RCM - R1 RCM: Progress Noted But At This Level Valuations Just Don't Make Sense (Rating Downgrade)

2023-11-25 01:52:50 ET

Summary

- R1 RCM Inc. has experienced a decline in its stock price due to a broad selloff in risk assets and weaker-than-expected quarterly numbers.

- The company's Q3 earnings showed a 15.5% increase in revenue and positive earnings, but the market is still pricing in a more difficult period of business.

- RCM's integration of AI and technological advancements could be catalysts for future growth, but the stock is exquisitely priced at 37x forward earnings.

Investment update

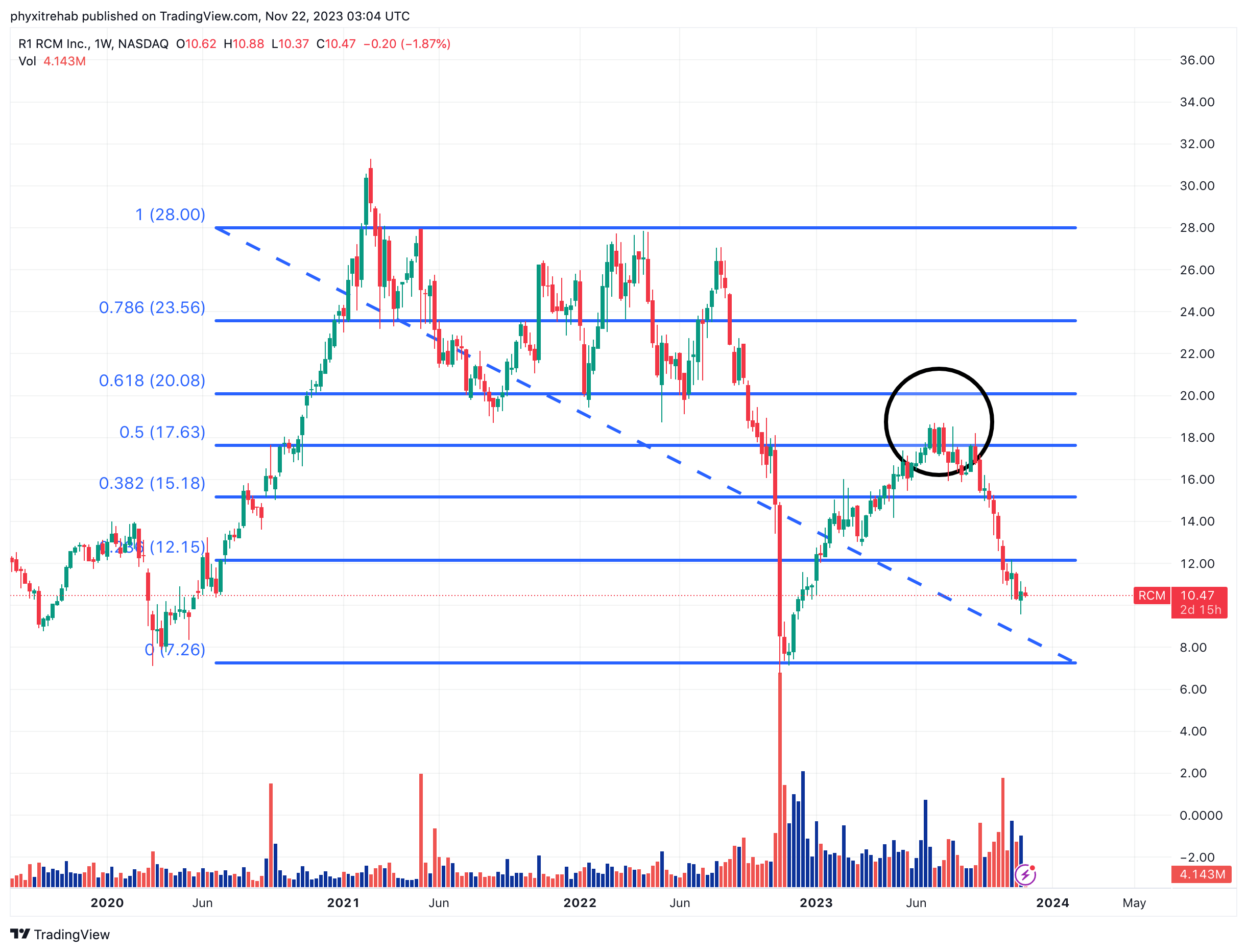

Almost a full year has passed since my initial recommendations to buy R1 RCM Inc. (RCM). The stock had rallied from ~$10.50 to >$17 in 7 or 8 months, before markets started to roll over from their October '22 rally.

Things were looking positive for the company until (1) a broad selloff in risk assets (equities + bonds), and (2) a weaker than expected set of Q2 numbers. Its latest filing for Q3 was a little stronger, but the investment outlooks seems to have pared back the shoots of growth.

We now find ourselves with the following investment facts pattern:

(i). Sound business model-proven product, adding value to customers in revenue cycle management ("RCM"). Business growth attests to market uptake of services.

(ii). In July, the stock retraced 50% of the August '23 dumping of its share price-a key technical area of support-but couldn't find buyers above this level (Figure 1).

(iii). Selling volume was instead immense out of this competition. The market is pricing in a more difficult period of business for the company. Most broad indices have caught a November rally, and have taken back this corresponding level. RCM hasn't found the buyers one would have hoped at the critical levels observed.

(iv). The company's Q3 2023 numbers were mixed but ahead of expectations.

(v). We still don't have the company's 10-Q (it has since been noticed by Nasdaq).

(vi). You are paying 37x forward earnings to buy RCM even within this broader downtrend, or 1.6x book value with negative 3.6% ROE.

It was Keynes who supposedly said that " When then facts change, I change my mind-what do you do sir?", well the investment facts have changed for RCM for the time being in my opinion. We now have a company priced to perfection but not exhibiting the economics to support this notion. At 37x forward earnings, I find it difficult to grow into this number. The market's reappraisal should not be ignored. In my judgement, there is scope for further downside. Net-net, revise to hold.

Before proceeding, I encourage you to read my last 4x coverage on RCM:

- Attractively Priced, Capital Produces $0.90/Share In Earnings (BUY)

- Value Proposition Is Only More Attractive Now (BUY)

- Cloudmed Already Paying Dividends, Look For Double-Digit Growth In FY23 (BUY)

- Reversal Rally Well Supported In The Data (BUY)

Figure 1.

{kind=link}

Q3 earnings insights

Snapshot of growth and financials-

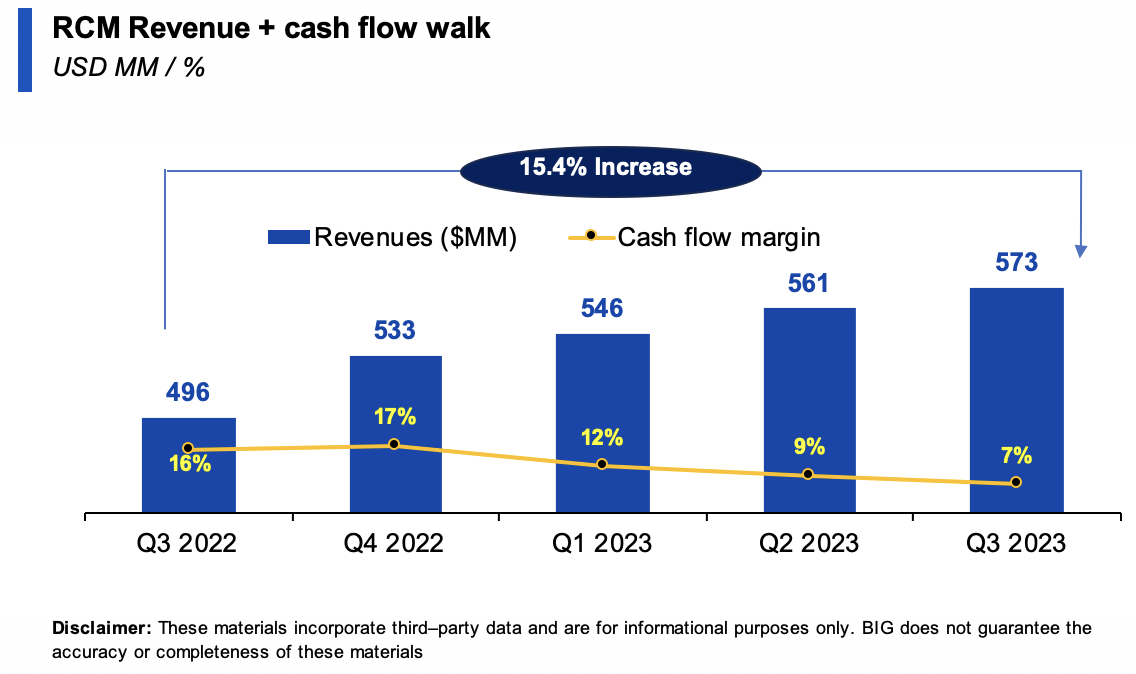

Observations: RCM put up a 15.5% upswing in revenue to book $572.8mm at the top line in Q3. Adj. EBITDA grew 30.2% YoY on this, tallying $161.5mm or 2x operating leverage. Critically, it put up earnings of $1.3mm in Q3, a positive turn from last year which can't be overlooked.

Gross margins, at 21.8%, were up 300bps and in-line with historical range. Expenses were $365mm on revenues and 14.7% on operating costs- the highest in 2 years for OpEx, but in-line for COGS. The operating profit on cost came to 28% for the quarter. Meanwhile, the percentage of operating cash flow backing revenues has peeled back to 12-month lows of 7% by the end of Q3.

Figure 2.

{kind=link}

Maintained FY'23 guidance-

Given the performance this YTD, management reiterated its 2023 guidance at the top and bottom lines. It expects the following:

-

Forecasts FY'23 top-line in the range of $2.25Bn-$2.275Bn (no change), up from $1.18Bn last year.

-

Down the P&L-to produce adj. EBITDA of $600mm-$615mm. With its Cloudmed integration, it is on track to hit $30mm in operating cost synergies by yearend.

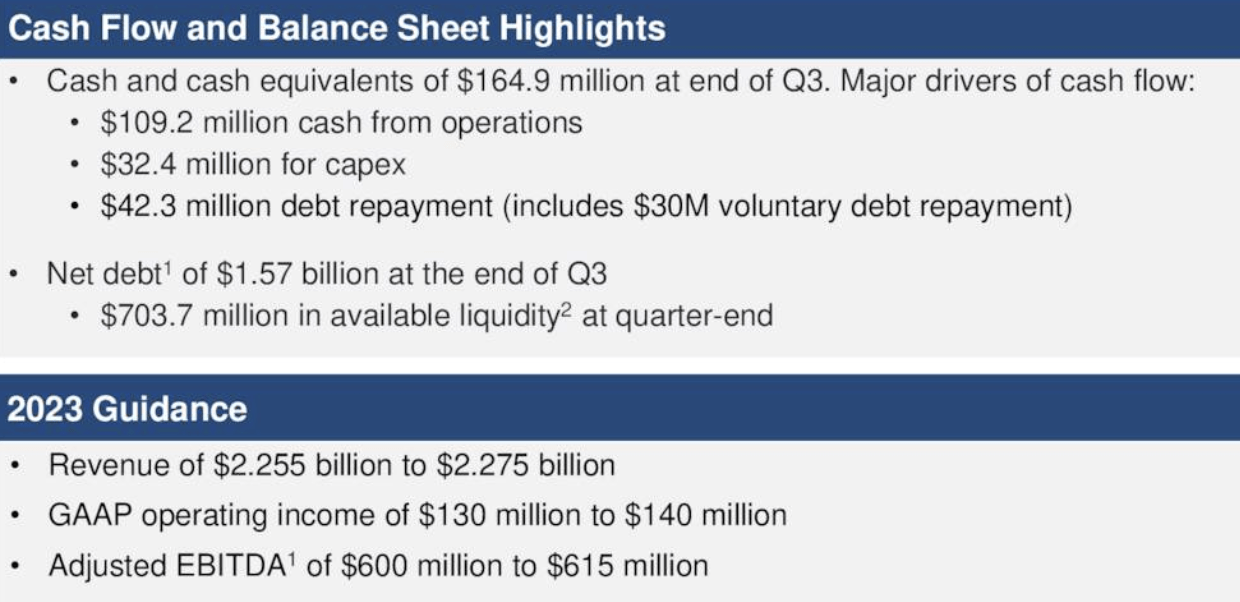

Cash accumulating, but ready to deploy-

There's been a buildup of cash on hand since 2021 ($165mm vs. $103mm 2 years ago). It invested $32mm to CapEx and $42mm to reducing its debt balance to $1.57Bn. It had $700mm of available liquidity end of the quarter.

The company has been happy to continue paying down its 5-7% notes, vs. get 5% or so on the cash in the money markets. As the CEO said on the call, " we're leaving ourselves some opportunity and flexibility with the cash balance, but certainly paying down debt is one of our priorities ".

It may be sitting back for an upcoming asset purchase as well, and may even be enjoying the fruits of its Cloudmed acquisition. Cloudmed contributed $174.7mm to Q3 sales. So 30.5% of the top line was diversified, on track to meet $30mm in annual cost synergies, as mentioned earlier.

Figure 3.

{kind=link}

Innovation and AI integration could be catalysts-

- Advanced technology utilization. R1's foray into its Large Language Model ("LLM") application is a shift towards technological advancement. For a firm whose assets are already tech-heavy, it could be a pivotal one as well. For example, the application can now automate quality assurance for 100% of its coding volume. Early trials show this resulted in better coding quality and more satisfied physicians (achieved within 4 months in first round). The productivity gains are immense as well. According to the CEO:

"Historically, our team manually coded approximately 50,000 physician charts per week and sampled around 5% of those to assess quality.

Now we were able to automatically compare our 50,000 manually coded charts to the automated code."

This is a tailwind of proportions so I would urge investors to keep a close eye on RCM's integration of AI, both to what usage it makes of it, and what innovations from it. -

Strategic Roadmap. In fact, the company's product roadmap encompasses generative AI use cases on RCM's books. It plans testing and deployment through 2023 and into 2024 for these. One thing that I've always noted above RCM is its continued investment to data assets for sustained competitive advantage. This is another clear example of this. Again, I would strongly urge investors to pay close attention to the company's AI domain, as there could be some exciting developments if done right.

Economic value for shareholders

The company's Q3 numbers illustrate it remains on track to deliver a reasonable period of business in '24, still below the market's projections from earlier this year.

The economics underneath the hood include the following:

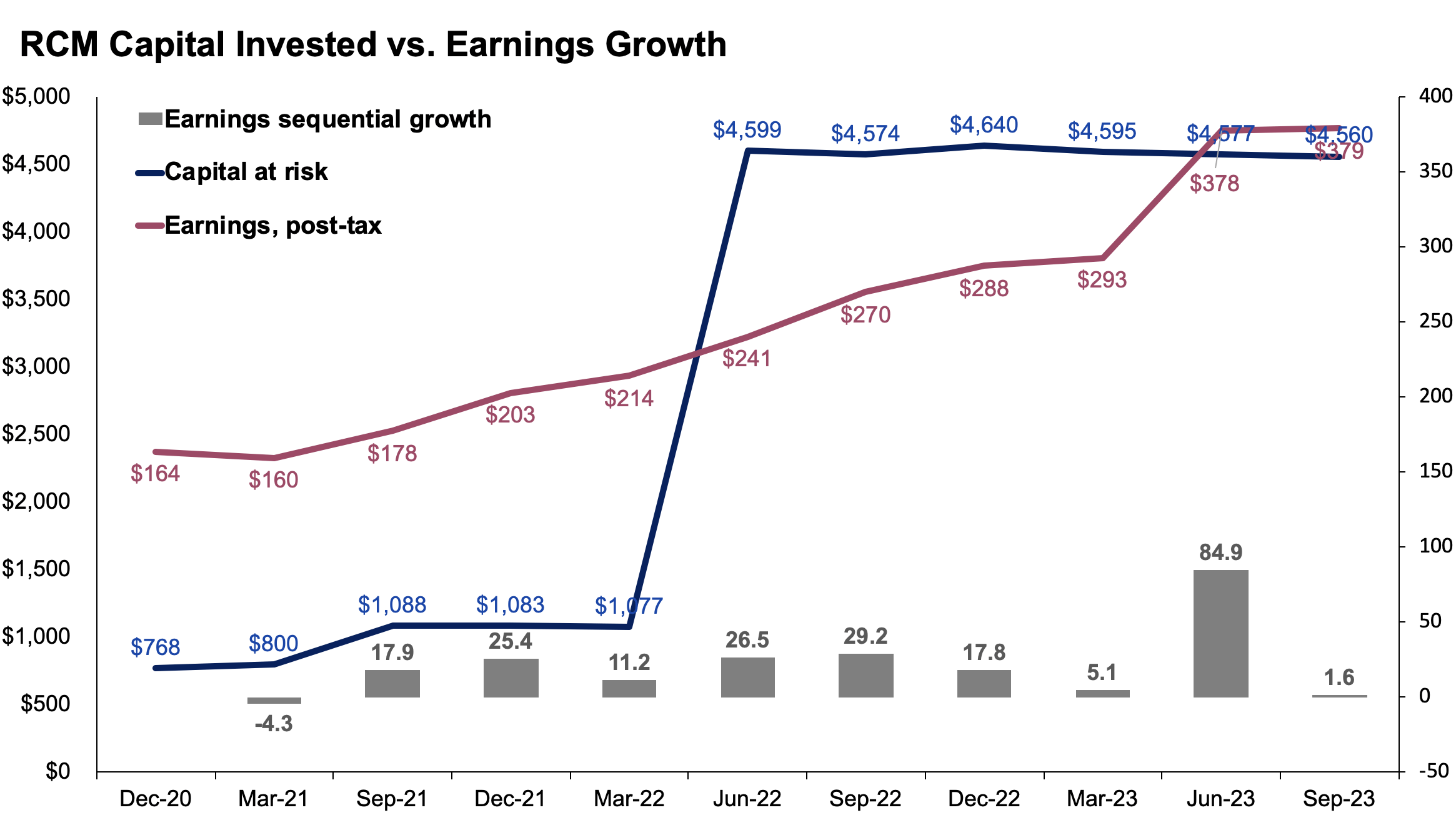

- The Cloudmed acquisition, completed at a $4Bn valuation, remains the company's largest investment over the last 3 years. This brought in $174mm in Q3 revenues on this ($696mm annualized). The balance sheet increased by c.$4Bn after the acquisition, so capital intensity is higher, from 1.7x capital turnover in 2020 to 0.5x last quarter.

- Critically, none of this capital budgeting has dented the trajectory of the company's earnings growth since 2021 (Figure 4). Earnings growth was highest in Q2 for the last 3 years (TTM values).

- From Q4 2021 to Q3 2023, the company invested $3.4Bn net in total, and grew earnings by $176mm in doing so (5.5% return on incremental capital).

- Since the acquisition was completed in Q2 '22, it has reduced assets by $39mm, but grown earnings for us by $139mm.

Figure 4.

{kind=link}

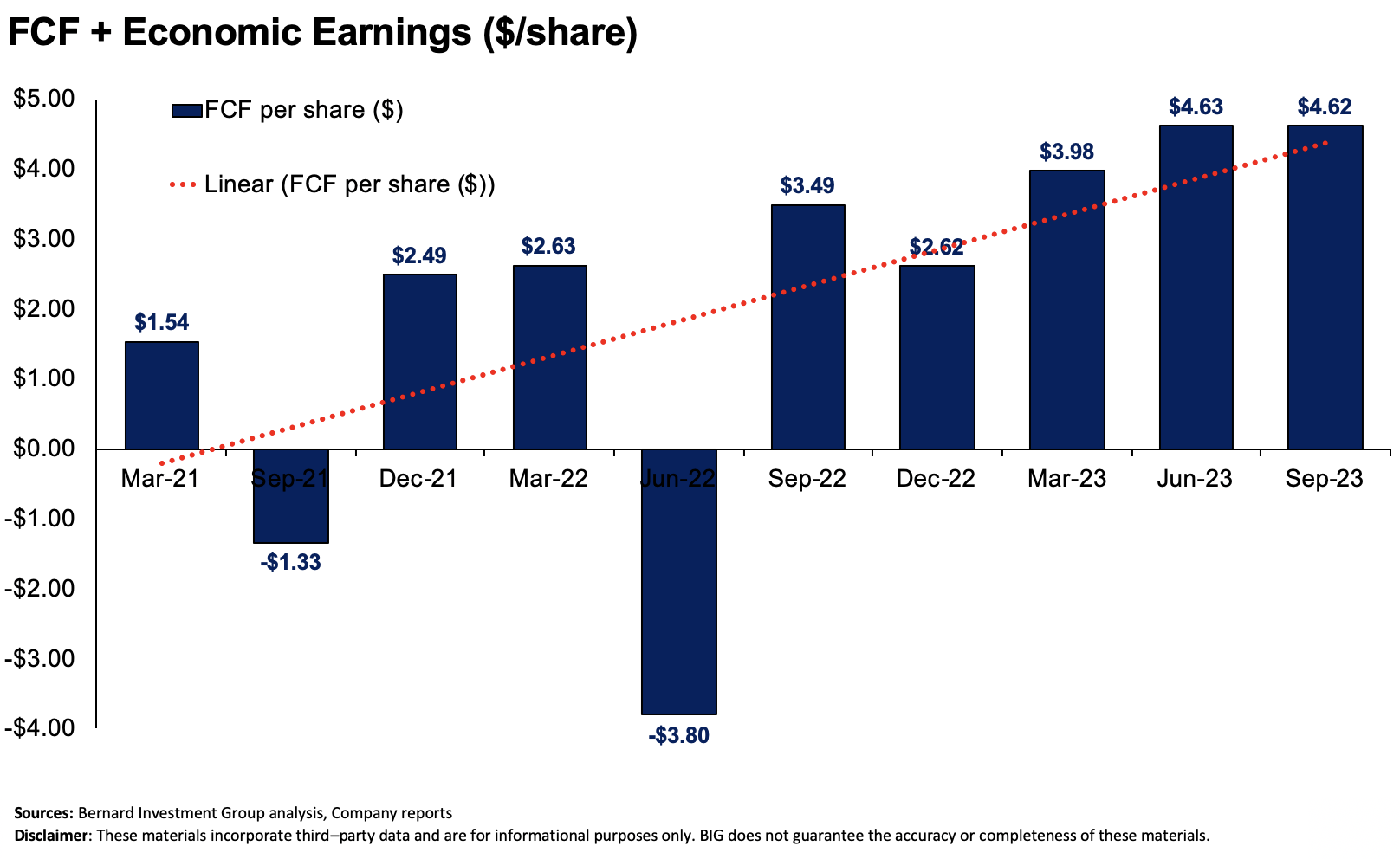

The analysis reveals a clear upward trend in FCF per share growth from 2021 to date. As seen in Figure 5, RCM has thrown off more than $4.60 in cash flow to its shareholders since Q2 2023, growing the 'equity coupons' from $2.50/share in '21 to $4.62/share in Q3 on a rolling TTM basis (85% growth in wealth). In my opinion, there is a small chance the market could be overlooking this fact of value creation from RCM.

Figure 5.

{kind=link}

Valuation + investment outlook

The stock sells at 37x forward earnings and 44x forward EBIT. These are quite the ask, and there's a reason to hold off on this. Forward 12 month investment returns are heavily impacted by starting multiples paid to acquire the securities.

At 37x forward and zero growth , this assumes a payback period of 37 years, provided the company can retain then keep all earnings for you.

Paying the 37x multiple, but with earnings growth of 74% in 1 year is slightly undervalued (37/74 = 0.5x); with 37% is fair (1x, similarly).

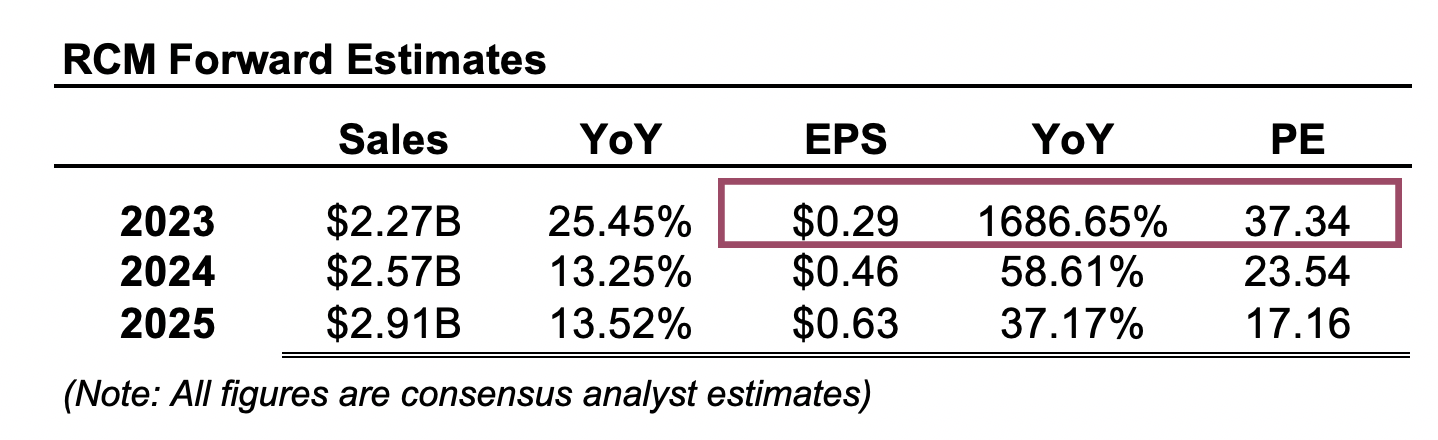

Analysts are in fact projecting eyebrow raising growth at the top and bottom lines (Figure 6):

- Consensus sales growth estimates are for 25% in 2023, continuing to 13.5% in '25 to produce $2.91Bn.

- Earnings growth forecasts for 2023 are-strangely enough- total 1,680% to $0.29/share, with a high of $0.48/share and low of $0.12/share.

- From there, the market expects it to grow earnings by 58% + 37% per year into 2025. This is equivalent to paying 17-23.5x 1-3 years out. With respect to sales, it is eyeing 13.5% per year into '25.

So you are buying a tremendous amount of earnings growth in acquiring RCM today. But you are paying $37 for every $1 of that future growth. This changes the outlook completely. So much so, the market requires over 90% rate of return to fairly compensate for the risk priced into RCM's stock price with a 12% discount rate.

Figure 6.

{kind=link}

Investment outlook

There are two questions. First, is this quadruple digit growth already priced in (and then rejected in price at the 50% retracement from earlier)? Second, is it worth paying 37x earnings to acquire RCM today? My judgement is, likely , and, no, not worth it. And here is why. I am neutral on RCM across all horizons.

- Short term (coming 12 months)- multiples of 37x earnings, far too high to realize any major gain or grow beyond this in the coming year (without catalyst).

- Mid term (1-3 years)- sales and earnings growth a standout. High projections top and bottom expecting a period of good business for the company. Could be skewed by '23 numbers, however. So company could rate higher-but off a lower base than it is now.

- Long-term (3 years+)- Business returns not at rates seen in 2020-'21, so we'd need a change in profitability to go bullish beyond 5 years.

Projected sales and earnings growth is undoubtedly strong. If these were to eventuate, RCM's stock returns could follow a different trajectory. Even if we have exhausted next year's 'growth trade', looking out 1 to 3 years, the picture may be very different. However, I can't ask to pay 37x earnings and get away with it. The punishment will be severe and painful. Those trading around the sector multiple of 18x earnings could be more viable. Net-net, revise to hold.

For further details see:

R1 RCM: Progress Noted, But At This Level, Valuations Just Don't Make Sense (Rating Downgrade)