RA - RA: Big Cut Leads To Opportunity

2023-09-27 09:21:10 ET

Summary

- Several higher-yielding closed-end funds have cut their distributions this year, resulting in significant drops for those trading at high premiums.

- Brookfield Real Assets Income Fund Inc. was one of these cutters that has now seen the fund drop to a deep discount.

- This deep discount makes the RA CEF now much more appealing than it had been at any time in the last few years.

Written by Nick Ackerman, co-produced by Stanford Chemist.

We've seen a number of higher-yielding closed-end funds ("CEFs") cut their distributions this year. A couple of noteworthy funds were trading at rich premiums, which then subsequently saw those premiums collapse upon the announced cuts. Generally speaking, high, unsustainable yields mixed with funds that are trading at rich premiums don't mix well. The timing is always different, but the end result is usually devastating losses for investors who bought at rich premiums.

One of those funds was the Brookfield Real Assets Income Fund Inc. ( RA ). I haven't covered this fund since going back to the end of 2020 . At least not specifically covering it, although I mentioned it alongside discussing Nuveen Real Asset Income and Growth Fund ( JRI ). In the world of CEFs, it's hard to find exact peers, but these two funds share several similar characteristics.

The main idea here was that JRI was a more attractive option than RA in most of the last several years now due to valuation. That was until RA's distribution cut of around 40% , which took the monthly distribution from the $0.199 per month amount that it paid for years down to $0.118. This is now where the potential opportunity lies in taking advantage of the fund dropping to such a deep discount. At the very least, the prospects going forward for this fund are much more promising than they were a month ago.

The Basics

- 1-Year Z-score: -3.46

- Discount: -16.39%

- Distribution Yield: 11.53%

- Expense Ratio: 1.69%

- Leverage: 16.35%

- Managed Assets: $970 million

- Structure: Perpetual.

RA's investment objective is seeking "high total return, primarily through high current income and secondarily through growth of capital." To achieve this, the fund will invest "primarily in real assets such as infrastructure and real estate securities, across equity and fixed income around the world."

While the fund mentions no constraints on asset class allocation, they've switched to almost entirely being a fixed-income fund with very little left in the equity sleeve. The fund is also not constrained to investing just in the U.S., although in implementing its strategy, the fund is highly dominated by U.S. exposure currently.

Why The Distribution Cut?

The fund is modestly leveraged, but this was a more recent change as they've been taking down their borrowings. At the end of fiscal 2021, the total amount outstanding on their credit facility or reverse repo was ~$405 million. This was brought down to ~$316 million by the end of 2022 and is now down to ~$162.3 million as of their last semi-annual report.

As with most other leveraged funds, they are having to deal with higher borrowing costs. The total expense ratio climbs to 3.54% when including borrowing costs, up from 2.76% at the end of 2022 and 2.13% the year before that. Their borrowings are based on OBFR plus 0.90%. That puts their latest borrowing costs at 6.22% - then you add in the fund's advisory and other operating expenses, and you can start to see why a cut was necessary for the distribution.

The world where you can earn a spread above that, without increasing risk substantially, gets smaller and smaller the more short-term rates rise. Of course, this has all been driven by the Fed bumping up interest rates, which is having a higher impact on the short-term rates relative to the long-term, which haven't reacted as much. Thus, the scenario we are in is where the yield curve is inverted.

The fund also has some floating rate exposure in its fixed-income sleeve. They had also recorded some gains from futures contracts, which were utilized to help hedge against some of the higher interest rates that were expected. As of their last semi-annual report, they showed no gains resulting from futures. At the end of their annual report, for the period ending December 2022, they also had no outstanding futures contracts at that time. Though they did record some gains, meaning at some point last year, they had these derivatives set up as a bit of a hedge.

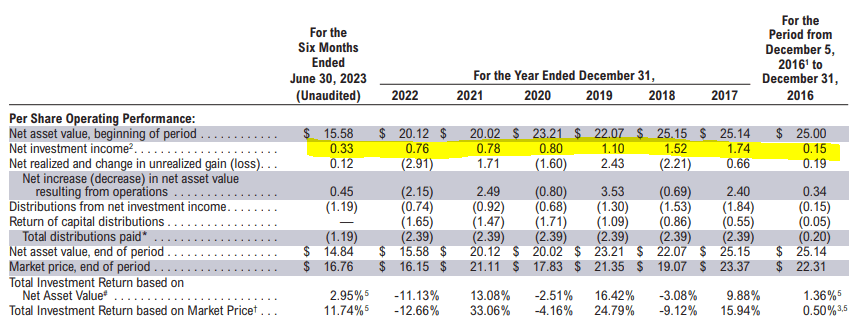

Now, let's put on top of this the fact that the fund was also struggling to cover its distribution previously, and the writing was on the wall. For the last several years, the fund's net investment income had been continuing to decrease while still maintaining what looked like an appealing distribution rate on the surface. Since 2017, the fund's NII has been in decline mode.

So, the latest increase in borrowing costs was just the final push they needed to succumb to what should have happened several years ago. At this pace, NII for this year would result in a decline of nearly 14% year-over-year.

RA Financial Highlights (Brookfield (highlight from author))

{kind=link}

Is The New Payout Sustainable?

Thanks to the deep fall in the fund, the actual distribution rate for RA hasn't moved that much, relatively speaking. Prior to the cut announcement, based on the old rate, it was trading with a 14.1% distribution rate. With the new rate against the lower share price, we are looking at a still tempting distribution rate of 11.76%.

However, one of the larger questions likely on the minds of investors is if the new rate is sustainable. On a NAV distribution rate basis, the 9.83% is certainly looking much more reasonable than it had been previously. Prior to the cut, it was at a 16.3% distribution rate.

That said, as we can clearly see, the fund's NII is going to look like it would run at about $0.66 this year. That's still well below the new lower annualized rate of $1.416, meaning that it still isn't really comfortably being covered. As we noted previously, the fund is dominated by fixed-income investments, with only around a 3% weighting in equities at this time. Therefore, capital gains may be harder to come by, as we'd expect with equity-focused funds.

RA Asset Allocation (Brookfield)

Given that they just recently cut and their prior hesitation to even do that, I don't suspect a cut anytime soon. It is even possible that during a black swan event or a deep recession, despite the fund's MBS exposure, they'd continue to carry on with the same distribution as well. That is, if history is any guide, as that's what the fund had previously done during the Covid crash.

On the other hand, should the Fed back off interest rates due to a mild recession or "soft landing," that could ease up the pressure from RA, which could provide improving coverage going forward. Additionally, most expect that we are at or very close to near-peak rates for this cycle. That could mean getting some stabilization in terms of their borrowing costs would stop increasing.

This would be the more optimistic view. Lower interest rates would ease the borrowing costs and could see increased prices for their underlying debt portfolio. According to CEFConnect, the average bond price of their debt comes to $88.51.

Big Premium Set Up For Big Fall

Of course, a high distribution rate that is unsustainable on its own isn't necessarily going to cause a lot of damage when it's cut. If a fund is already at a deep discount, it'll face some pressure, but nothing nearly like what we saw with RA due to its massive premium.

Thus, JRI seemed like a much better place to hide out and wait if one still wanted exposure to some of the same places that RA was invested. At one time, RA had a bit more in its equity sleeve, which had a more meaningful impact on the chances of producing capital gains. Admittedly, that made it more similar to JRI, and so these funds have drifted a bit in the last several years in terms of exposure.

Still, the actual underlying total NAV return of the two funds in the last year ended up almost identical. JRI took a bit of a divergence when it headed higher due to the fund's larger equity exposure through 2021.

Ycharts

Despite this, it was RA who had provided the mirage that made it seem like it was a better investment in terms of total share price return precisely because of that large premium.

Today, with the cut in now, we've seen JRI look like the better performer on a total share price return basis. However, the valuations in terms of discounts now put these two right at the same level.

While the cut is likely to leave RA with a scar for a long time and continue to trade at a deep discount for what could be a considerable period, it no doubt represents a better choice today than it had through most of the last few years.

Conclusion

Brookfield Real Assets Income Fund cut their distribution. It certainly took longer than I expected, but it was a fund ripe for a big tumble when it did due to its large premium. Today, the fund's distribution rate is much more reasonable, but they still are showing a lack of coverage based on their mostly fixed-income portfolio that is failing to produce enough NII.

That said, the valuation of the fund is much more tempting and puts it in a good spot for some of this to contract over time. Based on the much lower share price now, the distribution rate for shareholders is still a tempting ~11.5%. Those who bought before the cut in the last couple of years probably aren't happy, but there often comes a time to exploit these collapses based on the drastic valuation shift for new capital.

For further details see:

RA: Big Cut Leads To Opportunity