RCM - R1 RCM: Value Proposition Is Only More Attractive Now

2023-06-14 17:00:49 ET

Summary

- RCM continues to increase its contract balances and net patient revenue under management.

- The firm is creating value for shareholders through its strategic investments.

- Investors are paying a higher market value in 2023 and this has all the momentum to continue.

- I reiterate a buy.

Summary of investment findings

Following the buy ratings for R1 RCM Inc. ( RCM ) in December and March , the company has been revalued 53% and 14% higher, respectively. After extensively revisiting the thesis, my conclusions are there is more to go for RCM. The forward-looking investment case can be boiled down to three critical facts in my opinion.

- One, the company is pushing higher on its business KPIs and operating metrics, as you'll see posted today.

- Two, sales and earnings are growing above peers, in a high-growth market.

- Three, the firm is throwing off respectable amounts of owner earnings (that are then reinvested back into the business).

If we were at an investment party, RCM would stand out in my opinion, with an ensemble of forward earnings growth, high returns on capital and durable business economics. That is an attractive sight in any rational investor's investment cortex.

Net-net, I reiterate RCM as a buy, looking to $24 as the next price objective, $4 above my previous target.

Figure 1.

{kind=link}

Critical facts for RCM investment

The investment case is best separated into its critical facts, with an analysis of the contributing factors to follow. Much is gleaned from the company's latest numbers, that tie in with a broader set of uptrends.

1. Financial performance

RCM had a solid start to FY'23 , with 41% YoY growth in revenue to $545.6mm on c.60% upside in adj. EBITDA to $142.2mm. At this run rate, the firm is set to do $2.2Bn and $568mm in turnover and pre-tax income for FY'23, respectively. Looking further at the data, I would put the following points to investors:

- RCM's deep experience in revenue cycle management ("Rcm") is the major spectacle that should be closely monitored going forward, in my view. RCM boasts deep experience in managing the revenue cycle of healthcare providers, quite a niche segment to operate in. There are high switching costs and high-end software that must be licensed in order to participate.

- End-to-end customers represent >$55Bn of the company's accessible net patient revenue ("NPR"), a total figure it now has exposure to through its client base. The benefit of RCM's services for healthcare providers is the outcome of high-quality patient results while reducing frictional costs associated with patient and clinician management.

- In my view, RCM's Rcm expertise is one driver to its long-term competitive advantage and long-term growth potential. This boils down to the profitability of its investments into the RCM software (discussed later), but it is also evident in its customer engagement strategy.

Last time, I talked about how it synthesizes data from over 500mm patient interactions annually, constructing unique patient insights from the data. If you look at it on a first principles basis, this 'database' helps RCM with the predictability in its customers' operations, ultimately enhancing the value proposition for its end-to-end and modular businesses.

2. Market catalysts

It's worth reminding readers of the sizeable runway RCM has in front of itself, given the growth estimates of the healthcare Rcm market. Management said the Rcm market was valued at $115Bn and growing at roughly 10% annually on the earnings call. Contrasting forecasts suggest a 12% CAGR over the coming years. Either way, these are high-growth percentages for the company's end market, where over 70% of providers still reportedly manage their revenue cycle processes in-house. Hence, one could surmise that the bulk of RCM's growth still lies ahead on this basis.

Increasing patient volumes, medical claims, underlying disease trends, and regulatory factors all contribute to the Rcm market's viability in the long run. As healthcare providers face increasing complexities in reimbursement processes, regulatory compliance, and technology advancements, they seek partners like RCM to navigate these challenges and optimize their financial performance. Hence, if it is that 70% of the addressable market could benefit from an Rcm provider, I am looking to the company as one to capitalize on this.

As it would show, the company is already on the yellow-brick road, having secured a c.$90mm increase in contract balance from Q1 FY'22-'23:

Table 1. RCM Contract balance, Q1 from 2017-2023

Data: Author, RCM 10-Qs

Unsurprising is that booked revenues have surged $160mm YoY in the same fashion. Given the nature of the business, extra focus must be had on the movement of operating cash flows versus revenues and working capital.

You can see these have remained within a relatively narrow range for RCM over the last 2-years to date in Figure 2, except for the April-June period in 2022, when the change in cash collections to cash tied up in working capital gapped substantially. Overall, however, the company has maintained a tight relationship on these three. I'd be concerned if AR was to tick higher on lower cash collections. Similar to revenues and so on. But the trajectories have been fairly well in tandem.

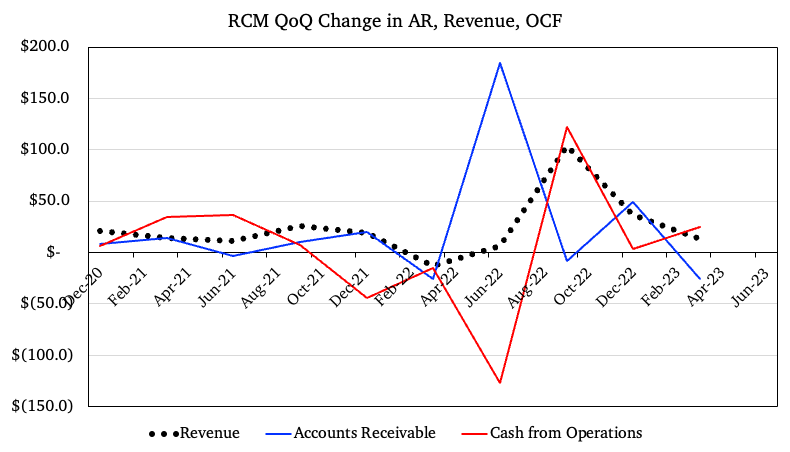

Note, Figure 2 shows the change in revenues, AR, and operating cash flows on a quarterly basis, versus the actual booked numbers. Here you can see the actual flow of cash and income, taking comfort in the correlation in all three, as mentioned.

Figure 2.

{kind=link}

3. Additional facts for consideration

RCM comes to us today with improving business economics that warrants close inspection. Investors were right to sell the company in June FY'21-December FY'22. RCM's market valuation took a good beating, that is for sure. But it doesn't surprise me why when looking at the data (Figure 2).

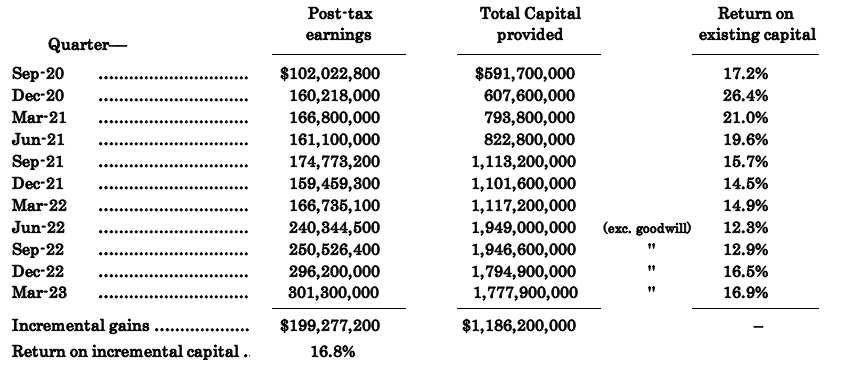

Across that time, the company averaged fairly sub-standard returns on its capital at risk, coincidentally, the same capital that investors have provided the firm. Hence, the returns of c.12-12.5% on capital provided, when investors could have got that in half the risk on their books in FY'22, were not attractive to intelligent capital. Shift forward two quarters and the story has changed drastically- another 4 points of incremental profit gains, plus, strong economic earnings above the hurdle rate (12% in this instance). Tracing back to the FY'20 period, this equates to a c.16% return on incremental capital, and 4% economic profit, tremendous value-add in my opinion.

Table 2. Return on incremental, existing capital

{kind=link}

Economic profits, those earnings above the discount rate, suggest RCM is worth paying for. To parse this out even further, observe Table 3, that shows the periodic investments/divestments RCM is making, next to the trailing post-tax earnings each quarter.

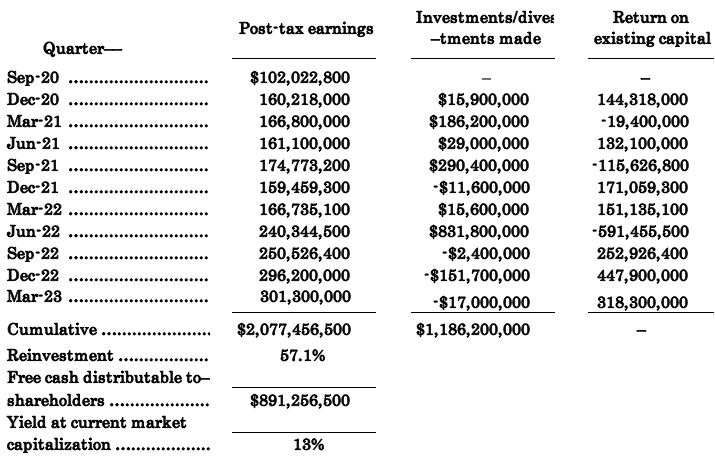

Notably, the firm has produced a cumulative $2Bn after-tax on just $1.18Bn in total investment. This suggests it invested just 57% of the earnings it produced, leaving 43% as residual earnings for shareholders, or as separate capital to invest for future growth.

Subsequently, the cash RCM has spun off to its owners amounts to a cumulative $891.5mm, otherwise 13% trailing yield on the current market cap. (note: figures use TTM values).

Table 3.

{kind=link}

4. Valuation

Investors are holding RCM with strong hands and are selling the stock at 3x forward sales and 2.5x book value.

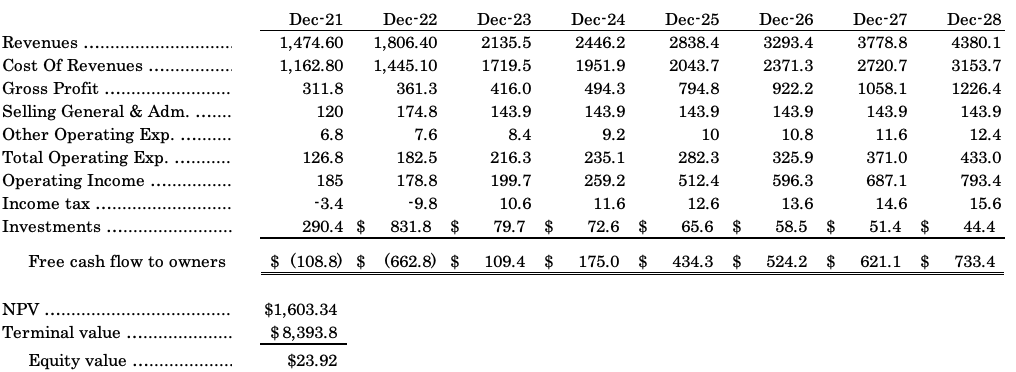

Given the company's forward estimates, there is potential for it to do $2.1Bn in turnover this year, or 16% YoY growth, on core EBITDA of ~$580mm and operating income of ~$200mm (Appendix 1). It could throw off $110mm in cash to shareholders on these results, stretching to $175mm the following year, presuming no extra reinvestment.

Projecting these cash flows out to FY'28 and discounting to an NPV at 12% gets me to $1.6Bn in steady-state value and $8.9Bn in terminal value (assuming a 3% terminal growth rate). This arrives at a $24 per share intrinsic valuation for the company, a substantial upside on the current market price.

In that vein, to get RCM at a 22% discount to the sector at 3x forward revenues is somewhat of a good deal in my eyes. I am happy to pay this and my numbers have the company fairly valued at 53x forward earnings (note: 1) treating earnings as post-tax income; 2) $9.9Bn firm value/$188.4 = 53x).

These numbers are supportive of a buy rating in my view.

In short

Net-net, there is supportive data to corroborate a revised buy thesis for RCM. Three major catalysts to price change exist:

- The firm is attracting higher amounts of NPR and has 500 customers on the books with 500mm patient interactions in its database. It will leverage this in its offerings going forward.

- The Rcm market is expanding at 10-12% going forward, serving the company well to push out its footprint and capture more NPR.

- With the increase in contract balances, the firm is primed to throw off cash to shareholders. My numbers have it to spin off $109mm this year and $175 in FY'24.

- Added to this, valuations are supportive when looking at the projected value of the company's cash flows.

Collectively, these points align with my investment criteria and build on an already-strengthening position. I advocate buying RCM and look to $24 as the next price objective.

Appendix 1.

{kind=link}

For further details see:

R1 RCM: Value Proposition Is Only More Attractive Now