PDO - RA: Brookfield Real Assets But Fake Yield

2023-08-30 11:35:14 ET

Summary

- Brookfield Real Assets Income Fund Inc. is a credit-focused fund that primarily invests in real estate and other "real assets."

- The fund had been trading at a premium to NAV.

- Multiple red flags pointed to the unsustainable distribution, and we got a good realignment this morning.

Some setups can be obvious but does not mean that they pan out immediately. Most excursions in the market are designed to frustrate you and test your patience. This can be true for both bearish and bullish calls. One notable area that we focus on are the yield plays and we do so to find where sustainable distributions can be found. Here, we don't mean sustainable in an ESG sense (though that's important too). No, we're referring to the ability of a fund or stock to pay distributions without depleting NAV. Shockingly, this simple knowledge piece is ignored by many. We look at one fund today that had all the red flags but no one bothered to listen.

Brookfield Real Assets Income Fund Inc. ( RA )

So you start off with a Brookfield name and, of course, add the asset class that Brookfield is most known for. A match made in heaven.

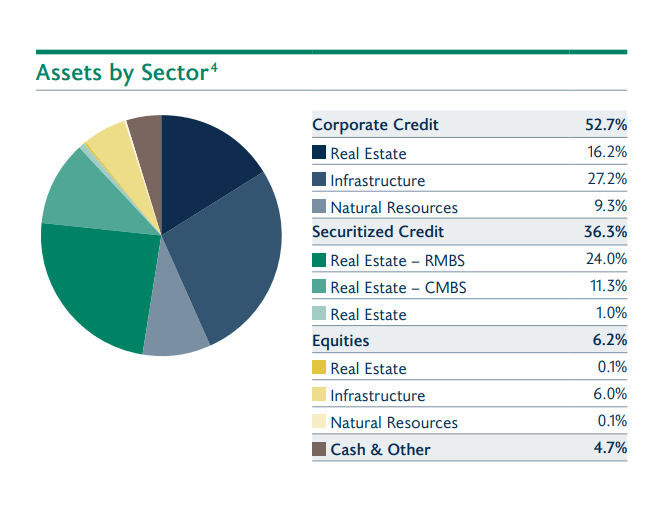

The investment objective of RA is to seek high total return while focusing on high current income and also aiming for growth of capital. We have lost track of the number of funds that talk about high current income as a primary objective, that don't even come close to preserving the NAV, let alone growing it. But we will get to that part later. Getting back to what RA does, it invests primarily in real estate and secondarily in other "real assets" like infrastructure securities and natural resources Securities. The fund is a credit-focused fund with fixed income securities ruling the roost. On last check, equities formed only 6.2% of the total assets.

{kind=link}

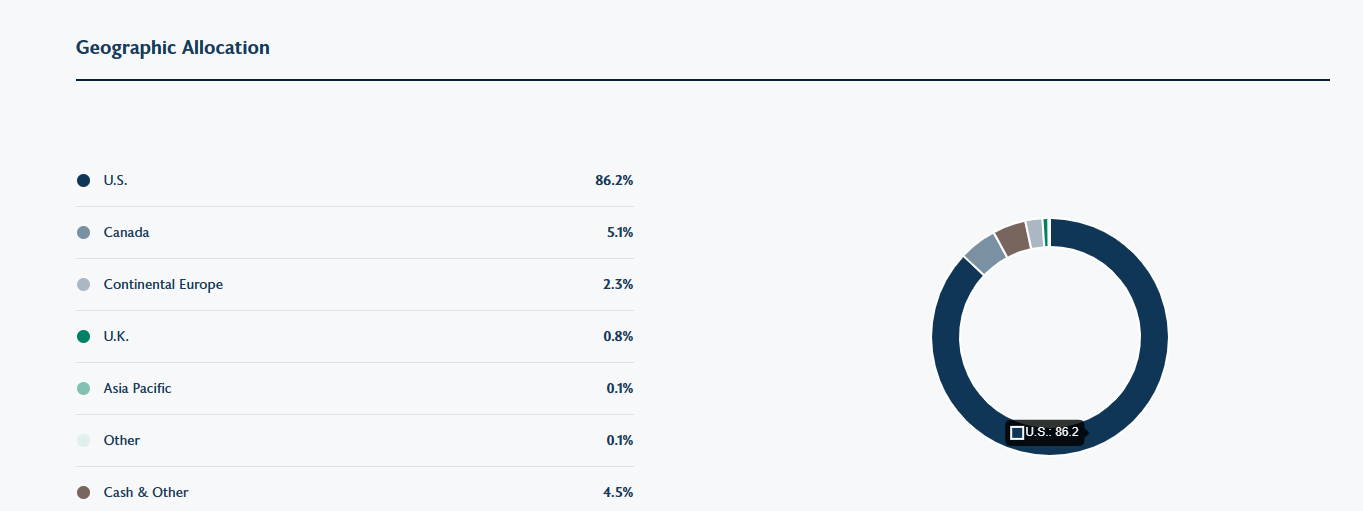

Credit was heavily focused on real estate either as corporate or securitized bonds. Overall the mix looks about in line with what their brochure hints they would do. The fund was primarily invested in the US but has just enough of an international flavor to be deserving of a geographic allocation slide.

{kind=link}

Risk Breakdown

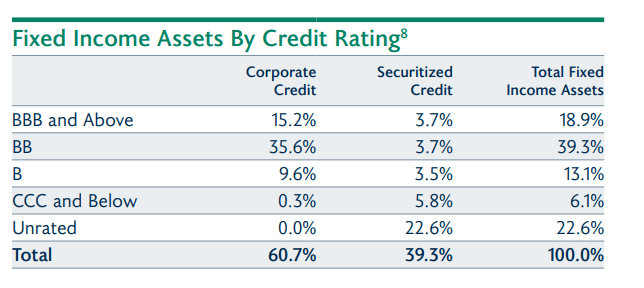

With a credit-focused fund you have to first break down the risk that it's taking. What we see is what you would find in the typical high yield funds like SPDR Bloomberg High Yield Bond ETF ( JNK ) and Shares iBoxx $ High Yield Corporate Bond ETF ( HYG ), although both of those tend to have far less unrated issues.

{kind=link}

Overall the credit risk here is likely to be similar to JNK and HYG as the former two don't hold so many BBB-rated securities. The fund is extremely diversified with 529 holdings and is currently taking almost no duration risk. The weighted duration was shown to be 2.4 years and that likely means it can handle further rate hikes quite well.

RA Fact Sheet

What Just Happened?

Of course, all of that was a routine description of what the fund does. Nothing there would prepare you for the morning bloodbath.

Interactive Brokers Pre-Market Aug 30

{kind=link}

So what happened? Well a little background story here will be required reading for investors. The fund, thanks to the Brookfield name and a massive distribution was trading at a decent premium to NAV.

CEF Connect

15% is not the realm of craziness we have seen, but it's definitely in the orange zone for funds. That premium meant that investors were enjoying a 16% distribution rate on NAV and a 14.15% distribution rate on market price. To put how silly this is in context of what the fund can/could generate we give you three reference points.

1) JNK yields 6.51%

Sure, that is an eyeballing way of looking at things, but these ETFs could not care less what you felt about becoming an income investor. They pay what they make. That number comes to 6.51%. If you look at their yields to maturity minus expenses (our favorite forward-looking measure), we see that is in the 8% range. A bit better but nowhere in the zone of the 16% distribution rate on NAV from RA.

2) Look At The Total Return Performance

This is a simple test. A fund that has been around for a long time should have a total return exceeding or at least matching its distributions for it to be sustainable distribution. We're ignoring managed payout funds, though even they have to pay the piper at some point. But even there, you should look at the total returns (on NAV, not on price) to see how sustainable your distributions are. This is how RA looked as of yesterday. As seen below we are nowhere near the zip codes of a double-digit total return on any time frame.

{kind=link}

So what part of those numbers made investors think that 16% distribution rates were sustainable is beyond rational comprehension. Did they add all those highlighted numbers to reach 17.84%?

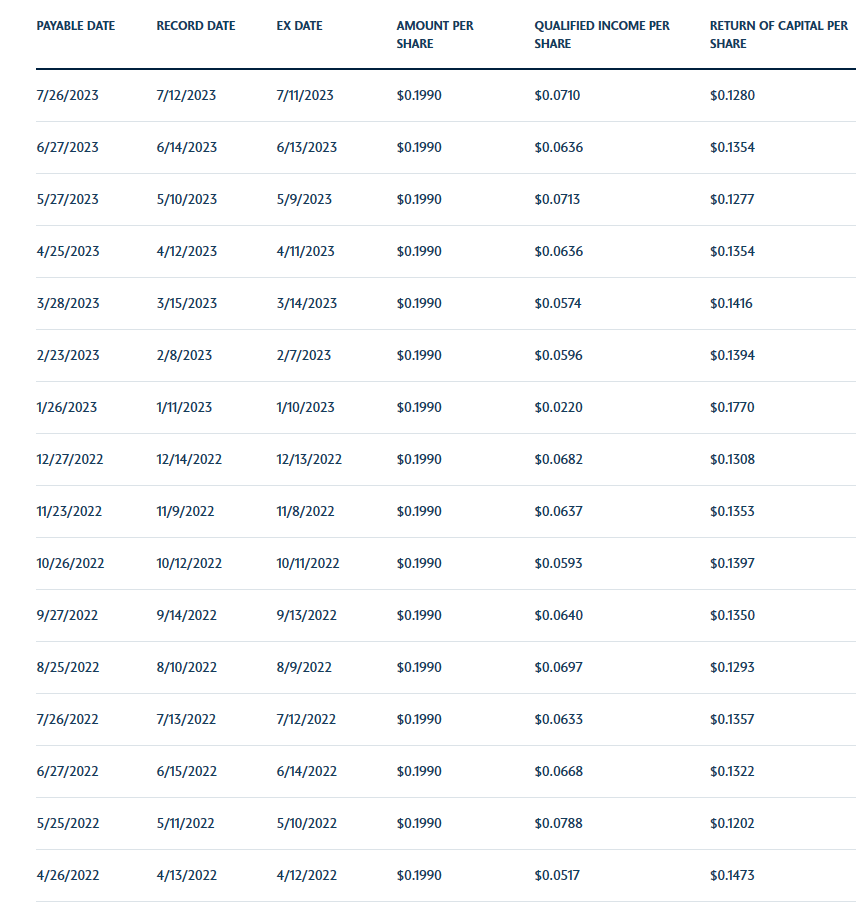

3) Look At The Return Of Capital

Alongside the total return, one needs to look at the relative amounts of return of capital that the fund designates on its distributions. While some like to argue that "ROC" is good, the fact is that it is good only to the extent point 2 above gives a green light. In other words high ROC with total returns coming in at 20%-30% of the distribution is the reddest of flags. RA gave you warning that this crimson tide was coming on your shores. Just look at the ROC over the past one and a half year. That looked sustainable?

{kind=link}

In fact, RA has an ROC for every single distribution all the way back to the first. So logically, there was no way this distribution was sustainable and eventually even the fund managers saw it that way. The distribution was reduced by 41% to $0.1180 per month from $0.1990 per month.

Outlook and Verdict

Let us mention the one thing we do like about this fund. Its leverage is on the lower side relative to peers.

RA Fact Sheet

Most funds are pushing 30% on this number. PIMCO Dynamic Opportunities Fund ( PDO ), one popular choice for dangerous yield chasing is at 50%.

CEF Connect

So at least RA has that going for it, which is nice. But coming back to what's a sustainable distribution here. We think the leverage is currently a wash thanks to very high interest expense and high management fees. Overall, we think the credit side can deliver about 7% annual total returns (after fees) assuming defaults remain mild and don't go wild. The equity side is too small to influence things so 7% is your best-case upper-end on NAV. If you think we sound too suspicious, just look at the long-term NAV returns which are half this number. We might add the bulk of that was during some rather benign credit conditions when Powell and company sang "the hills are alive with the sound of music."

So 7% on NAV would mean about a $1.00 annually. The fund is still going the way of overdistributing and aiming for $1.416 annually. So NAV depletion will still happen, even in the very best-case situation. Now, the new yield (still over 10%) and the Brookfield name might get a whole new set of yield chasers in. You know the kind that have no regard for total return and insist getting their money back to buy groceries is about all that matters in the world of investing. At present, we would avoid buying the falling knife. This is one to keep your eyes on in case of a very deep discount (20% plus) post a credit event. In other words we want a lower NAV and a wider discount to begin to consider this fund. Outside that, we would stay out.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

RA: Brookfield Real Assets But Fake Yield