QRTEB - Qurate Retail: Struggling Business With Tough Times Ahead

2023-03-08 10:41:03 ET

Summary

- Qurate Retail, Inc. is a company that operates in the video and online commerce space.

- The company has loyal customers but has seen diminishing relevancy as e-commerce has grown and T.V. declines.

- Economic conditions pose short-term headwinds as demand for retail is declining.

- The company's financial profile has declined substantially in the last few years, with profitability no longer attractive.

- With heightened solvency risk and no feasible turnaround in sight, we rate Qurate stock a sell.

Company description

Qurate Retail, Inc. ( QRTEA ) is a company that operates in the video and online commerce space across North America, Europe, and Asia. They primarily sell consumer products through T.V. shopping programs, mobile, and online. Its brands offer a wide variety of products, such as apparel, home goods, and beauty products.

Qurate Retail's portfolio of brands includes QVC, HSN, zulily, Frontgate, Garnet Hill, and Ballard Designs, among others.

Share price

Qurate's share price has achieved a monumental decline in the last decade, with the company peaking at a c.$30 share price before declining to below $2. This has been driven by weakening financial performance and the company's struggle with remaining relevant in the modern day. Our objective is to assess if the company has any hope for a renaissance or if it will quietly decline to obscurity in the coming years.

Death of TV

Cutting straight to the point, the biggest headwind the company faces is the death of the traditional cable television service. Qurate reaches hundreds of millions of people through TV packages yet the number is declining quickly as consumers increasingly consume online content and utilize streaming services. Further, this has contributed to changing trends in the way TV is consumed, with less "browsing" TV channels but rather browsing shows/movies. This will contribute to declining traffic to Qurate's channels, with this only increasing as the amount of tech-savvy individuals grows. Our view is that this is an irreversible trend which will only diminish the number of new customers it can reach.

Products offered

One of the fundamental issues with the company outside of macro/industry factors is its product offering. The company's offering, beyond a select few brands, is dire compared to current industry trends and tastes.

{kind=link}

Notable brands (Qurate)

This is problematic for many reasons but the biggest being is that consumers are not going to find their website when searching for products they are looking for. The biggest attraction for a retailer is its products, even before price. If Best Buy ( BBY ) didn't sell LG or Samsung TVs, it would have no hope of competing against any of the companies in its industry.

E-commerce shift

The retail industry has seen a major shift in the last decade with customers increasingly choosing to shop online. The COVID-19 pandemic has accelerated this trend, with more consumers realizing the convenience benefits that come with e-commerce. Qurate response to the e-commerce trend was to develop its online presence, primarily through QxH, which has allowed the company to modernize. The problem with this is that consumers who shop online are very different from their core audience. Although many of their core customers use their website, growth in this segment has not been at the level required because the wider public does not see the value they provide above and beyond the current retail offering. The nature of e-commerce creates transparency, with consumers able to shop for the best prices, brands/products, delivery dates, and added benefits. This goes against how the T.V. sales channel operates, where it's more about traditional sales tactics. E-commerce puts the power in the hands of consumers.

In terms of competition, Qurate faces significant challenges from established e-commerce giants such as Amazon ( AMZN ), as well as more specialist retailers such as Etsy (ETSY). These companies have significant resources and technological capabilities, which differentiate their products beyond just price, allowing them to carve out market share. Qurate's brands just do not have anything compelling about them, making it incredibly difficult to re-invigorate growth.

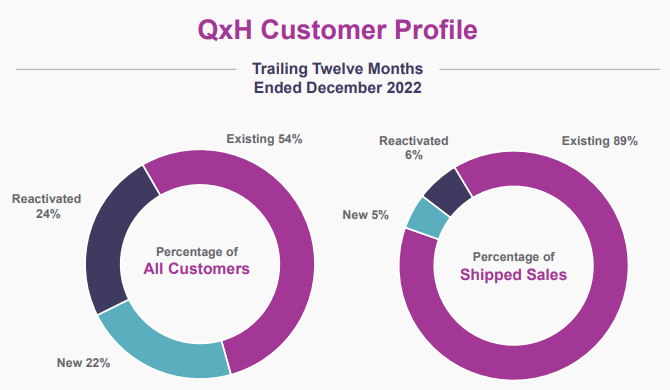

Customer profile

QxH's customer data supports the developing view of the business we have. The company's core segment is its existing customers, with little in the way of new customers or returning customers following a past purchase.

{kind=link}

Customer profile (Qurate Retail)

The company is seriously struggling to attract new customers, while its current customer base continues to dwindle. Our view is that this can only accelerate further over time. As with an increasing number of their core base moving to their e-commerce offering, there is a greater chance that they will see less value and start comparing them to other retailers.

Customer count (Qurate Retail)

Economic conditions

We are currently experiencing heightened inflation as supply-side issues wreak economic havoc. Interest rates have been raised in response but inflation is showing itself to be stubborn, suggesting current conditions will continue at least until the end of the year.

This is an issue as consumers are seeing their discretionary income shrink, with the cost of living rising to unsustainable levels. As a result of this, consumers are looking to cut back spending where possible, in order to ease their financial distress. Even those who are more financially comfortable will inevitably defer some unnecessary spending due to concerns about the economic outlook. During such times, many fear unemployment or an extended period of economic weakening. Interest rates have compounded the issue as it impacts almost everyone, be it due to credit cards, mortgages, or rent increases (in response to rising mortgages). For this reason, it is likely Qurate will face a tough 2023, with demand continuing to trend down. Analysts are forecasting a 7% decline in sales and an 80% decline in EBT ( Source: Tikr Terminal ).

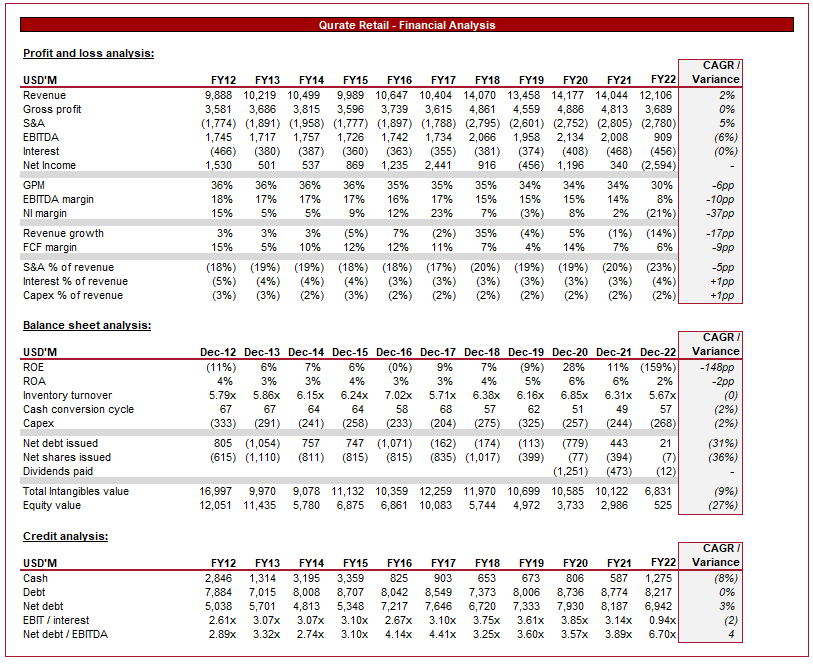

Financials

{kind=link}

Qurate Financials (TIkr Terminal)

Presented above is Qurate's financial performance for the last decade.

Qurate experienced a 2% revenue growth rate across this period, driven by the company's transition to e-commerce, which now constitutes 62% of total revenue. Although the growth rate comes out at 2%, the company has experienced substantial volatility Y/Y, unable to achieve stability. In the most recent quarter, the company saw revenues decline 13%, with macro conditions biting. Despite this, most retailers have not seen such a sharp decline, suggesting the company is more greatly exposed to changing demand.

Gross profits have performed worse, with margins consistently declining from 36% to 30%. The recent decline has been driven by rising costs attributable to inflation, with the company unable to pass on inflationary increases to customers. This is not usual given the level of competition in the industry. It is likely that the company has been discounting products at increasing rates throughout the period, also contributing to this.

Things continue to get worse, with S&A expenses increasing at a surprising rate of 5%. This has occurred as the company has maintained its investment in marketing, distribution, and customer service. Qurate has already undertaken a headcount reduction exercise but this may not be enough to move the needle. We can understand why the company continues to maintain these cost levels as it was able to achieve a 15-20% EBITDA margin historically.

The company has a lot of noise below EBITDA, including cash received from an S&LB transaction, impairment of goodwill, restructuring charges, and costs incurred due to a fire at a distribution facility.

This leaves the company's profitability profile at an unhealthy level, with its EBITDA margin declining to 8% and its FCF margin to 6%.

Moving onto the balance sheet, the company is seeing its operational cash position deteriorate. Inventory turnover has declined and CCC has increased. This suggests inventory is becoming harder to sell, even after the company has chosen to reduce its inventory levels. This could contribute to greater discounts in 2023 as the company seeks to liquidate inventory.

The company's net debt position has trended up in the last few years as the company has found itself facing problem after problem post-COVID. In Management's defense, it is not like they could have foreseen a fire or inflationary conditions. Despite this, the company has distributed far too much cash in the past and is now paying the price. Qurate's interest coverage has fallen to 0.94x with a ND/EBITDA ratio of 6.7x. This leads to questions about liquidity and solvency. The good news is the company continues to generate cash from operations at a healthy level. With things weakening in FY23, the company will likely generate in the region of $500-750M in FCF. This gives the company firepower in the region of $1.5-2BN, with consistent debt repayments and interest due in the coming years. For this reason, we do not see default in the next year or two but the company will likely refi at rates that will put the final nail in Qurate's coffin. Fitch currently assigns a BB- rating to the stock but this was prior to the most recent decline in financial security.

Valuation

Qurate valuation (Tikr Terminal)

Qurate is currently trading at a very low valuation, with markets pricing in financial distress and a continued decline. This is far below the industry average, with Seeking Alpha's quant rating the stock's valuation a B+.

Seeking Alpha's rating (Seeking Alpha)

This presents an opportunity for speculators in both directions, who are banking on price action . In our view, the valuation is a reflection of both the company's current performance and its dire outlook, not suggesting any long-term opportunity for alpha on a risk-adjusted basis.

Final thoughts

Qurate is a technologically inferior business that has been eaten alive following a change in consumer spending habits. The company has a loyal customer base that will continue to shop but this number is dwindling, with new customers not even replacing those leaving. The company does not inherently offer anything unique, which makes the long-term difficult. With short-term headwinds ahead, we can see the company facing a tough 12 months as it navigates financial distress. We rate this stock a sell.

For further details see:

Qurate Retail: Struggling Business With Tough Times Ahead