QRTEA - Qurate Retail: Appears To Have The Ability To Meet Future Debt Obligations

Summary

- Qurate Retail has faced a plethora of headwinds, creating downward pressure on customer count, sales, and margins, sending shares down over 70% in the past year.

- The market is pricing Qurate as if bankruptcy is imminent; however, cash flow models with modest assumptions appear to disagree.

- Qurate has plenty of short-term liquidity, with $2.5 billion in its credit revolver and ~$600 million of cash on its balance sheet.

- Qurate has a strong history of producing FCFs, and if current headwinds can be resolved in the next year, Qurate should be able to adequately deleverage.

- At the current price, the risk/reward ratio appears to be attractive, with the capability to 7x or -1x your investment in the next 5 years.

Investment Thesis

Qurate Retail ( QRTEA ) is the parent company of the popular Home Shopping Network and QVC, as well as Zulily and Cornerstone Brands. Home Shopping Network and QVC account for >80% of Qurate's revenue in Q3, making them the core of Qurate's business. Qurate operates in a sector that is arguably in a secular decline as streaming continues to triumph over cable. Qurate is also highly leveraged, which is exacerbating the recent headwinds the business has faced, leading many to fear that Qurate is on the edge of bankruptcy. However, I don't believe that the current price reflects realistic probabilities of the terminal value of Qurate. "Live shopping" has exploded in China, growing from a $3 billion market in 2017 to an estimated $171 billion in 2020. While they are many questions as to the future of live shopping in the US, Qurate appears to be well-positioned within the market. Additionally, recent struggles largely appear to be short-term, driven by the fire at their Rocky Moun tain Fulfillment Center and softening consumer demand. In regards to bankruptcy, Qurate has $2.5 billion available on their credit revolver (due 2026), ~$600 million in cash, and contrary to popular belief, strong FCF generation capabilities. With this in mind, Qurate offers a relatively binary investment opportunity. 5 years from now, Qurate will not be trading at $1-$3, they will be trading at $10+ or $0. After completing a detailed analysis of future cash flows, I believe that Qurate has the ability to pay off all upcoming debt maturities, and has a reasonably high chance of doing so. Therefore, given the risks, I believe that Qurate deserves a small position size in a portfolio, with LEAPs being an option to create additional risk/reward asymmetry.

Secular Decline or Rapid Growth Opportunity?

Qurate Retail relies on cable TV to generate sales from consumers watching on the QVC and HSN channels. Qurate has strong relationships with telecom and cable companies that distribute QVC and HSN to roughly 216 million households each day. However, cable TV is slowly dying, with only 56% of Americans watching TV via cable/satellite compared to 76% in 2015 . As there is no reason to expect a reversal in this trend, Qurate's fate seems to be tied to that of cable... Or is it? Qurate has made progress in its shift to e-commerce, mobile, and streaming, giving me hope that Qurate has some potential long-term growth opportunities.

As mentioned earlier, live stream shopping has been a booming industry in China over the last several years (from $3 billion USD to $171 billion USD in 3 years). If this trend is able to continue over to western nations in which Qurate operates, we could see a long-term secular shift for the business. In 2019, Amazon launched Amazon Live, allowing sellers to host live-stream shows to sell their products. Facebook also launched a live shopping feature in 2018, but later shut it down in October of 2022 . TikTok also revoked their plans to expand into e-commerce, implying weakness in western adoption of live stream shopping. Nonetheless, Qurate's e-commerce and streaming platform offer some hope amidst lackluster cable usage.

Roughly 60% of QxH's (QVC US and HSN) revenue came from e-commerce sales, with a majority coming from their mobile apps at 41% of total revenue. In June of 2022, Qurate launched the QVC+ and HSN+ streaming platform, which includes on-demand streaming of existing QVC/HSN channels, and also streaming exclusive channels. Qurate has expanded the streaming channels to Samsung Smart TVs, Fubo TV, Roku, Apple TV, Amazon Fire, and several others. Monthly active users for their streaming platform increased 40% QoQ in Q3 and when asked about streaming as a percentage of revenue, CEO David Rawlinson said ,

"So we haven't broken that out up until now. We're looking at how to give you some additional visibility into how to think about our streaming and context. I would say it's not a primary driver today, but it has been growing very quickly. It's material, but I wouldn't say it's a primary driver of results yet."

I think this is an interesting market opportunity for Qurate, but it likely won't be a driver of returns in the next year or two. Reporting streaming as its own segment could definitely serve as a catalyst, but the main focus of my thesis is whether or not the company can survive its debt obligations. Before we get into the current situation, let's look at what happened back in '09 when Qurate shares fell ~90% to <$2/share.

Bankruptcy Fears? This Isn't The First Time

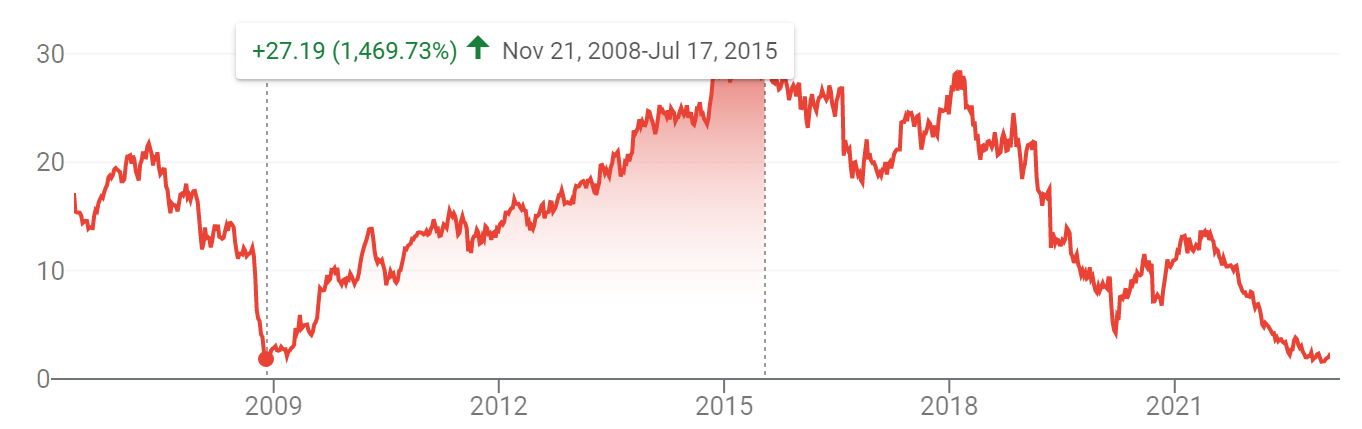

This isn't the first time that investors have worried about Quarte's ability to meet their debt obligations. Historically, Qurate has gotten away with high levels of debt due to their ample amount of FCF despite their large interest burden. This high degree of leverage allows them to generate ample returns when things go well, but generate bankruptcy fears when things go poorly. In December 2008, Qurate shares fell to $1.85, crashing from their 2007 high of $20+/share. Despite the troubling headwinds, Qurate eventually rebounded and rewarded investors with a 6-year run that generated returns of ~1500%.

{kind=link}

Declining sales led by the Great Recession and a large debt burden led to a price very similar to what we're seeing today. Despite these worries, Qurate proved that they were still a company that could generate strong FCFs, and have continued to do so. Qurate was able to pay off upcoming obligations by using a combination of FCF and newly issued long-term debt.

{kind=link}

I think this is one of the key differences that will make this rebound materially more difficult. As interest rates continue to rise, credit markets are seizing up, meaning Qurate won't be able to raise cheap long-term debt to pay off short-term obligations, at least not in the next couple of years. Qurate will have to rely on their current cash on the balance sheet, leasebacks, FCF generation, and credit revolver to survive the coming years. The question is, will they be able to meet their obligations until credit markets ease up? I think the answer is yes. Let's take a look.

Why Is Qurate Facing Bankruptcy Fears Yet Again?

As mentioned before, Qurate is a highly leveraged business. Net debt to EBITDA is currently sitting at 4.5x and EBITDA/Int Expense is at 3.2x. Qurate has several bonds maturing in the next couple of years, which is the primary reason for bankruptcy fears.

{kind=link}

(The $330 million obligation in 2023 is a call date for an exchangeable bond due 2046)

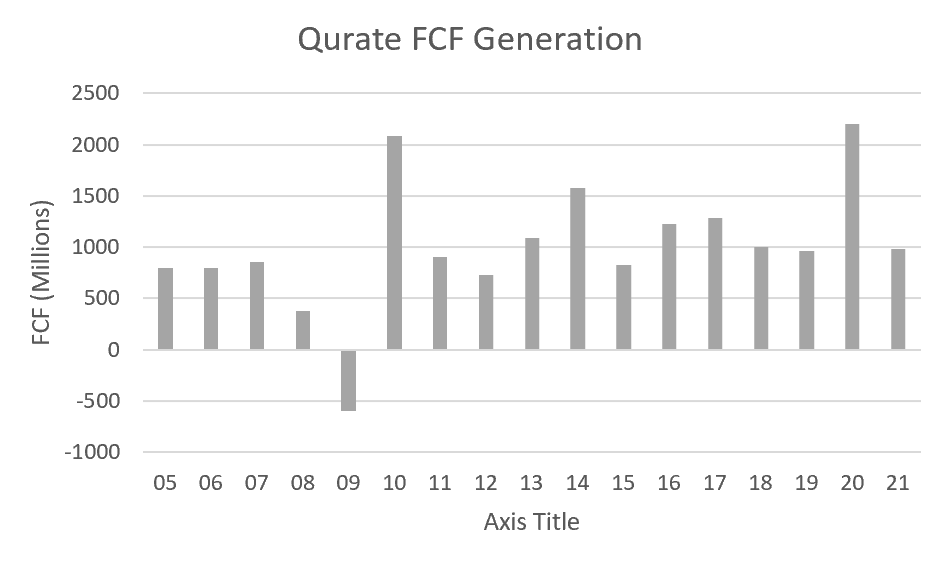

Qurate has almost non-stop maturities over the next several years, starting at the end of Q1 2023 (this quarter). I believe that Qurate needs to be able to pay off 2023, 2024, and potentially 2025 maturities without the safety net of issuing more long-term debt. This means they will need to do so with their current cash balance, FCF generation, leasebacks, and credit revolver. As mentioned before, Qurate has a long history of very strong FCF generation.

{kind=link}

As you can see, despite being a "melting ice cube", Qurate has continued to generate FCF of ~$1+ billion over the last decade. If the market thought this was going to continue, that would imply Qurate will have ample cash to pay off upcoming maturities, and would not be trading at ~$2/share. However, Qurate has been facing a substantial number of headwinds, which have led markets to question Qurate's cash generation abilities. This begs the question: will these headwinds persist for multiple years, or will they subside in the short term?

Plethora of Headwinds

Current headwinds can be put in two buckets:

- The December 2021 fire of the Rocky Mountain Fulfillment Center.

- Macroeconomic headwinds creating cost pressure, leading to softening consumer demand.

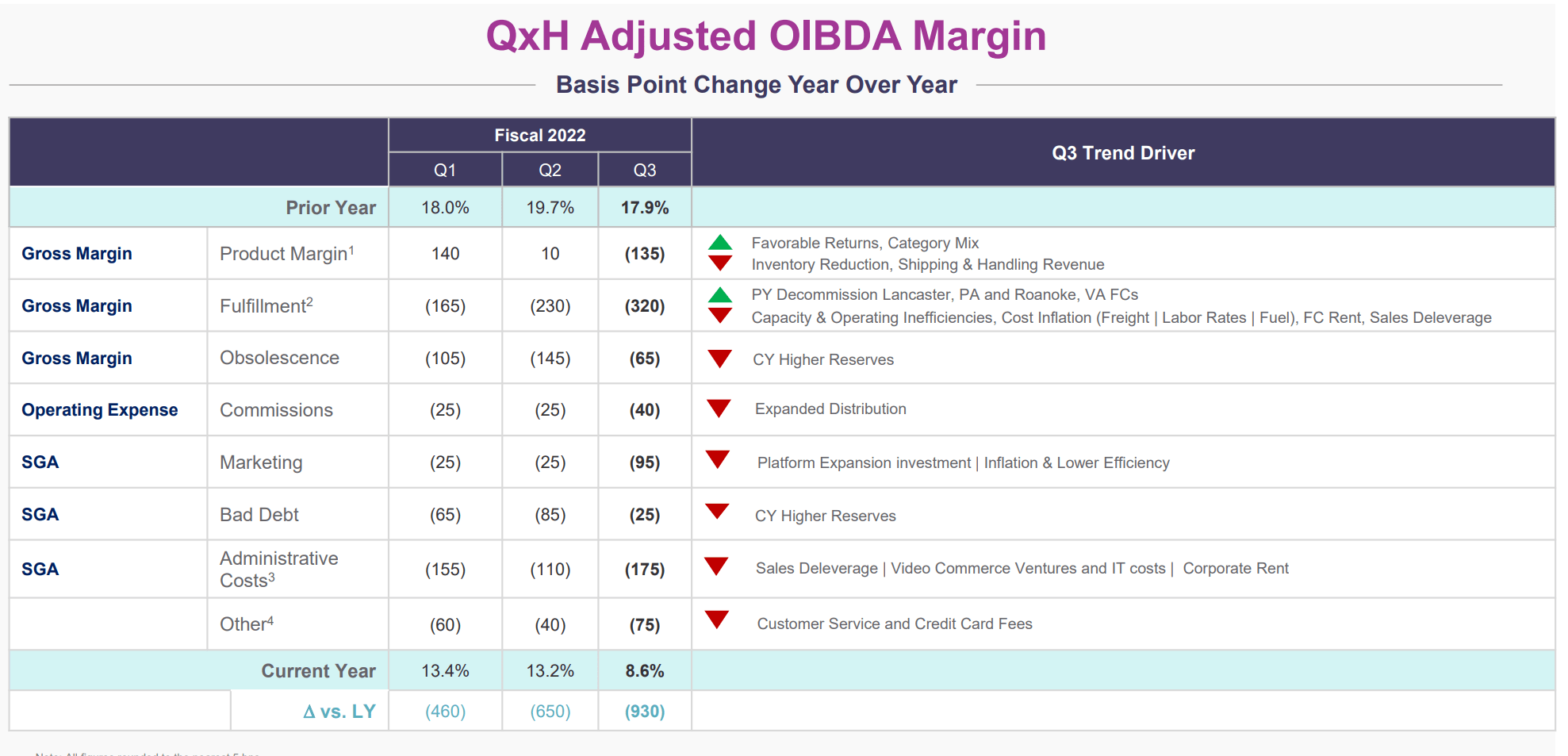

If we take a look at recent Adjusted OIBDA margins, we can get a good understanding of what's happened.

{kind=link}

The Rocky Mountain Fulfillment Center was Qurate's second-largest fulfillment center for QVC and HSN, Qurate's largest business segment. The actual loss of property is not really the main issue for Qurate. (One life was lost in the fire, which is truly more tragic than any financial repercussions the fire has caused) Qurate recognized a loss of $250 million in December 2021 and received $100 million of insurance proceeds in the same month. Qurate recognized another $147 million in losses in 2022, while also collecting another $280 million in insurance proceeds. Qurate also has $35 million worth of insurance receivables on its balance sheet. As you can see, insurance collections have offset the losses of the loss of inventory and PPE, but the effects are still being felt today.

Qurate Q3 Investor Presentation

{kind=link}

YoY, Qurate has experienced a 930 bps decrease in adjusted OIBDA margins. 520 bps of this decrease are due to a decrease in gross margins, which can be largely attributed to the Rocky Mountain fire. Qurate has had to rent an extraordinary amount of storage trailers to house excess inventory, causing dramatically increase costs and inefficiencies in fulfillment. CEO David Rawlinson said this during Qurate's Q3 earnings call,

"We improved our inventory position in Q3 with more than a 70% decrease in the numbers of trailers at our fulfillment centers by the end of Q3 compared to the end of Q1. That said, we continue to face capacity constraints at our fulfillment centers and incremental detention and demurrage costs. We expect to realize lower costs in Q4 due to the reduction in trailers. We also anticipate better capacity utilization as we have secured third-party logistics providers to alleviate some of the capacity constraints. We are close to retaining our normal operating goals for order-to-delivery times in our current fulfillment network. And going into the holiday season, we believe our fulfillment centers are well staffed."

To counteract the capacity constraints, Qurate has been trying to unload inventory, which means discounts and lower margins. We can see this reflected in the 135 bps decrease in "Product Margins" in the graphic above.

{kind=link}

In addition to the warehouse fire, Qurate has been facing the same macroeconomic challenges as the broader retail market. Inflationary pressures have negatively impacted Qurate, and they have not raised prices in response. "Despite elevated costs, we elected not to raise prices this year, primarily due to the macroeconomic environment and consumer sentiment, but also to manage our promotional cadence as we took actions to address excess inventory." (David Rawlinson Q3 Earnings Call)

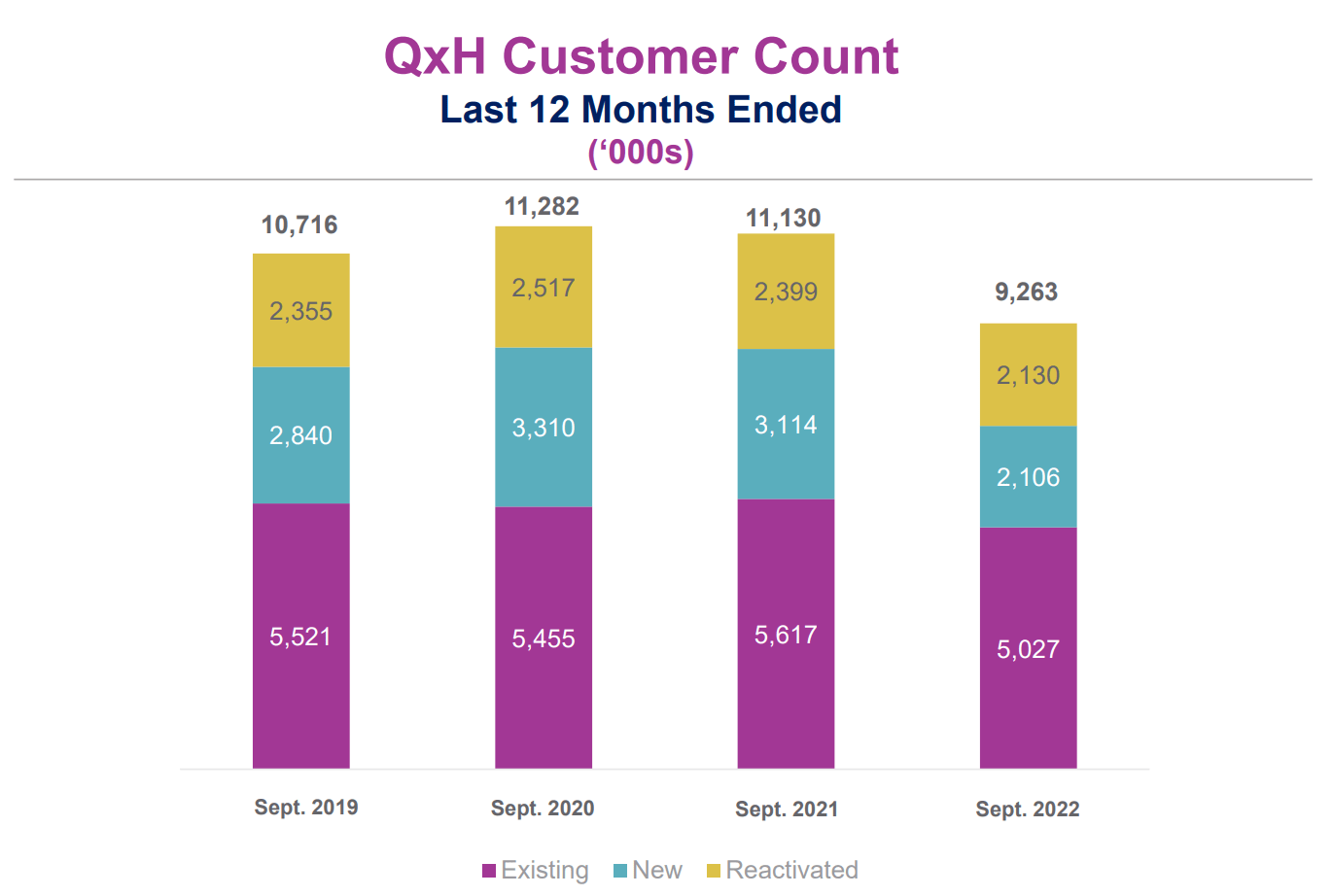

The other major headwind, caused by both the macroeconomic environment and the fulfillment center fire, is the decrease in QxH (US QVC and HSN) customer count.

Qurate Q3 Investor Presentation

{kind=link}

While existing customers only make up a little less than 50% of total customers, they make up for ~90% of sales. Existing customers have less churn and a much higher lifetime value than new and existing customers. The lack of retention of new customers is actually quite worrisome. Over the last few years, QxH has consistently had ~2-3 million new customers. However, existing customers barely increased through 2021 and have sharply declined as of Q3 2022. This lack of retention is likely a result of poor customer experience, which results in customers never buying from QxH again. This is a problem that goes beyond recent headwinds and is a long-term risk for the business. However, it has been exasperated by the macroeconomic environment as well as the warehouse fire. Poor order fulfillment and return management have likely led to an even worse customer experience, causing even the most loyal existing customers to churn off the platform. Here are some recent anecdotal customer reviews from Consumer Affairs ,

"Was a longtime customer but I'm never ordering from them again...[A] terrible company that doesn't follow through." January 2023

"I had been a QVC customer for over 12 years... I ordered an item the other day and it was in process. All [of a] sudden my order is canceled. I call customer service and get all kinds of responses that make no sense and are different. WHAT A AWFUL COMPANY! I have opened a BBB case and will continue. Not that I want to order from them EVER but will make sure nobody else has this happen to them."

While I don't want to place too much weight on anecdotal reviews, consumer review sites are filled with complaints saying they received the wrong item, or simply didn't receive an item at all. Poor customer experience has likely been the driver behind the decrease in customers, decrease in sales, and increase in SG&A margins due to unfavorable sales leverage. However, if Qurate can solve its fulfillment issues, I believe that could experience reduced churn and stabilized revenues.

With all of these recent headwinds in mind, let's try and figure out where Qurate is headed from here.

Looking To The Future

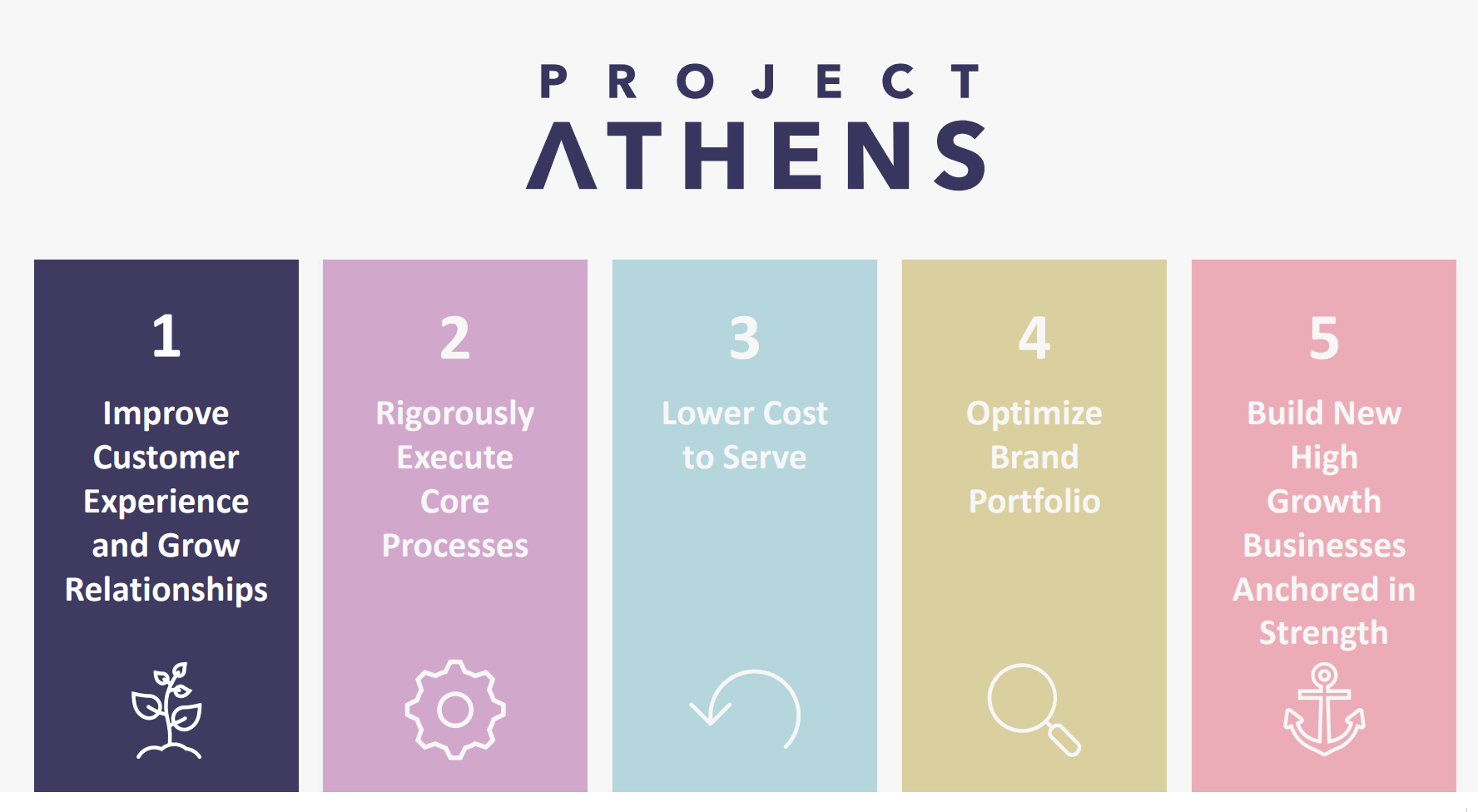

Qurate's relatively new management team (CEO David Rawlinson joined in Oct 2021) is implementing what they're calling "Project Athens". Project Athens has 5 main pillars:

Qurate Investor Day Presentation

{kind=link}

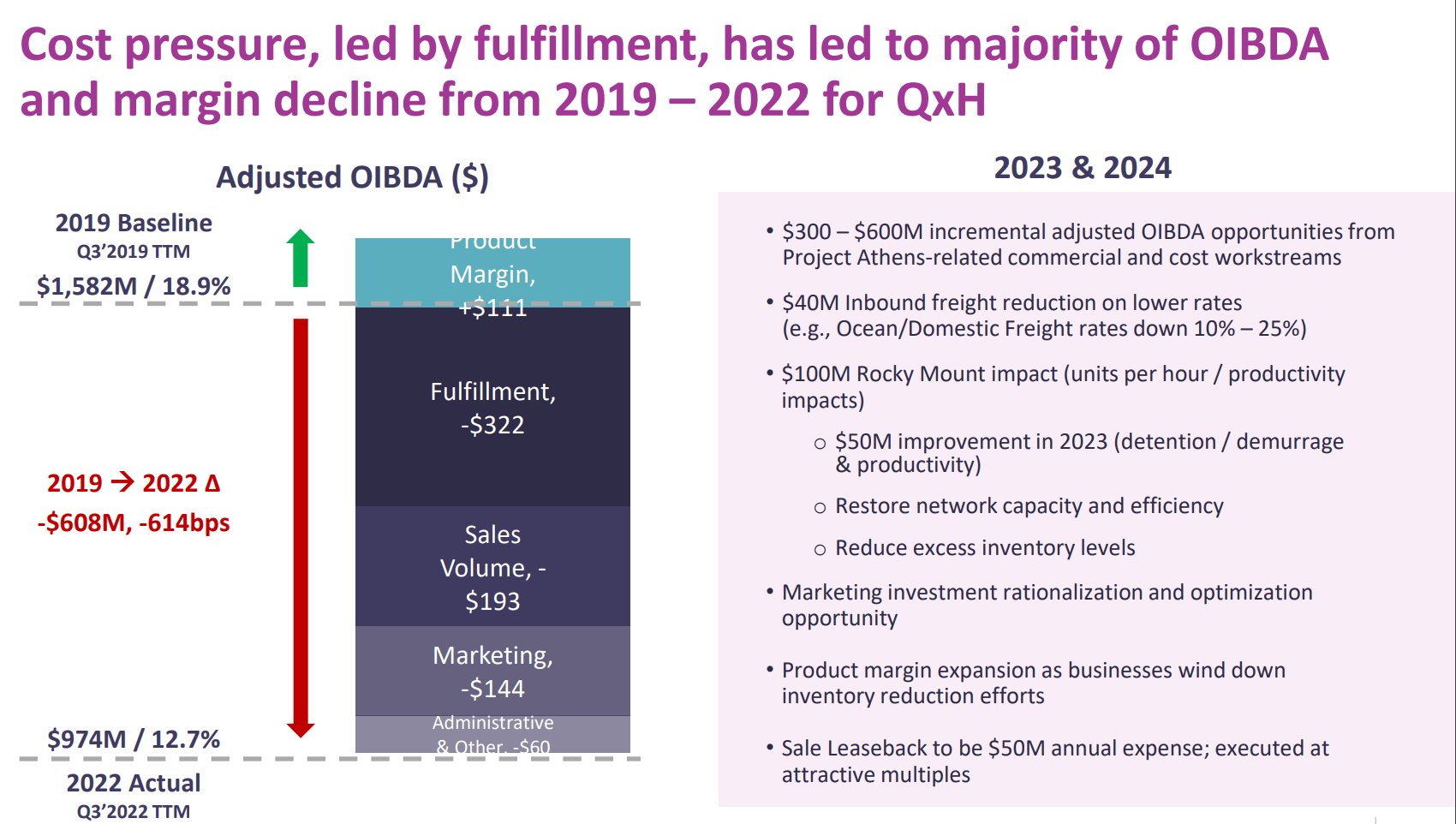

I've talked a lot about the recent headwinds creating margin pressure, so I'll start by looking at management's plans to stabilize margins. As mentioned earlier, Qurate has been reducing the number of storage trailers being used to house excess inventory. Additionally, inventory dumping should cease in Q1, leading to increased product margins. Qurate has also announced a hiring freeze and has reduced headcount by 7% YoY, which will help stabilize SG&A margins. A reduction in freight rates is expected to reduce $40 million in costs annually, offset by an expected $50 million expected annual increase in costs from sales leasebacks. Overall, management believes they can realize $300 million - $600 million of incremental OIBDA in 2023 and 2024.

Qurate Investor Day Presentation

{kind=link}

Using the Q3 LM TTM OIBDA of $974 million, a $300 - $600 million incremental increase would result in 2023 and 2024 OIBDAs of $1.274 billion and $1.674 billion. If management is able to manage even the lower end of this range, it appears that Qurate would be able to generate sufficient cash to meet its debt obligations.

I do believe that Qurate's biggest issue is its customer experience. I'm happy to see that "Improve Customer Experience and Grow Relationships" is the first pillar of Project Athens. They seem to be committed to fixing the problems that I discovered while looking through consumer reviews, "Improve post-purchase/returns experience; measure results through NPS scores".

Despite high levels of execution risk, there seems to be a clear pathway for Qurate to generate the cash required to pay off debts.

Modeling It Out

I'll provide screenshots of the important assumption of the model, but you can access the full model here .

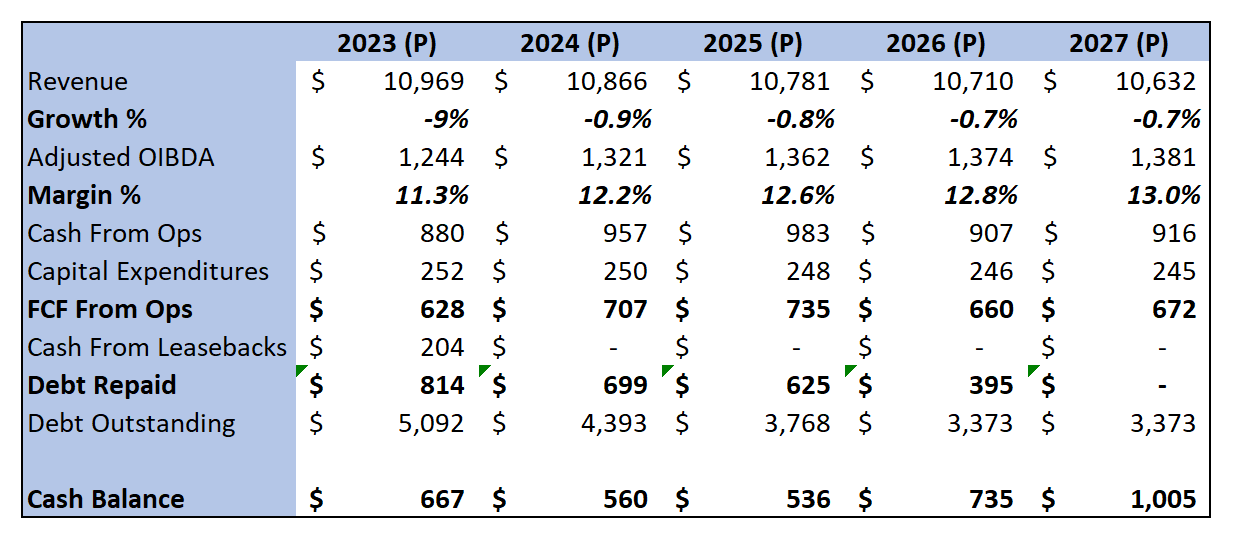

In the model, I project out all three statements quarter by quarter, line item by line item. Here's a summed-up version containing the most important items:

{kind=link}

In my projections, Qurate is able to maintain a healthy cash balance without drawing from its credit revolver.

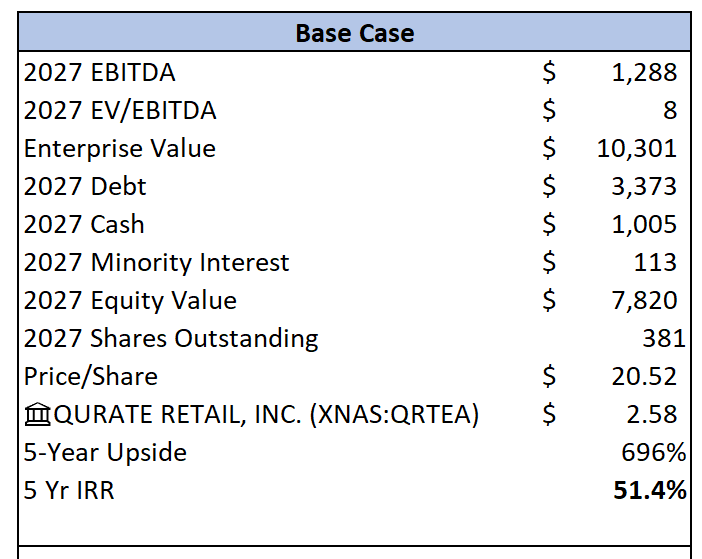

{kind=link}

With an implied 5-year IRR of 51.4%, I believe that Qurate adequately pays you for the risk you're taking.

Final Recommendation

At the end of the day, Qurate is a very risky investment, borderline speculative. Risks include declining customer count, poor customer experience, reliance on cable TV, margin pressure, softening consumer demand, and a heavy debt burden. Regardless, the risk asymmetry is what makes Qurate an attractive investment candidate. I think that Qurate shouldn't take a large position in any portfolio, but a small position due to the chance of permanent capital loss. Additionally, this is an investment that needs to be watched very closely. If it appears that headwinds are not being resolved after a few quarters, it may be time to reassess your position. Ultimately, with the potential to generate multi-bagger returns in just a few years, a small position in Qurate could turn out to be a lucrative decision.

For further details see:

Qurate Retail: Appears To Have The Ability To Meet Future Debt Obligations