AMT - Radius Global: Shares Surge On Renewed Hopes For Takeover

Summary

- Shares of Radius Global Infrastructure surged 16% on Monday as reports of a potential takeover surfaced.

- I see an acquisition of Radius Global as being likely in the next 6-9 months as the company requires additional capital to continue its tower site rollup strategy.

- Selling a portion of its site lease portfolio and/or pivoting to an acquire, bundle, and sell strategy is a possible alternative to an outright sale of the company.

- The rumored $14/share sale price implies a 5.3% cap rate for the portfolio with no credit given to Radius' valuable acquisition platform.

- I see significant upside potential (50%-plus) for shareholders if the company is able to craft a creative solution to monetize some or all of its existing portfolio while retaining its origination platform.

Shares of Radius Global Infrastructure ( RADI ) have risen 62% since my October article highlighting the company's significant undervaluation including yesterday's 16% surge in the wake o f renewed reports of a potential takeover surfaced . T his follows reports of a potential deal in late January.

In today's article I will discuss the reason why Radius is seeking a strategic alternative, evaluate the proposed $14+/share rumored purchase price, and discuss potential alternatives to an outright sale of the company.

Why I view a sale of Radius Global as Being Likely

In my previous article, I highlighted the investment merits of Radius Global which include durable contractual cash flow from creditworthy tenants, a value accretive cell tower site rollup strategy, and a very attractive valuation.

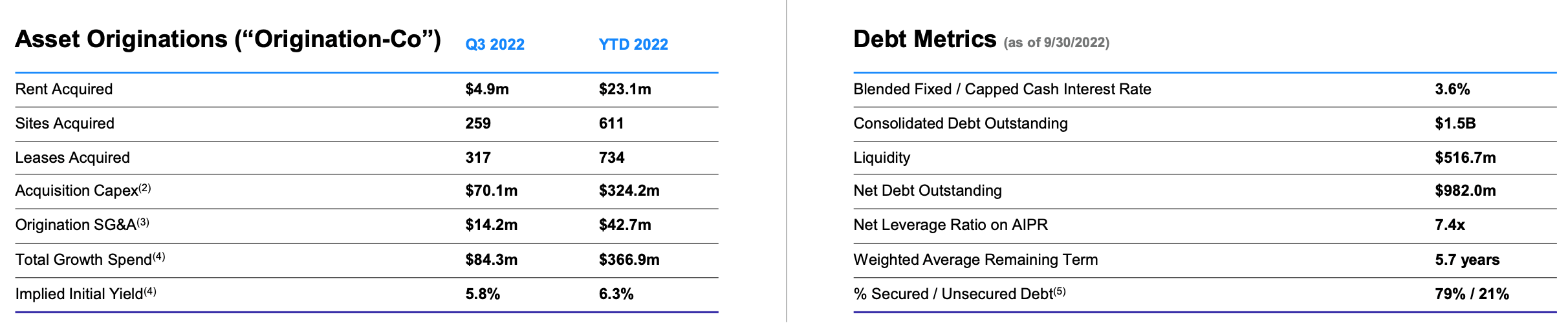

Given the strong operational performance and continued successful execution of its rollup strategy, a reader might wonder why Radius would entertain a sale, particularly given that bidders are unlikely to offer a 'knock out' as acquisition financing costs have surged with interest rates. While the company is doing a fine job of executing, as it has continued to acquire additional cell tower sites, it's liquidity (source of tower site purchase funding) has dwindled to about $500 million at the end the third quarter (and is likely around $400 million following fourth quarter cell tower site originations). While $400 million may sound like a lot, Radius has been making purchasing tower sites at a pace of ~$110 million per quarter as shown below.

{kind=link}

Radius Acquisition Pace & Liquidity (3Q22 Supplemental Report)

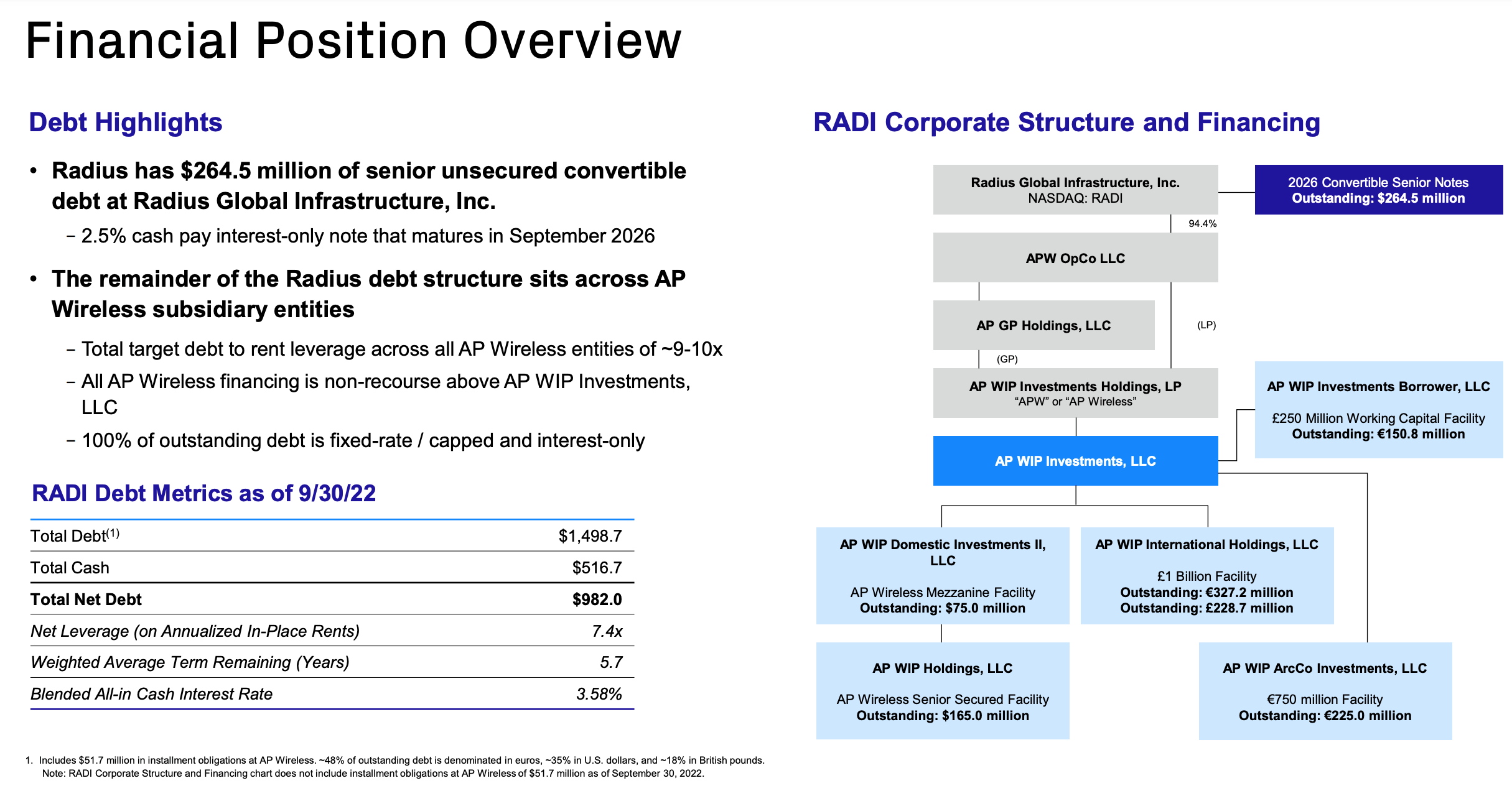

The rise in interest rates and decline in Radius' share price over the past 15 months have increased the company's cost of funding. As such, once Radius utilizes its remaining ~$400 million of existing funding capacity it will have to access capital markets at much less favorable terms than when its existing funding sources were put into place. Note that Radius' current debt structure (with a weighted cost of debt of just 3.7% as shown below) was put into place during the ultra-low interest rate conditions of 2020-2021.

{kind=link}

Radius Financial Position (3Q22 Supplemental Report)

Were Radius to raise debt today to fund additional tower site purchases, it's safe to say that the cost of financing would be much less attractive (likely 7.5%+ in today's market) than its current cost of debt. Similarly, with its shares having traded in the $11-12 (prior to yesterday's bounce) range, Radius' cost of equity financing is relatively unattractive (implied cap rate of 6%). With new site originations a cash cap rate of ~7% his higher cost of capital limits the NAV accretion from further site originations. This is the source of Radius's present dilemma which has caused the company to explore strategic alternatives.

Are there any alternatives to a sale of the company?

I see a couple of alternatives to an outright sale of the company, including:

- Continue status quo and hope cost of capital falls. As discussed above, once Radius exhausts its existing liquidity (within 12 months), at the expected current cost of capital, this would result in minimal NAV accretion to Radius shareholders from site originations. The hope in following this course of action would be that Radius stock rebounds/cost of new debt declines in the future (which would lead to NAV accretion from site originations).

- Sell a portion of its existing site lease portfolio to fund new site originations. Beyond private equity firms like EQT (rumored bidder), I believe that Radius' largest tenants, cell tower REITs American Tower ( AMT ) and SBA ( SBAC ), are natural acquirers for Radius' cell tower sites (would reduce the rent burden borne by these REITs). These REITs currently trade at implied cap rates of 4.5-5.3%, implying they could fund site purchases in an accretive manner and purchase Radius's sites in a win-win transaction.

- Similarly, Radius might be able to structure a "forward sale" type arrangement with cell tower REITs whereby they agree to purchase newly originated cell tower sites on an ongoing basis. This would relieve Radius from having to raise capital to fund site originations but allow Radius shareholders to capture value from its origination platform. I explore the potential value to shareholders from such an arrangement below.

Valuation

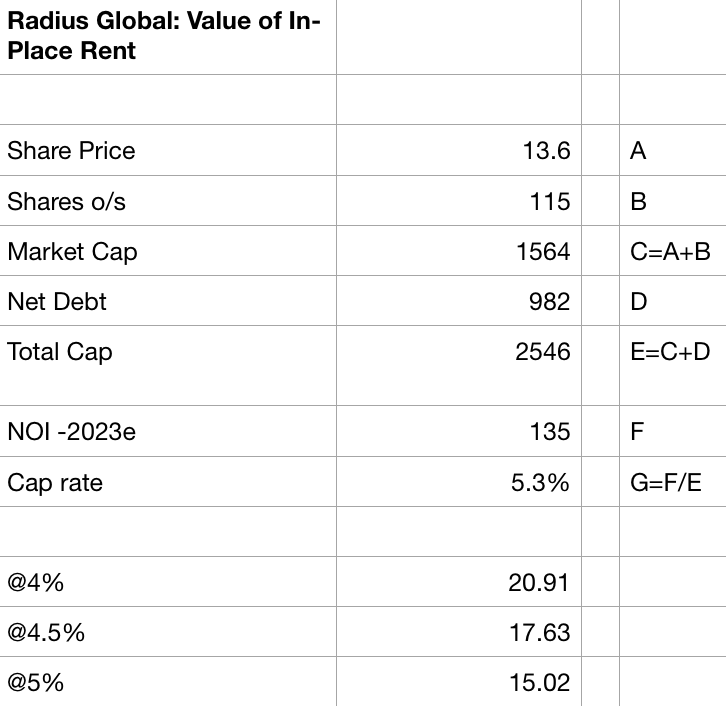

Below I show the implied cap rate at the current share price and some sensitivity analysis for Radius's existing portfolio of tower sites:

{kind=link}

Radius Global Implied Cap Rate & Sensitivity (Company Filings; Author Estimates)

The above valuation only gives credit for Radius's existing portfolio. The rumored sale price from yesterday's news was "greater than $14 per share." At $14-15 per share this works out to an implied cap rate of 5-5.3%. This compares to implied cap rates of 4.5-5.3% for the cell tower REITs. The 6-7 year publicly traded debt of the cell tower REITs is currently yielding 5.6-6.7%. Relative to tower debt, Radius has a senior claim (leases get paid before bondholders) and the debt has a fixed coupon payment whereas the cell tower site leases benefit from escalators at 3% (US leases) and CPI (international).

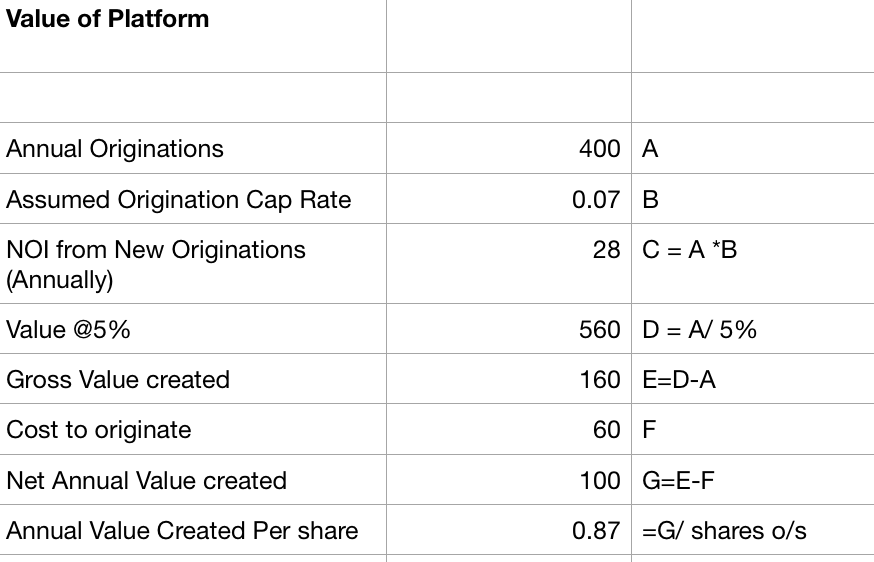

Below I show the potential annual value creation of Radius's site origination platform:

{kind=link}

Radius Platform Value Creation (Company Filings; Author Estimates)

The above analysis assumes that Radius is able to continue to originate (acquire tower sites from small owners) at 7% cash cap rates, that it's able to bundle (value is aggregation of hundreds/thousands done one by one) and sell these sites at a 5% cap rate. It incorporates the annualized cost of $60 million (Radius has several hundred people negotiating deals with small owners) to originate these sites.

At a multiple of 8-10x, this implies another $7-9 of potential value for Radius shareholders (on top of the $14-15/share for its existing portfolio). I see this as the value maximizing strategy for shareholders (as opposed to a near term sale at $14+).

Conclusion

One way or another, I expect we will see a strategic resolution announcement from Radius Global over the next 6-9 months. Should the company choose an outright sale (for whatever reason), I see little downside. I see significant upside potential (50%+) for shareholders if the company is able to craft a creative solution to monetize some or all of its existing portfolio while retaining its origination platform. As such, I continue to maintain a long position in Radius Global Infrastructure.

For further details see:

Radius Global: Shares Surge On Renewed Hopes For Takeover