RAIN - Rain Oncology: Multiple Data Catalysts In 2023 For This Precision Oncology Pioneer

Summary

- Shares have fallen by nearly 40% since 2021 IPO.

- Oral MDM2 inhibitor milademetan potentially has an efficient path to market via pivotal study in WD/DD LPS (rare cancer).

- Basket studies in MDM2-amplified tumors as well as patients with CDKN2A loss exponentially increase market opportunity.

- Bear thesis is that such studies take a LONG time to recruit and early-stage competitors like Kymera Therapeutics could more efficiently restore p53 versus inhibition.

- RAIN is a Buy. I see a pathway to value creation via 2023 readouts for pivotal study as well as a higher number of patients in basket trial.

**This article was originally published for ROTY Biotech Community subscribers on November 10th but has been updated where necessary. Despite the +68% gain since purchase, I continue to think there's room for further upside in 2023 and 2024 via progress in basket studies.

Shares of precision oncology upstart Rain Oncology (RAIN) have fallen by nearly 40% since its IPO was priced at $17 in 2021. Trailing twelve month gain is a more respectable +35%.

The company in-licensed its lead drug candidate RAIN-32/milademetan from Daiichi Sankyo in September 2020 for $5M upfront and remains on the hook for up to $200M+ in milestone payments along with high single digit royalty on annual net sales should they make it to market. At the time of IPO in 2021, I found the story interesting but too early-stage for my liking.

Flash forward to the present, where a few months ago they reported phase 2 interim data from an open-label basket study in MDM2-amplified advanced solid tumors has shown encouraging signs of activity. Namely, of 10 evaluable heavily pretreated patients (median 4 prior lines of therapy), there were two unconfirmed partial responses ((PR)) along with two patients continuing on therapy with tumor regressions of 29% and 27%, respectively.

Given these initial results coupled with a swiftly executed $50M private placement, I'm inclined to believe that my estimated EV of $240M is still discounted as clinical momentum continues to accelerate.

Chart

{kind=link}

Figure 1: RAIN weekly chart

When looking at charts, clarity often comes from taking a look at distinct time frames in order to determine important technical levels and get a feel for what's going on. In the weekly chart above, we can see shares fall from a high in the low $20s to bottoming out just above the $2 level (perhaps attributable to lack of material news flow). From there, the share price rebounded as high as $8 and consolidated in the mid-single digit range (where I purchased my initial position in November). Recently, the share price ran up as high as $14 before pulling back to the $10 level. My current take is that investors interested in this name could still purchase a pilot position ahead of data, then take further action based on strength of results and resulting reaction of the stock price.

Overview

Founded in 2017 with headquarters in California (44 employees), Rain Therapeutics currently sports enterprise value of ~$70M and a Q2 cash position of $105M providing them operational runway into mid-2024. Keep in mind estimated quarterly burn rate is $20M and recent $50M financing boosted their cash balance.

As mentioned prior, lead drug candidate milademetan is a small molecule, oral inhibitor of MDM2 and being developed for treating patients with MDM2-dependent cancers. In the past, MDM2 inhibition has been challenging due to dose-limiting, on-target hematologic toxicities leading to a narrow therapeutic window. The company's differentiated take includes optimizing the dosing schedule to improve peak drug exposure leading to apoptosis and cell cycle arrest during the dosing period, while permitting hematopoietic precursor cell recovery during the dosing break to minimize these toxicities. While one would think competitors would simply copy this approach, keep in mind that residual drug concentration (due to poor drug clearance or tissue accumulation during dosing break) could prevent recovery from thrombocytopenia and milademetan's differentiated profile allows for rapid plasma clearance and lack of drug accumulation in tissues, which in turn enables this unique dosing schedule to pursue MDM2-dependent cancer populations across solid tumors and heme malignancies.

The company also has a preclinical program targeting RAD52 in the DNA damage repair pathway, though it's not central to my focus at this point. This drug candidate could have utility in patients with a molecularly diagnosed HRD+, such as mutations and loss-of-function in BRCA1/2 or others that utilize RAD52 as an alternative DNA repair pathway, as well as for patients that may have relapsed to poly (ADP ribose) polymerase (PARP) inhibitor therapy. The differentiator here is that there are no other RAD52-targeting programs in the clinic currently. Tumor types it could be applicable to include breast, prostate, pancreatic, ovarian and possibly other cancers. Unlike certain synthetic lethality programs I've been following for related targets where the only path forward is via combination with standard of care therapy, what I like here is that the development path forward could entail monotherapy in HRD+ patients relapsing on PARP inhibitor therapy as well as front-line combinations with PARP inhibitors in HRD+ tumors.

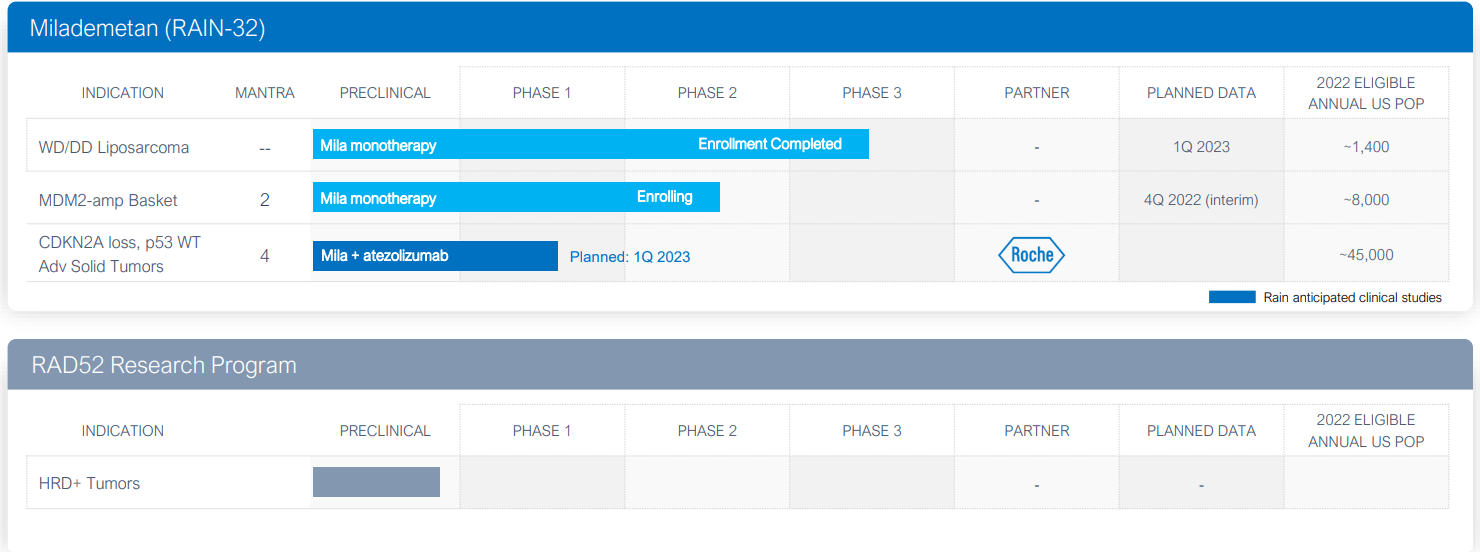

{kind=link}

Figure 2: Pipeline

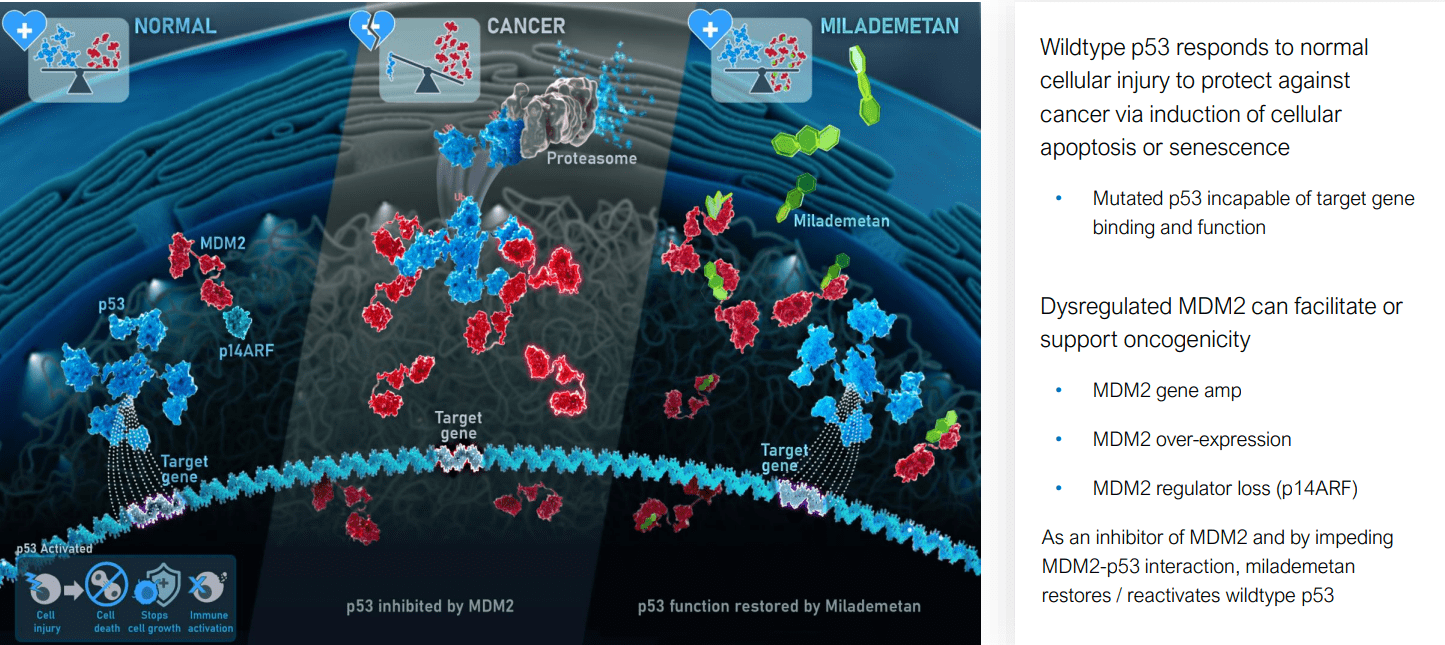

Focusing on the first candidate, milademetan reactivates p53 (guardian of the genome) by inhibiting MDM2. Per 10-K filing, "p53 is present in every cell and acts as a key regulator of a variety of cellular processes including cell cycle, DNA repair and apoptosis". Essentially, p53 activity in a normal cell is controlled and regulated by inhibitor protein MDM2 (binds to p53 and induces degradation, allowing normal cells to function properly). However, in response to cell damage and other stressors, p53 is activated and prevents formation of cancerous cells by inducing apoptosis (programmed cell death).

In tumor cells, p53 can be inactivated by mutations in p53 or activation/overexpression of MDM2. Half of all tumors have p53 gene mutations, and the remaining cancer patients have WT p53 (can be functionally suppressed through activation or overexpression of MDM2). The central focus of the company is on solid tumor types it's identified that are MDM2-dependent and where milademetan could have utility via binding MDM2 at the p53 interaction site (thereby preventing formation of the MDMD2-p53 complex and triggering cancer cell cycle arrest or apoptosis).

{kind=link}

Figure 3: MDM2-p53 axis and milademetan MOA

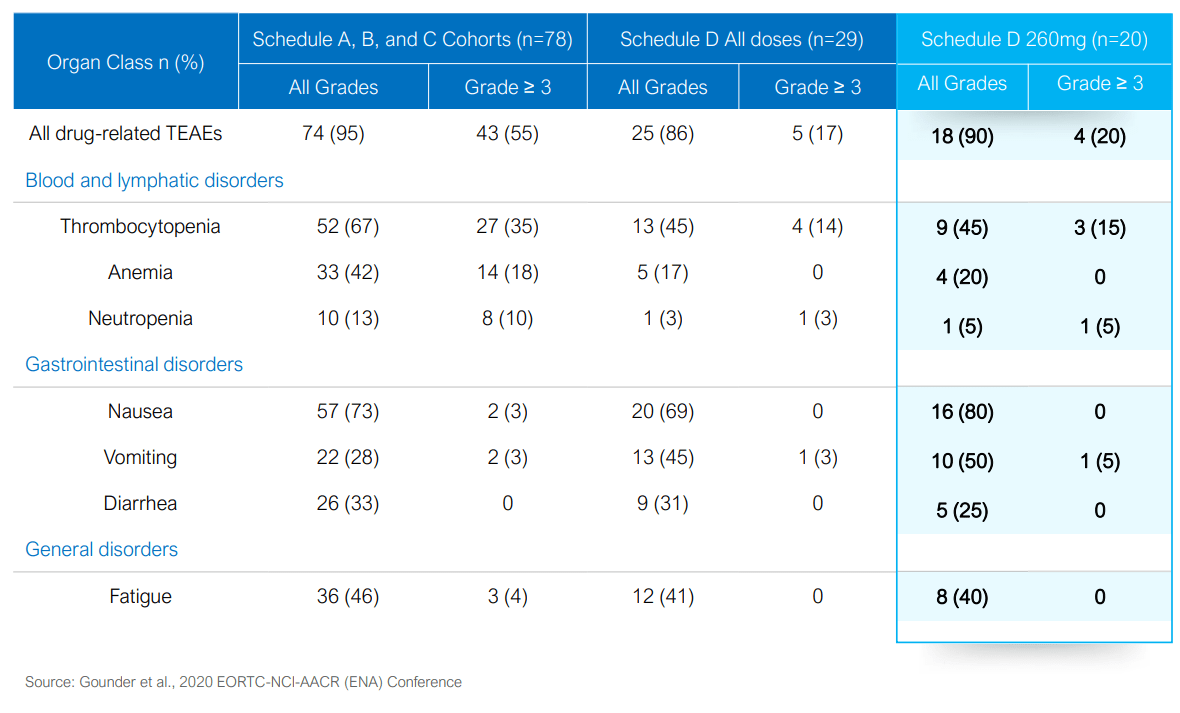

The backstory of milademetan is that it was previously developed at Daiichi Sankyo (and before that Rigel I believe) in various solid tumors including phase 1 study in WD/DD LPS (liposarcoma). These types of tumors have nearly universal MDM2 gene amplification and WT p53 (thus are nearly universally MDM2-dependent). Comprehensive results from Daiichi's phase 1 study in 107 patients showed meaningful antitumor activity in an MDM2-amplified subtype of LPS and other solid tumors (validated the newly designated dosing schedule and its ability to widen the therapeutic window of MDM2 inhibition).

{kind=link}

Figure 4: Select treatment emergent adverse events in phase 1 study

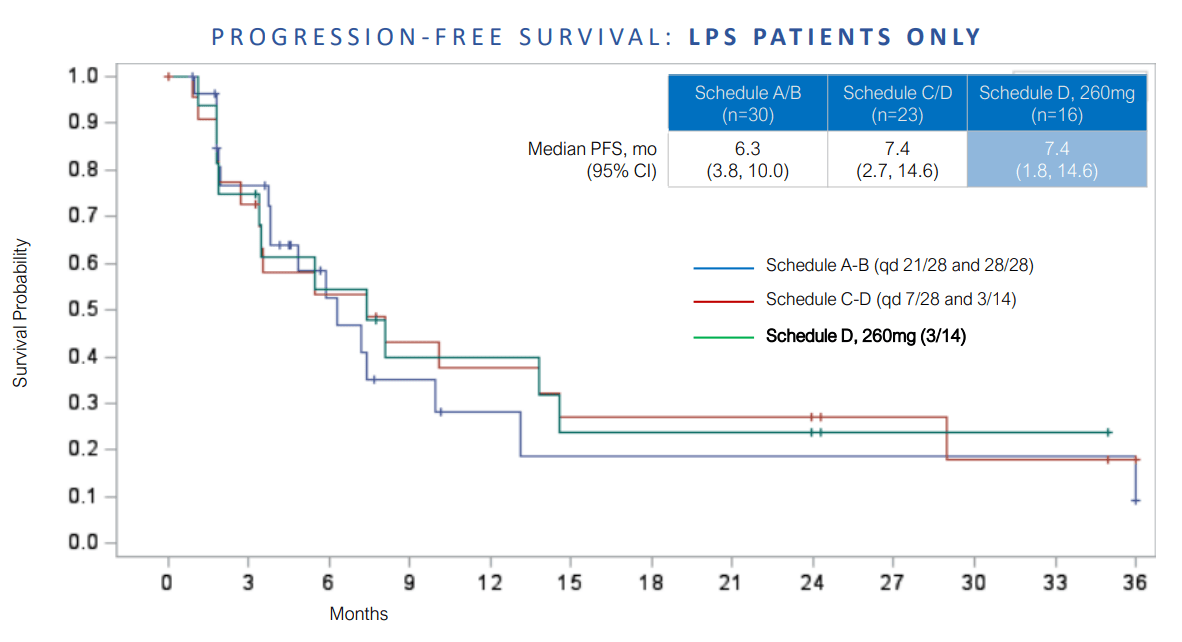

For context, LPS treatment almost never produces tumor responses regardless of therapy or line of treatment. Thus, efficacy is evaluated with the endpoint of progression-free survival or PFS which is also being used in the company's MANTRA phase 3 LPS trial. On ORR basis, phase 1 results were underwhelming with 3.8% partial response rate (two patients) and 64.2% stable disease rate. However, DCR in the LPS population (versus non-LPS) was nearly double and supported the plan to select patients with MDM2 amplification in future studies. July phase 1 update shared that three WD/DD LPS patients received treatment with milademetan monotherapy for greater than 51 months (two with durations of 51 and 57 months without disease progression, third patient with 59 months before discontinuation). Devil's advocate would point out that the phase 3 trial is being initiated based on a prior low N (patient number) data set (something to keep in mind).

In regard to market opportunity in LPS, US annual incidence is 3,500 patients of which WD/DD is 65% of LPS p53 WT & MDM2 amplified in nearly 100% of WDLS/DDLS cases. Thus, annual US addressable market is around 1,400 patients. Approved therapies from JNJ and Eisai yield 2 to 2.2 months of PFS, a number that milademetan more than tripled with dose schedule D.

{kind=link}

Figure 5: Phase 1 PFS in LPS patients

On the heels of these results, in July 2021 Rain initiated the phase 3 registrational MANTRA trial in patients with unresectable or metastatic DD LPS with or without a WD LPS component that has progressed on one or more prior systemic therapies, including at least one anthracycline-based therapy. Top-line data is expected in 2023. PFS assumptions for statistical powering are based on PFS assumption of three months for control arm and six months for milademetan (both appear conservative and appropriate, to my eyes). Doubling of PFS would equate to a hazard ratio of 0.5, which would be very significant.

As for the more lucrative potential via tumor-agnostic approach in patients with MDM2-amplified tumors, in the prior phase 1 study 10 non-LPS patients received milademetan in Schedule D. Three of them were characterized for MDM2 gene amplification. These included patients with breast cancer (copy number of 16.8), synovial sarcoma (copy number of 25.9) and small cell lung cancer (SCLC) (copy number of 36.6). The first patient experienced confirmed tumor volume reduction, while the latter two exhibited partial responses (only one of which was confirmed).

{kind=link}

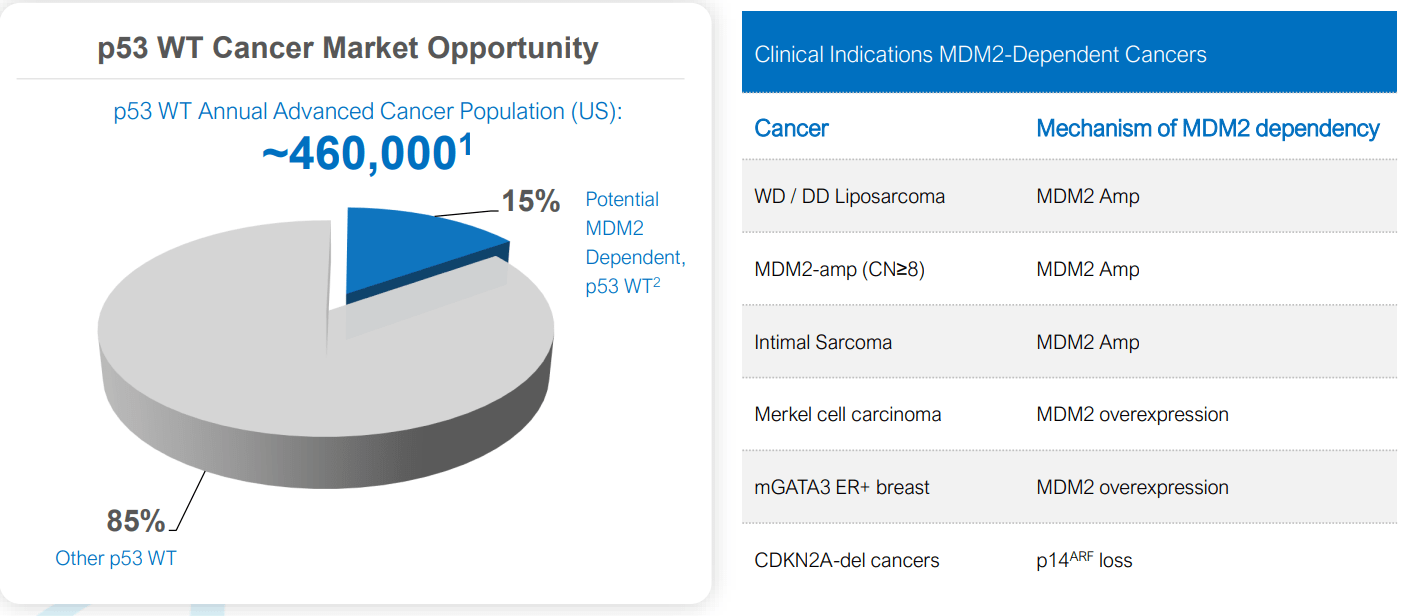

Figure 6: P53 WT cancer market opportunity is outsized relative to current valuation

The phase 2 MDM2-amplified tumor-agnostic basket trial (MANTRA-2) was initiated in November 2021 evaluating milademetan in patients with advanced or metastatic solid tumors refractory or intolerant to standard-of-care therapy and that exhibit wild-type p53 and a prespecified minimum MDM2 gene copy number. The goal is to enroll 65 patients with primary endpoint of objective response rate (ORR) as measured by RECIST criteria. Key secondary endpoints include duration of response, disease control rate, progression-free survival, overall survival and growth modulation index. Keep in mind these patients are far from being low-hanging fruit, as they have progressed on standard of care therapy and are unlikely to derive benefit from or tolerate it. I will go more into the data in recent developments section below.

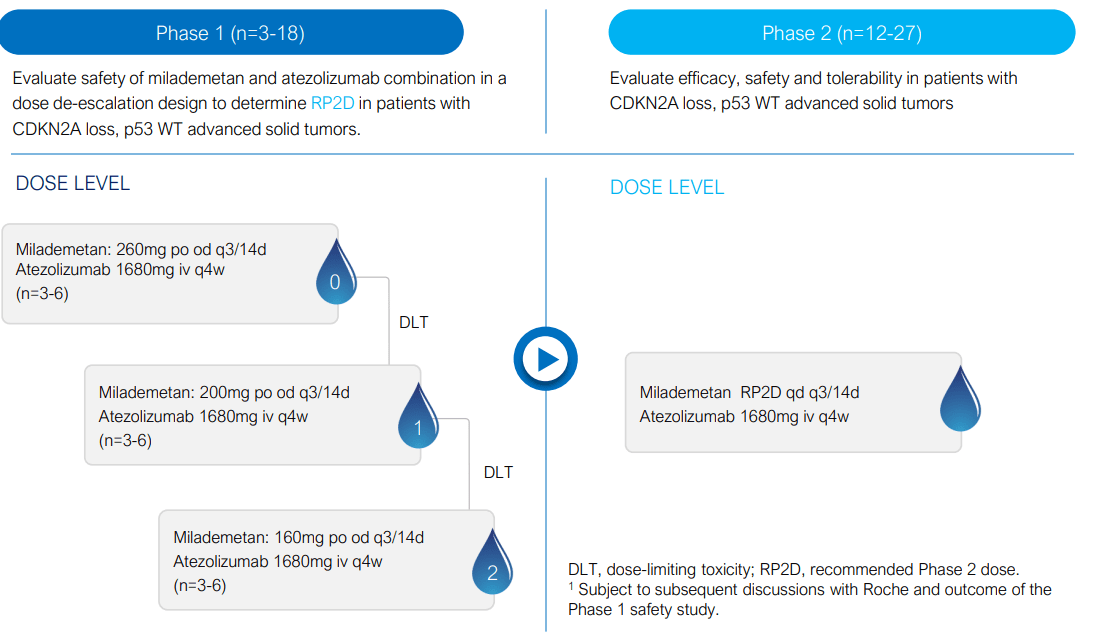

Lastly, the MANTRA-4 phase 1 study will combine milademetan with atezolizumab (PD-L1 inhibitor) in patients with CDKN2A loss and wildtype p53 advanced solid tumors (start enrollment in Q1 2023). The rationale here is that cyclin-dependent kinase inhibitor 2A (CDKN2A) encodes for the tumor suppressor p14ARF, an inhibitor of MDM2, and the loss of CDKN2A may lead to MDM2-dependent cancers. This is supported by nonclinical data demonstrating in vitro sensitivity to milademetan of cancer cell lines harboring CDKN2A loss and WT p53 as well as several in vivo models with CDKN2A loss showing anti-tumor activity of milademetan. Also, prior publications show that loss of p53 activity via MDM2 and/or CDKN2A has also been associated with poor clinical outcomes for patients treated with immune checkpoint inhibitors. Preclinical data in an immune competent mouse model of colorectal cancer with CDKN2A loss demonstrated enhanced combinatorial activity of milademetan plus an anti-PD1 antibody compared to either agent alone. On the basis of these results, in January the company announced clinical supply agreement with Roche for atezolizumab for the phase 1 study. This patient population amounts to an opportunity of 45,000 annually (quite sizeable and would be a needle-moving catalyst should early efficacy be observed).

{kind=link}

Figure 7: MANTRA-4 study design

Select Recent Developments

In February, I identified a green flag with a strengthening of the leadership team including new VP of Clinical Development Nora Ku (joining from Loxo Oncology at Lilly) and BP Head of Global Drug Safety and Pharmacovigilance Flor Nicolas (joining from Gilead Sciences). Likewise, new VP and Head of Global Regulatory Affairs Tina Kim-Hafken joined from Seagen (served there as Senior Director of Regulatory Affairs). Anytime I see such appointments for a company of this small size, at the very least it's a positive indicator that should be taken into account. Not to be overlooked, Dr. John Maraganore assuming an advisory role to CEO and Leadership team adds significantly to credibility here (well-known executive for his founding role and serving as CEO at Alnylam Pharmaceuticals for 20 years).

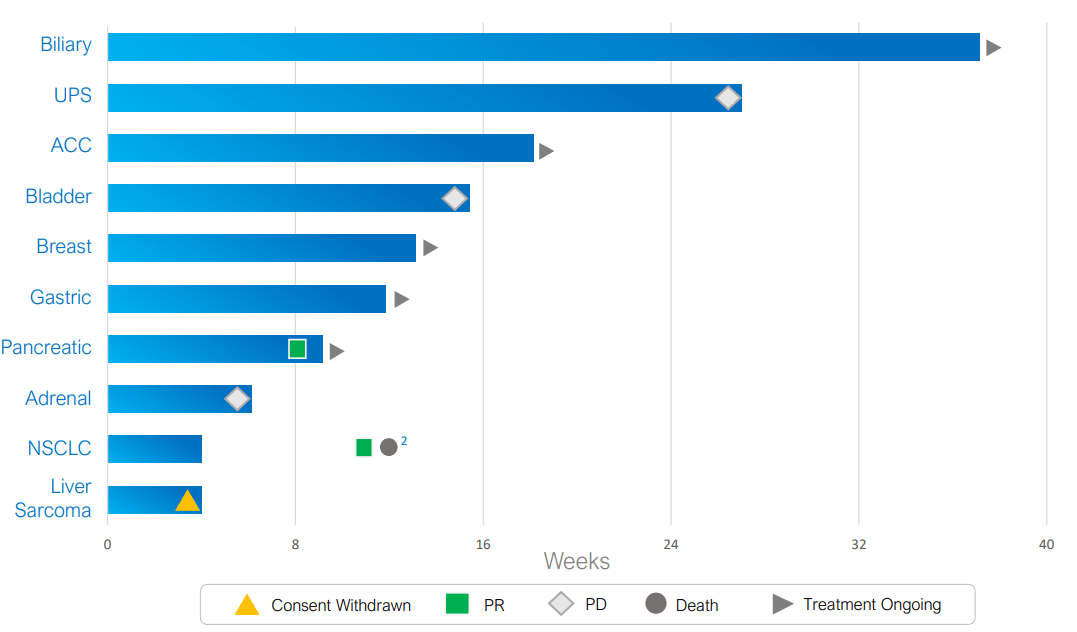

Flash forward to November 4th, where promising interim phase 2 data for milademetan allowed the company to easily raise $50M in a private placement. In the first 10 evaluable patients, there were two unconfirmed partial responses observed at first scan and promising tumor regression activity in two additional patients on monotherapy. Also of note is that anti-tumor activity was observed in patients with genetic co-alterations, and in tumors with MDM2 copy number above 8 (allowing them to revise protocol to include patients tested locally for MDM2 copy number of 8 and greater). One negative aspect, playing devil's advocate, is how long it's potentially going to take them to enroll the desired 65 patient number.

{kind=link}

Figure 8: Duration on therapy in MANTRA-2 study

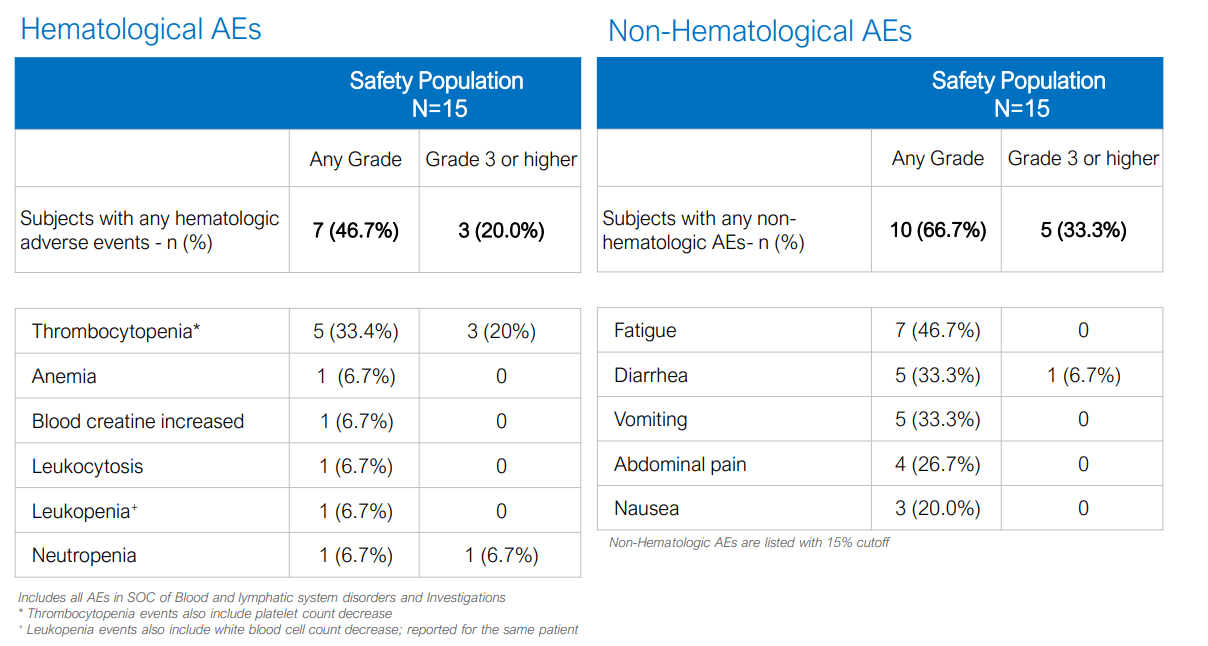

Diving into specifics, the two unconfirmed PRs were observed with tumor regression of 34% and 30% in pancreatic and lung cancer, respectively. The pancreatic cancer patient is pending response confirmation and treatment is ongoing (seems likely this becomes a confirmed PR, which would be significant). Likewise, the two patients with tumor regression of 29% and 27% (biliary tract and breast cancer) continue on monotherapy so these results could further improve. As for why the lung cancer patient did not further improve, he or she unfortunately died due to Covid-19. Keep in mind that patients in the study had co-alterations in oncogenes or tumor suppressors including KRAS, EGFR, and PIK3CA. Population was heavily pretreated with median four prior therapies, while safety profile was similar to prior phase 1 study.

{kind=link}

Figure 9: AE profile for MANTRA-2

Other Information

For the third quarter of 2022 , the company reported cash and equivalents of $140M (includes proceeds from secondary offering) as contrasted to net loss of $18M. Research and development expenses came in at $14.5M, while G&A rose to $3.9M. Thus, I conservatively estimate that they have operational runway into 1H 24. Accumulated deficit of just $90M is on the low side and perhaps speaks well as to fiscal stewardship.

Here are a few nuggets from the Wainwright presentation :

- End goal here is to reactivate p53 and MDM2 acts as natural inhibitor of p53. It could be more appropriate to cite mechanism as inhibitor of MDM2 p53 complex, which keeps p53 (guardian of genome) where it is protected. p53's normal function as a transcription factor is to induce activity of several genes that protect cells from cancer. Cancer has to find a way to get rid of p53, by mutating and breaking it so it can no longer bind DNA or the other way is by enhancing levels of an inhibitor of p53. Tumors where there is enhanced reliance on MDM2 or overexpression or gene amplification of MDM2 could be targeted with an inhibitor like milademetan.

- MANTRA-2 basket study is open label and will enroll 65 patients with advanced solid tumors with degree of MDM2 gene amplification they think will be sensitive to response (treat with monotherapy). This is the first time an MDM2 amplified strategy has been employed as a prospective patient selection approach. Other companies are trying to pursue the strategy and follow them. Initial 10 patient data is encouraging, every patient with a different tumor type (pancreatic, breast, lung, biliary, etc). This is reflective of tumor agnostic strategy. They saw patients with significant number of prior therapies including pancreatic, lung, breast and cholangiocarcinoma with compelling and rapid initial tumor regression. 2 patients (pancreatic and NSCLC) achieved threshold of partial response in first scan. 2 additional patients (breast with PIK3CA mutation and biliary) with near PRs at first scan. This is encouraging, as they represent patients with multitude of coalterations (KRAS G12D, EGFR, PIK3CA, etc). Patients receiving milademetan as 5th line, 6th line, 7th line and showing this activity is encouraging. They are NOT at the point of being able to draw definitive conclusions yet, but clear activity in deep salvage patients is telling. They are excited due to safety, because predecessors have failed because of class of on-target cytopenias. New dosing schedule optimizes for safety thus giving them best-in-class safety profile and enables them to stack their therapy on top of other therapies (increasing market opportunity).

- Ultimate opportunity is not just monotherapy but combinations with others, including PD-1. Initial threshold for enrollment was 12 copies of MDM2 gene or greater, and they saw activity in patients with copy numbers of less than 12 so they lowered that copy number for enrollment to 8 (reasonable chance of efficacy there). The benefit there is to give greater perspective across greater number of tumors, expedite enrollment leading to less cash burn and broaden market opportunity.

- A front door approach is to adopt a tumor agnostic strategy, then see level of response (at least 30% by RECIST) with duration of response north of 5 months. In that range, they would be encouraged enough by data and take it to FDA to see what trial needs to look like to be registrational (expand existing phase 2 versus run another trial). Door B is if they see responses by tumor types over time (greater number of patients with certain tumors responding), there is opportunity to look at tumor-specific cohorts. Lung, breast and bladder comprise vast majority of patients with MDM2 gene amplification in terms of US incidence. Door C (if needed) is to give the program an additional push for meaningful activity via synergistic combinations.

- Bottom line, they think of MANTRA-2 study as providing multiple ways to win.

- MANTRA lead study got enrolled 5 months ahead of schedule. They are blinded to trial, but management hopes the reason for rapid enrollment is because of enthusiasm from clinicians and patients. The CEO does not believe liposarcoma opportunity is appreciated at 1400 patients eligible in US each year for therapy (corroborated by speed of enrollment in pivotal study). Pivotal study enrolled 175 patients in 12 months (most sites came on prior to completion of enrollment, so really 6 months for ramp up not indicative of ultra-orphan indication). Big milestone next quarter is pivotal readout and if positive they could file for registration in US + EU (first MDM2 inhibitor to become commercially available, then expand indications from there). They will start MANTRA-4 study (PD-L1 combo) in the near term.

As for other competitors in this space, this publication on alrizomadlin is on the combination with pembrolizumab. Thus, it's hard to draw conclusions. BI-907828 was the one mentioned by analysts ( see abstract ) and activity here was promising. Again, conclusions are hard to draw as it's on doublet therapy (combine with checkpoint inhibitor) but of nine evaluable patients, four had confirmed partial response (two biliary tract carcinoma, one urothelial carcinoma and one myxoid liposarcoma). There was also an unconfirmed PR in a patient with adenocarcinoma and four patients with liposarcoma and gastric cancer had stable disease.

As for institutional investors of note , Perceptive Advisors owns a 9.4% stake and Biotechnology Value Fund owns an 18.8% stake. Cormorant Global Healthcare Master Fund owned a 9.99% stake. Of note regarding insiders, CEO Vellanki recently bought 25,000 shares on the open market and owns 2.471 million shares.

As for relevant leadership experience, co-founder and Chief Scientific Officer Dr. Robert Doebele has significant experience in precision oncology including leading research that launched the TRK field by demonstrating that NTRK1/2/3 gene fusions (led to approval of Loxo's larotrectinib and Ignyta's entrectinib). Chief Medical Officer Richard Bryce served prior as Chief Medical/Scientific Officer of Puma Biotechnology (led development for TKI neratinib). He also served as senior medical director of clinical science at onyx Pharmaceuticals (eventually bought out by Amgen for $10.5B). VP Regulatory Affairs Tina Kim-Hafken served prior as Senior Director Regulatory Affairs at Seagen (led submission and approval of Tukysa in HER2+ breast cancer).

Interestingly enough on the board of directors, we find Aaron Davis (cofounder and CEO of Boxer Capital), Gorjan Hrustanovic (principal at BVF Partners) and Peter Radovich (COO of Core Biotech holding Mirum Pharmaceuticals_

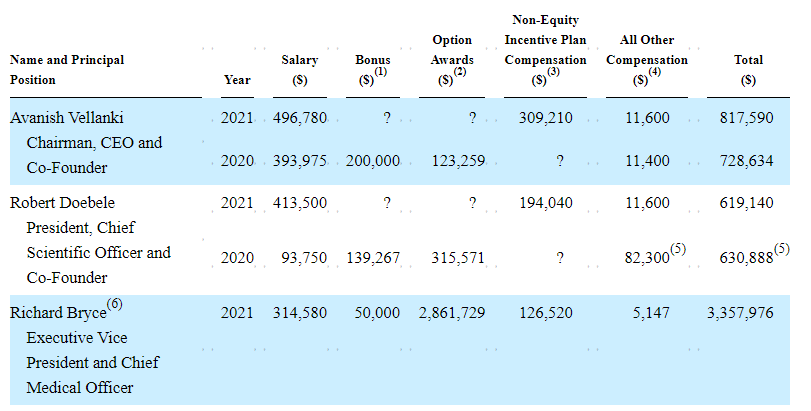

Moving on to executive compensation, base cash salary in the $314k to $496k range seems quite reasonable for a company this size. Likewise, non-equity and options awards are much lower than for similar companies I've examined in recent articles.

{kind=link}

Figure 10: Executive compensation table

The important thing is to avoid companies where the management team is potentially in it for self-enrichment instead of creating value for shareholders, and looking at compensation is one of several indicators in that regard.

As for IP, patent portfolio for milademetan contained 14 US patents, three pending US applications, 97 foreign patents issued and 34 pending foreign patents. One patent family directed to composition of matter is expected to expire in 2032, excluding potential term adjustments or extensions. Additional patent families are directed to combination therapies, methods of synthesis and dosing regimens (expiring 2034 to 2037). Lastly, the company intends to pursue additional patent protection for milademetan and other development candidates relating to milademetan, its methods of use and related technologies. As for the RAD52 program, second patent family is expected to expire in October 2040 (composition of matter IP was licensed via Drexel 2 patent families).

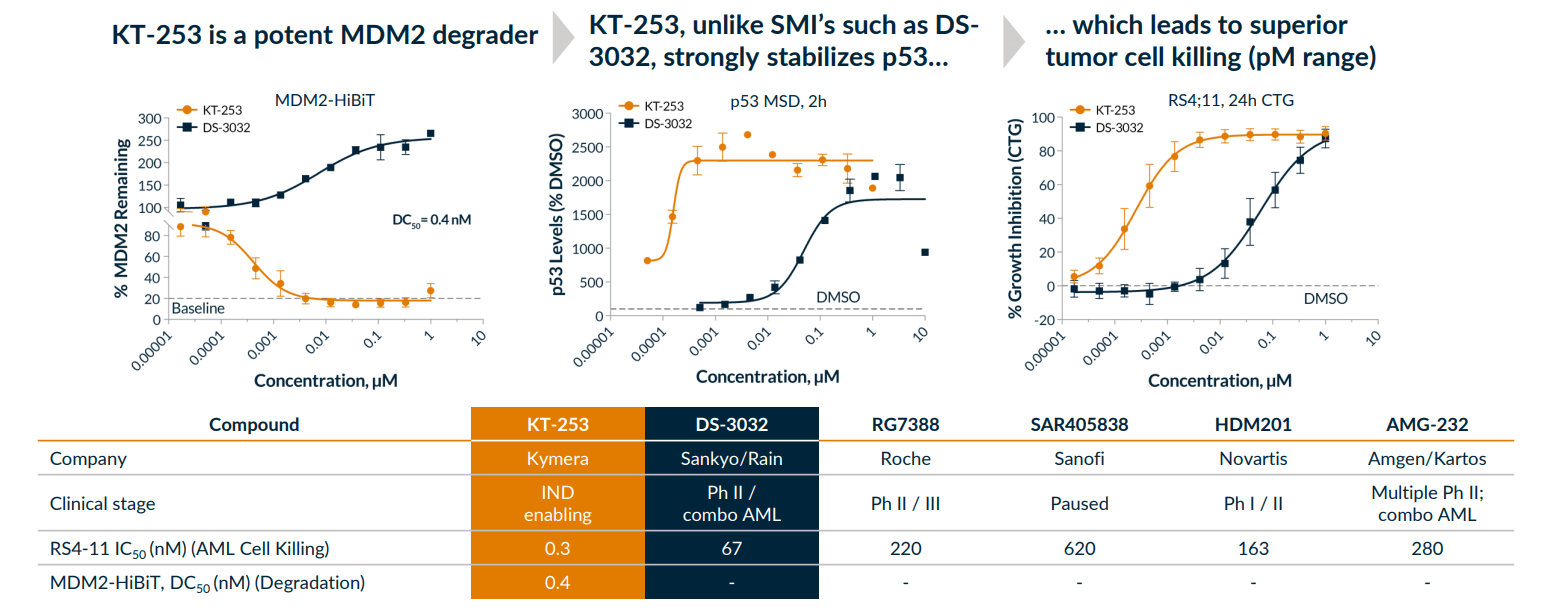

As for other useful nuggets from the 10-K filing (you should always scan these in your due diligence as many companies like to sweep undesirable elements under the rug), in regard to competition the company refers to other MDM2 inhibitors and degraders in various stages of development including Kartos (navtemadlin), Ascentage (alrizomadlin), Boehringer Ingelheim (BI-907828), Aileron (ALRN-6924), Kymera (KT-253), and others. Kymera's candidate would be my principal concern as a fast follower, but keep in mind they won't enter the clinic until 1H to mid 2023 (would expect dose escalation for a degrader candidate to take some time). The company (rightly) claims that degradation more efficiently restores p53 versus inhibition and its candidate KT-253 was shown to be over 200 times more potent in tumor cell killing assays versus small molecule inhibitors due to its mechanism of action.

{kind=link}

Figure 11: KT-253 superiority versus MDM2/p53 small molecule inhibitors

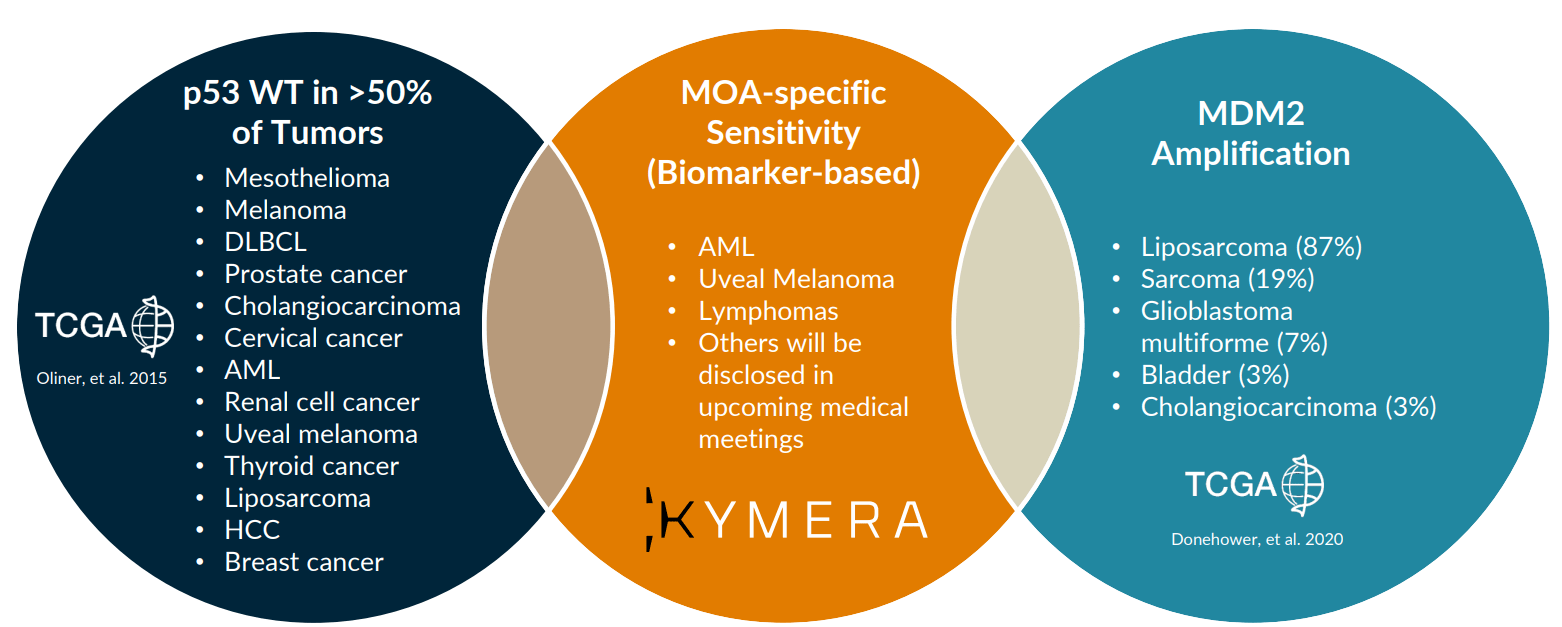

In terms of validation of the market opportunity, the fact that Kymera's highly experienced management and clinical development team sees enough value in this target to prioritize it is important.

{kind=link}

Figure 12: Indications Kymera could focus on where MDM2 degradation leads to acute apoptotic response

Final Thoughts

To conclude, while I do have concerns about the long term in regard to competition in the MDM2 space (particularly from protein degradation), that will take a considerable amount of time and by no means can we be certain whether Kymera and others will close the gap. Milademetan to my eyes appears to be the lead horse in this race and data to date suggests they could pursue a tumor-agnostic label if responses continue to be observed across various types of cancer. While Rain in essence is a single drug company currently, they do have multiple shots on goal and I look forward to seeing how combination efforts with PD-L1 in patients with CDKN2A loss and wildtype p53 advanced solid tumors works out (45,000 patient opportunity here alone).

For readers who are interested in the story and have done their due diligence, RAIN is a Buy and I suggest initiating a pilot purchase on dips. From there, a prudent strategy could be to wait for near term data and take further action depending on strength of the results.

As for my personal clinical-stage portfolio (ROTY), I would prefer to hold this position patiently during 2023 to 2024 timeframe especially as basket studies (larger opportunities) make progress in the clinic.

As for risk rating (1=low, 5= high), I will err on the side of caution and assign this one a 4 considering its a single-drug story and supportive data sets with low number of patients. Key concerns include additional dilution in the latter part of 2023, safety/tolerability issues which have plagued drug candidates pursuing this target and competition including from the likes of Kymera and Boehringer Ingelheim. Another cause for concern is that these types of studies can take a LONG time to enroll (screening for high expressors of the target).

For further details see:

Rain Oncology: Multiple Data Catalysts In 2023 For This Precision Oncology Pioneer