RDNT - RadNet: Growing Procedure Volumes - Significant Upside Potential

2023-07-17 00:36:24 ET

Summary

- RadNet has seen a 13.5% increase in capital appreciation due to growing procedure volumes and overall profitability, with the position up 50.6% since August 2022.

- RDNT's Q1 FY'23 showed attractive growth percentages in imaging volumes, with double-digit gains across the board.

- Net-net, reiterate buy, still eyeing $40/share, a potential 30% upside.

Investment updates

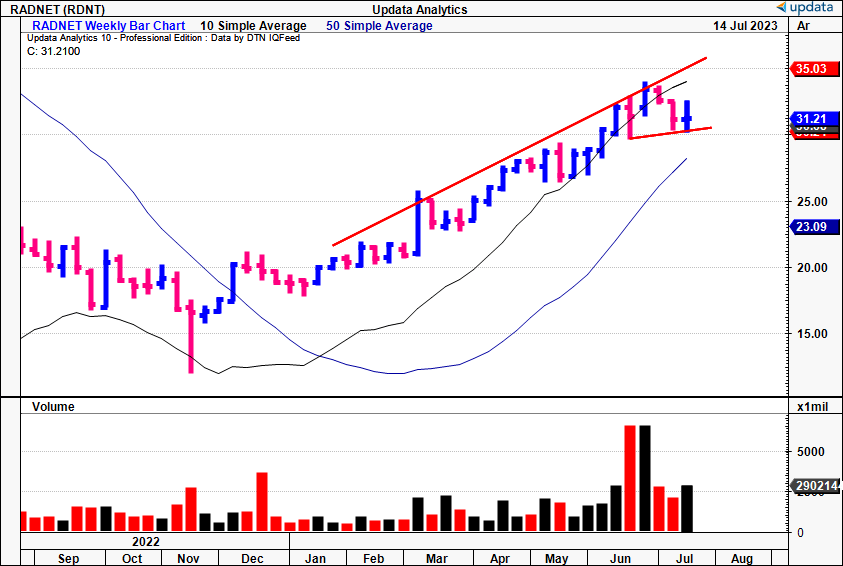

Following my April publication on RadNet, Inc. ( RDNT ) investors have been rewarded with another 13.5% in capital appreciation thanks to the company's efforts in growing procedure volumes, de novo centres, and overall profitability. Since the original buy thesis posted in August 2022, the position is up 50.6% in the money as I write.

Now with the company's latest numbers in hand, there are a number up critical updates to the investment debate that are worthy of discussion. Here I'll run through how RDNT now qualifies as a legitimate growth company, growing the core drivers of its business, thus creating immense value for shareholders downstream. Chiefly, these changes centre around fundamental and valuation forecasts, however, I'd also point out that sentiment is positive as well. For example, with reference to options-generated data , those with actual money at risk in RDNT are looking to a price change to $35 at least by August and September (note, these are for calls currently in the money, with contracts of August and September expiry).

Net-net, on earnings power and asset factors, RDNT is chugging along just where it needs to be in order to drive further equity value this year, based on my analysis. Reiterate buy, still eyeing $40/share as the next price objective, another 30% upside on today's market value.

Figure 1. RDNT rally since October '22

{kind=link}

Critical investment facts for discussion

After a strong set of numbers last month, we were privileged to see the company's earnings power and asset factors in full-force. In particular, sales and profit growth are the result of additional volumes (demand) of all services, versus purely price increases related to the same. This tells me RDNT's capital budgeting strategies laid out midway through FY'22 is starting to come to fruition. To illustrate the point here, consider the following facts.

1. Growth in imaging volumes

RDNT produced very attractive growth percentages in imaging volumes in Q1 FY'23.

MRI volumes were up 16.7% YoY, CT volume by 16.8%, and PET/CT procedures 20.9%.

Overall volume increased by 14% over the prior year when considering routine imaging exams- including X-ray, ultrasound, mammography, and others. You can thank heightened demand for imaging services for the tidy increases. The reasons for this are twofold:

- For one, there's been enormous medical breakthroughs in the treatment of complex disease segments in recent periods, in areas such as haematological cancers, non-alcoholic fatty liver disease ("NASH"), and, in particular, Alzheimer's Disease ("AD"). Eisai Co.'s ( ESALF ) Leqembi label recently obtained full FDA approval for the treatment of AD, for instance, (check out my deep dive of the approval here ). As a result of said breakthroughs, there will be a much higher indication for referral for imaging, knowing there is an effective, safe, and affordable treatment option within these kind of domains.

- Secondly, with the pandemic now fully behind us, we are back at a pace of patient turnover in healthcare systems that permits the routine growth in imaging to steer back on its longer-term trends.

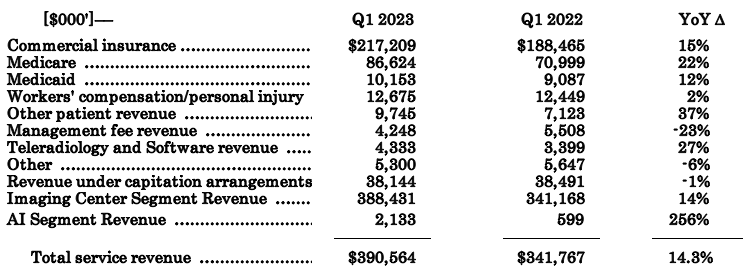

2. Respective growth across entire spectrum of top-line

First-quarter sales clearly demonstrated the momentum RDNT is building across the board. The firm has multiple sources of value feeding into its top line, and the distribution of revenue is spread well amongst these from a risk perspective [Figure 2].

With respect to the figures, observe the following:

- RDNT clipped Q1 sales of $388.4mm from its Imaging Center reporting segment, as mentioned, but it also saw reasonable growth in Teleradiology sales and from commercial insurance channels. Both were up 27% and 15% YoY, respectively.

- Most intriguingly, the artificial intelligence business [discussed later] came in with $2.1mm in quarterly revenues.

- Additionally, adjusted EBITDA, excluding losses from the AI reporting segment, reached $52.7mm, representing a YoY increase of 26.2%. Including the AI reporting segment, revenue amounted to $390.6mm, a 14.3% increase from the previous year's first quarter. Adjusted EBITDA for the first quarter of 2023 stood at $48.2mm, compared to $38.1mm in the prior year's first quarter.

In light of the above points, I'd also point out the one-time items that stood out during the quarter. These included 1) a non-cash loss from its interest rate hedging activity, as the unrealized loss on its interest rate swaps came to $4.1mm, 2) an expense of ~$960K related to leases for its de novo facilities presently under construction [thus, no revenues to offset this], and 3) a net of $7.6mm related to losses in its AI division.

Figure 2.

{kind=link}

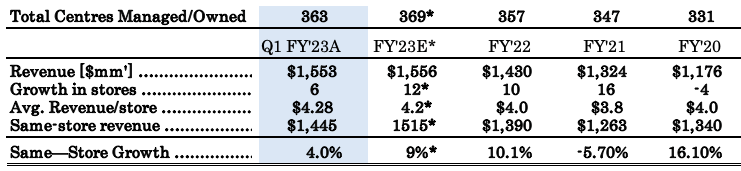

3. Compounding sales from incremental capital commitments

In the last publication, I performed an extensive analysis comparing RDNT's same-store growth averages [see: last RDNT analysis, see: " Fig. 3" , and "Fig. 4" ]. I've carried this through onto the Q1 results, and annualized the data to check where RDNT is in respect to the previous forecasts, which built a $36 valuation for the coming 12 months.

You can see in Figure 3 that RDNT is fact on the right track:

- It held 363 stores under its books (either owned or managed) at Q1, 6 more than at the end of FY'22. I had called for 12 openings this year, in line with management's language, and so it's pleasing to see the company already halfway there, whilst only 25% of the way through the year.

- Q1 revenues annualized to $1.553Bn, a shade off the $1.556Bn I'd projected for FY'23 in April.

- Same-store growth is roughly half of where I want it to be by the end of the year at 4% vs. 9%.

- Average revenue per store is also in line at $4.2mm, versus $4mmend of last year.

Based on this analysis, these forecasts may need a revision if the company pulls in with an outperformance within its Q2 numbers. Already it has completed many of the required tasks to get to a $39 valuation, therefore, this will need scrutiny a bit later on.

I'd also point out same-store volumes of MRI, CT and PET/CT's were up 12%, 10.6% and 20.5% respectively. You can really start to see the ball rolling for RDNT based on all this data, in my view.

Figure 3.

Note: All figures for "FY'23E" were estimated in the April publication. All figures for "Q1 FY'23A" have been annualized for a common-size analysis. (Data: Author, RDNT 10-Q's)

{kind=link}

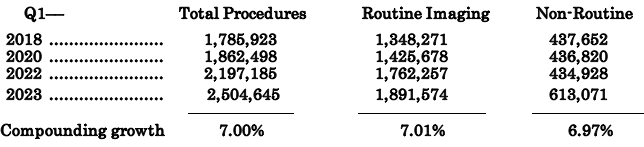

4. Procedural volumes ratcheting higher as well

All of the above would be in vain if the procedure volumes weren't there to back things up. Looking specifically to the quarter, procedure numbers are attractive. It grew total procedures 14% YoY -more than double its 5-year compounding rate- with c.17% growth in MRIs and CTs, and ~21% expansion in PET/CTs. In the first quarter of 2023, RDNT conducted an impressive 2,504,635 procedures. Notably, >75% of all work performed by volume adhered the multimodality approach that emphasizes routine imaging.

Figure 4.

Data: Author, RDNT 10-Q's

The above data doesn't portray the expansion efforts over time, however. Note below [Figure 5], that RNDT has compounded procedure volumes across the board by an average 7% per year since 2018, completing an additional 718,722 total procedures over this time. These numbers have generated an additional $4.36Bn in revenues, and additional $763mm in pre-tax earnings. As mentioned earlier, Q1 FY'23 procedures grew more than double the 5-year average. This tells me RDNT is poised for an exceptional period of growth moving forwards, thus supporting the buy thesis.

Figure 5.

{kind=link}

This forms one of the central tenets of my investment thesis here. As mentioned, there's no business growth for RDNT without the procedural growth. You could sum the firm's value-added equation as: Growth = Growth in same-store procedures + de novo facilities + additional procedures. In that vein, the flywheel is well in motion for RDNT in my firm estimation.

5. Strategic initiatives and future growth

As mentioned a littler earlier, RDNT has taken a strategic route in establishing an artificial intelligence ("AI") division. It's incorporated AI technology into imaging studies, as a recognition tool to reduce inter-reliability issues amongst imaging specialists. In particular, it hopes to enhance interpretations of breast, lung, and prostate images. This isn't the first mark of AI into helping specialists interpret medical studies. It has been incorporated into cardiology and ECG studies for a few years now with excellent confidence, and the diabetes crowd has also benefitted immensely from the regulation of blood sugars and so on. The AI division is led by DeepHealth, and incorporates the acquisitions of Aidence Holding BV and Quantib B.V. made in recent periods. I'd note RDNT copped some flack for both these transactions, but they look to be finally pulling through in the right steed in my view.

In addition to the points on procedural growth earlier, it's equally important for RDNT to push ahead with its de novo facilities. It needs this, in order to:

(a). Place additional imaging equipment

(b). For additional patient capacity

Both measures revert back to the key metric- procedural growth. Hence the growth ecosystem for RDNT is a symbiotic one between existing and new facilities, each driving imaging growth.

To this point, note the following:

- It has 13 de novo facilities currently under development. They are expected to commence operations in the H2 of 2023 and throughout 2024.

- These facilities are strategically located in markets with patient backlogs and capacity shortfalls. This strategy addresses the need for access points for both patients and physicians.

- Exactly 121 of the company's 363 centres, accounting for 33% of the total, operate within health system partnerships. RDNT's partners include reputable institutions such as RWJBarnabas, MemorialCare, Dignity Health, Lifebridge, University of Maryland Medical System, Adventist, Cedars-Sinai, and others. The more partnerships on board = the more referrals = more imaging. It is as simple as that.

Finally, the continuous evolution and improvement of technology in diagnostic imaging have expanded indications for ordering imaging procedures in the first place. I touched on this earlier with specific conditions like AD. But it actually extends further than this. Things like shortened scan times (hence higher patient flow) and improved image quality through software, and now AI, have also played a pivotal role. The integration of tech and advancements in the ancillary factors of imaging are also factors as to why I am bullish on RDNT.

Valuation

Investors aren't parting with their RDNT stock with ease, selling the stock to you at ~43 forward EBITDA and 5.5x book value, but just 11x cash flows. On face value, these might seem expensive. But I'd urge you to consider the following points in the discussion as well.

One, that RDNT trades at 5.5x its net asset value simply tells me the company has generated $5.50 for every $1 in equity value over its time. That is tremendously attractive, and tells me the market values the company's net assets very highly, important to the buy thesis here because for RDNT- the capital produces the profits.

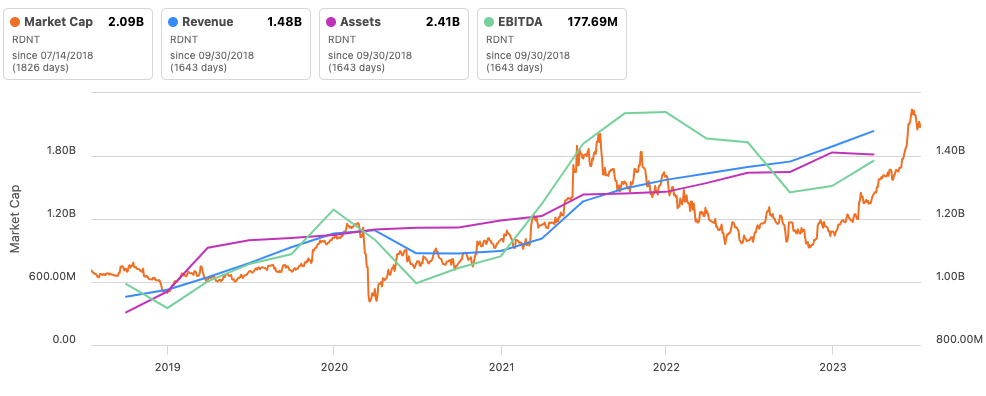

Two, the market looks to have been valuing RDNT on factors of earnings power, rather than asset factors or sales, as seen in Figure 6. Again, this is unsurprising, seeing as the model RDNT employs is one of capital placements, to produce earnings on said capital (earnings are defined here as net income plus depreciation and amortization). In that vein, it should be no surprise to see its market value stretch higher with the recent uptick in earnings since H2 FY'22.

Figure 6.

{kind=link}

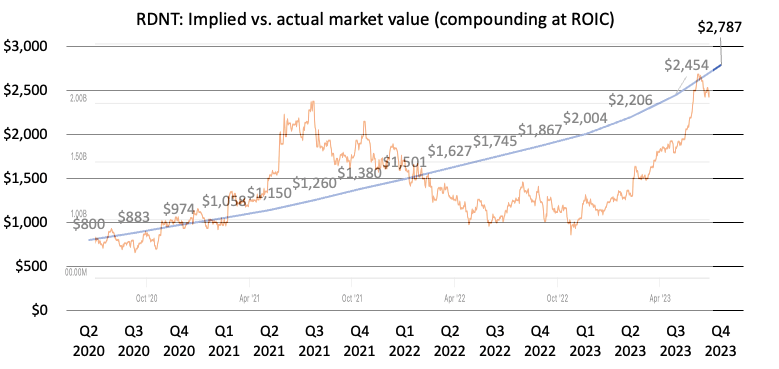

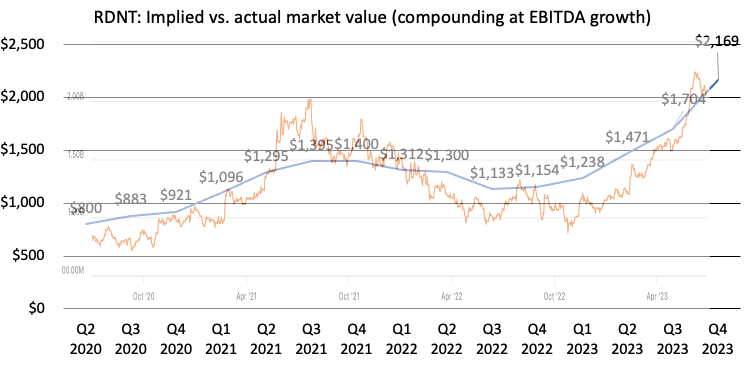

Three, based on the logic from above, I've built out two implied market valuation models, noted in Figure 7 and Figure 8. Recall, a firm can compound its intrinsic value at the function of the returns on invested capital, and the amount of earnings it reinvests at these rates. RDNT is high on both.

The first model looks at an implied value compounding at the firm's periodic ROIC; the second, at the sequential growth in earnings. You'll note two things from this:

- RDNT converged to the implied fair value in both instances, after displaying "overvalued" characteristics from Q1 FY'20-'22 (remember what else happened during that time though? Only the most spectacular bull-run in market history. So this wasn't out of the norm).

- If the implied value is a leading indicator, as it seems to be -the market is discounting projected earnings, and compounding RNDT's cap at the forward ROIC each period- then we have more room to run here. Based on my forward estimates [outlined in the last RDNT publication, see: "Appendix 1: RDNT 5-year P&L forecasts ], then both models point to $2.1-$2.7Bn in implied market value by the end of this year, getting me to $32-$40 per share, in line with my previous estimates of fair value.

Hence, each of these points on valuation are supportive of the buy thesis in my opinion.

Figure 7.

- Note: The image is comprised with the implied valuation line superimposed onto the market capitalization of the firm over the testing period. The market cap line is retrieved from Seeking Alpha , the former is constructed by the author. This is the reason for the slightly blurred image.

{kind=link}

Figure 8.

- Note: As above.

{kind=link}

Discussion

In the two most recently published deep dives on the investment debate for RDNT -one in April, and what's presented here- I outlined the bullish features comprising the investment thesis. Chief among these are the growth in procedural volumes, capital investments, same-store sales growth, and underlying market trends. There are obvious risks based on these. RDNT could fall short on same-store growth, procedures could roll right off, and capital charges for its facility expansions could blow right out. This wouldn't be ideal.

However, you've got to think in terms of combinations and permutations. What's likely to happen, and how likely is it to happen. Question yourself- is RDNT likely to slow down on procedures, and, how certain would that be? In my estimation -based on the data, mind you- the bounce of probabilities favours those long of RDNT stock. Management have proven to date that its strategy is fruitful, and aligns with the end market's needs. Further, we've got new conditions that need to be screened, imaged, and processed, and with the momentum some companies are building in these complex disease segments, there is all chance these trends will even increase into the future.

In that vein, RDNT has potential to compound earnings at 15-20% each year into FY'25, factors I discussed last time and carry through into the present analysis. It also just raised another $225mm at $29.50/share to pay down $100mm in debt, thus freeing up cash flow, and providing additional working capital. Recall, changes in working capital underline the difference between earnings and cash flow- and the more cash RDNT can free up, the more it can reinvest into new facilities and equipment, thus promoting further procedural growth. Win-win, in that regard.

Hence, when you put it all together, I am retaining the buy rating on RDNT, still eyeing the $40 target as my next objective. I look forward to the company's Q2 numbers, where I am preliminarily estimating that we'll have to update our models to accommodate the firm's momentum in sales and earnings. Net-net, retain buy.

For further details see:

RadNet: Growing Procedure Volumes - Significant Upside Potential