RDNT - RadNet Stock: Bullish With Several Growth Tailwinds For Diagnostic Imaging

2023-10-04 16:45:44 ET

Summary

- RadNet is capturing a strong demand for diagnostic imaging which benefits from several secular growth trends.

- The approval of new Alzheimer's drugs represents a growth driver given the requirement of an amyloid PET scan in the initial treatment assessment.

- We are bullish on the stock and see room for shares to climb higher.

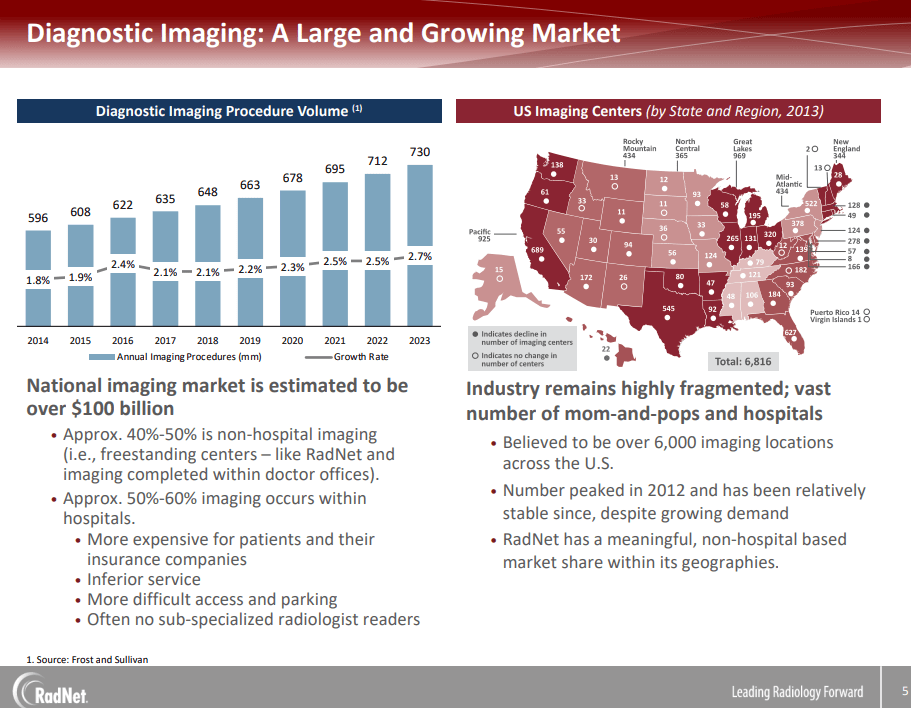

RadNet ( RDNT ) operates one of the largest networks of medical imaging diagnostics centers with 363 locations in the U.S. The attraction here is the recognition that radiology solutions represent a growing market amid an aging population alongside a trend of more preventative screening in healthcare.

Indeed, shares of RDNT have outperformed over the last several years, including an impressive 50% return year-to-date. Part of the momentum in 2023 includes enthusiasm with the approval of "Leqembi" as a first-of-its-kind Alzheimer's drug from Biogen Inc. ( BIIB ) and Japan-based Eisai Co., Ltd. ( ESAIY ).

The idea here is that treatment requires an amyloid PET scan or MRI as a new growth driver for RadNet imaging services. Separately, the company is also incorporating artificial intelligence to detect anomalies seen as transforming the industry.

There's a lot to like about RDNT as a high-quality small-cap, segment leader with overall solid fundamentals. The company beat estimates in the last reported quarter with management offering positive guidance for the rest of the year. We expect shares to trade higher going forward.

RDNT Financials Recap

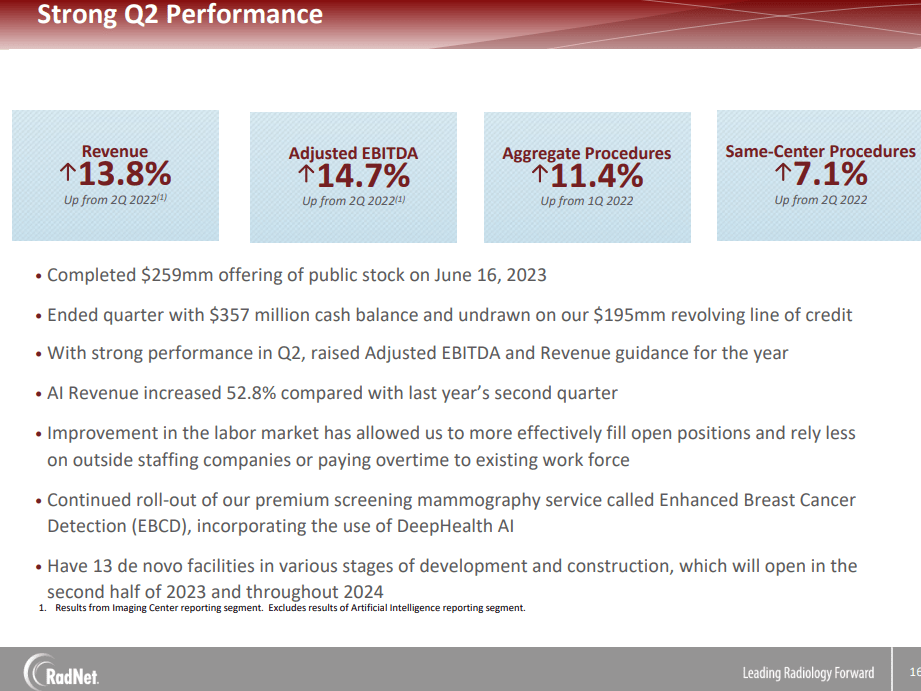

RDNT last reported its Q2 earnings back in early August with EPS of $0.24, up from $0.15 in the period last year, coming in well above the $0.10 estimate. Revenue of $404 million, climbed by 14% year-over-year and was also ahead of the consensus.

Compared to a 7.1% increase in same-center procedures over the past year, the aggregate number of producers is up 11% y/y reflective of a heavy demand environmen t for the company.

{kind=link}

We mentioned AI solutions, revenues grew by 53% y/y in Q2 but keep in mind this segment still represents a small part of the business at less than 1% of the business. Management is confident that its potential is still in the early stages and largely untapped, with good customer feedback from the "Enhanced Breast Cancer Detection".

While the physical capacity of the machines has not been an issue for the company considering the ability to extend operating hours as necessary, one bottleneck in the system has been a shortage of qualified technicians in certain markets.

RadNet has responded by expanding the use of "remote operation command centers" allowing a technologist to operate more than one piece of equipment at a time. This was explained as also addressing the ability to manage new demand from an influx of PET scans required for Alzheimer's drug patients allowing for better management of existing resources. From the conference call :

So the initial PET CT, which is one of the key ways of detecting the presence of these amyloid plaques which is necessary to get these patients on to the newer therapies that have come out by some of these pharmaceutical companies, that could be a huge opportunity for diagnostic imaging and obviously, for us.

If we had -- if there were a flood of PET CT demand in relation to these Alzheimer's drugs, what we would do is to utilize our existing PET CT capacity. And each PCT, a busy PET-CT can be doing 13, 14, 15 scans a day. So we have a lot of PET-CT capacity in our existing installed base.

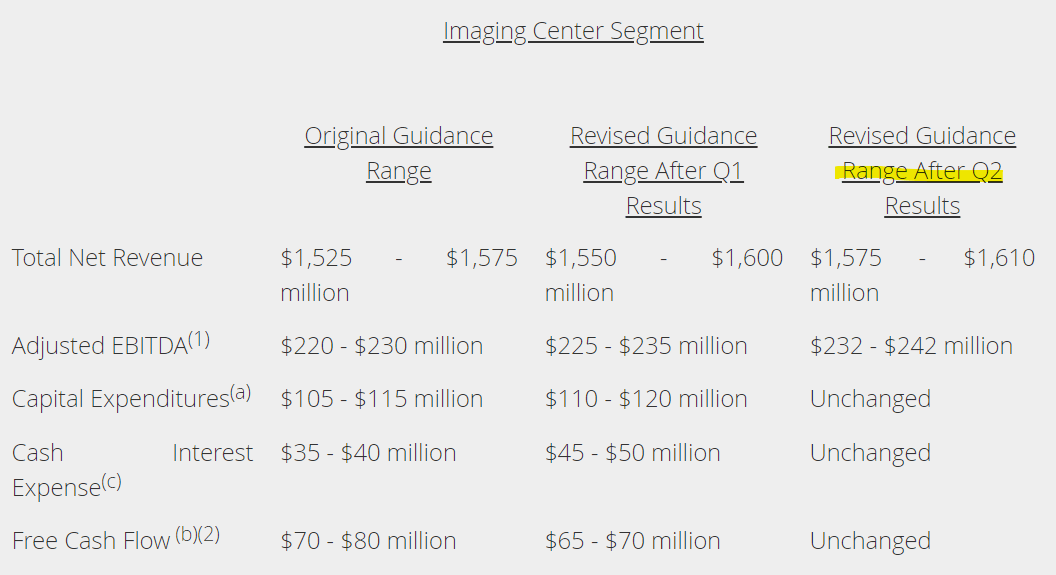

In terms of guidance, the company now expects full-year revenue between $1.58 billion and $1.61 billion, representing a 12% increase from 2022. Adjusted EBITDA is now seen at around $237 million as a midpoint estimate, compared to $209 million last year. Notably, this is the second revision higher to both revenue and EBITDA compared to the original guidance set back with the Q4 report back in February.

RadNet ended the quarter with $357 million in cash, against $848 in long-term debt. A net leverage ratio of around 2x is a strong point in the company's investment profile, in our opinion considering significant recurring free cash flows.

{kind=link}

What's Next For RadNet?

What we like about RadNet is its position in this large and growing market of diagnostic imaging. According to the company, the industry remains highly fragmented which opens the door for the company to continue consolidating with strategic acquisitions and market share gain. The expectation is that several trends support continued growth.

First, we mentioned the theme in healthcare with a growing focus on preventative non-invasive medicine and the effort to detect diseases earlier. Favorably, managed care and insurance providers are becoming more and more willing to move in this direction.

This includes Medicare which uses imaging two to three times more than with the younger population. Notably, Medicare and Medicaid together represent about 25% of total payers, highlighting the overall diversification including commercial insurance.

Finally, technological innovations have expanded the number of indications where diagnostic imaging tests are useful. Advances in MRI technology with the integration of post-processing software have added to the efficiency of the solutions.

{kind=link}

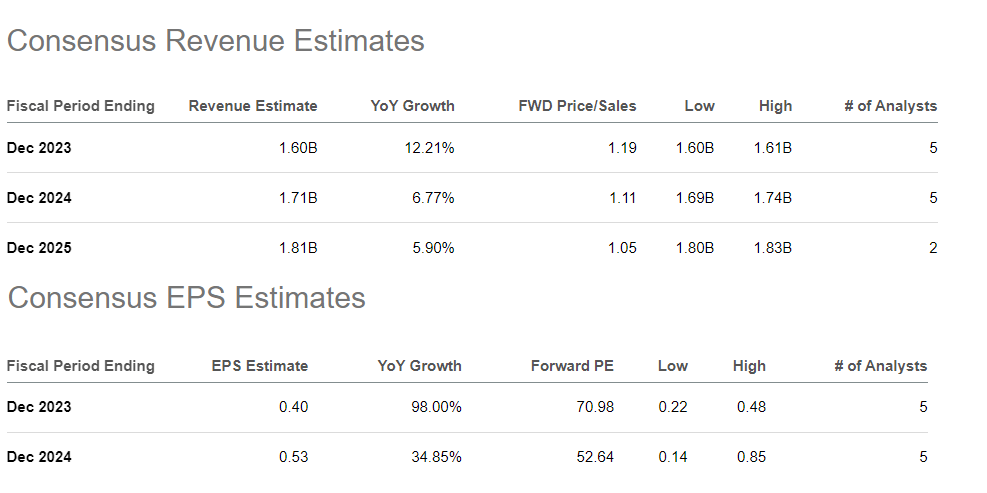

Overall, the outlook is positive for RDNT to generate shareholder value in our opinion. That being said, we can point out what is a currently lofty valuation. RDNT is currently trading at a forward P/E of 70x reflecting the market optimism for many of the themes we've covered.

The consensus expectation is for EPS to reach $0.40 this year, double from $0.20 in 2022. The momentum is forecast to continue with earnings climbing again by 35% towards $0.53 per share in 2024. This push narrows the earnings premium down to 53x on a 1-year forward basis.

Objectively, RadNet is an expensive stock but we believe that premium is justified considering the earnings momentum. The bullish case will need the company to continue outperforming expectations over the near term.

{kind=link}

Final Thoughts

We rate RDNT as a buy and see a path for shares to reclaim its recent high of $35.00 as a price target for the year ahead. This level implies a 66x multiple on the current 2024 consensus EPS, which is pricey, but justifiable given the company's unique positioning and long-term growth tailwinds.

The risk here is that this type of valuation multiple and RadNet's profile as a momentum stock opens the door for wide swings of volatility. The potential for disappointing results over the next few quarters, forcing a reset of earnings estimates lower, would result in a deeper downside for the stock. Monitoring points here include the trend in imaging procedures as a gauge of underlying operating conditions along with free cash flow levels.

{kind=link}

For further details see:

RadNet Stock: Bullish With Several Growth Tailwinds For Diagnostic Imaging