RDUS - Radius Recycling: Holding After The Rebrand

2023-10-18 07:27:41 ET

Summary

- Radius Recycling has experienced management and a strong balance sheet, but there are risks related to commodity prices, the strength of the dollar, and potential impairments.

- Shares trading below $23 present a multi-year investment opportunity with a margin of safety and asymmetric upside potential of nearly $40.

- I anticipate RDUS to generate a normalized FCF of 1.50 to 2.3 dollars per share during up-cycle years.

Thesis

I rate Radius Recycling (RDUS) a hold due to short-term macroeconomic risk neutralizing the increase in demand for the low-carbon industry. I consider the risk of a global economic slowdown within the next 12 months high, increasing the chance that RDUS will have another set of bad quarters. The current share price of $26 does not reflect this risk.

On the other hand, shares trading below $23 paint a rosy picture for a multi-year investment. RDUS's rebrand, seasoned management, historical FCF consistency, low-cost debt, and secular tailwinds with the non-ferrous recycling upgrades. Given a tangible book value per share of $23.20 an entry at 23 dollars, provides a 2 to 3 dollar margin of safety with upside potential above $35.

Overview

Radius Recycling, formerly known as Schnitzer Steel, is a ferrous and non-ferrous metals processor. The Oregon-based company operates 4 segments across the US: metals recycling, auto-dismantling, steel manufacturing and recycling solutions. At the end of FY 2022, Radius operated 51 retail auto parts stores (Pick-n-Pull, etc.), 54 metal recycling facilities, and a single electric arc furnace ((EAF)) steel mill.

RDUS core business involves purchasing scrap metal, typically from used automobiles, shredding, separating, selling and/or remilling these scraps. The bulk of RDUS' revenue comes from the volumes of ferrous, non-ferrous and finished steel products multiplied by the price sold for each unit. Revenues are constrained by downstream recycled metal market prices, but can be partially offset by higher sales volumes on years with weak prices. RDUS' profitability is determined by spreads between scrap and recycled metals, putting particular emphasis on operating efficiencies. To this end, management focuses much of its efforts on acquiring scrap metal for as cheap as possible, typically through the acquisition of scrap yards and recycling centers, and tucking scrap assets into its network of operations.

Management

Radius Recycling has experienced management that should be considered upon investment. The firm's CEO Tamara Lundgren joined Schnitzer Steel in 2005 and has held the role of CEO since 2008. In addition to her long-time role as CEO, Lundgren also serves as the Chair of the Board of Directors of the Federal Reserve Bank of San Francisco and has held a seat on the President's Advisory Committee for Trade Policy and Negotiations under Presidents Obama and Trump. I would think she has some insights on the US economy that aid her business decisions as CEO. Lundgren owns about 913,000 shares, or 3.3% of common stock.

Radius' SVP Richard Peach and CFO Stefano Gaggini have been with the firm since 2007 and 2011, respectively, and together own about 200,000 shares of common stock. The average tenure of the eight members of executive management is 12 years. There has not been significant insider buying recently.

DCF Analysis

To establish a minimum intrinsic value, I conduct a 3 year DCF using conservative revenue estimates and a 6.5x EV/EBIT exit multiple.

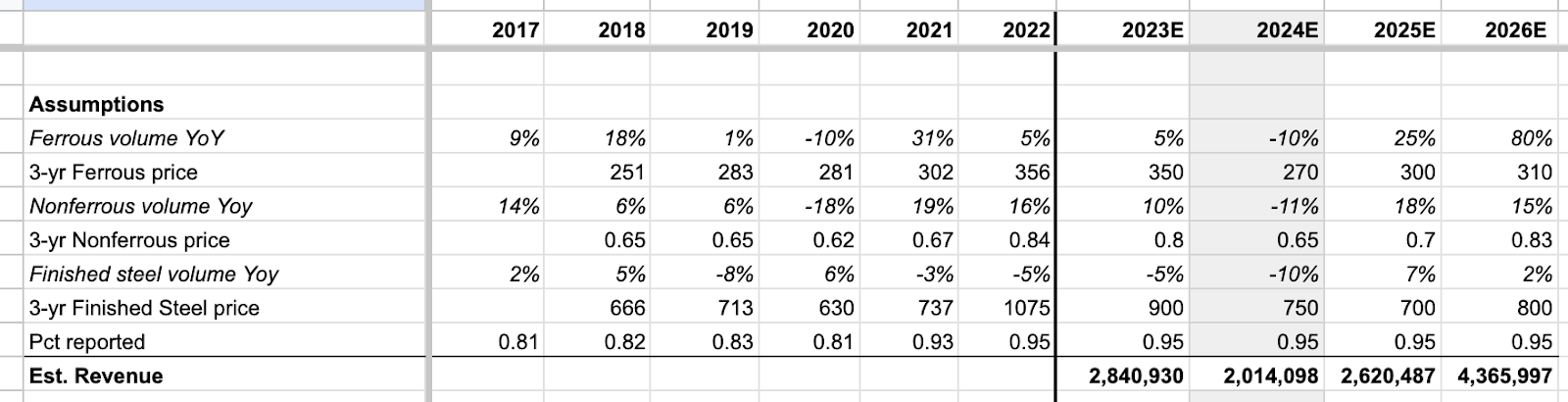

My revenue projections are presented below. I assume that prices for all products remain within the range of their three-year average. I include a modest recession in 2024, negatively impacting volumes and prices, that recover swiftly in 2025. I also assume that the revenue estimated from the model accounts for 95% of the revenue reported.

Revenue Estimates (SEC filings and company presentations) DCF with conservative revenue estimates (SEC filings and author's work)

{kind=link}

Although the current intrinsic value of RDUS stock is under 23 dollars a share, or a 14% decline from current prices, I suggest this to be a minimum estimate. The potential for long-term revenues could be much higher, depending on the strength of the dollar and demand for low-carbon steel and recycled metals feedstock.

Other Considerations

In eight of the last 10 years, RDUS has produced positive free cash flow. RDUS will not be FCF positive this year due to growth capex on new nonferrous recovery processes and an acquisition in the first quarter. I estimate normalized FCF to be between 40 and 60 million, or 1.5 to 2.3 dollars per share. At a target share price of 23 dollars, this implies a 10x to 15x FCF multiple, in line with historic multiples.

RDUS' balance sheet is strong and I believe several of RDUS deepwater assets are not properly reflected on its books. As of the most recent quarter, RDUS has 344 million outstanding debt with an average interest of 6 percent. There are no major debt maturities until 2027, when a 230 million credit facility will be due. On the asset side, Radius has a sufficiently diverse geography. Operations are focused on the Northeast and West coasts, and in the South. Radius also owns 6 deepwater ports in California, Hawaii, Oregon, Puerto Rico and Washington. With a tangible book value of about 23.20 per share, downside risk looks limited to 19 or 20 dollars per share.

Catalysts

The largest catalyst for Radius Recycling, of course, will be the attention given to the low-carbon economy. Radius has positioned itself to cover many low-carbon projects without taking on considerable risks or relying on cheap debt to fund green operations.

Radius CEO Tamara Lundgren has communicated this vision clearly on the second quarter conference call :

Decarbonization is a powerful structural driver of demand for recycled metals, which require less carbon to produce than mined metals. Many low-carbon technologies are widely acknowledged to be more metal-intensive. Maximizing the environmental benefits of decarbonization will require increasing use of recycled metals versus virgin materials.

With this in mind, the Company has been upgrading its non-ferrous recycling capabilities through 130 million in capex over the past three years. In the Q1 earnings call, CFO Gaggini expects non-ferrous volume recovery from shredding to increase by approximately 20%, which is not accounted for in my conservative estimates. CEO Lundgren announced that these impacts will be fully realized at the end of calendar 2023, or the first quarter of 2024:

One thing we expect to conclude this calendar year is the rollout of a multiyear capital program that's been focused on extracting more and more non-ferrous materials from the materials that we recycle. Take, for example, a car that we will recycle, it has ferrous metal, which is steel, and non-ferrous metal, which are things like copper and aluminum. We've been investing in technology and equipment that allow us to extract smaller and smaller pieces from what we recycle and then separate them into their intrinsic parts.

Nonferrous revenues account for less than a third of total sales; however, growth in the electrical and renewables markets is expected to lift and support demand for the foreseeable future. Looking beyond 2026, I think demand for copper, aluminum, nickel and other nonferrous scrap is obvious given electrification trends. Investing in enhanced nonferrous volumes is a strong managerial decision.

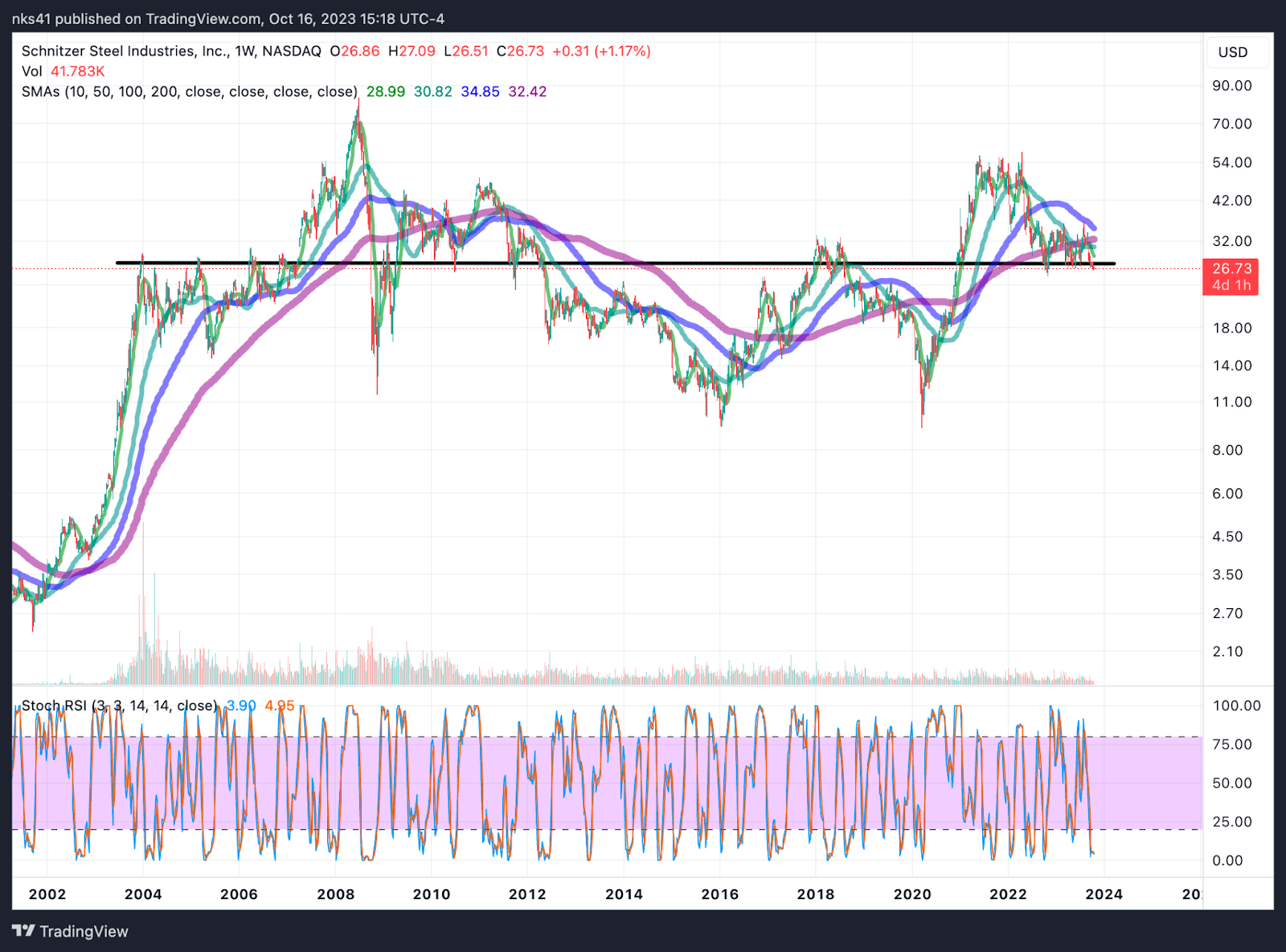

Technical Analysis

RDUS does not yet look oversold on a technical level, however, the stock is approaching a level of weekly support at around 27.00. With a 200-week average price of 32 Radius does not look deeply oversold. For reference, the stock declined over 50% from the 200-week average during periods of cycle bottoms in 2009, 2016 and 2020.

A multiyear weekly view RDUS (Tradingview)

{kind=link}

I would be hesitant to buy such a cyclical stock so close to a significant moving average, even if tailwinds in end markets are present. On a daily basis, RDUS looks range bound between 26 and 34. Maybe there is potential for a swing trade here, but for the long-term investor, a cost-basis of 26 is not worth the maximum rangebound price of 34, especially when the stock could decline around 40% if the economy falters in 2024.

Risks

There are four main risks to RDUS: commodity risk, dollar strength, fire and impairments, and higher American interest rates.

First and foremost, Radius does not have downstream pricing power on the sale of its recycled materials. Hence, operating margins compress during bad years when the prices of ferrous and nonferrous metals are low, even if scrap spreads are high.

Second, a continued strong dollar beyond 2025 will undermine sales volumes considerably. The majority of Radius sales volumes come from foreign destinations.

Third, some of its RDUS assets are risky. In recent news , a fire from the recycling yard in Oakland prompted the state of California to issue the company 2 air pollution violations. This news comes just after Schnitzer Steel announced a rebrand to Radius Recycling . Furthermore, in 2013 and 2015 the firm had major asset impairment charges from goodwill write downs, something to be cautious of moving forward.

Finally, RDUS is not debt free. Despite having historically responsible leverage ratios and low-cost debt, Radius will look to refinance before 2027 to cover about 250 million in maturities. Rate cuts will be beneficial to Radius and the overall American economy.

Conclusion

I like the focused business model of Radius. It operates as a major player in an industry that will withstand pandemics and geopolitical black swans. The company's management has weathered recessions and cycle bottoms and owns a significant amount of common shares. On a conservative basis, the stock does not look cheap, nor has it reached significant drawdowns from its 200-day weekly moving average. I would hesitate to own this stock above $26 knowing that recession risk in the next 12 months is elevated. Finally, I am waiting until there is heavy insider buying action from CEO Tamara Lundgren, who has bought consistently at market lows. At the next earnings call and full-year update, I will be looking for a material increase in the volume of nonferrous sales to confirm my view of management's capability.

For further details see:

Radius Recycling: Holding After The Rebrand