RCM - R1 RCM: Cloudmed Already Paying Dividends Look For Double-Digit Growth In FY23

Summary

- The Cloudmed integration appears to be already paying dividends for R1 RCM as a growth accelerator.

- Projections are for 48% YoY adj. EBITDA growth in FY23.

- The company looks undervalued at 12.75x forward EBITDA.

- I reiterate a buy rating, revising my price target higher to $20.

Investment summary

As we enter the final third of Q1 FY23, it's been pleasing to see a number of my broad healthcare longs catch a steady bid from initial coverage. R1 RCM Inc. ( RCM ) is one such name and has clipped a 29% return since my initial publication in December, titled " Reversal rally well-supported in the data ". Following the company's latest set of numbers , I'm remaining very constructive on this name, for several reasons. The firm's end-to-end ("E2E") solutions now embrace $55Bn in net patient revenue ("NPR") combined with >500 modular customers that see it grip $850Bn in NPR from 94% of the leading E2E systems in the U.S. The company's CEO debacle is now well sorted and new captain Lee Rivers has a good understanding of the business coming from the role of RCM President. Further, the company's Cloudmed acquisition has proved already to be a growth accelerator and has built RCM into a now $1.8Bn revenue company, forecasted to print ~$2.3Bn at the top-line this year, another c.30% in growth. Net-net, I reiterate RCM as a buy, revising the return objective to $20 in doing so. See the valuation and conclusion section at the end of this analysis for more on the methodology of obtaining this.

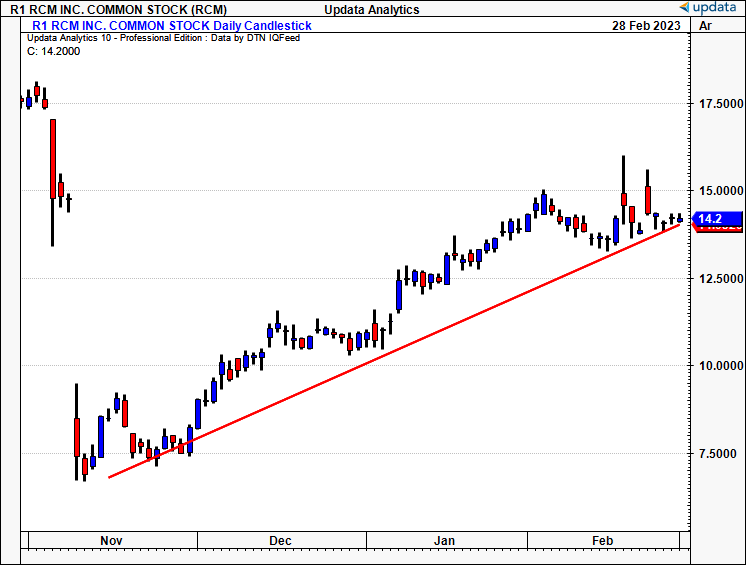

RCM Price Evolution Since Bottoming in November FY22

{kind=link}

Key factors to the RCM buy thesis

There are several upside factors that separate RCM from its broad health-tech peers within the current macro-milieu that is plaguing the global equity markets. In particular, I'd note the company's progress on its Cloudmed integration, following its acquisition in January last year (note: it actually closed the transaction in June). As a reminder, Cloudmed serves >400 of the largest health system across the U.S., notwithstanding its service to 47 of the top 50 hospitals in the country. It made the transaction in an all-scrip transaction of $4.1Bn. Management notes it has now consolidated the bulk of its corporate, HR, and finance systems within the Cloudmed system. Subsequently, it envisions $15-$30mm in cost synergies this year, accretive to ~500bps of additional adj. EBITDA growth for Q1. Further, it sees 500mm patient transactions with the Cloudmed integration and its E2E business combined. I'd note this is a strong probability, given the new integration now gives RCM access to patients all across the payer spectrum in each state. Further, it can boast a level of automation to scale this, and drive efficiencies. These are good numbers and, going by FY23 guidance listed a little later, I'd suggest is also a key performance driver for RCM heading into the years ahead.

Second, touching on the automation point, management is looking to continue on the automation front, which is a major standout in the company's value proposition by estimation. Given the labor costs and supply issues experienced by healthcare providers in FY22 that show no signs of normalizing in the near term, companies are looking to methods that mitigate these risks that erode operating margins. Further, investors are looking to the same, given the impact to earnings. With a push towards automation, there are two factors to consider, 1) that it makes operating processes reliable, repeatable, and accurate (i.e., automated), and 2) reduces the need for labor in the first place. Hence, my estimation is that RCM will continue pitching this as part of its Cloudmed and E2E expansion going forward, further insulating it from competitors on this front.

Data: RCM Investor Presentation, pp.3

{kind=link}

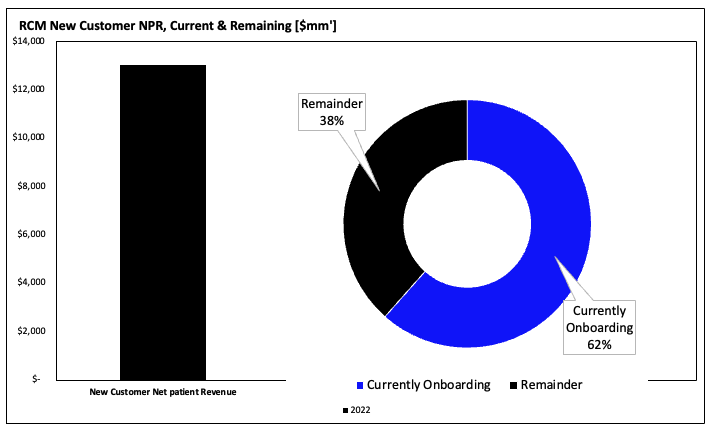

Third, RCM announced it obtained >$13Bn in NPR from new accounts, including the likes of Scion, St. Clair Health, and Sutter. Further expanding on this, I'd emphasize the additional 600 distinct modular bookings and 15 additional physician groups that were signed throughout the period. These are tremendous growth numbers in my opinion. Importantly, of the $13Bn in new NPR, it has already onboarded ~62% of this (Figure 1) and expects the remaining 38% to be onboarded over the coming 24 months. Hence, this will be a strong tailwind and catalyst to watch out for into next year.

Fig. (1)

Data: Author, using data from RCM 10-Q

{kind=link}

Now, switching to the numbers. There are multiple talking points for discussion here, and I'd note the following analytics from RCM's Q4 and FY22 performance:

- RCM booked quarterly top-line sales growth of 34% to $532.8mm on adj. EBITDA of $125mm, also up 31%. Looking to the FY22 result, revenue climbed 22.5% to $1.8Bn and the firm saw a 23.6% adj. EBITDA margin on this. Importantly, as mentioned above the Cloudmed integration was a major contributor to top-line growth, attributing ~24% and 14.4% to overall turnover in Q4 and FY22 respectively. As a measure of the acquisition's success, if we back these numbers out, growth in the core business was only 200bps and 500bps from Q4 FY21 and FY21 respectively. Hence, I'd reiterate once more that Cloudmed has been a major growth accelerator for the company.

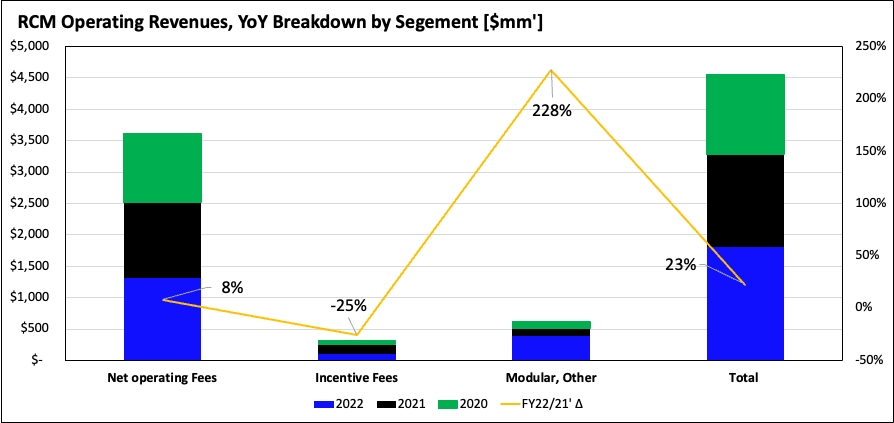

- Breaking down by segment (Figure 2), the major upside in Q4 came from the company's modular solution business with a c.230% YoY gain, once more thanks to the integration of Cloudmed. Separate to this, incentive fees were down 25% over the year to ~$26mm, whereas it saw ~400bps of expansion in net operating fees to $344mm. I'd note that momentum built substantially in net operating fees towards the back end of Q4 FY22, with a $12.4mm YoY growth, but $20mm growth in Q3.

- Moving down the P&L, it recognized a net loss of $64mm versus a profit of $127mm the year prior, given a $500mm increase in OpEx, tied principally to the acquisition and integration of Cloudmed. Hence, these are non-recurring, one-line items that I don't see continuing in FY23.

- With the integration of Cloudmed in place, coupled with the accelerated growth effect this has had, management now projects $2.33Bn in revenue for FY23, calling for another 29.4% growth at the top-line. On this, it forecasts $630mm in adj. EBITDA at the upper end of range, underscored by a 20% YoY growth route in Cloudmed contributions. Baked into this as well as the cost synergies listed earlier, which could be accretive to bottom-line growth into the coming periods.

Fig. (2)

Data: Author, data from RCM 10-K

{kind=link}

Valuation and conclusion

With the strong delivery in FY22, the market is now pricing RCM at a 12.75x forward EBITDA, below the industry's 13.4x multiple. I believe this is an unfair compression as management is calling for >48% growth in adj. EBITDA for this year, notwithstanding the Cloudmed accelerant discussed at lengths throughout this analysis. Last time, I mentioned that a 14.4x forward EBITDA multiple "represents a price target of $14.70" and, at the current momentum, RCM looks to take this figure out. Hence, looking to the industry's 13.4x multiple and assigning this to the midpoint of RCM's FY23 guidance of $612mm, this derives a price target of ~$20, otherwise 40% upside potential on the current market price at the time of writing. I'm therefore revising my target higher to $20 and searching for this next return objective.

Net-net, there are multiple mid-term growth catalysts that RCM has to look forward to in the coming 12-24 months. With the Cloudmed integration already paying dividends, I've revised my target higher to $20, and I am eyeing this number as the next return objective. A new CEO, plus 48% projected growth in adj. EBITDA for FY23 is additional support for this target. Reiterate buy.

For further details see:

R1 RCM: Cloudmed Already Paying Dividends, Look For Double-Digit Growth In FY23