RAAX - RAAX Remains A Subpar Inflation-Hedge ETF No Reason To Buy

2023-04-29 06:38:26 ET

Summary

- Federal Reserve hikes and changes in underlying economic conditions have caused inflation to go down these past few months.

- Lots of investments and funds are likely to underperform under these conditions.

- RAAX is one of them.

I last covered the VanEck Inflation Allocation ETF (RAAX), a multi-asset class inflation-hedge ETF, in late 2021. In that article, I argued that RAAX's asset allocation strategy was ineffective, and so the fund did not merit an investment. RAAX has posted moderate loses since, even though inflation remains elevated, broadly in-line with expectations.

RAAX Previous Article

RAAX's asset allocation strategy remains broadly ineffective and inflation seems to be moderating. Under these conditions, I see no reason to invest in the fund.

RAAX - Quick Overview

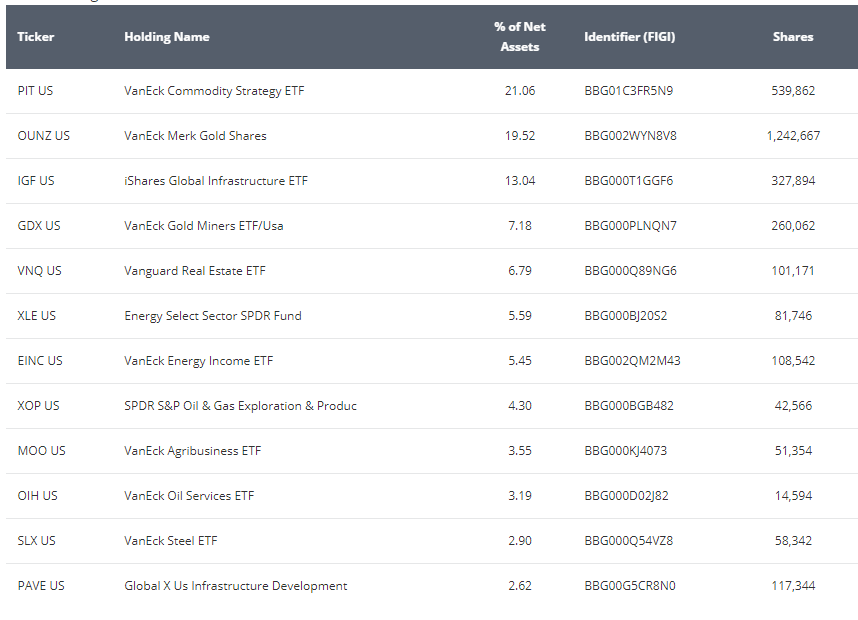

RAAX is a diversified, multi-asset class inflation-hedge fund-of-funds. It invests in most relevant inflation-hedge asset class, through investments in cheap, simple, broad-based index ETFs. Asset class weights and holdings are as follows.

{kind=link}

RAAX provides investors with diversified exposure to inflation-hedge asset classes, so the fund should outperform when inflation is high and rising. That was the case in 2022, as expected.

Data by Ycharts

In my opinion, and considering the above, RAAX is an adequate, diversified, broadly effective inflation-hedge ETF. Although there is some merit to an investment in such a fund, there are two important negative issues to consider. Let's have a look at these.

RAAX - Moderating Inflation

RAAX is an inflation-hedge ETF, meant to outperform during periods of high and rising inflation. Although inflation remains elevated, it is going down, and fast. Annual inflation has dropped from higher than 9.0% in mid-2022, to 5.0% in March. MoM inflation seems to be going down at a slightly more accelerated pace, but with significant volatility.

Economic conditions are such that inflation should continue to trend downwards. The Fed has vowed to do whatever it takes to bring inflation back under control, has hiked rates aggressively in an attempt at doing so, and has indicated that further hikes are likely . Banks are tightening lending standards in the wake of SVB's ("SVB") collapse, which means effectively higher rates, even if benchmark rates themselves remain unchanged.

Bloomberg

Commodity prices are softening too, with oil prices down almost 25% these past twelve months.

Considering the above, inflation seems likely to go down moving forward. RAAX is an inflation-hedge ETF, and does not really make much sense as an investment under these conditions.

RAAX - Subpar Asset Allocation Strategy

Conditions are currently not very favorable to RAAX, and the fund's specific strategy does not help matters.

RAAX's asset allocations are partly dependent on fundamental and technical indicators. RAAX might decide to overweight energy stocks on valuation or momentum grounds, and vice versa. Same for most other asset classes and securities. Details are scarce, the process is proprietary, but results seem subpar, at best.

RAAX has underperformed relative to most inflation-hedge ETFs during recent inflationary episodes. Specifically, RAAX underperformed relative to the SPDR SSGA Multi-Asset Real Return ETF ( RLY ), another diversified, multi-asset class fund. RLY's returns looked particularly strong in 2022, a year of elevated inflation.

Data by YCharts

RAAX's performance compares unfavorably to narrower inflation-hedge asset classes and ETFs too. By my counts, RAAX underperformed commodities, energy, miners, and inflation equities during 2022. The fund did outperform relative to treasury inflation-protected securities, partly due to timing: RAAX's relative performance was much weaker prior to, and after, 2022 relative to these securities.

Data by YCharts

On a slightly more positive note, RAAX's underperformance is not consistent, with the fund sometimes (slightly) outperforming relative to peers, sometimes matching their performance. RAAX slightly outperformed RLY YTD.

Matched the performance of said fund in 2021.

Data by YCharts

As mentioned previously, RAAX's underperformance is at least partly due to a subpar asset allocation strategy. The fund attempts to invest in best-performing inflation-hedge asset classes, but does not consistently accomplish said goal, and sometimes selects worst -performing asset classes instead. As an example, the fund heavily invested in gold in 2022, during which said asset class underperformed other inflation-hedge securities, including commodities and energy equities.

Data by YCharts

RAAX also attempts to minimize losses during downturns, by shifting towards cash during these. Said attempts have been unsuccessful in the past, with the fund going into cash quite late in 2020, and remaining there for too long. Significant underperformance followed.

Data by YCharts

On a slightly more positive note, RAAX's asset allocation strategy does not consistently fail, with the fund sometimes making successful, profitable trades. These were almost certainly responsible for RAAX's stronger performance YTD, although I had difficulties pinpointing which specific trades or positions were responsible for this. From what I've seen, the fund decided to take some profits on its energy and real estate holdings sometime in the past few months, which have coincided with weak performance in these two industries.

Considering the above, it seems that RAAX sometimes underperforms, sometimes matches the performance of an inflation-hedge index ETF / the average inflation-hedge asset class. Current economic conditions do not seem particularly favorable to RAAX, and the fund does not look to be a particular strong fund in its niche either.

Conclusion

RAAX is a multi-asset class inflation-hedge ETF. RAAX's asset allocation strategy is broadly ineffective and inflation seems to be moderating. Under these conditions, I see no reason to invest in the fund.

For further details see:

RAAX Remains A Subpar Inflation-Hedge ETF, No Reason To Buy