RDN - Radian Group Inc. Seems To Be Quite Fairly Valued At The Moment

2023-07-17 13:20:38 ET

Summary

- Radian Group's stock price has risen nearly 30% in the last six months, as the company benefits from lower interest rates and a strong investment portfolio.

- The company has been growing its dividend aggressively, with a payout ratio of 17.5%, and is expected to increase its dividend yield from the current 3.5%.

- Despite a large portion of its portfolio in corporate bonds, Radian's strong net margins and free cash flow margins indicate potential for further growth and larger returns for investors.

Introduction

As many are making predictions about how the FED will continue developing the path of interest rates and whether or not we will continue to see higher rates, the stock price of Radian Group Inc. ( RDN ) has been climbing higher and fast - up nearly 30% in the last 6 months alone. For the moment, the FED is holding steady as they continue to monitor the decrease in inflation. Lower rates could be a benefit to a mortgage lender like RDN and seeing as a nearly half of their investment portfolio sits in corporate bonds, lowering rates could be a bullish signal for bonds and yield RDN higher ROI.

The valuation is slightly below the rest of the sector with a p/e of 7.8 and a p/b of 0.91. The company has been quite aggressively growing its dividend the last few years, but still only has a payout ratio of 17.5%. I think we can go higher which would result in a higher dividend yield than 3.5% which it currently has. I view RDN as a company that has efficiently grown its investment portfolio and sits in a position where it will grow quickly as interest rates go lower and more volumes come in.

Company Structure

Radian has been operating since 1977 and focuses on mortgage and real estate services in the United States. They have divided the business into two primary segments , Mortgage and Homegenius. The mortgage segment offers credit-related insurance coverages with the aid of private mortgage insurance on residential first-lien loans. Apart from this the segment also focuses on credit risk management and underwriting solutions for clients.

Primary Insurance (Investor Presentation)

The second segment primarily focuses on title services, covering a variety of insurance and noninsurance titles. Here the revenue streams are diversified to cover many bases and ultimately have it result in strong customer and client retention. The Homegenius segment also does real estate valuations and different asset management services.

{kind=link}

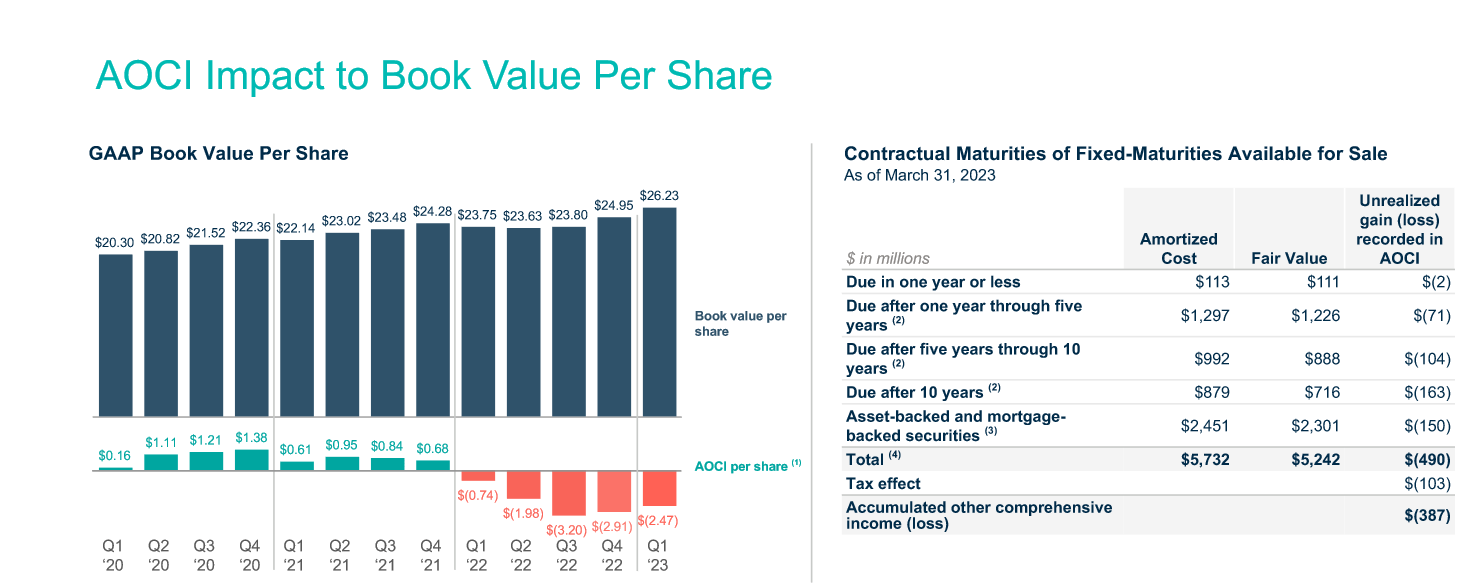

Given that RDN has a large amount of its portfolio in corporate bonds, nearly 46%, the company has accumulated a significant AOCI per share value right now. Sitting negative at $2.47. Luckily when looking at what the AOCI entails, the near term is quite fine. There is a total of negative $2 million in unrealized losses within the coming 12 months. That should have no major impact on the final net income for FY2023. Rather the reason for the AOCI decreasing this much is because of the “due after 10 years” having unrealized losses of $163 million. As many banks and companies investing in bonds have seen worrisome results, for RDN I expect this to be short-term volatile, as not a large amount is due shortly. That means for now the situation might look difficult to assess, but the long-term for corporate bonds are positive in my view.

Fundamentals

Since its founding the margins of RDN have been improved and grown into a state where I think they are some of the best in the industry. The net margins sit at a TTM of 59%, the result of a very solid investment portfolio that has netted them very good NI growth. FCF margins are at 53% but the payout ratio is still only 17.5%, this showcases the potential that RDN can expand further with their dividend and yield investors larger returns.

Dividend Summary (Seeking Alpha)

RDN hasn't been distributing a dividend for a long time, but only recently started making strong improvements to it. I think this is the result of them realizing the stability of their financial position and how they are in a place where it makes sense to pass down earrings to investors. Dividend growth is expected to continue and in 2023 the total amount would be $0.9 per share, up 12.5% from the $0.8 per share in 2022 which was given out.

Earnings Transcript

On May 4 2023 RDN announced its Q1 report for 2023 and there were some comments on the earnings transcript that stuck with me.

-

Our primary Mortgage Insurance in force, which is the main driver of future earnings for our company, grew 5% year-over-year to $261.5 billion, including 8% year-over-year growth in our more profitable monthly premium insurance in force.

Seeing continued growth for the upcoming Q2 report in terms of Mortgage Insurance in force will be a key metric to evaluate the future potential of the business. Seeing a 5% growth YoY in Q1 set the tone that RDN will continue yielding large returns, and if Q2 posts similar results we might see the valuation grow even higher. The p/e could in my opinion for the short term reach a 9x multiple if the report is a positive surprise. On August 3 we will know, even though it's not long from now I am confident enough in the management team that rating RDN a buy now seems reasonable.

Risks Associated

The primary risk that I associate with RDN right is the exposure it has to bonds right now. The loss in AOCI hasn't been decreasing the last few quarters, but rather increasing. In Q3 2022 it reached a low of negative $3.2 per share, which also dragged down the book value per share it seems. Since it has increased to negative $2.47. But I would worry that if we see rates maintained at a high level for longer than the market expenses then it will continue to be a tough investment, and hurt the earnings in coming quarters. But as we discussed, the portfolio which RDN had wasn't in a lot of short-term bonds, but rather in 10-year ones.

Investor Takeaway

RDN is right now a solid dividend investment even though the yield sits at 3.2%. Estimates suggest a 12% increase in 2023 compared to 2022 to it. This is setting RDN up to be on track to become a very solid dividend payer in the future. The payout ratio is still not that high and with strong FCF margins, I find there to be room for more growth. That leaves me with a very positive view of RDN right now, especially when the valuation is not higher than the sector's. I'm therefore rating RDN a buy now.

For further details see:

Radian Group Inc. Seems To Be Quite Fairly Valued At The Moment