DGX - Quest Diagnostics Q4: The Kind Of Company We Like

Summary

- Core business generating robust growth structure with upsides versus consensus.

- Diverting capital away from COVID-segments into new growth initiatives.

- Able to reinvest relatively small portion of post-tax earnings at high rates of return, the rest as residual cash flows distributable to equity holders.

- 7.6% quarterly dividend increase on $1Bn authorized buyback.

Investment Summary

Quest Diagnostics Incorporated (DGX) posted Q4 FY22 earnings last week, with plenty to unpack. Its stock price has caught a reasonable after the print and investors will be pleased at the 7.6% increase in quarterly dividend and $1Bn in authorized buybacks. We've been positioning against long-term cash compounders exhibiting high returns on capital, and equally high distributable free cash to equity holders since early FY22. We make a long-term practical assessment of all potential allocations to our equity risk budget, and using that approach, have noted several changes worth noting on DGX from its Q4 numbers. Net-net, we rate the stock a buy at 24x P/E.

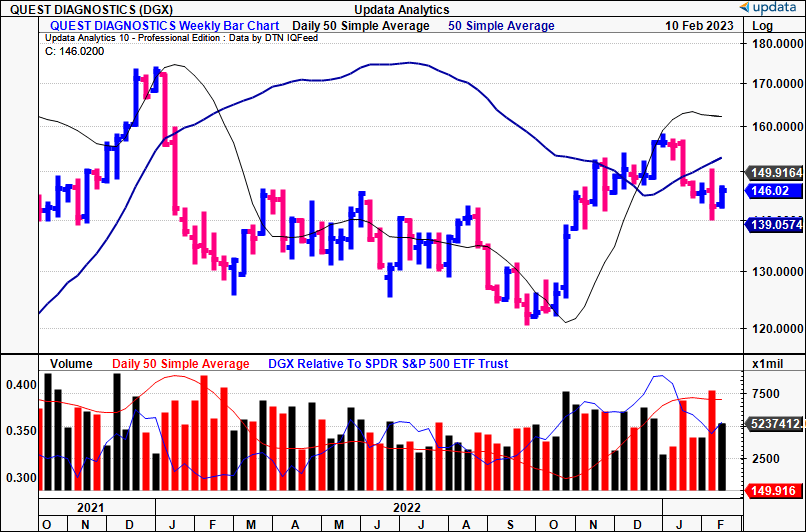

Exhibit 1. DGX price evolution

{kind=link}

Data: Updata

DGX Q4 results assessment

In examining DGX, it's important to take a practical view in backing out its COVID-19 performance to its core business segments. First, looking at what's changed:

Notably, Q4 top-line sales clipped $2.3Bn, a 15% YoY decrease. Yet, disaggregating this further, we see the core business grew 630bps to $2.15Bn and COVID-revenues slipped~75% to $184mm. Noteworthy, is diagnostic information services recorded a 15% YoY wind-back on the back of this. It pulled this down to core quarterly operating income of $135mm on a 5.8% margin, well off the 19.5% margin in Q4 FY21. On an adj. basis, operating income was $330mm vs. $580mm last year. We'd note the YoY decrease at the operating level stemmed from the reduction in COVID-related revenues. Moreover, it diverted capital over to its legacy business segments, as an extension of this point.

Moving down the P&L, Q4 earnings was $0.87 per share, and non-GAAP EPS came in to $1.98, each down from >$3 the year prior, again due to adjustments from COVID-sales. However, cash flows were still reasonably strong – $1.7Bn, down from $2.2Bn in Q4 last year.

Looking deeper at the results in more detail, we'd emphasize the movement in its key operating metrics, namely:

- Number of requisitions [total volume] decrease of 11.2% YoY, where acquisitions attributing ~20bps to volume.

- Related to 1), although total revenue per requisition for the Q4 also slipped back by 510bps YoY, this was underscored again by the COVID-normalization. Extrapolating this further, the core business's revenue per requisition was up 680bps.

- Extending on the above point, there were multiple growth drivers to the core business revenue per requisition, specifically the more benign pricing environment, reduced patient concessions and consistency in the unit price reimbursement [~50bps for Q4, as reported].

- Looking at the COVID-testing segment further, DGX reported ~1.9mm molecular tests, a decrease of 5.4mm over the 12 months. Management put this at an average decrease of "roughly 17,000 tests per day in January and currently make up less than 3% of our daily volumes".

Next, understanding what's driving DGX's value. As mentioned, we make a practical assessment of each name in our coverage universe, beyond the reported growth percentages. This involves a deeper analysis on profitability, namely, ROIC and reinvestment for growth. This is integral in tracking the estimated growth route for DGX looking ahead.

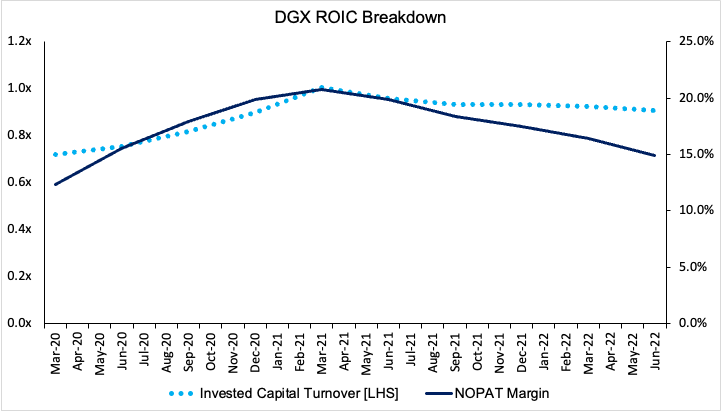

For a broader view, we examined rolling TTM periods to Q4 FY22. Looking at DGX's return on investments, observed below, note that it generated double-digit ROIC each period. Even with the decrease in post-tax earnings, related to COVID-turnover points above, DGX remains profitable moving into the new year.

Exhibit 2. DGX periodic ROIC

{kind=link}

Data: Author, using data from DGX SEC Filings

Our readers might recall that ROIC can be disaggregated further into its subcomponents, NOPAT margin and invested capital turnover. As expected, the former, measuring profit per unit, has clipped back since FY21. Yet, DGX has diverted capital into new growth areas, noted by the divergence between the two lines in Exhibit 3.

Exhibit 3.

{kind=link}

Data: Author, using data from DGX SEC Filings

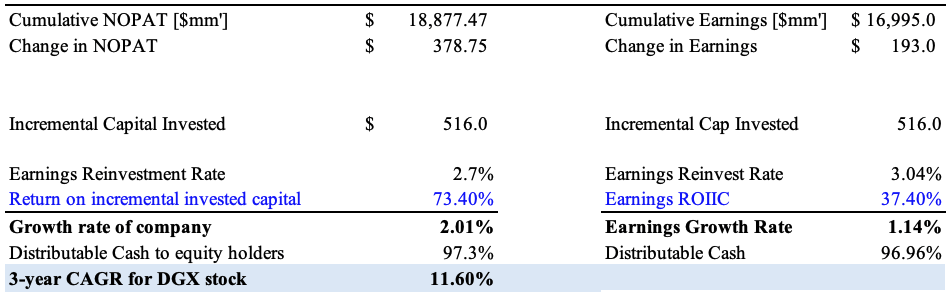

Considering the divergence and lower contribution from COVID-related revenues looking forward, it's essential to gauge the effectiveness of DGX's capital investment decisions over the testing period. To measure the success of this, we emphasize the cumulative gain in post-tax earnings, the delta of the same, and the incremental return on invested capital ("ROIIC"). See in Exhibit 4, that, over the testing period, DGX generated a cumulative $18.8Bn in NOPAT, on ~$17mm in earnings, with additional growth of $378 and 193mm respectively.

The following observations can therefore be made from these figures [see: Exhibit 4]:

- To generate the NOPAT and earnings numbers above, it invested an additional $516mm capital.

- Related to the above, it only reinvested ~3% of NOPAT and earnings on this investment to grow.

- Subsequently, the ROIIC was 73.4%, [37% on earnings], alas, a 2.7% investment for a 73% return.

- In that vein, ~97% of post-tax earnings were distributable to equity holders.

- This supports the dividend increase and the impeding buyback and serves as critical data to extrapolate for the forward-looking analysis.

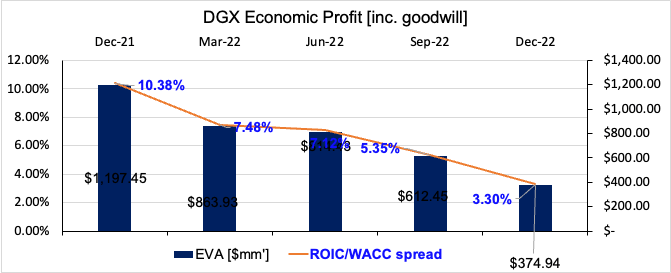

- Because the incremental and periodic ROIC's were above the cost of capital YoY, [see: Exhibit 5], the economic profit meant the growth was certainly accretive to shareholder value.

- These numbers also represent the reinvestment for future growth of the company.

Exhibit 4. Substantial incremental return on investment

{kind=link}

Data: Author, using data from DGX SEC Filings

Exhibit 5.

{kind=link}

Data: Author

The only criticism we'd make from this analysis, is that if DGX is generating such high rates of return, it could be more appropriate for it to reinvest a higher proportion of post-tax earnings to generate more growth. Using the above calculus, we estimated that with a 15% reinvestment rate, DGX would realize an 11% forward growth rate [assuming the same ROIIC]. This creates an opportunity cost for the dividend and buyback, nonetheless, is food for thought. Hence, any increase in reinvestment into growth it likely to yield positive results for the company in our opinion, serving as a strong springboard for DGX to work from.

Valuation and conclusion

Aside from analysis on how DGX generated value for equity holder listed above, the company announced a 7.6% increase in quarterly dividend, plus $1Bn in authorized buybacks. It also trades at a respective discount to sector peers across the majority of money multiples, with a 25% discount at 18x trailing P/E alone. Moreover, it trades at a 21% premium to its 5-year P/E average

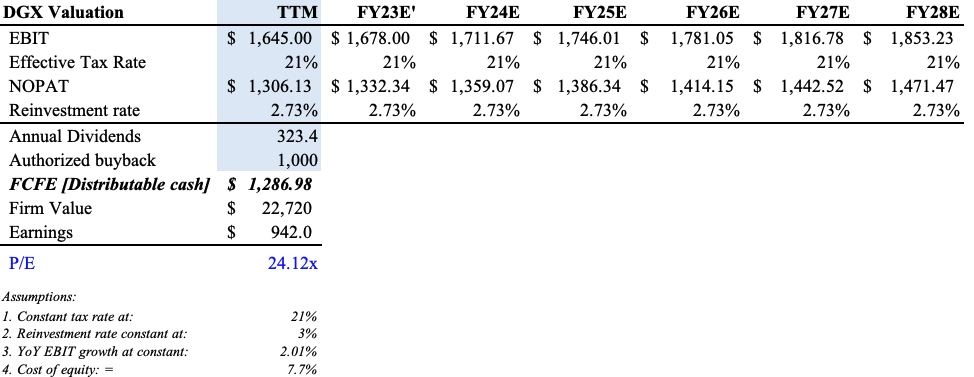

Taking into consideration forward guidance as well – $9Bn in top-line sales at the upper end of range, with core EPS of $7.61–$8.21 on cash flows of ~$1.3Bn – the firm looks well positioned to reinvest into new growth initiatives at high rates of return. In this vein, we derived a valuation of 24x P/E. Key supportive points to this valuation include:

- Considerations to its reinvestment for growth,

- The incremental ROIIC on new growth initiatives

- Dividends/buybacks

- Forward guidance

Subsequently with the stock priced at 18x trailing earnings, this looks undervalued, and eye a price target of $189 at 24x EPS estimate of $7.91.

Exhibit 6.

{kind=link}

Data: Author estimates

Net-net, extrapolating the data presented in this analysis, forward-looking numbers look appealing for DGX and we are constructive on the name for this reason. We see the stock fairly valued at 24x P/E and are eyeing a price target of $189 over the coming 12 months.

For further details see:

Quest Diagnostics Q4: The Kind Of Company We Like