QRTEB - Qurate Retail 4.85% 2024: The Last One Of My Favorite Short-Dated Bond

2023-03-06 04:45:55 ET

Summary

- Qurate has a 4.85% April 2024 bond outstanding.

- Qurate was an obvious "COVID over-earner" and the reality has caught up with the company.

- While the fundamental looks challenging, Qurate has ample liquidity to deal with the forgiving maturity profile.

- I believe the bond will be satisfied with cash on its stated maturity date - April 1, 2024.

Situation Overview

Qurate is confronting a series of maturities in the next few years. There is a small $214 million maturity due on March 15, 2023, followed by $320 million of puttable exchange notes, $600 million due on April 1, 2024, and another $600 million due on February 15, 2025. Against this series of maturities, Qurate has $1.275 billion cash on hand, $2.15 billion revolving credit facility capacity, and should generate positive free cash flow provided that the economy doesn't roll over precipitously.

To be perfectly clear, this trade is very different from my previous short-dated bond recommendations ( CNGO and ESI ) because this is purely a liquidity dance. Qurate is facing some obvious macro headwinds (cord-cutting and consumer spending) and I don't expect the fundamentals to turn around any time soon. However, given the somewhat forgiving maturity profile and ample liquidity, I believe the 2024 maturity will be satisfied with cash.

Company Description

Qurate Retail Group is a multinational e-commerce conglomerate that operates various retail brands across the United States, Europe, and Asia. It was founded in 1993 as QVC, Inc. and has since expanded to include several other well-known brands. Qurate Retail Group's portfolio includes QVC, HSN (Home Shopping Network), Zulily, Ballard Designs, Frontgate, Garnet Hill, and Grandin Road. These brands offer a wide variety of products including clothing, jewelry, beauty products, electronics, home decor, and more.

The company operates primarily through its TV channels, websites, and mobile applications, with a strong focus on customer engagement and interactive shopping experiences. Customers can view and purchase products through live TV broadcasts, online shopping, and mobile apps.

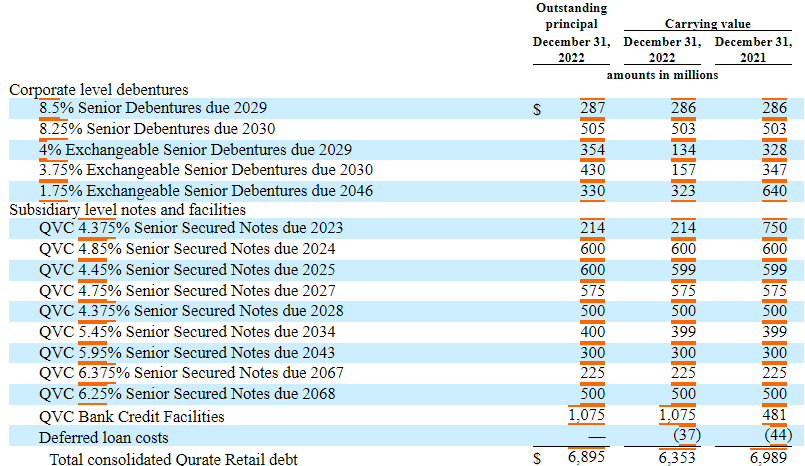

Capital Structure

Qurate has a complicated capital structure. For our purpose, a deep dive is unnecessary. Simplistically put, Qurate has two sets of obligations. The "corporate level debentures" are structurally junior to the "subsidiary level notes and facilities" because the latter is closer to the actual assets. In fact, corporate level debentures rely on upstream dividends from the subsidiaries to satisfy any interest, principal, dividend and tax payments.

{kind=link}

{kind=link}

On a consolidated level, Qurate's net leverage is ~5.3x (~$6.9 gross debt minus $1.3 billion cash, against ~$1.0 billion EBITDA). Through the QVC subsidiaries level, the net leverage is ~4.3x (~$5.0 billion gross debt minus $357 million sub-level cash, against the same ~$1.0 billion EBITDA). Another way to think about this is that there is ~$1.9 billion corporate (or holdco) level debt and the holdco doesn't generate any EBITDA.

EBITDA Pressure

While the leverage looks elevated, Qurate generated an EBITDA of $1.8-2.0 billion between FY2015 and FY2021. The recent EBITDA decline is due to topline decline (driven by cord-cutting and consumers pulling back on discretionary spending) and cost inflation (due to Rocky Mount fire and freight rate). The management expects stable revenue over the next two years, but double-digit EBITDA growth in 2023 and 2024. It's definitely an easier puzzle to solve on the cost side, especially after the recent headcount reduction and the normalization of freight rate, but I'm not sure if the revenue will stabilize soon, especially when Qurate is pulling back on marketing investment. In any case, I believe as long as we don't have a consumer-led recession where retail sales level drops significantly, Qurate should be able to stabilize its EBITDA at ~$1.0 billion level, and use the free cash flow to delever. Roughly speaking, $1.0 billion EBITDA should translate to $210 million free cash flow, after $440 million of interest payment, $230 million capex and $120 million of distribution rights payment.

Liquidity

As shown below, Qurate is fortunate that its maturity is spread out over the next few years and that it has ample liquidity. For FY2023, Qurate will pay off the $213 million March 2023 bond with cash on hand ($357 million at the QVC subsidiary level). For FY2024, adding the $210 million free cash flow to the remaining $144 million cash, there should be ~$350 million cash on hand at the QVC subsidiary level. Qurate will need to tap the credit facility to partially fund the redemption of the $600 million 4.85% 2024 bond. This assumes no EBITDA growth for the next two years. If we assume $1.2 billion EBITDA for FY2024, Qurate could almost self-fund the 2024 maturity and it can potentially refinance the 2025 maturity as well given the operating momentum.

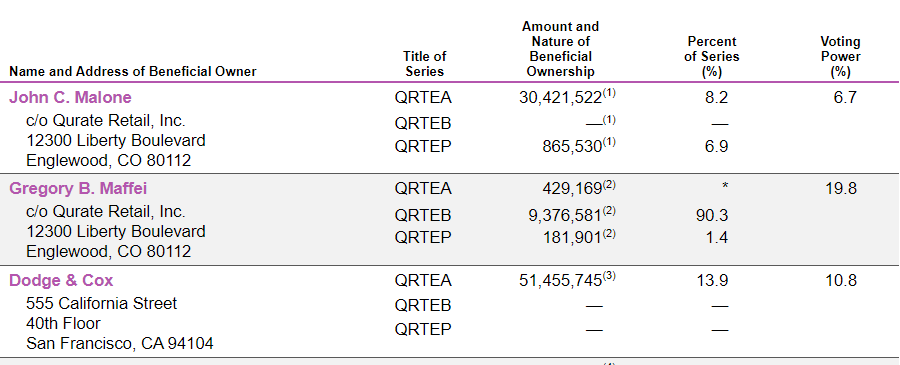

Major Shareholders

This is not a major part of my thesis by any stretch but it's good to see a billionaire owning a significant equity stake in the company. A deep-pocket and long-term focused investor like Malone could step in and provide some liquidity at the expense of other minority shareholders (but to the benefit of the bondholders).

{kind=link}

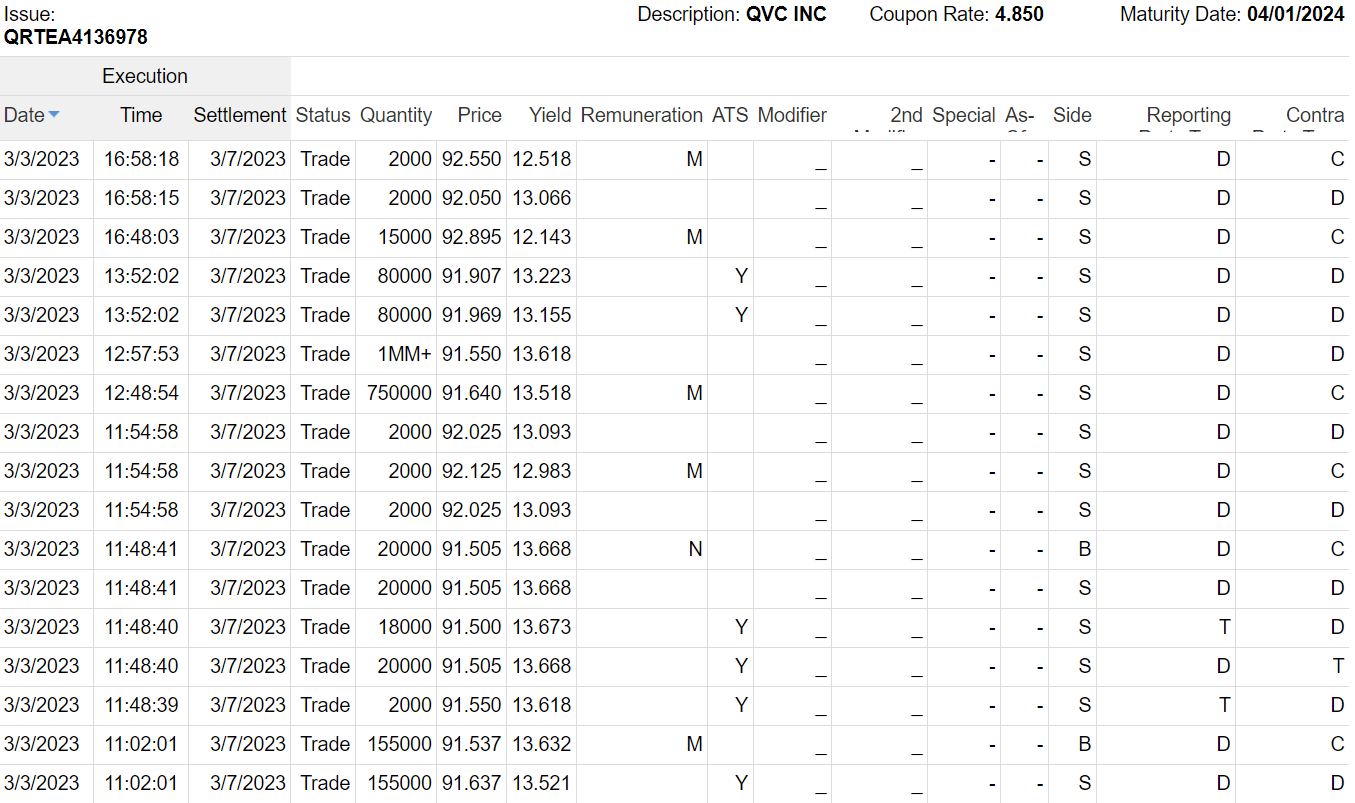

QVC 4.85% 2024

According to TRACE, Qurate 2024 is trading in the $91-92 context. I don't think Qurate is in any hurry to redeem this bond, so investors will most likely hold this bond to maturity, at which time my expectation is that the bond will be redeemed with cash on hand plus a little help from the revolver.

{kind=link}

Conclusion

In this uncertain market environment, the return of capital is more important than the return on capital. I believe Qurate's spread-out maturity profile will give it enough breathing room to tackle each bond maturity as they come due. There is also ample liquidity and free cash flow generation in the next two years to satisfy at least the 2023 and 2024 maturities.

For further details see:

Qurate Retail 4.85% 2024: The Last One Of My Favorite Short-Dated Bond