DGX - Quest Diagnostics Remains A Solid Long-Term Company

2023-03-20 04:20:31 ET

Summary

- Quest Diagnostics core business is experiencing strong growth and has a structure that could potentially exceed market expectations.

- The current valuation seems very promising and making an entry at these prices I think would offer good returns.

- DGX has the ability to reinvest a small portion of its post-tax earnings at high rates of return, and the remaining amount can be distributed to shareholders through dividends.

Investment Summary

While Quest Diagnostics Incorporated's (DGX) profitability margins have been affected in the short term, the company remains financially stable with solid cash flow from operations. The company's valuation metrics are generally in line with industry peers, suggesting that it may be fairly valued.

Looking ahead, Quest Diagnostics is well-positioned to benefit from ongoing trends in the healthcare industry, particularly in the areas of personalized medicine and population health management. However, the company is also exposed to a number of risks, including increasing competition, potential regulatory changes, and ongoing uncertainties related to the pandemic.

Company Overview

Quest Diagnostics Incorporated is a leading provider of diagnostic testing, information, and services in the United States. The company was founded in 1967 and is headquartered in Secaucus, New Jersey.

Quest Diagnostics operates through a network of more than 2,200 patient service centers and laboratories in the United States, providing a comprehensive range of diagnostic testing and information services to patients, physicians, hospitals, and other healthcare providers. The company's services include routine blood tests, infectious disease testing, genetic testing, and drug testing, among others.

The company's focus is to improve patient health and enable better healthcare outcomes through diagnostic insights. The company's focus on innovation, quality, and customer service has earned them recognition as a leader in the diagnostic testing industry.

Revenue Breakdown

Quest Diagnostics, the world's leading provider of diagnostic information services, announced its financial results for the fourth quarter and full year that ended December 31, 2022. The company reported a decline of 15% in its fourth-quarter revenues, which came in at $2.33 billion compared to the same period in 2021. Despite the drop in revenues, the company's base business revenues grew more than 6% in the fourth quarter, and 5% for the full year, which is a positive sign for the company. Full-year revenues also declined by 8.4% from 2021, totaling $9.88 billion.

Earnings Highlights (Q1 Report)

The company's fourth quarter reported diluted EPS of $0.87 was down 72.1% from 2021, while adjusted diluted EPS of $1.98 was down 40.5% from 2021. Similarly, full-year reported diluted EPS of $7.97 was down 48.7% from 2021, while adjusted diluted EPS of $9.95 was down 30.1% from 2021. Although the EPS numbers were down, it is important to note that the company's base business revenues increased by 5.1% from 2021, which is a positive indicator.

Quest Diagnostics' fourth quarter COVID-19 testing revenues declined by 74.6% from 2021, coming in at $184 million. Full-year COVID-19 testing revenues also declined by 47.5% from 2021, totaling $1.45 billion. However, CEO and President Jim Davis said that despite the decline in COVID-19 testing revenues, the company still exceeded $1.4 billion in 2022. This suggests that the company has been able to diversify its revenue streams, which is a positive for the company's future growth prospects.

Looking forward, Quest Diagnostics expects its reported diluted EPS for 2023 to be between $7.61 and $8.21, while adjusted diluted EPS is expected to be between $8.40 and $9.00. The company's base business revenues are expected to continue growing, and it remains to be seen if the COVID-19 testing revenues will pick up as the pandemic situation evolves.

In conclusion, while Quest Diagnostics' fourth-quarter revenues declined by 15%, the company's base business revenues increased by 6.3%, and it still exceeded $1.4 billion in COVID-19 testing revenues in 2022. The CEO's positive outlook for the company's growth prospects suggests that Quest Diagnostics is well-positioned to navigate the challenges posed by the COVID-19 pandemic and grow its business in the future.

Market Tailwinds

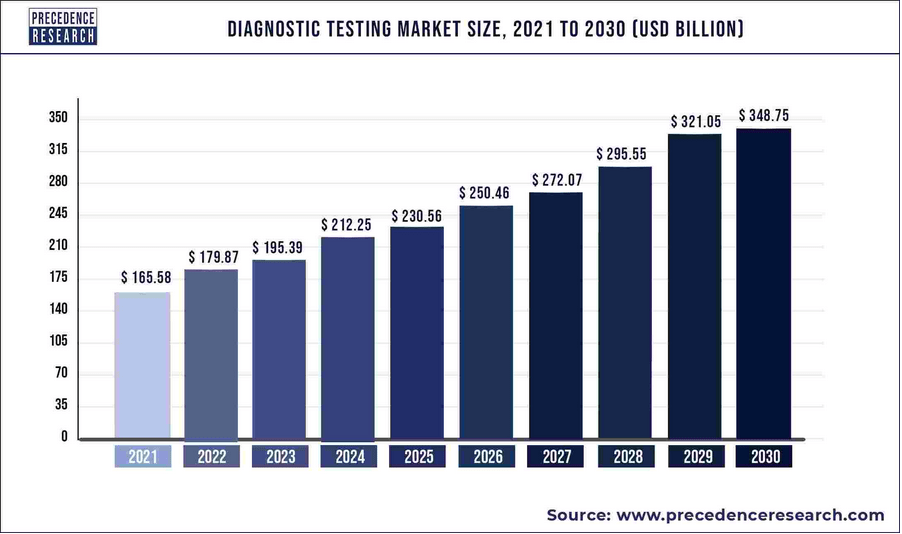

The diagnostic testing industry is expected to experience significant tailwinds in the coming years. According to a report by PrecedenceResearch , the global diagnostic testing market is projected to grow at a CAGR of 8.63% from 2022 to 2030, reaching $348 billion by 2030.

{kind=link}

One of the main drivers of this growth is the increasing prevalence of chronic diseases and infections, which requires frequent monitoring and testing. In addition, the aging population and growing demand for personalized medicine are also contributing to the growth of the industry.

According to a statement by Quest Diagnostics CEO Jim Davis, "As the population ages and chronic diseases become more prevalent, there will continue to be a strong demand for diagnostic testing services." He also noted that advancements in technology and data analytics are enabling more accurate and efficient testing, further driving growth in the industry.

Experts also predict that the COVID-19 pandemic could continue to boost demand for diagnostic testing services. While COVID-19 testing revenues declined for Quest Diagnostics in 2022, the company still exceeded $1.4 billion in testing revenues for the year. As variants of the virus could emerge there will be an ongoing demand for testing and monitoring.

In conclusion, the diagnostic testing industry is expected to experience strong tailwinds in the coming years, driven by factors such as the increasing prevalence of chronic diseases, the aging population, and advancements in technology. While the COVID-19 pandemic could contribute to short-term volatility in testing revenues, the long-term outlook for the industry remains positive.

The Company's Profitability

Looking at the income statement, we can see that Quest Diagnostics reported a decline in net revenues of 15% for the three months ended December 31, 2022, compared to the same period in the previous year. The decline is mainly due to a drop in COVID-19 testing revenues, which decreased by 74.6%, while the diagnostic information services revenues also decreased by 15.3%.

On the positive side, the base business revenues increased by 6.3%, which is a good sign that the company's core operations are growing. However, the decline in revenue per requisition of 5.1% and the decrease in requisition volume of 11.2% indicate that the company may be facing challenges in maintaining its market share.

Assets (Q1 Report)

When it comes to profitability, Quest Diagnostics reported an operating income of $135 million for the three months ended December 31, 2022, which is a significant drop of 74.9% compared to the same period in the previous year. The operating income as a percentage of net revenues also decreased significantly from 19.5% to 5.8%. This decrease in operating income is mainly due to the decline in COVID-19 testing revenues, which had high margins.

However, when we look at the adjusted operating income, we see that Quest Diagnostics was able to maintain a healthy operating margin of 14.2%. This indicates that the company was able to manage its expenses efficiently during the pandemic and maintain profitability, despite the decline in revenues.

In terms of net income, Quest Diagnostics reported a decline of 74.2% in net income attributable to Quest Diagnostics for the three months ended December 31, 2022, compared to the same period in the previous year. The diluted EPS also declined by 72.1%. However, the adjusted net income attributable to Quest Diagnostics declined by 44.9%, and the diluted EPS declined by 40.5%. These adjusted figures show that the company was able to maintain profitability and generate earnings per share that were in line with market expectations.

Cash Flow Statement (Q1 Report)

When compared to other companies in the industry, Quest Diagnostics' operating margin of 14.2% is higher than the industry average, which is around 10%. This suggests that Quest Diagnostics is more efficient in managing its expenses than its peers in the industry. However, the decline in revenues and net income indicates that the company may be facing challenges in maintaining its market share and expanding its business.

In conclusion, while Quest Diagnostics faced challenges due to the decline in COVID-19 testing revenues, the company was able to maintain a healthy operating margin and profitability, thanks to its efficient expense management. However, the decline in revenue per requisition and requisition volume suggests that the company needs to address challenges in maintaining its market share in the long term.

Risks

Quest Diagnostics operates in a highly competitive industry, with several established players and new entrants. Competition could lead to pricing pressures and loss of market share.

As a healthcare company, Quest Diagnostics is subject to regulatory risks, including changes in healthcare policies and regulations. Non-compliance with regulatory requirements could result in legal and financial penalties.

The choice of labs by patients primarily based on brand, cost, or convenience? The prevailing belief is that most patients tend to choose the lab closest to their work or home that is covered by their insurance provider, which could be Quest, LabCorp, or XYZ.

However, the perceived economic advantage of established players in this industry may not be as significant as previously assumed, given that CVS Health and other healthcare providers are now venturing into the diagnostic lab sector to offer convenience to their existing customer bases.

Investors should also be aware of the company's debt levels and liquidity position, as well as its exposure to interest rate risks. The company's financial performance and ability to generate cash flow could also impact its ability to invest in new technologies and growth opportunities.

Valuation And Conclusion

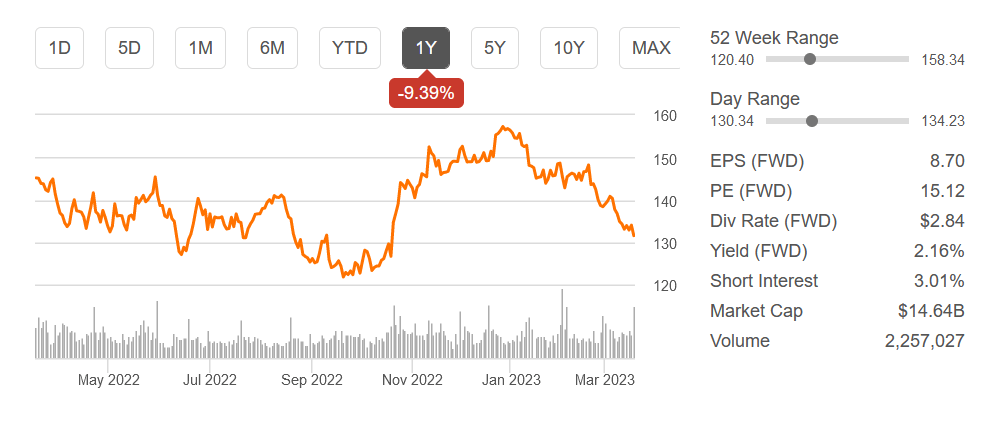

Quest Diagnostics has a market capitalization of around $14.6 billion. Based on the company's 2022 earnings, Quest has a price-to-earnings (P/E) ratio of around 13.2x, which is slightly below the industry average of 18x. The company's forward P/E ratio, which is based on estimated earnings for the next 12 months, is also around 15.1x, compared to the industry average of 18.6x.

{kind=link}

In conclusion, Quest Diagnostics is a well-established company with a strong market position in the diagnostic testing industry. The company has a solid financial performance and offers attractive dividend yields, which may make it an attractive investment option for income-oriented investors. However, investors should also consider the potential risks facing the company, such as regulatory changes and reimbursement rate cuts, as well as the impact of the COVID-19 pandemic on its financial performance.

For further details see:

Quest Diagnostics Remains A Solid Long-Term Company