QRTEA - Qurate Retail Isn't Going Bankrupt. Yet

2023-03-22 09:28:38 ET

Summary

- Qurate Retail is at all-time lows; the market thinks bankruptcy is imminent.

- The company faces a number of challenges, but there are few bankruptcy catalysts on the immediate horizon.

- Qurate might not survive another decade, but I think the odds are high that it survives the next 2-3 years.

- In this article, I look at the company over a variety of time frames and assess bankruptcy risk.

" First of all, I appreciate our limited audience. Two years from now when we are a rollicking success, y'all will be the only ones who heard the story in person, so welcome to the privileged few. " - David Rawlinson at Bank of America Consumer & Retail Conference, March 14th

Qurate Retail's (QRTEA) CEO David Rawlinson sounds confident that the company will still be around in two years. The market is... skeptical. The company's share price is down 66% in just the last two months and fell below the NASDAQ's minimum trading price of $1 on March 17th. The company's bonds are also trading at distressed levels. All market indicators are saying that QRTEA is going to go bankrupt in short order, but I think the company is more likely to survive, at least for the next few years. In this article I walk through potential bankruptcy catalysts over a variety of time frames and discuss their probabilities.

In all scenarios, I will make two assumptions. The first is that QRTEA will not be able to raise additional capital, neither via shareholder dilution nor by issuing new debt. Second, I am assuming that management will not voluntarily choose bankruptcy unless the company cannot meet its obligations with cash on hand. Both are possible, but I want to focus on QRTEA's operational performance in relation to its debt burden. I am also assuming that the reader is fairly familiar with QRTEA; I have another article I wrote recently that goes into more depth about the company here .

Will Qurate Retail Go Bankrupt in the Next 90 Days?

QRTEA started 2023 with $1.2b in cash and $2.15b available to borrow on their credit facility. The credit facility has limitations, but can be used for working capital needs and to pay off other debt. Over the next 90 days QRTEA will need to pay off the remaining $214mm of the 4.375% Senior notes due in 2023 and manage their working capital. Management stated that they expect a working capital tailwind of about $150mm in Q1, due to the timing of payments accrued in Q4 of last year ( source ). I expect this to translate into positive free cash flow in Q1 and at least flat free cash flow in Q2. Even using Q1 2022 free cash flow of -$200mm, net cash going out the door for operating needs and debt repayments only comes out to $414mm. Cash on hand can more than cover cash needs over the next 90 days, so I would rate the chances of bankruptcy in this timeframe as very low.

End of period liquidity (worst case): $2.9b (-$414mm in cash flow)

Will Qurate Retail Go Bankrupt by the End of 2023?

Once QRTEA pays down the 4.375% Senior notes balance in H1 of 2023, there are no other note payments due in the back half of the year. Management may choose to get a jump on repaying the 4.85% notes due in 2024 (there is an incentive to keep leverage ratios as low as possible), but this will not be required.

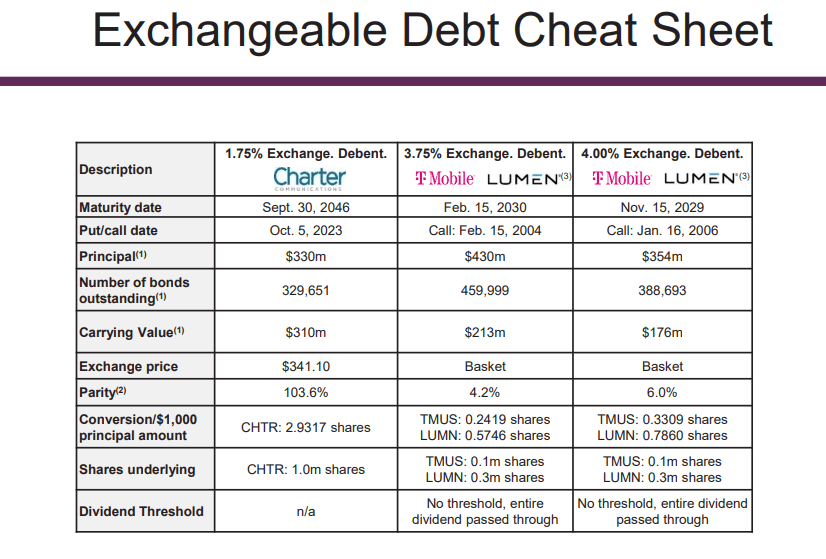

There are two other factors to consider for the remainder of 2023. The first is QRTEA's $1.1b worth of exchangeable senior debentures. Due to previous spin-off and subsequent acquisition transactions with other Liberty companies, QRTEA subsidiary Liberty Interactive LLC is responsible for three tracts of senior debentures:

Company 10-K

The 4% and 3.75% debentures can be exchanged for fractional shares of T-Mobile (TMUS) and Lumen (LUMN) at the discretion of the debenture holders, while the 1.75% debentures can be exchanged for shares of Charter Communications (CHTR):

{kind=link}

As the share prices of CHTR, TMUS, and LUMN fluctuate over time, the potential cash liability to QRTEA changes as well. The cash cost of an exchange of the 3.75% and 4% debentures, for example, is only $213mm and $176mm respectively, primarily because LUMN's share price has dropped significantly in recent years.

The 1.75% debentures are going to be the most relevant of the three in 2023, as these debenture holders have the right to exchange their debt into CHTR shares beginning this year. Given that 1.75% is an unfavorable interest rate (for investors) in today's economic environment and that CHTR shares are trading at a favorable exchange price, I think it is likely that QRTEA will receive substantial exchange requests this year and could potentially need to pay out the entire $330mm principal balance. QRTEA is protected from paying above the principal amount due to an indemnification agreement with Liberty Broadband Corporation (LBRDK).

The other major factor to consider is free cash flow. Management is implementing a turnaround plan (labeled Project Athens) that they expect will grow free cash flow generation in the second half of 2023 and more fully in 2024 and beyond. The plan involves cost cutting measures and a return of focus to the company's core customer base. Rawlinson says he expects the plan to generate an additional $300mm-$600mm in annual cash flow once it has been fully implemented ( source ).

Tipping the scale in the other direction is the potential for an economic recession. Macroeconomics is not my specialty, but you don't have to look far to find articles and opinions that expect a recession to begin sometime in 2023. A slowdown in consumer spending would unfavorably affect QRTEA's performance and cash flow, though the severity of the impact would depend on the severity of the recession. I could see a recession canceling out the benefits of Project Athens in H2 2023, causing break-even operating cash flow. If we assume the full $330mm of 1.75% debentures get called, we have negative cash flow of $330mm in H2, which is still comfortably covered by cash and the credit facility. I think the odds of QRTEA going bankrupt in 2023 are very low.

End of period liquidity (worst case): $2.57b (-$330mm in cash flow)

Will Qurate Retail Go Bankrupt by the End of 2026?

QRTEA has $600mm of senior notes due in both 2024 and 2025, for total debt repayments of $1.2b. With over $2.5b of liquidity likely available at the end of 2023, as long as the company can avoid burning $1.3b in cash over those two years, I would expect them to be able to stay afloat. October 2026 is the first major bankruptcy catalyst, in my opinion, as at this time the loans under the credit facility will come due. The amount of free cash flow that QRTEA generates in 2024 and 2025 will determine whether or not they can meet this repayment. If the company fails to generate any free cash flow during that period and the 2023 worst-case occurs, for example, then QRTEA will be facing an insurmountable $1.8b liquidity gap and almost certainly end up in bankruptcy. If Project Athens is a rousing success and QRTEA gets back to $650mm in average annual free cash flow starting in 2024, then they would be able to cover the credit facility loan repayments (barely). Of course, if QRTEA is back to generating that kind of free cash flow then it would likely be able to renegotiate or extend the credit facility and not be facing a liquidity crunch in the first place.

End of period liquidity (worst case): -$1.8b, (bankrupt)

Will Qurate Retail Eventually Go Bankrupt?

Even if QRTEA can survive through 2026, it isn't a given that they can survive indefinitely. Between 2027 and 2031, QRTEA will have another $3.9b of debt repayments come due, between their various notes and the redemption of their preferred shares (QRTEP). This works out to an average of almost $800mm per year that QRTEA will need to cover with free cash flow. From 2011 thru 2021, the company averaged $1b in annual free cash flow, so it is certainly possible that QRTEA can cover these obligations if things return to a pre-pandemic "normal." However, recent performance suggests that getting back to that level of free cash flow will be difficult. Even management's optimistic projections for Project Athens top out at about $600mm in free cash flow; if QRTEA averages $600mm in annual free cash flow, starting in 2024, then the company will still run out of cash by 2031 (unless debt is restructured at some point).

Investment Implications

So, what is the investor takeaway? For fixed-income investors, I think the risk/reward ratio is quite favorable for any debt with a maturity prior to 2026. Nothing is certain in investing, but I would expect liquidity to be available to cover those maturities. The picture is less clear for equity investors. If you told me for sure that QRTEA will go bankrupt in the future and will return no capital to investors in the interim, then it is hard to see the value in owning shares. You would be relying on investor sentiment to shift at some point and hope to sell your shares on a pop of optimism. On the other hand, if QRTEA can return to meaningful free cash flow and avoid bankruptcy, then the potential upside in the equity is immense. QRTEA shares traded hands at $7/share as recently as January of 2022 and would be a multibagger many times over if the market shifts from extreme pessimism to extreme optimism. The most compelling investment thesis for the equity, in my opinion, is that investors are overly pessimistic about the short term; taking a contrarian position to the market can pay off in a big way if your variant perception turns out to be right. The story here really hasn't changed much in the last year; QRTEA is either going to be a zero or a substantial multibagger over the next 5-10 years.

Risks

There is a lot of risk to both a bullish and bearish investment in QRTEA at these levels. For those long the stock, the risk of bankruptcy over the next 5-10 years is high, even in a scenario where Project Athens is moderately successful. For those short the stock, I don't see bankruptcy as a likely outcome in the next 2-3 years, which exposes bears to the risk of short-term pops on any good news that is announced during that time frame.

Conclusion

I find the current situation at QRTEA fascinating, though I don't see that it lends itself to an obvious investment thesis. I think the risk/reward ratio favors the bulls, especially in the short term, but the risk of long-term ruin is unacceptably high for me. I have a very small, speculative position in QRTEA, but in the spirit of "no called strikes" in investing I don't see this becoming a meaningfully sized holding in my portfolio unless circumstances dramatically change.

For further details see:

Qurate Retail Isn't Going Bankrupt. Yet