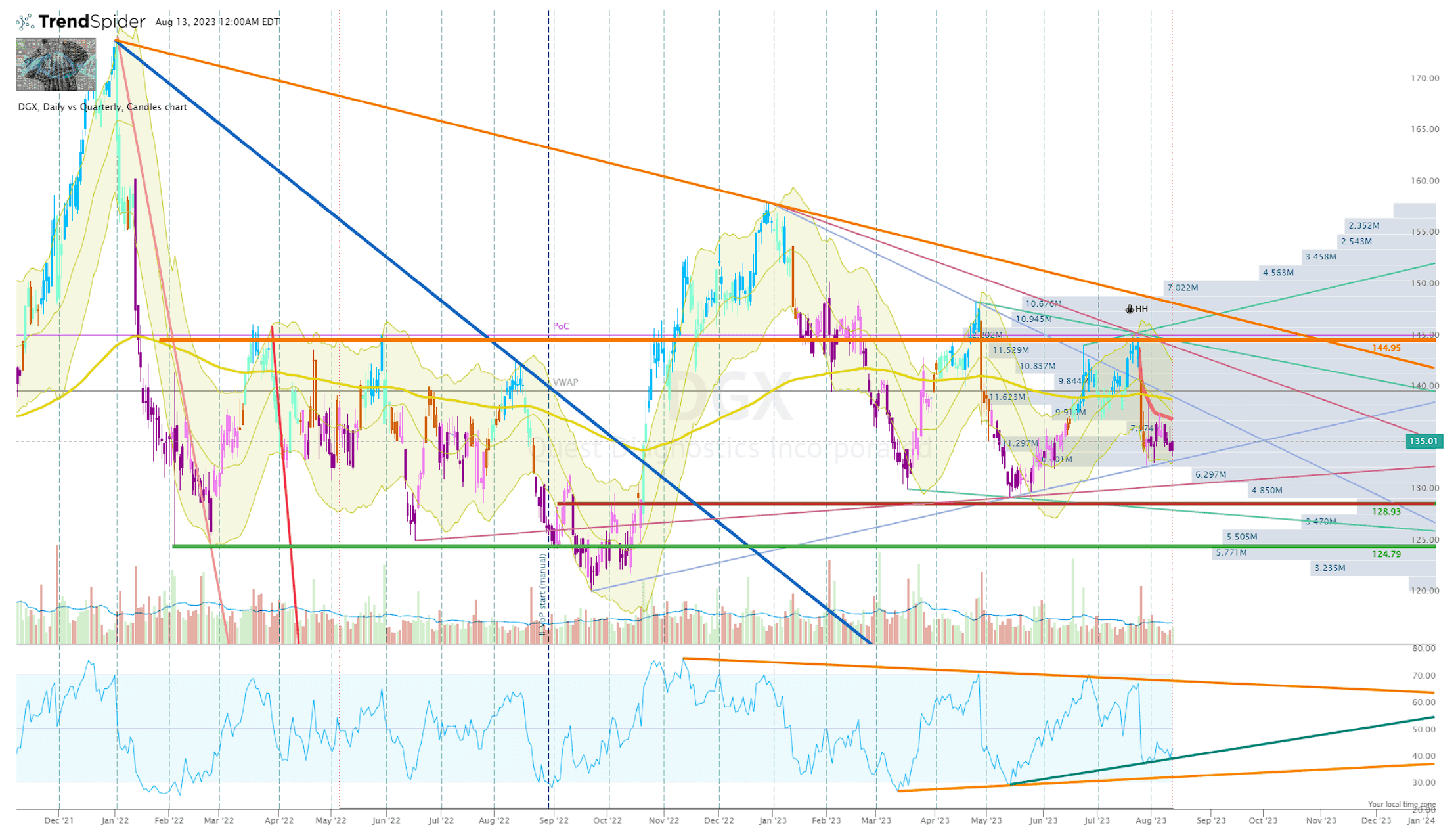

MY DGX position has been incredibly dormant over the past 12 months. In fact, I have only made one small addition back in September of 2022, thanks to a beautiful bullish divergence on the DGX Daily Chart.

{kind=link}

DGX Daily Chart Enhanced View ( Trendspider )

Since then, I have been sitting on my hands waiting for DGX to dip below my Buy Threshold of $129 per share, but with a solid reversal set-up. Well, we haven’t seen those conditions arise, so my DGX continues to remain in mothball at the moment. However, the ticker has been trading in this large pennant formation and the share price is hovering just above the bottom uptrend line of the formation. Perhaps the overall market or the sector will bring the ticker down below our Buy Threshold with a potential bounce around $125 per share. If the share price drops and bounces off $125, I will look to make a small addition. Until then, I will remain patient bull collecting a small, but healthy dividend.

Long term, DGX will remain in the Compounding Healthcare “Healthy Dividend” Portfolio for the foreseeable future due to its reliable dividend and its ability to benefit from its position as the largest player in the U.S. clinical laboratory market.

For further details see:

Quest Diagnostics: Q2 Earnings Reveal Promising Growth Trends Despite Dwindling COVID Testing Revenues