RADI - Radius Global Infrastructure: Although The Merger Agreement Is Risky It Looks Undervalued

2023-05-30 09:51:50 ET

Summary

- Radius Global Infrastructure signed a merger agreement for $15 per share under complicated macroeconomic conditions, despite receiving bids for up to $20.25 per share.

- The company operates rental streams underlying wireless sites and has valuable assets, with clients including large, well-established companies worldwide.

- Despite the risks from the merger, RADI is considered a stock for long-term shareholders, with the potential to be worth more than $19 per share.

Radius Global Infrastructure (RADI), after receiving bids for $18 and even $20.25 per share, signed a merger agreement for $15 per share in cash under complicated macroeconomic conditions. Considering capex acquisition growth, annualized in-place rents growth, and the special characteristics of the properties owned, I believe that RADI could be worth more than $19 per share. In my view, buying shares only because of the merger spread does not make a lot of sense because the spread is small considering the risks. Even considering the risks from the merger, I believe that RADI is a stock for long term shareholders.

Radius Global Infrastructure

Radius Global Infrastructure operates a significant number of rental streams underlying wireless sites through the management of tower, rooftop, and cell site leases.

I believe that the assets acquired by Radius Global Infrastructure could be quite valuable in the future. It is a pity that the company decided to sell itself. It is a pity mainly for shareholders, who may not be able to enjoy future FCF streams. According to the website of Radius, the properties do not only offer high barriers to entry, but are also predictable and offer durable escalating rents. In my view, both predictability and the recurrent revenue make the assets quite unique.

Finally, I believe that it is worth noting that tenants are large and well established companies all over the world. I would not expect them not to pay the bills. The company reported a list of the clients in a presentation given to investors.

Source: Presentation To Investors

{kind=link}

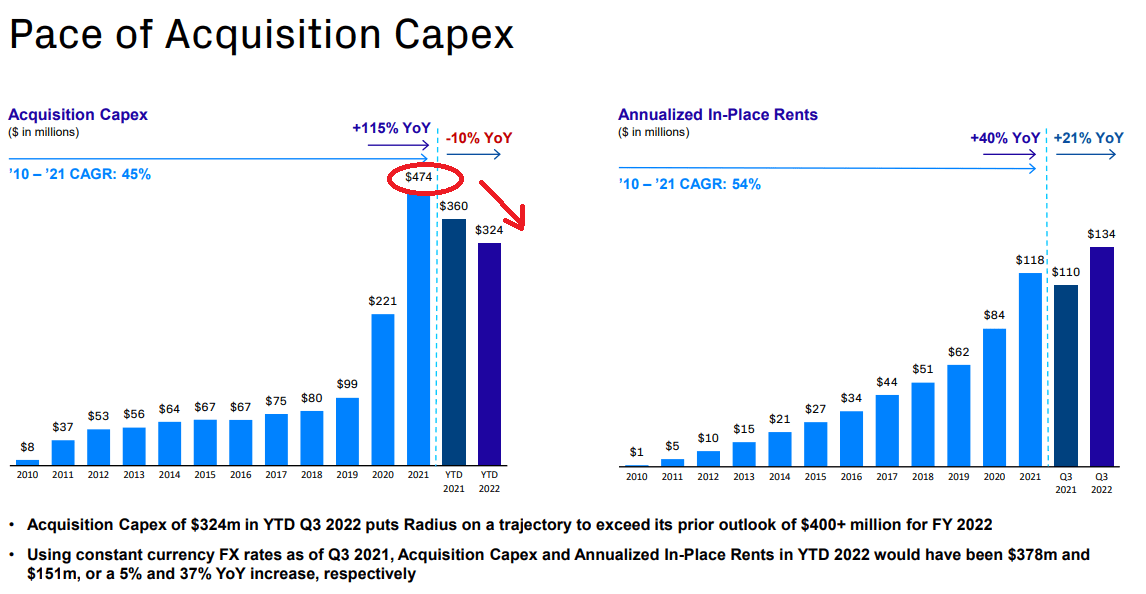

I also believe that Radius was reducing the level of capex acquisition, which means that FCF could emerge in the coming years. Since 2010, the company reported acquisitions capex growth close to a CAGR of 45% and annualized in-place rents growth of close to 54%.

Source: Presentation To Investors

{kind=link}

Balance Sheet

As of March 31, 2023, Radius Global reported cash and cash equivalents worth $197 million, restricted cash of $2 million, and short-term investments close to $34 million. Also, with trade receivables worth $11 million and prepaid expenses and other current assets close to $29 million, total current assets stood at $275 million.

The most valuable assets are right-of-use assets or finance leases worth $415 million, telecom real property interests close to $1.582 billion, and real property interests worth $1.998 billion. Management also reported intangible assets of $11 million, goodwill close to $80 million, and total assets worth $2.452 billion.

{kind=link}

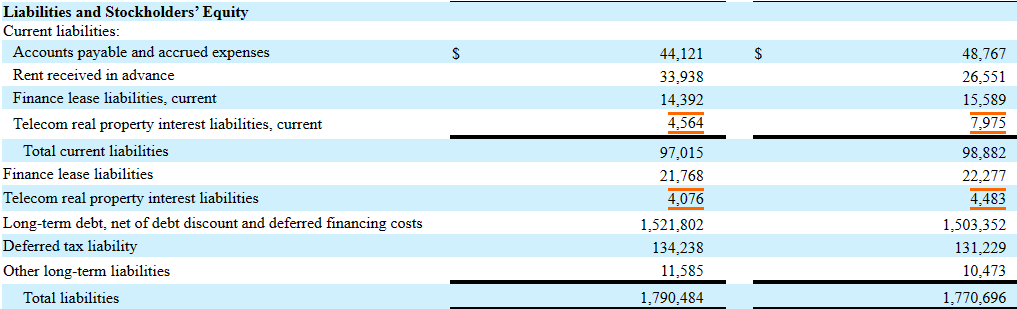

With respect to the total amount of liabilities, Radius Global Infrastructure reported accounts payable and accrued expenses close to $44 million, rent received in advance of $33 million, total current liabilities of $97 million, finance lease liabilities close to $21 million, telecom real property interest liabilities close to $4 million, and long-term debt of $1.521 billion with total liabilities of $1.79 billion. The asset/liability ratio stands at more than 1x, however the total amount of debt appears elevated. I believe that the Board of Directors decided to sell mainly because of the total amount of debt.

{kind=link}

Valuation Of Financial Advisors, Forecasts From Management, And My Valuation

Before I offer my own valuation figures, I believe that offering some context about the forecasts made by financial advisors to the merger makes sense. I used some of the figures from other advisors, so my numbers are not out of the box. One of the financial advisers used discount rates close to 7.9%-8.7% and estimates given by management.

Using the mid-year convention for discounting cash flows and discount rates ranging from 7.9% to 8.7%, reflecting estimates of Radius' weighted average cost of capital, Goldman Sachs ( GS ) discounted to present value, as of December 31, 2022, (i) estimates of unlevered free cash flow for Radius for the calendar years 2023 through 2032, as reflected in the Forecasts . Source: Merger Agreement

The price obtained by this advisor through a DCF model was between $5.35 and $16.11 per share. I could see other methods used for Radius Global Infrastructure, but I believe that the DCF model is the most appropriate.

Goldman Sachs then divided the range of illustrative equity values it derived by the number of fully diluted outstanding shares of Class A Common Stock as of February 28, 2023, as provided by and approved for Goldman Sachs' use by the management of Radius, using the treasury stock method, to derive a range of illustrative present values per share of Class A Common Stock ranging from $5.35 to $16.11. Source: Merger Agreement

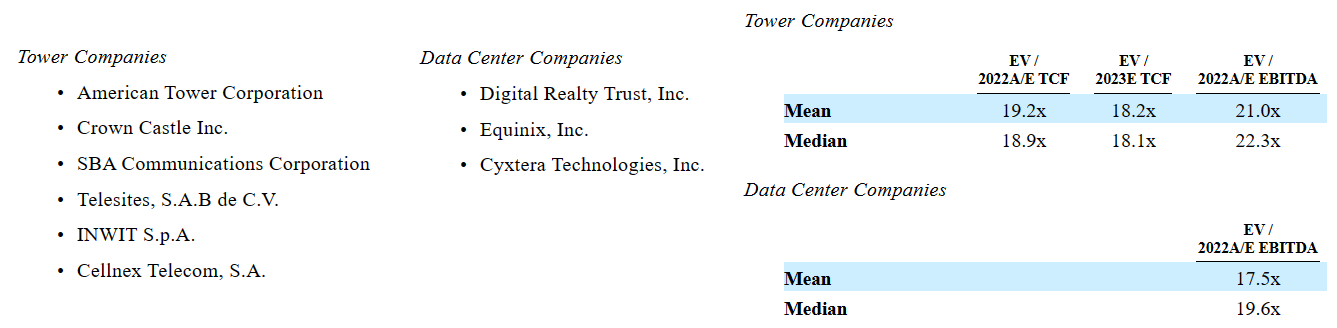

Another advisor who shared his figures in the merger agreement included a median EV/2022 EBITDA of close to 22x for Tower Companies and median EV/EBITDA of 19x for Data Center companies. I believe that Radius Global Infrastructure is more a tower company than a data center, so I believe that using a valuation close to 22x EBITDA sounds like more correct.

{kind=link}

The implied valuation obtained by this other financial advisor to the merger stands at close to $12-$15 per share. Note that the multiple used was close to 15.5x-17.5x EBITDA.

{kind=link}

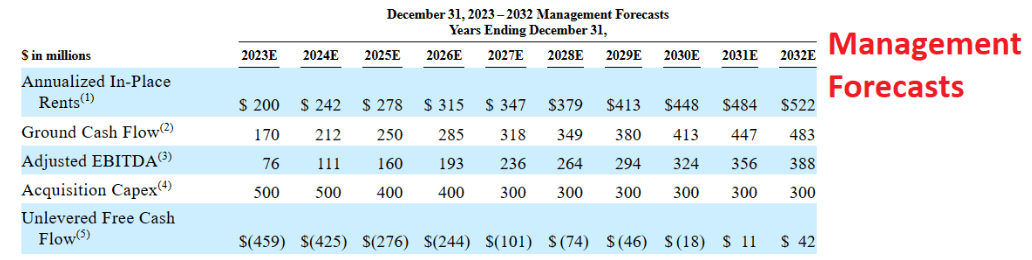

I could also find the forecasts given by management about the future. The management believes that it could reach an adjusted EBITDA close to $388 million in 2032. Besides, it forecasted 2032 unlevered FCF close to $42 million, capex close to $300 million, and ground cash flow of about $483 million.

{kind=link}

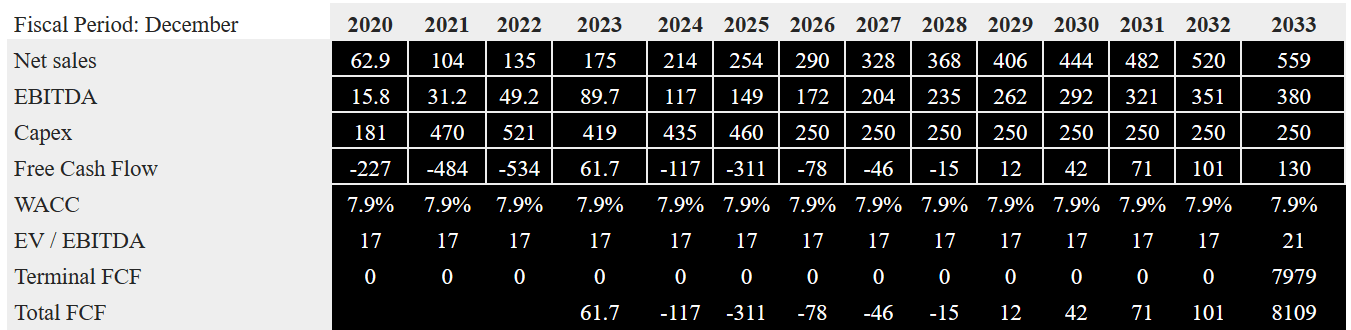

My figures included ground cash flow of $483 million, 2032 adjusted EBITDA of $388 million, acquisition capex close to $300 million, and 2032 unlevered free cash flow of $42 million. If we use an EV/ground cash flow of 17x and a WACC of 7.9%, the implied enterprise value would be close to $2.633 billion.

{kind=link}

If we add cash and cash equivalents of $197.879 million, restricted cash close to $2.417 million, and short-term investments worth $34.612 million, and subtract finance lease liabilities worth $14.392 million and long-term debt worth $1.521 billion, the implied equity valuation would be close to $1.310 billion. In sum, the implied price would be $13.14 per share.

Source: Work From The Author

Under my optimistic case scenario, I included my own estimates, and combined them with those from advisors who did not work in the deal . In my view, these figures could be a bit more realistic than those seen in the merger agreements.

I included 2033 net sales close to $558 million, 2033 EBITDA around $379 million, and 2033 capex close to $250 million. If we also include 2033 free cash flow of $129 million, a WACC of 7.9%, and EV/EBITDA of 21x, the implied enterprise value would be close to $3.237 billion.

{kind=link}

I added cash and cash equivalents close to $197.87 million, restricted cash of $2.4 million, and short-term investments of around $34.612 million, and subtracted finance lease liabilities of about $14 million and long-term debt close to $1.521 billion. In sum, the equity valuation would be close to $1.914 billion, and the implied price would be close to $19.1 per share.

{kind=link}

The Background Of The Merger: There Was A Lot Of Demand For The Company, But Bidders Lowered Their Bids As Macroeconomic Conditions Worsen

The background of the merger showed that a significant number of investors and strategic buyers were interested in the business model of Radius. I could read that close to 11 parties held conversations with financial advisors to the merger. I also saw bids for close to $20.25 per share in April 2022 and $18 and $17.5 per share in March 2022. However, as soon as the stock price declined, buyers lowered their offers. One of the buyers, which had offered $20.25 per share, ended up offering $12.0 per share. My conclusion from the background of the merger is that Radius Global could be worth close to $19-$22 per share under a favorable macroeconomic scenario.

{kind=link}

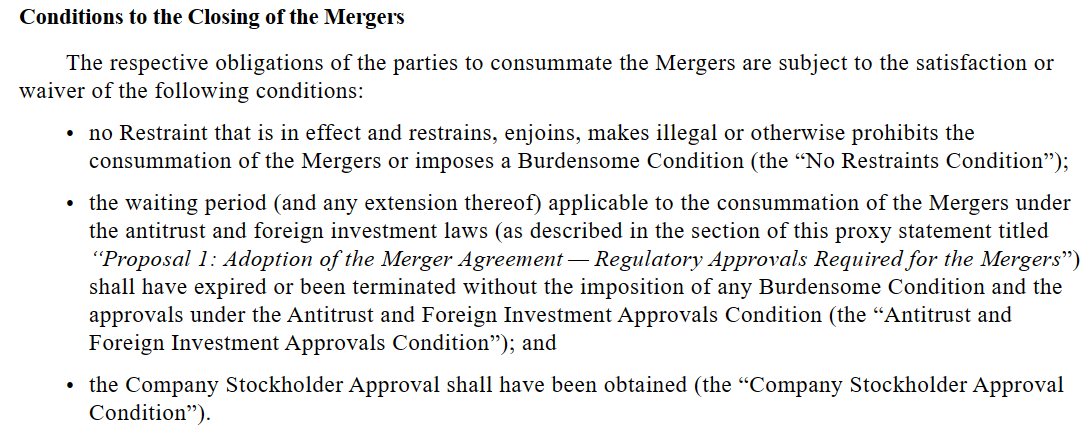

The Conditions Do not Seem Difficult To Reach

I believe that the conditions are not very complicated. The buyer and the seller will have to respect the waiting period required for antitrust laws and the approvals under the Antitrust and Foreign Investment Approvals condition. Shareholders will have to approve the deal too. Most investors may not appreciate the Foreign Investment Approvals condition. The deal may take a bit longer than usual.

{kind=link}

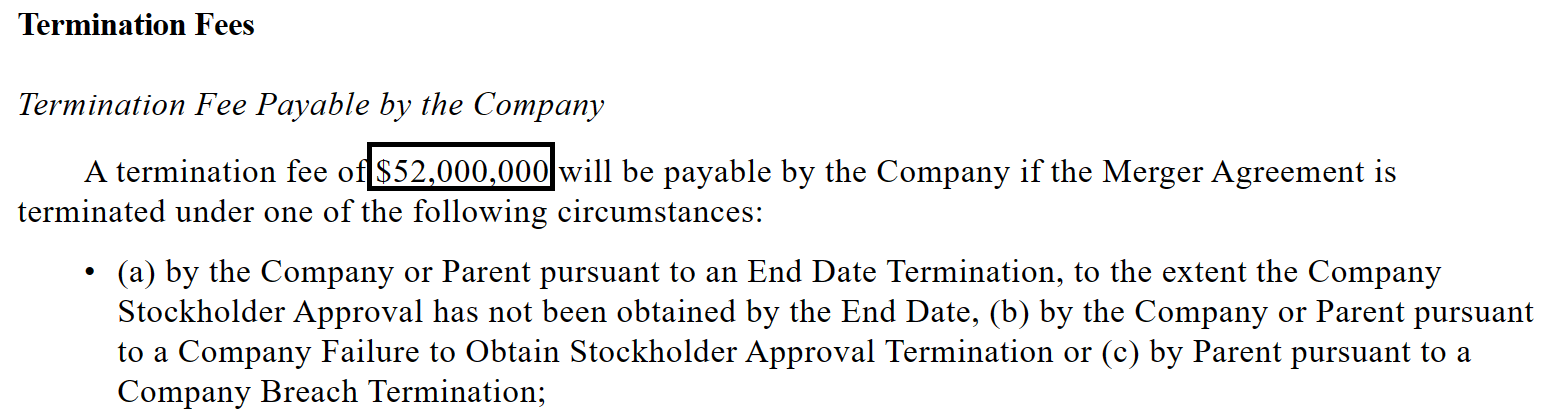

I Dislike The Termination Fees

Radius may have to pay a termination fee of $52 million, which represents close to 1.89% of the total enterprise value. The termination fee could be a bit more significant. It is not ideal.

{kind=link}

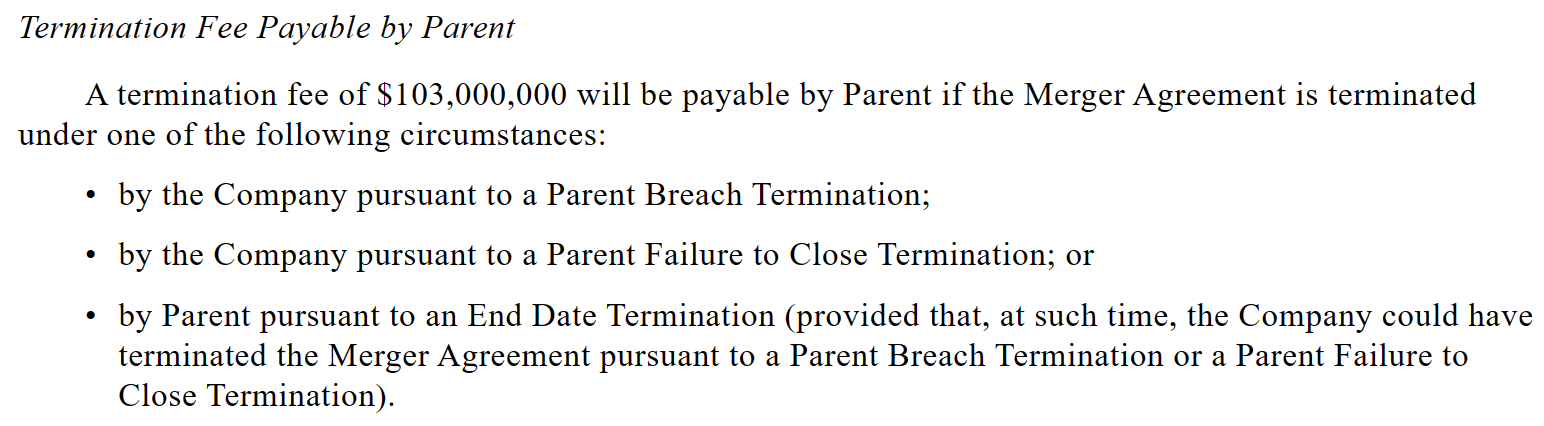

The buyer may have to pay a total of $103 million, which is close to 3.7%. I believe that the termination fee is not that significant here either. Some investors may believe that the deal is a bit less likely to close because of these termination fees.

{kind=link}

Risks

If the merger does not close, I believe that the stock may fall to around $11-$13 per share, so investors could lose more than 20% of the total amount invested. There are many events that could trigger a failure, including the precedent conditions, worsening macroeconomic conditions, or force majeure events.

Radius Global expects to close the deal around the third quarter of 2023. With the merger spread close to 1.5%, I believe that we are talking about an annualized spread of close to 6%, which I think is too small. In my opinion, I would be waiting to find a spread closer to 8%-9% because the risk is not small. In sum, if you are buying the company only to wait for the merger, I believe that the spread is not adequate. In my view, Radius Global Infrastructure looks more like a stock that we want to hold for a long time, even if the merger does not close.

There is no assurance that the companies will obtain all the due approvals in that period of time. In my view, the Foreign Investment Approvals condition may take longer than expected. If traders do not wait for a long time, they may sell their shares before the merger closes. As a result, I believe that the stock price may decline, lower than the current price mark.

While it is currently expected that the Mergers will close on or around the third quarter of 2023, there can be no assurance that all required approvals will be obtained or that all closing conditions will otherwise be satisfied (or waived, if applicable), and, if all required approvals are obtained and all closing conditions are satisfied (or waived, if applicable), we can provide no assurance as to the terms, conditions and timing of such approvals or that the Mergers will be completed in a timely manner or at all. Many of the conditions to completion of the Mergers are not within our or Parent's control, and we cannot predict when or if these conditions will be satisfied (or waived, as applicable). Source: 10-k

The total amount of debt reported is significant. In my view, if credit markets worsen, or the ability to repay financial obligations deteriorates, I believe that investors may sell their stakes. As a result, I believe that we may see a decline in the stock price even before the company makes any announcement with respect to these matters. Management made the following commentary in this regard.

As of December 31, 2022 and 2021, we had total outstanding indebtedness of $1,536.4 million and $1,295.5 million, respectively. Our ability to make scheduled payments or refinance our obligations depends on our financial condition and operating performance, which are subject to prevailing economic and competitive conditions and to certain financial, business, legislative, regulatory and other factors beyond our control. Source: 10-k

Conclusion

With an impressive recent increase in capex acquisition growth and annualized in-place rents growth, Radius Global Infrastructure also reported properties that offer high barriers to entry. For all these reasons and the easy predictability of future free cash flow, I believe that under different macroeconomic conditions, the company could be worth much more than $15 per share. It is a pity that the Board of Directors had to sell at that price because other bidders offered close to $20 per share before the macroeconomic expectations deteriorated in 2022. With this in mind, in my view, shareholders will do good by keeping the shares until the merger closes. New stock buyers willing to make dollars from the merger transaction may want to wait a bit more to find larger spreads. I do not believe that the current spread successfully shows all the deal risk.

For further details see:

Radius Global Infrastructure: Although The Merger Agreement Is Risky, It Looks Undervalued