RAIFF - Raiffeisen Bank International: Strong 2022 Results Confirm Buy Recommendation

Summary

- This is an update to my article on Raiffeisen Bank International from the beginning of December. The bank published preliminary 2022 financial results on February 2.

- RBI is significantly engaged in Russia, but due to Russian regulations, RBI cannot access profits, nor easily exit the country completely.

- In December, I rated RBI a contrarian Buy.

- The Q4 and full year 2022 preliminary numbers have confirmed this view.

- One change is that a Russia exit has become more likely, which could be a positive trigger for a share price move.

Investment Thesis

In a Seeking Alpha article in December I recommended Raiffeisen Bank International (RAIFF) (RAIFY) as a contrarian Buy. The bank’s share price is depressed because of its significant exposure to Russia. My argument was that RBI is undervalued when the Russian business is discarded, and exceptionally undervalued when the Russian business is included in the valuation.

The bank announced preliminary 2022 and Q4 2022 results on February 1, based on unaudited numbers. The results were exceptionally good, guidance for 2023 was cautious though. The market reacted negatively and shares went down around 10 percent over the following days.

Still, I find my investment thesis confirmed.

One change is that a Russia exit has become more likely in my view, which could be a positive trigger for a share price move.

Financial results for 2022

Financial results for 2022 were very good. After the record results of the previous quarters, RBI also outperformed in Q4 2022 with an exceptionally strong quarterly profit of 826mn euro.

RBI Group including Russia and Belarus

Management made a point to report numbers in a dual way, the complete RBI group with Russia and Belarus included (abbreviated as RU/BY in the rest of the article), and also separately without RU/BY. Tellingly, management calls the latter one "core group".

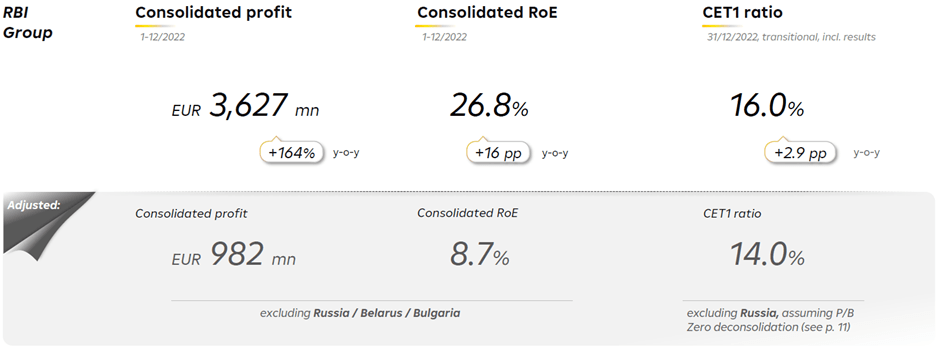

Here is a snapshot from the management presentation showing the key results on one page. While the bank did well across almost all its markets (Poland, which is in rundown mode, being the exception), the contribution from Russia is significant:

Key 2022 results for RBI group (with RU/BY) and without RU/BY (Source: Raiffeisen Bank International)

{kind=link}

As you can see, consolidated profit for the group increased 164% YoY to 3,627mn. This includes a one-time of 453mn gain from the sale of the Bulgarian subsidiary. Even without the one-time gain the YoY increase is an impressive 131%.

Net interest income increased by 52% and Net Fee and Commission Income by 95%.

While operating also expenses increased 19.3% YoY from 2,978mn to 3,552mn, this was significantly less than the increase on the top line, so the Cost Income Ratio stood at a very low 36.6%, down 17pp YoY.

Risk provisions rose to 949mn euro (490mn in RU/BY), up more than 221.7% YoY from 295mn in 2021. Additionally 262mn euro were provisioned for the CHF loan portfolio in Poland (which is in run-down mode). Overall, the NPL ratio was stable at a good 1.8%.

To sum up: really nice numbers. But there are some details to consider.

Business in Russia was exceptionally strong, but drivers are temporary

Fee and commission income growth in Russia was especially strong and income here increased more than 4x YoY.

Net fee commission and income in Russia ((Source: Raiffeisen Bank International)

{kind=link}

The reasons for this increase were the foreign exchange business and currency effects. We should not expect this to continue after the political situation has hopefully normalized over 2023 or 2024 (if it does so).

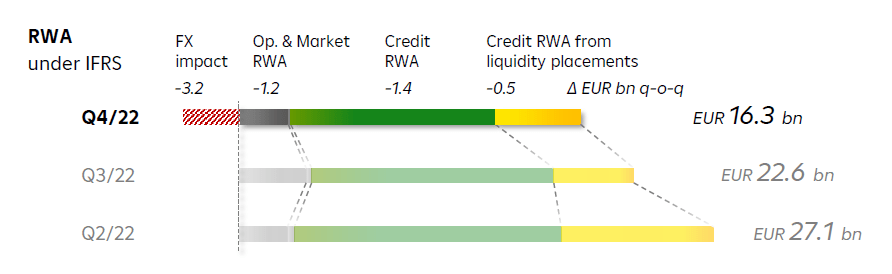

At the same time, RBI does no new business in Russia and RWAs in Russia decreased a further 6.3 bn in Q4 to 16.3bn, the main causes being reduced corporate business and the RUB depreciation. Loans to customers decreased by 30% YoY.

RWA development in Russia from Q2 to Q3 2023 (Source: Raiffeisen Bank International)

{kind=link}

The financial numbers in Russia are astounding when compared to a bank in a normal situation. CET1 ratio is 27.14% (19.14 pp above regulatory requirements) including the FY 2022 profit. The Liquidity Coverage ratio is 309%, 9.9bn above a 100% LCR. With a Loan/Deposit ratio of 45% the bank is also overfunded by its own deposits.

Profits in Russia are not accessible to the group

The profits in Russia are currently only of limited use for the group. Due to sanctions and regulations the bank has no access to the surpluses in Russia and dividends may not be distributed either.

Even if RBI cannot get the profits out of Russia, they improve the capital situation there tremendously. While the financials in Russia are generally out of the ordinary, one number stands out in my view: Raiffeisen Bank Russia has equity and capital of 4.5bn euro. This is not far away from the current 5.04bn euro market capitalisation of the whole RBI group.

Earnings and book value per share

On a group level earnings per share for 2022 are EUR 10.76, from EUR 3.89 in 2021. At the current share price this comes to a P/E ratio of 1.53. So RBI is cheap.

Book value per share stood at EUR 48.72 at the end of the year up from EUR 39.04 YoY, meaning the stock trades at a very low 0.34% of book value.

But we need to acknowledge again that a considerable part of that money is trapped in Russia (and to a lesser extent in Belarus). The bank has not changed its cautious approach and continues to say that it is evaluating all options, including a carefully managed exit without giving any specifics.

Results without RU/BY

Therefore, let’s have a look how the bank has been doing without RU/BY.

Consolidated profit without RU/BY was 1,435mn. This also includes the 453mn one-time gain from the sale of the Bulgarian subsidiary. Without the one-time gain consolidated profit was 982mn.

A look at the development of consolidated profit over the last 5 years shows two things. One, the profit development in Russia in 2022 was really extraordinary and cannot be expected to continue. Two, while Russia was always something like the cash cow of the group, RBI still managed to considerably increase profit outside of RU/BY. It is now not far off from the profit of the whole group in previous years.

RBI consolidated profit 2018-2022 (Source: Author based on RBI financial reports)

CET1 would still stand at 14% if the business in Russia were completely written off with zero value (I consider this quite unlikely). A 0.8 dividend per share is already considered here.

As announced last year, dividend decisions are being made considering the bank capital position without RU/BY. Management said that they will propose a dividend of EUR 0.8 per share for 2022. This is lower than expected and at the current share price gives a 5.2% yield.

Management also said that they do not expect the dividend decision to be made in the next Annual General Meeting in March, as is the usual practice, but later. A possible reason is a potential Russia exit. On the management call the CEO Strobl said that, if the Russian business was written off with zero value, there could be a temporary need for more capital above the 14% CET1 ratio.

2023 guidance

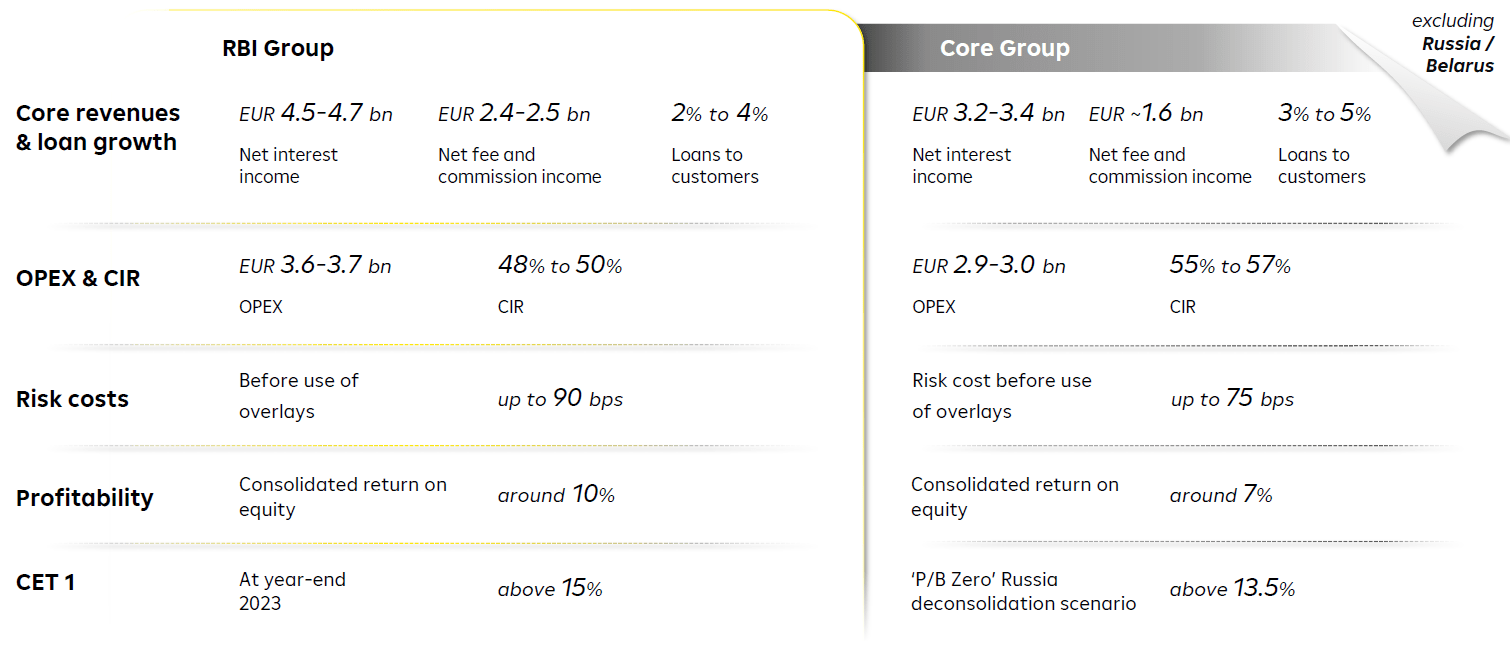

Management guidance for 2023 was somewhat muted.

RBI 2023 guidance (Source: Raiffeisen Bank International)

{kind=link}

I am just going to focus on the core group without RU/BY. Guidance is for Net Interest and Net Commission Income to be in line with 2022 or a few pp lower. Loans to customers are supposed to grow between 3% and 5%, also slowing down from the 6% in 2022.

To me those numbers look conservative and I think RBI management is overcautious, pointing to current uncertainties in Eastern Europe. For 2022 RBI management forecasted NII and NCI increases in the single digits, and even without RU/BY it turned out to be 37% for NII and 16% for NCI, so there is possibly an under-promise and over-deliver pattern here. Anyway, this is what they are saying and for the RBI share price over the next months it is probably less important than what happens with Russia.

How likely is a Russia exit?

A potential Russia exit was obviously front and center in the FY 2022 results presentation call.

The Management Board again left it open whether such a thing will happen, and if so, when. As in previous months, CEO Strobl said again that all options, including a complete exit, are currently being considered. He did not want to give a time horizon as to when a decision could be made.

Beginning of the year, Raiffeisen Bank International, like other Austrian companies, has come under pressure in Kyiv. Almost the entire board, including CEO Johann Strobl, was put on a list in Kyiv to be recommended for sanctions. The RBI is also currently accused of granting loan deferrals to Russian soldiers. RBI says it is required by law to do so.

On January 28 the Russian leasing subsidiary of Raiffeisen Bank International Russia has been put on a sanctions list by Ukraine. The same happened for 30 other Russian leasing companies, one of them the subsidiary of UniCredit (UNCFF). This means that leased goods from customers of Raiffeisen Leasing Russia can be confiscated if they are on Ukrainian territory. According to the bank, the volume financed by the leasing subsidiary was EUR 362mn at the end of December and no new leasing contracts had been concluded since the outbreak of war.

While there is practically no financial impact (obviously not many Russians are going to drive around Ukraine with leased vehicles), the market is nervous about this and RBI shares dropped almost 10 percent.

Given these pressures, it seems to me that a Russia exit is becoming more likely and the bank seems to be at least theoretically working on this. In the management call the CEO mentioned that the bank would see at least a 50 percent discount, if not more, when selling the Russian business.

If it happens, this would very likely be a significantly positive trigger for the share price – in my view. The market seems to attribute almost zero value to the Russian business currently. Given the amount of capital that has accumulated in Russia, even a large haircut means a significant upside from the current situation. So I think the bank will actively pursue this. An early exit, even with a haircut, is more likely now.

Risks

The risks to the investment thesis are unchanged since my last article, so please find more details there. The key risks are a deteriorating economic situation in Russia and adverse political decisions.

The most important risk to the thesis though is that the Ukraine conflict goes on without a resolution and RBI cannot find a buyer for the Russian subsidiary, leaving the situation of Raiffeisen Bank Russia undecided for a prolonged period of time. It is everybody’s best guess how and when the war will end. Bloomberg reported recently that Russia will be able to finance the war through existing Yuan reserves for two to three more years unless oil prices reduce significantly. This is probably the worst outcome for the share price: the situation drags on with constant bad press and RBI being unable to sell.

Conclusion

The key investment thesis is that the deterioration in RBI's share price due to the conflict in Ukraine is not supported by how well the bank is performing, resulting in a contrarian Buy opportunity.

I find that the thesis has been validated by the FY 2022 results.

Until the situation of the Russian subsidiary is resolved, the share price will probably stay depressed though, or at best move with the market (up or down). So, investors need to have a mid- to long-term view here to be rewarded.

For further details see:

Raiffeisen Bank International: Strong 2022 Results Confirm Buy Recommendation