QRTEP - Qurate Retail: Project Athens Is Not Enough

2023-03-31 08:45:00 ET

Summary

- Qurate Retail, which owns QVC and HSN, has a loyal customer base and benefits from an asset-light business model but also has significant leverage and operational challenges.

- The stock price has plummeted 95% since becoming an asset-backed stock in 2018, and the market has priced it for bankruptcy.

- The company's turnaround plan, Project Athens, faces significant execution risks and debt servicing issues, which makes it risky for equity holders.

Qurate Retail ( QRTEA ) is a John Malone-backed Holdco that owns prominent legacy video and online streaming commerce brands such as QVC and HSN. It also owns assets, including Cornerstone Brands ((CBI)), Zulily, and other minor cost and equity method stakes. The company serves 13.2 million unique customers across its legacy network business and produced $12.1B in annual sales.

The retail stock was converted from a Liberty Media tracking stock to an asset-backed stock in 2018. The value has since plummeted by 95% to a mere 95 cents. This out-of-favor security piqued my interest due to its severely depressed price, its surprisingly loyal core-customer base, a long history of generating cash, massive leverage ($8.5B TEV vs. $360 million market cap) with spread-out maturities , and potentially transient operational issues particularly impacted by the Rocky Mount fire along with associated significant non-recurring expenses. Trading at 1/3 of 2021 FCF, my thinking was that if the company's earnings can return to a normalized level even after accounting for some attrition from a slowly dying business, the equity could re-rate to a multiple as low as 3-5x FCF, or I could receive sweet dividend payouts worth more than the market cap, leading to a sweet multi-bagger.

Sounds great, doesn't it!?

The primary issue with Qurate's turnaround plan, named Project Athens, is its dependence on management's ability to execute flawlessly while dealing with significant leverage. For the program to be successful, customer counts and ARPUs will need to stabilize over multiple years, margins must return to at least their pre-2022 levels, and working capital needs to be managed impeccably. If one or more of these conditions are not satisfied, cash will not likely be available for equity holders. I believe that the market is correct to price the stock for bankruptcy in the not-too-distant future. There is just too much risk of a permanent risk of capital and thus no margin of safety. I recommend that investors avoid this value trap unless it constitutes a negligible portion of their portfolio. However, there may be other opportunities available within its complex capital structure, such as the 2024 or 2025 senior secured bonds , for those interested in distressed debt situations.

How is QVC/HSN still around!?

As a proud millennial, I had no idea that QVC generated billions of dollars in revenue, let alone still around as a viable business before the stock appeared on my radar. To my surprise, the QVC and HSN brands are still relatively thriving, and together they form the Qurate Retail Group, which happens to be the most significant player in video and online streaming commerce in North America. After digging further, I discovered that QVC's resilience is attributed to two durable competitive advantages.

Q4 2022 Investor Deck (QRTEA IR)

{kind=link}

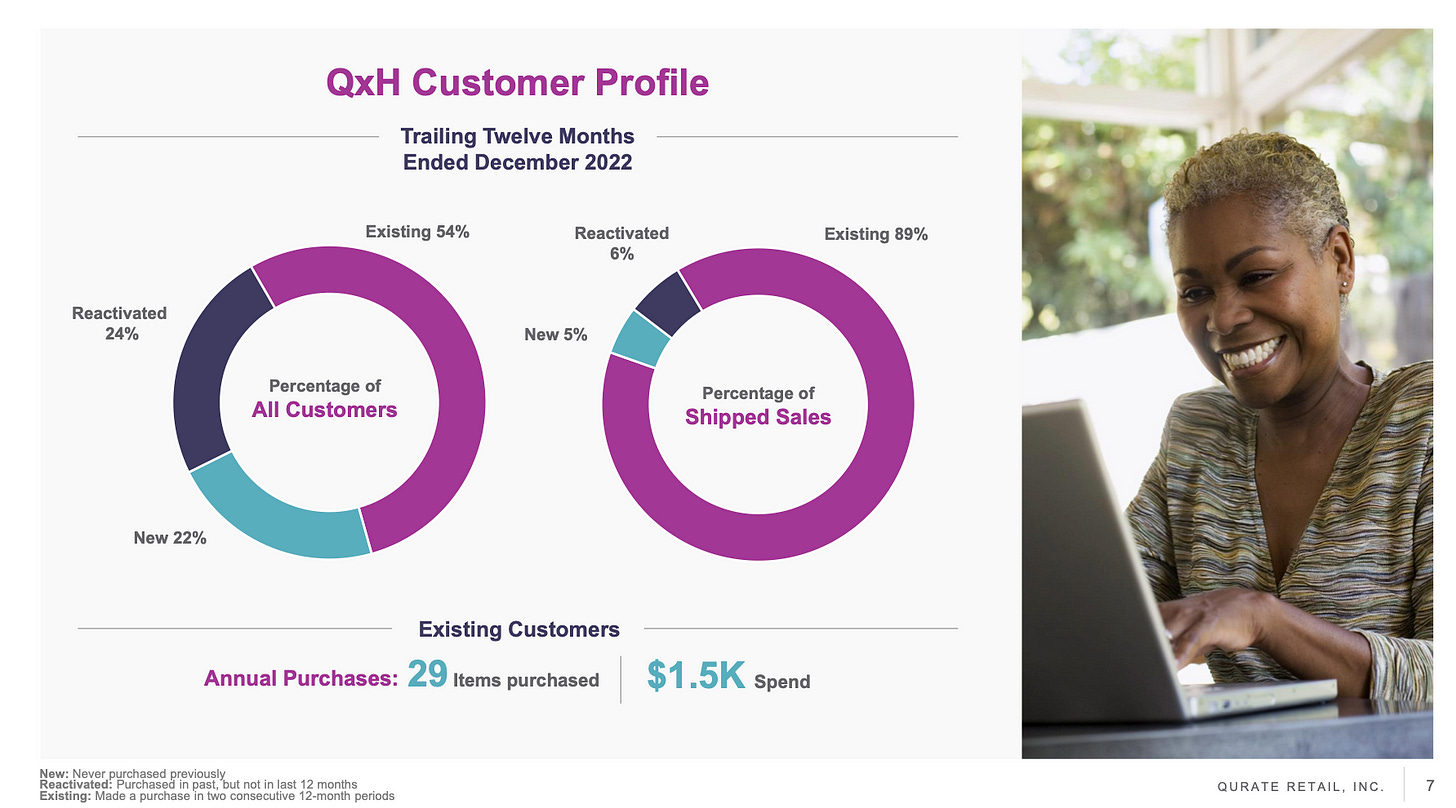

The first is a strong brand moat that it has cultivated within a specific demographic segment. QVC and HSN have a dedicated cohort of long-standing customers who have demonstrated unwavering loyalty to the brand over time. Approximately half of the existing 8.8 million QxH (QVC US) customers in the United States, who spend an average of $1.5k per year, account for around 90% of the sales. Moreover, an even smaller subset of customers, comprising 1.8 million super users, representing a mere 17% of the customer base, is responsible for approximately 70% of the revenue generated by QxH. Qurate cultivated this loyalty through its tv personalities, who have cultivated deep connections and trust with audiences. These viewers are typically women between the ages of 35 and 65 with considerable discretionary spending power. This buyer concentration makes the business a money printer when customers are satisfied. However, it can also be a double-edged sword, as any misstep by the company could unravel its operating leverage in a hurry.

The second advantage is the low-cost nature of its massive operational scale, eliminating the need to maintain a physical store presence (aside from CBI). This business model reduces expensive capital expenditures that competitors may have to invest in operating a large-scale physical store footprint. This feature allows the company to manage inventory levels at its centralized warehouses efficiently. It also allows for more flexibility as it can respond quickly to changing trends and demands by adjusting programming schedules and product mix. This characteristic alone doesn't confer a distinctive edge since e-commerce companies possess comparable asset-light characteristics. However, when combined with brand power, it creates a powerful synergy that results in strong returns on tangible capital (ROTC). Qurate Retail Group, for instance, achieved ROTC levels of over 60% before 2022.

Qurate's Post-COVID Hangover

Throughout 2020, Qurate's enterprise thrived due to consumer behavior, driven by pandemic-induced restrictions, which resulted in a heightened attraction to the platform. This translated to notable year-over-year revenue growth of 5.3%, a substantial improvement from the previous year's negative 4.3%. Furthermore, cash flow performance was even more impressive, surging by over 100% to reach a staggering $2.2 billion, after growth stalled the year prior.

However, fortunes started to change for the worst in 2021 as costs skyrocketed and substantial operational efficiencies plagued the business. According to CEO David Rawlinson, the supply chain and distribution system proved to be expensive and fragile when compared to those of competitors, and management faced challenges in handling it. For example, cancellations of scheduled trans-pacific vessels and delays at US ports of up to 45 days led to significantly delayed receipts of purchase orders. Additionally, the tragic fire at Rocky Mount, the company's second-largest fulfillment center, further exacerbated the operational inefficiencies, resulting in significant setbacks.

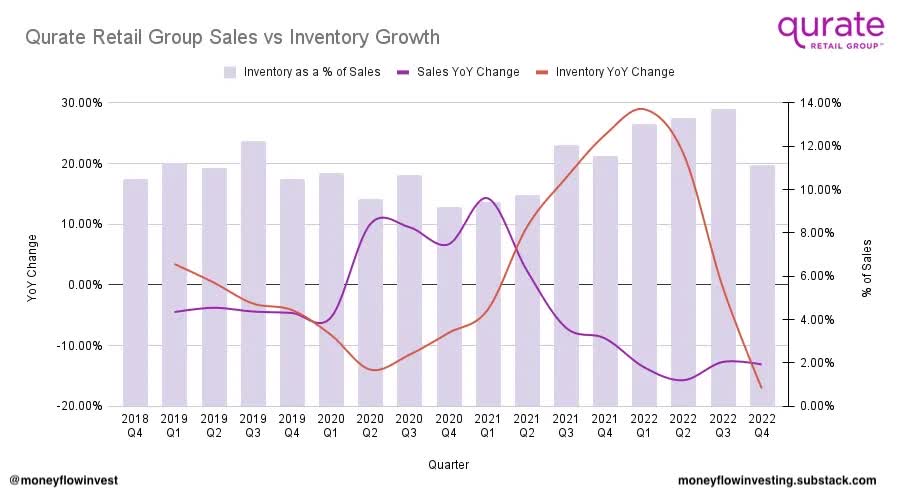

Qurate Retail Quarterly Sales Growth vs. Inventory Growth (10-Ks/Author)

{kind=link}

The effect was an inflection point for inventory levels in Q2 2021 as the supply chain eased, and previously delayed purchase orders were finally coming through just as demand cratered. Consequently, costs were out of control, and inventory as a % of sales rocketed from 9.73% to a Q3 2022 peak of 13.74%. Qurate experienced a significant setback with the loss of its Rocky Mount facility, which constituted a loss of between 20-30% of its most effective inventory storage and processing capacity. This, in turn, resulted in additional costs such as detention and demurrage, further exacerbating the financial implications of the warehouse's closure. As a result, the company had to resort to leasing approximately 1,000 trailers to manage the excess inventory. Moreover, the emergence of inflationary headwinds caused a surge in expenses, including transportation and freight costs, as well as labor wage hikes stemming from labor shortages. Collectively, these developments compounded Qurate's financial challenges, adding to the complexity of the situation.

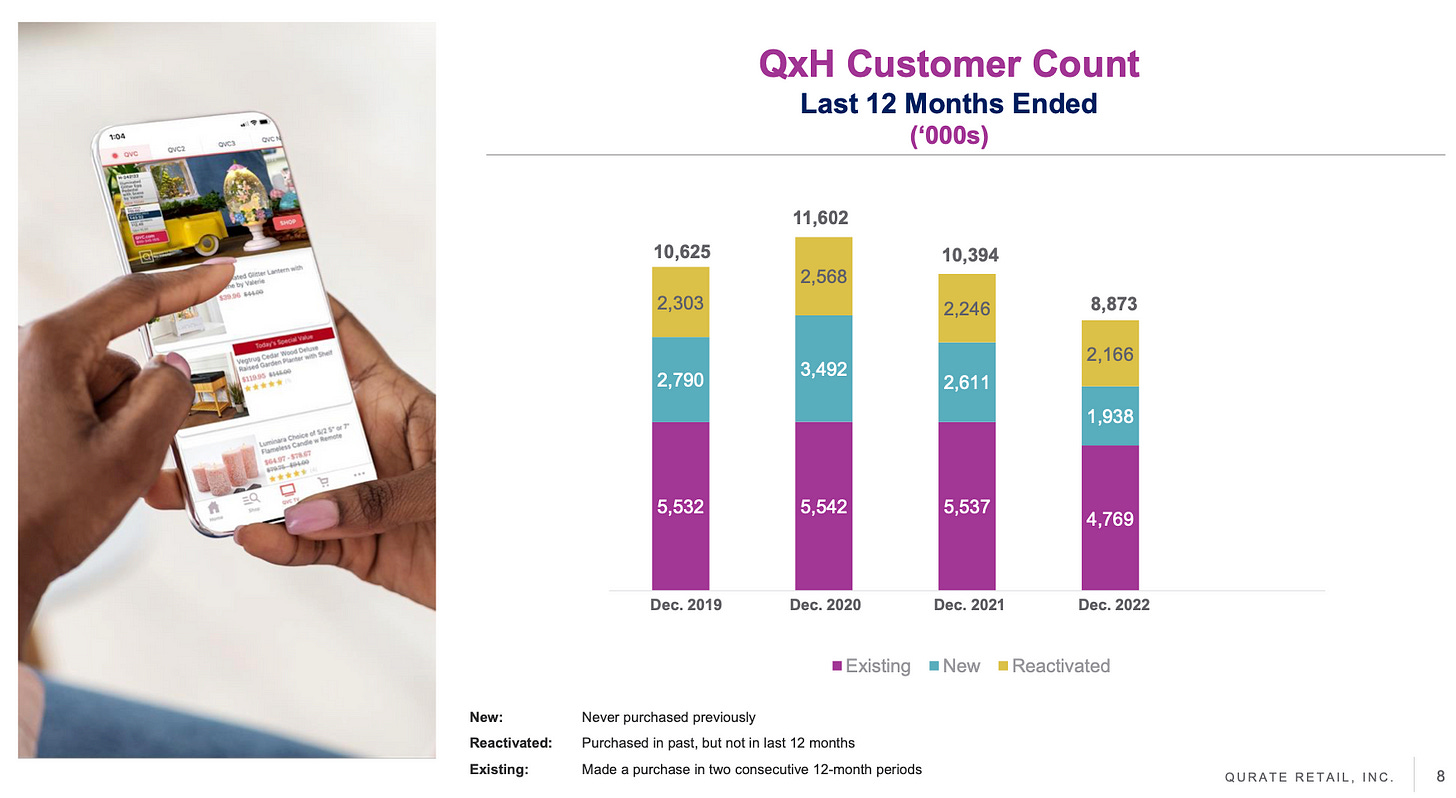

While Qurate battled these fires (quite literally), customer counts suffered tremendously. There are a few reasons for this. First, the secular decline brought about by cord-cutting further accelerated during the pandemic and continues today. The number of paying households declined by 27% from 2018 to 2022. Second, fickle shoppers, who had little attachment to the brand and were flush with cash from stimulus checks and limited options to spend the money during COVID, left.

Q4 2022 Investor Deck (QRTEA IR)

{kind=link}

Furthermore, a portion of its loyal customer base churned. Poor operational execution against a deteriorating macroeconomic backdrop led to pervasive customer experience issues that eroded trust. For example, the inventory disruptions greatly impacted Today's Special Value (TSV) deals, which are the focus of customer engagement and typically account for 20-25% of sales . At one point, 3/4ths of the planned TSVs were shifted to adjust for lack of product availability. Management also acknowledged that a lack of discipline caused customer pricing confusion. The multiple pricing tier structure it had between TSVs and other sales campaigns ultimately eroded the customer value perception of the TSVs. Eventually, QxH customer count fell 23.5% from the covid peak in 2020 and 16.5% from 2019, a stable pre-covid baseline year.

Project Athens: Is it Enough to Revive the Stock?

5-Pillar Strategy for Project Athens (June 2022 Investor Day)

{kind=link}

During the June 2022 investor event, the CEO unveiled Project Athens, the company's multi-year 5-pillar turnaround strategy to re-establish revenue growth, margin expansion, and incremental cash flow generation. Its primary purpose is to reinforce discipline from the top down to reverse or mitigate the issues that eviscerated cash flow and investor confidence. The initiatives include intentionally reinvigorating customer relationships, alleviating pricing confusion, reducing direct and indirect costs, returning Zulily to profitability, sustaining CBI's momentum, and prudently investing in online streaming. Management believes there is an opportunity for an incremental $300-$600 million in Adjusted OIBDA and a $300-$500 million free cash flow run rate starting in 2024.

Some good progress has already been made that will improve margins and working capital. For example, inventory levels are down 27% from June 2022 and inventory as a % of sales is now only slightly above its 10.5% pre-Q2 2021 average. As a result, margins should improve as heavy discounting tapers off. Changes in accounts payables should be less of a headwind to cash flow for the next couple of years as the business worked off $450 million off the balance sheet last year including $150-$200 million in covid-era inventory purchases.

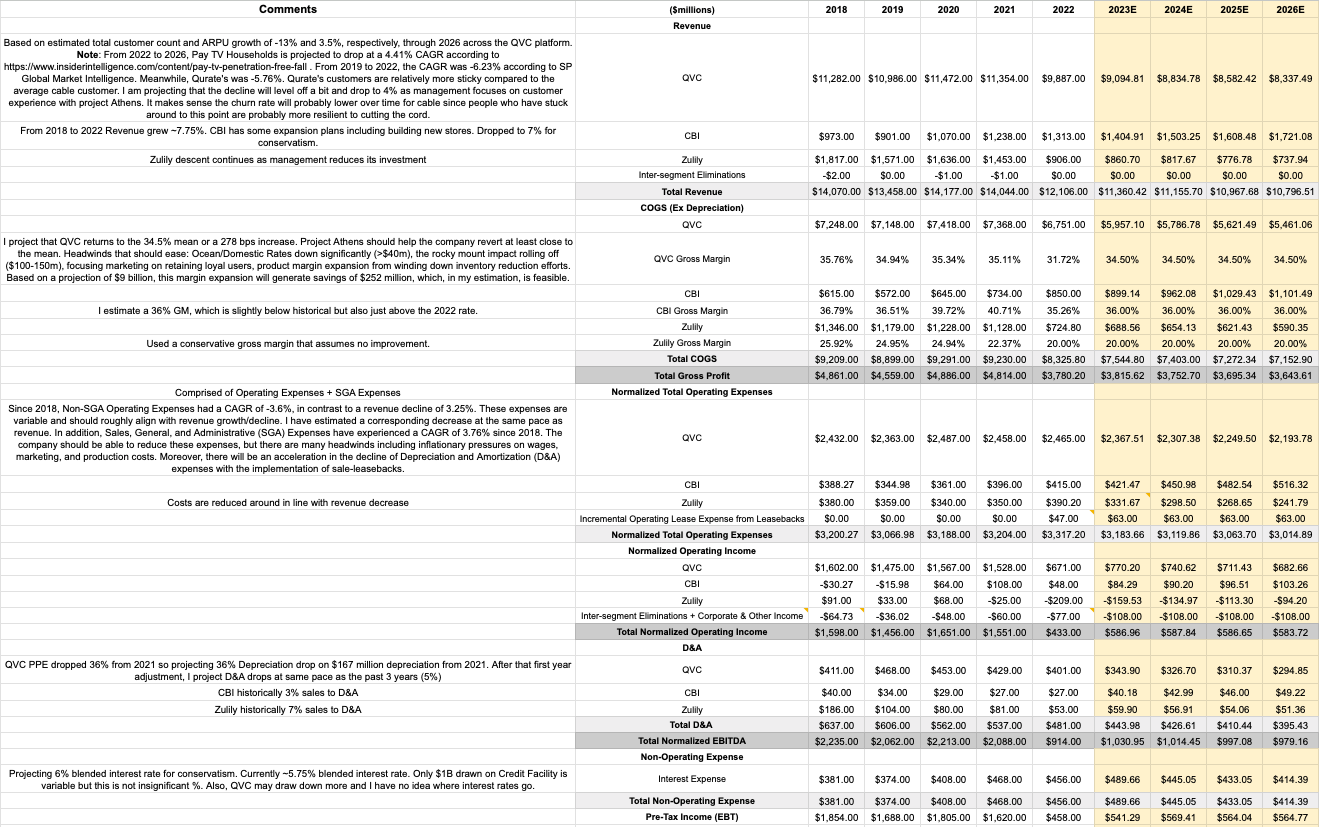

In my view, it is reasonable to believe that QVC's gross margin will roughly revert to the mean through Project Athens and the easing of macro conditions. Expanding the gross margin from a 5-year low of 31.72% to an average of 34.5% is a 2.78% difference or $252 million incremental cost savings on $9.094B in sales (see comments below). Operating expenses will also decrease but at a slower pace than revenue due to operating deleveraging.

QRTEA P/L Model through 2026 (Author/10-Ks)

{kind=link}

QRTEA Cash Flow Model through 2026 (Author/10-Ks)

{kind=link}

Despite the improvements from Project Athens, there is not enough margin of safety for an equity holder to sleep well at night and be assured the equity won't go to 0. Before 2021, the annual interest payments of $460-480 million were tolerable, given that the business consistently generated an unlevered free cash flow of $1.2-$2 billion. From my perspective, Qurate's unlevered future earnings potential is weakened to under $700 million due to a reduced customer base, margin reduction from operating deleveraging, Zulily's cash-sucking business further deteriorating, an additional ~$60 million in operating lease payments resulting from sale-leasebacks, and ongoing inflationary costs.

The business carries a debt burden of $8.1 billion, with a blended interest rate of ~5.75%, including $1.2 billion in 8% preferred stock and $6.9 billion in higher-ranking debt securities, of which $2.5 billion will mature by 2026. With ~$1.2 billion in excess cash and ~$700 million in cumulative free cash flows through 2026, management could allocate the entire $1.9 billion from cash flows to repay bondholders. In this scenario, management should be capable of addressing at least some of the $600 million gap with some financial maneuvering, such as liquidating more PPE through additional sale-leasebacks or selling stakes in its businesses. It could also extend maturities or roll over debt, especially if the leverage ratio improves and creditors have more confidence. However, as an investor whose priority is to avoid permanent capital loss, I am not willing to rely on the credit market as a white knight to provide liquidity.

Ultimately, there are three primary concerns for shareholders. Firstly, all cash flows are directed toward bondholders and not equity holders. Even though Project Athens is anticipated to enhance the business's financial standing, the immense debt burden implies that virtually all cash flows will continue to be paid to creditors. Secondly, even if Qurate stays afloat over the next four years, the outlook beyond 2026 is notably worse, given the business's declining cash flows and substantial debt and tax liabilities of $4.7 billion through 2030 (which should be slightly offset by at least $400-$500 million in DTAs). Lastly, success is largely predicated on management's capacity to execute their strategies with exceptional precision and for exogenous factors not to become setbacks as they did in 2022. If one or more variables, including an unexpectedly high rate of customer attrition, a failure to restore gross margins to the historical mean, a slower-than-anticipated decline in operating expenses, or suboptimal management of working capital, deteriorate beyond expectations, cash flows and therefore the ability to pay back debts or maintain covenants successfully will be adversely impacted.

Radio Silence from Insiders

Qurate Retail Insider Purchases (openinsider.com)

{kind=link}

At the end of the day, if insiders had confidence that this was a home run deal, you would think insiders would be doing everything they could to buy up shares. The reality is that there have been 0 open market purchases. The only sign of optimism is that Malone elected to exchange all of his B shares for A shares at $14 instead of receiving cash in 2021. However, I would take this with a grain of salt since it is plausible that this was simply another of his tax-saving strategies, which he is famously known for , to avoid capital gains taxes.

How Qurate can Prolong its Lifespan

The executive team could make some decisive capital allocation moves to shore up Qurate's financials, decrease its leverage, and extend its lifespan. First, it can shut down and liquidate the unprofitable Zulily. This will improve operating earnings by $100 to $200 million annually. Even if management can get the business back to break even in such a fiercely competitive market, it is still diverting valuable attention away from its struggling core business. Finding an acquirer or selling off some of Zulily's assets would be a bonus. Secondly, it could sell off the valuable CBI assets and instantly pay off a portion of its high-interest debt. If a buyer is willing to pay a multiple of 7-9x CBI's operating earnings power, which I estimate is roughly $100 million, the company's capitalized value could range from $700 million to $900 million. Then, it could tender the 8% preferreds or redeem the remaining $792 million 8%+ yielding LI LLC Senior Debentures and offset most of the lost earnings.

Conclusion

Qurate Retail Group's stock may appear to value investors to be a tempting investment opportunity given its anemic valuation, recent non-recurring costs, loyal customer base, and long history of generating cash. The company's operational scale and resilient tv streaming business model have enabled it to thrive for decades. However, the company's high leverage and dependence on management's flawless execution of the Project Athens turnaround plan make the equity risky. I agree with Kingdom Capital's assessment to focus on the high-yielding bonds rather than the stock, especially if yields continue to grow.

For further details see:

Qurate Retail: Project Athens Is Not Enough