RA - RA: This Incredibly Expensive CEF Has An Unsustainable Distribution

2023-05-02 17:17:52 ET

Summary

- Investors are trying to desperately protect their wealth and increase their incomes to handle the current high rate of inflation.

- Brookfield Real Assets Income Fund Inc. invests in a portfolio of securities issued by companies that use significant real assets in their operations, which should help protect wealth.

- The RA closed-end fund is mostly debt, which is surprising and may prevent these securities from protecting purchasing power as well as equities would.

- The fund is substantially overdistributing and is dependent on new investors purchasing shares to maintain the distribution.

- The RA fund is substantially overvalued at the current price.

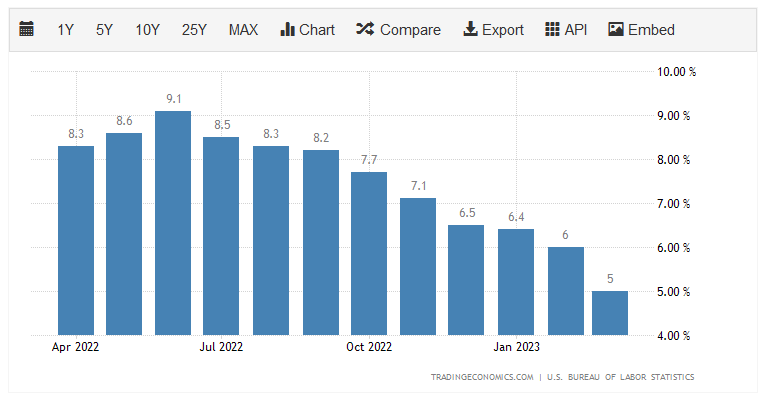

It is quite certain that one of the biggest problems facing the average American household today is the rapidly rising cost of living. Over the past several months, inflation has run at the highest levels that we have seen in more than forty years. This can be seen quite clearly by looking at the consumer price index, which has increased by at least 6% year-over-year in eleven of the past twelve months:

{kind=link}

This high rate of inflation has caused real wage growth to be negative for 24 straight months as well as pushed many families to have to take on second jobs, enter the gig economy, spend down their savings, or borrow against their credit cards. I have discussed this in recent blog posts, such as this one . In short, most people today are desperate to increase their incomes just to keep their bills paid and maintain their lifestyles.

As investors, we are certainly not immune to this. After all, we have bills to pay too. We also have a second concern, which is maintaining the purchasing power of the wealth that we have spent a considerable amount of effort accumulating. After all, what is inflation if not the destruction of the purchasing power of a given currency? Fortunately, there is a good way to achieve both goals with one simple trade. This is to purchase shares of a closed-end fund, or CEF, that specializes in investing in real assets, such as infrastructure and real estate. This is because infrastructure and other real assets tend to hold their value as they are necessary for the proper functioning of society and require actual human or mechanical labor to construct and maintain. There is also a limited supply of infrastructure as it cannot be created out of thin air like fiat currency.

In a recent article , I discussed how infrastructure can also be a good source of income. This comes from the fact that most infrastructure companies have fairly low growth rates and so pay out most of their cash flows to investors. When we combine this with the generally low multiples that are assigned to infrastructure companies by the market, the distributions tend to be a high percentage of the share price of these companies, which translates to high yields.

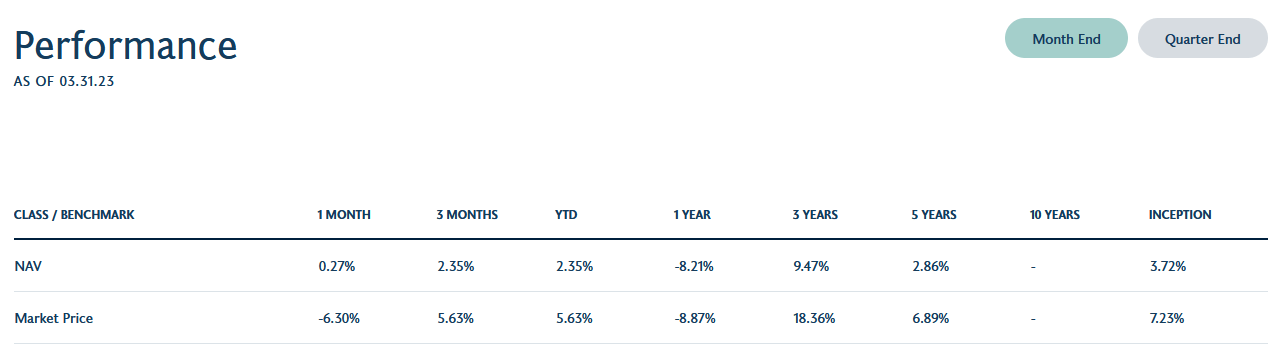

In this article, we will discuss the Brookfield Real Assets Income Fund Inc. ( RA ), which is a closed-end fund that specializes in investing in real assets. This fund has consistently proven to be one of the most popular funds in the sector, which is probably due to Brookfield's somewhat legendary status when it comes to infrastructure funds. Despite this popularity, the fund still boasts a 13.92% yield at the current price. It is somewhat overpriced though, which is not exactly surprising considering the Brookfield name. Let us investigate and see if this fund could be a good addition to a portfolio today.

About The Fund

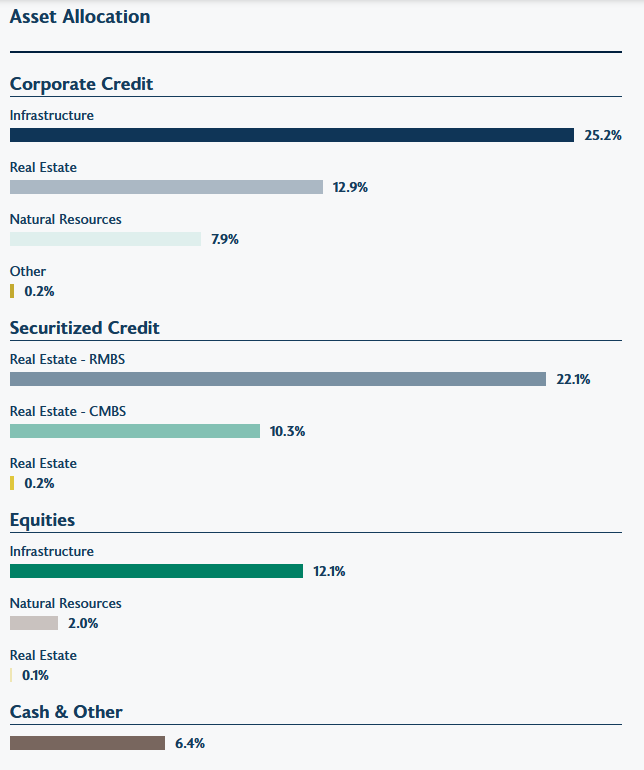

According to the fund's webpage , the Brookfield Real Assets Income Fund has the stated objective of providing its investors with a high level of total return. This is somewhat surprising considering that this is primarily a debt fund. In fact, 74.14% of the fund is currently invested in bonds and other debt securities:

CEF Connect

A look at the fund's own website says essentially the same thing. In fact, the fund's website says that only 14.2% of the fund is currently invested in equities:

{kind=link}

The difference between the two sources is likely due to the dates of the material. The CEF Connect data comes from the fund's financial statements dated December 31, 2022, but no date is given for the data on the website. It seems likely that the website is newer, which would imply that the fund has been moving its assets out of common equities and into debt securities and cash during the first few months of this year. That is not necessarily a bad move, considering that energy prices have been weak so far this year and there are numerous problems currently plaguing the commercial real estate sector.

This may explain why the fund is more exposed to residential real estate than to commercial real estate. As everyone reading this is likely well aware, the pandemic and the lockdowns caused a major change in how many people work. Rather than going to the office every weekday, many people have been given the option to work from home and have yet to return to work in their offices. In fact, we have seen many companies embrace this shift and cancel their office leases, opting to save money and let their staff work from home. This has caused a surge in real estate vacancies.

According to CommercialEdge , the national office vacancy rate sat at 16.7% in April, representing a 0.20% increase year-over-year. This high vacancy rate is undoubtedly straining the finances of many real estate developers and investors, who generally need the rent money to cover the mortgages on their properties. Residential properties have not been having the same problem as these properties are generally used by people as primary homes, so they will generally opt to pay their rent or mortgages in order to avoid being homeless. The fund seems to realize this, which we can clearly see in the fact that residential mortgage-backed securities greatly exceed commercial mortgage-backed securities in terms of weighting in the fund.

We can also see that the RA fund is more heavily invested in infrastructure than in real estate. The fund, unfortunately, does not define what it means by infrastructure. Usually, this refers to things like toll road owners, railroads, pipeline operators, telecommunications companies, and utility firms. Basically, these are the companies that own things that most people take for granted but are very necessary for the proper functioning of modern society. After all, an Internet-based company like Alphabet Inc. ( GOOG ) would be gone in a few days if there was no functioning telecommunications infrastructure. The same goes for most companies.

As a result of being necessities, these companies tend to enjoy remarkably stable cash flows over time, regardless of macroeconomic conditions. This is because most people prioritize paying their utility bills over discretionary expenses during times when money is tight. That is something that is a real advantage today considering the strained finances of many American households and the fact that we are seeing numerous indicators that point to a possibility of a recession in the latter half of this year. In short, it is a good idea for your portfolio to include assets that are unlikely to be affected by a recession. As we can see above, infrastructure accounts for the majority of this fund's portfolio so it could be an option to get this exposure.

As we saw earlier, the fund's portfolio is primarily weighted towards debt. This is why its focus on total return is somewhat surprising. After all, debt is generally considered to be an income investment because its potential for capital gains is limited. After all, debt securities have no inherent connection to the growth and prosperity of the issuing company since a firm will not increase the interest rates that it pays its creditors just because its profits went up. In addition, a bond pays out its face value at maturity so any investor that buys a new issue debt security and holds it to maturity will only receive the interest payments as a return from the bond.

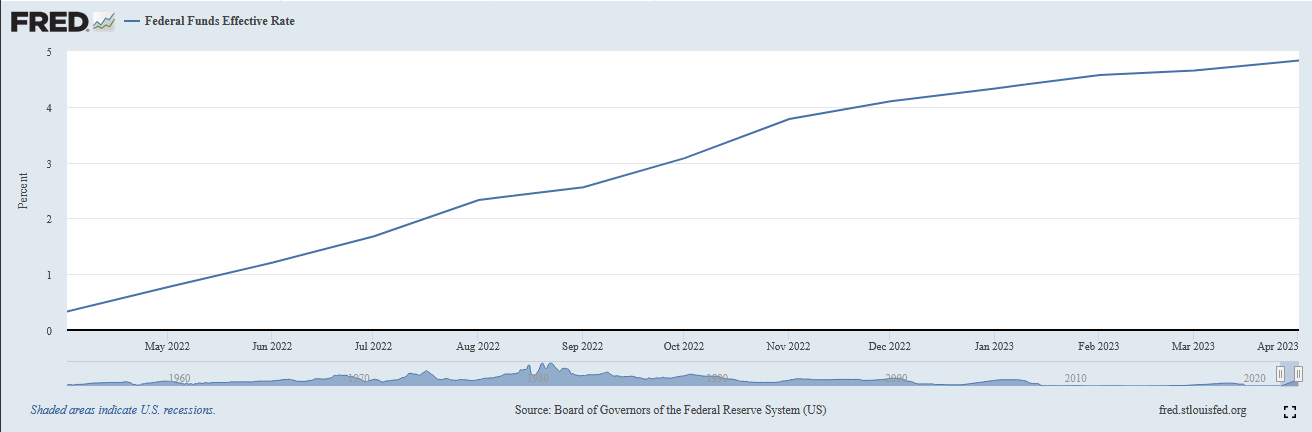

With that said, it is possible to earn some capital gains by trading bonds. This is because bond prices vary with interest rates. It is an inverse relationship, so when interest rates go up, bond prices go down. The reverse is also true. As everyone reading this is likely well aware, the Federal Reserve has been aggressively raising interest rates over the past year in an effort to combat the incredibly high inflation rates in the economy. Back in April 2022, the effective federal funds rate was 0.33% but today it is 4.83%:

{kind=link}

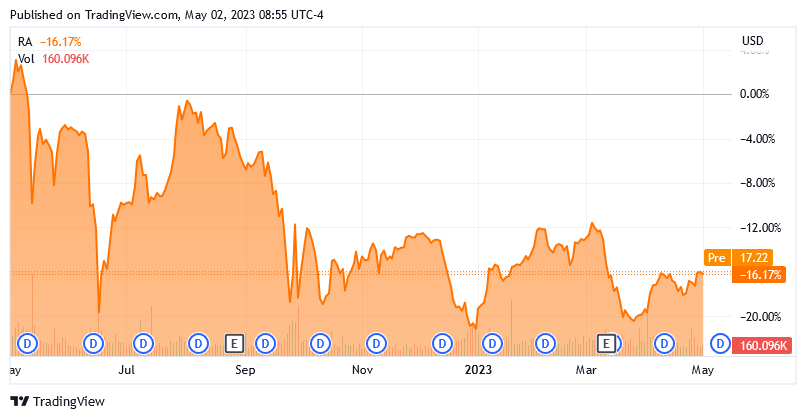

This has created a very challenging environment for bonds and bond funds, with nearly all of them handing in losses over the past year. The Brookfield Real Assets Income Fund is no real exception to this as it is invested primarily in debt securities. The fund is down 16.17% over the past year:

{kind=link}

This is not exactly the kind of performance that most investors would find endearing, but it is somewhat misleading. One big reason for this is that the fund paid out distributions over the entire period. As such, an investor over this period would have received those and offset some of the losses in the share price. In addition, the fund's share price performance does not always match the performance of the underlying portfolio. In fact, the fund's portfolio delivered a positive total return in March, but the shares still delivered a negative return:

{kind=link}

The fund's net asset value performance is the most important thing because this is the figure for the total return of the portfolio. As we can see, it usually underperforms the shares in the market, which is disappointing as it means that most of the time investors are overpaying for the fund's performance. However, we can also see that the portfolio holds up much better than the fund's shares during periods of weakness. Thus, the shares appear to be far more volatile than the actual portfolio. This could be something that can be exploited during periods of market weakness, but it does not help our thesis of buying the fund to preserve purchasing power. That is unfortunate.

Leverage

Closed-end funds like the Brookfield Real Assets Income Fund have the ability to employ certain strategies that have the effect of boosting the effective yield of the portfolio well beyond that of any of the underlying assets. One of these strategies is the use of leverage. In short, the fund is borrowing money and using those borrowings to purchase fixed-income and common equity securities issued by infrastructure and real estate companies. As long as the purchased securities have a higher yield than the interest rate that the fund must pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not using too much leverage because that would expose us to too much risk. I generally like to see a fund's leverage remain under a third as a percentage of its assets for this reason. Fortunately, the Brookfield Real Assets Income Fund meets that requirement as its levered assets only comprise 27.03% of the fund today. Thus, this fund appears to be striking a reasonable balance between risk and reward.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Brookfield Real Assets Income Fund is to provide its investors with a high level of total return. However, the fund primarily invests in debt securities issued by infrastructure or real estate companies in pursuit of that objective. These securities primarily provide their investment return through direct payments to the investors. The same is true of infrastructure companies, which have relatively limited growth and compensate for that with incredibly high yields.

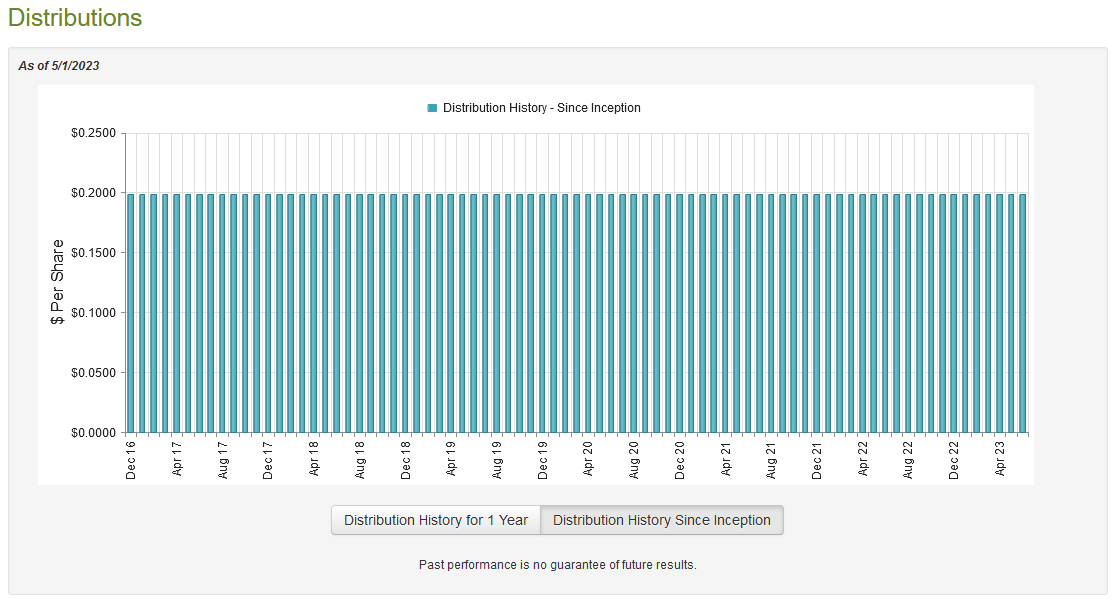

The fund applies a layer of leverage to these securities in order to boost the income (and total return) that it obtains from them and then pays its investment profits out to the shareholders. As such, we can assume that this fund probably has a fairly high yield itself. That is certainly the case as it currently pays a monthly distribution of $0.1990 per share ($2.388 per share annually), which gives the fund a 13.92% yield at the current price. The fund has been remarkably consistent about its payout over the years, as it has never changed its distribution over its entire history:

{kind=link}

This makes the Brookfield Real Assets Income Fund one of the few real estate or infrastructure funds that has never changed its distribution. This is surprising because a number of infrastructure companies cut their own payouts back in 2016 and 2020 due to the turbulence that affected the energy markets during those years. Then again, the fact that this fund is much more focused on debt than equity meant that it could avoid the worst of that turbulence. After all, companies do not cut the money that they pay on their debt unless they have absolutely no choice. It is very rare for the financially stable companies that this fund invests in to be forced to take that option. This is yet another reason to consider a position in this fund, and it will undoubtedly appeal to any investor that wants a stable and secure source of income to maintain and grow their wealth in the face of today's very high inflation rate. As is always the case, though, it is critical that we have a look at the fund's finances in order to determine its ability to maintain this distribution. After all, we do not want to find ourselves the victims of a distribution cut since that would reduce our incomes and almost certainly cause the fund's share price to decline.

Fortunately, we have a fairly recent document that we can consult for the purposes of our analysis. The fund's most recent financial report corresponds to the full-year period that ended on December 31, 2022. As such, it will not include any information from the first quarter of this year, but it will still give us a good idea of how well the fund handled the challenging market conditions that dominated headlines all last year. This report is also newer than the one that we had available the last time that we discussed this fund so the update will be very helpful.

During the full-year period, the Brookfield Real Assets Income Fund received $57,522,822 in interest and $11,551,627 in dividends and distributions from the assets in its portfolio. As is usual for a closed-end fund that includes infrastructure assets, some of the money received was considered a return of capital and is not included in investment income. When we net this amount out of the total, the fund reported an investment income of $66,740,754 over the course of the year. It paid its expenses out of this amount, which left it with $40,945,992 available for investors.

This was, unfortunately, nowhere close to enough to cover the $127,844,826 that Brookfield Real Assets Income Fund actually paid out in distributions during the period, though. At first glance, this is certain to be concerning as the fund's net investment income was substantially less than the amount that it is actually paying out to shareholders.

It is important to note though that the fund has other methods that it can employ in order to get the money that it needs to cover its distributions. For example, it might have capital gains. The fund failed miserably at this over the course of 2022 though as it reported net realized losses of $486,772 and had another $163,642,906 in net unrealized losses. Overall, the fund's assets declined by $140,459,239 after accounting for all inflows and outflows. Its assets would have declined by much more than this over the course of the year, but the fund sold new shares to raise $105,641,039 over the course of the year. The fact that it did this and still saw its assets decline is concerning.

This is not a new problem for the fund, though, as it also failed to cover its distributions in 2021. Despite 2021 having a much stronger market environment, the fund only earned $105,413,205 through investment income and capital gains, yet it distributed $110,234,761 to its shareholders. In other words, the fund is dependent on bringing in money from new investors just to maintain its distribution even in a very strong market environment. This is ultimately unsustainable, especially considering that the money supply has been declining over the past few months.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the Brookfield Real Assets Income Fund, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of all the fund's assets minus any outstanding debt. This is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can obtain them at a price that is less than the net asset value. This is because such a situation implies that we are buying the fund's assets for less than they are actually worth. This is, unfortunately, not the case with this fund today. As of April 28, 2023 (the most recent date for which data is available as of the time of writing), the Brookfield Real Assets Income Fund had a net asset value of $15.31 per share but the shares currently trade for $17.17 each. This gives the shares a 12.15% premium to the net asset value at the current price.

This is a very high price to pay for any fund, especially one that is consistently failing to cover its distribution. It is also well above the 7.17% premium that the shares have had on average over the past month. Thus, Brookfield Real Assets Income Fund appears to be excessively expensive at the current price. Caution is urged for anyone that is interested in buying it.

Conclusion

In conclusion, real assets such as real estate and infrastructure are a good way to generate income and maintain the purchasing power of your wealth in the current environment. The Brookfield Real Assets Income Fund seemingly offers a great way to do that with its incredibly high yield and portfolio of securities issued by companies that own significant real assets. The fact that the fund's assets are mostly debt does reduce the appeal somewhat though since debt will not benefit from appreciating asset values driven by inflation.

The more important thing here, though, is that Brookfield Real Assets Income Fund is consistently failing to cover its distribution solely through its operations and is dependent on new investors putting money into the fund. It is also incredibly expensive at the current level. Thus, it would be a very good idea for any potential investor to be cautious here before buying shares of the Brookfield Real Assets Income Fund.

For further details see:

RA: This Incredibly Expensive CEF Has An Unsustainable Distribution