IYR - Rally Fades After Fed Warning

2023-06-25 09:00:00 ET

Summary

- U.S. equity markets posted their worst week since March after central bank officials in the U.S. and globally warned that further monetary tightening is necessary to contain inflation.

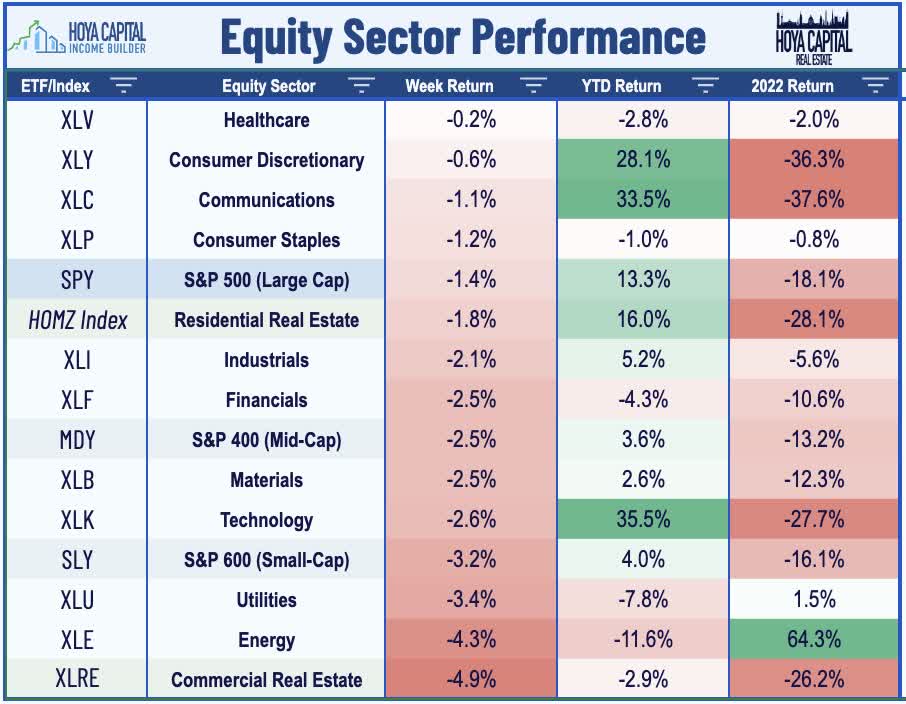

- Snapping a five-week winning streak that had sent the benchmark to its highest levels since April 2022, the S&P 500 declined 1.4% this week. Small-Caps slid by more than 3%.

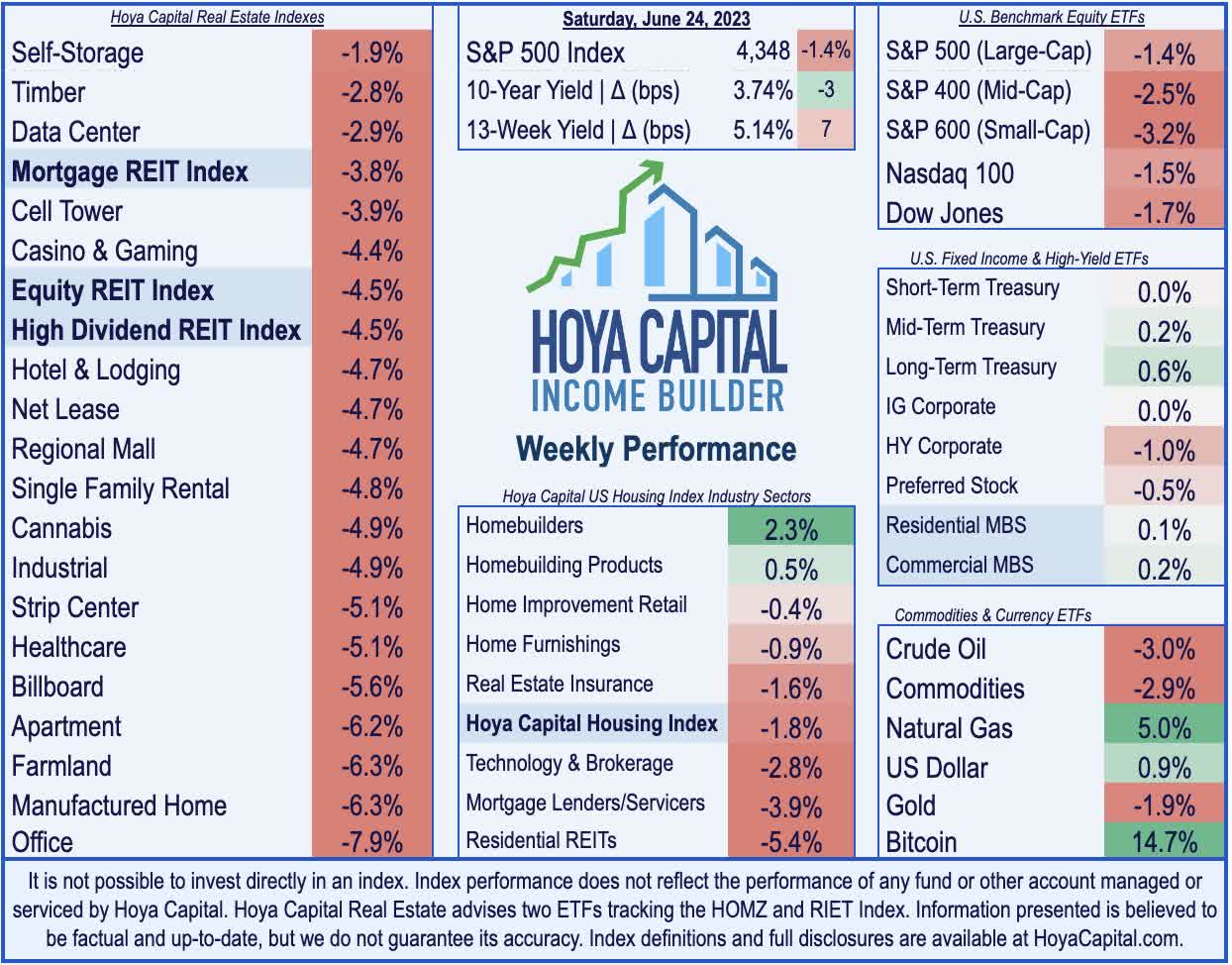

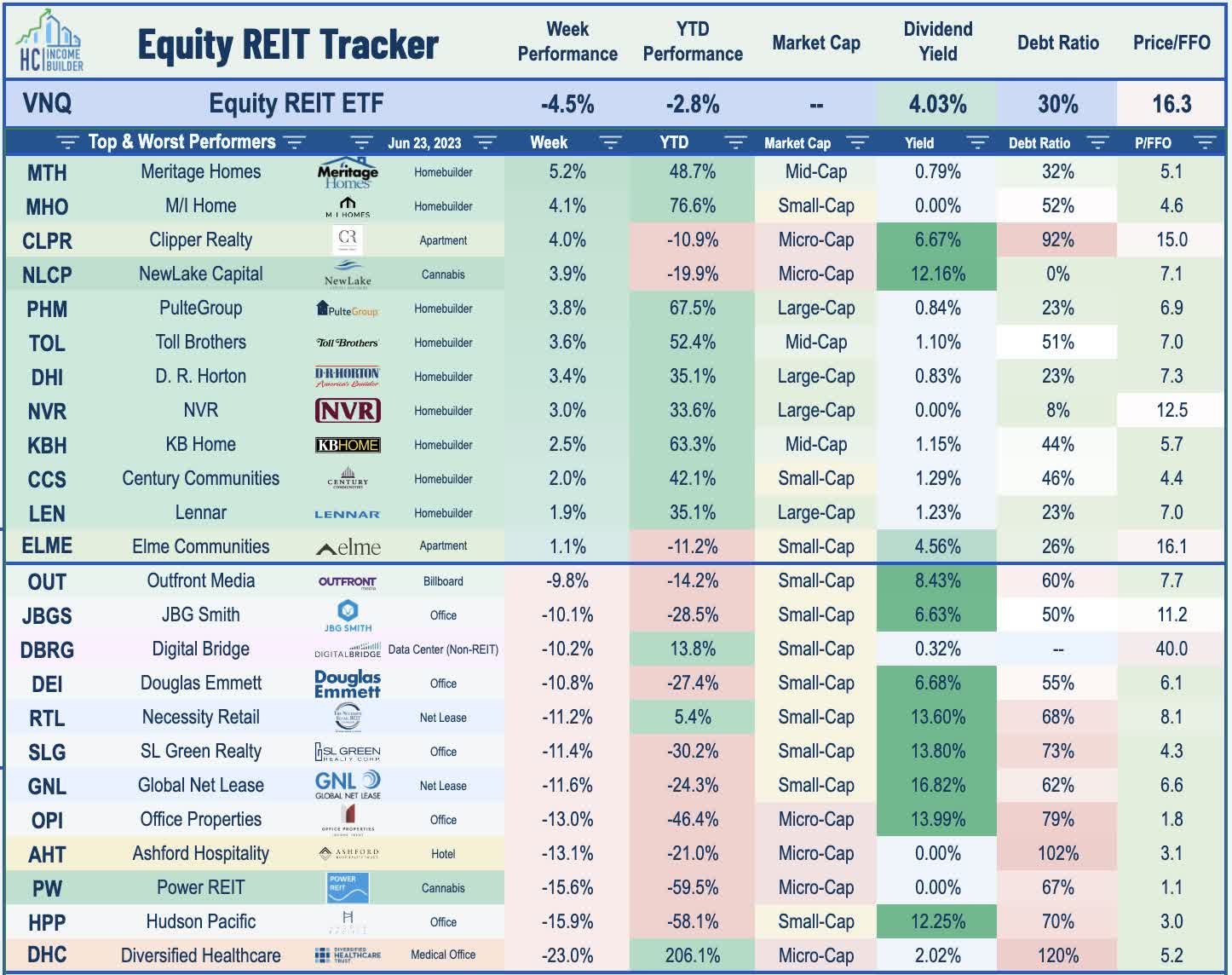

- Real estate equities were also under sharp pressure following three weeks of gains. The Equity REIT Index dipped 4.5% this week, with all 18 property sectors in negative territory.

- Left for dead at the start of the year, single-family homebuilders added to their impressive year-to-date gains on data showing a rebound in housing activity this Spring following a sharp cooldown in late 2022 and into early 2023.

- Hawkish remarks from central banks clashed with data last week showing that several of the major inflation indexes have been running below the Fed's target since last July. PMI data this week showed a "dramatic" decrease in price pressures in the manufacturing survey and a nearly three-year low in price pressures in the services report.

Real Estate Weekly Outlook

This is an abridged version of the full report and rankings published on Hoya Capital Income Builder Marketplace on June 23rd.

U.S. equity markets posted their worst week since March after central bank officials in the U.S. and globally reiterated their stance that further monetary tightening is necessary to contain inflation. In closely-watched testimony to Congress, the Federal Reserve Chairman warned that markets should expect more rate hikes in the coming months, remarking that there remains "a long way to go” to get inflation back to the Fed's target range. The remarks clashed with data last week showing that several of the major inflation indexes have been running below the Fed's target since last July and PMI data this week showing a " dramatic " decrease in price pressures in the manufacturing survey and a nearly three-year low in price pressures in the services report.

{kind=link}

Hoya Capital

Snapping a five-week winning streak that had sent the benchmark to its highest levels since April 2022, the S&P 500 declined 1.4% this week. Declines from large-caps were muted compared to their smaller peers, as the Mid-Cap 400 dipped 2.5% and the Small-Cap 600 slid more than 3%. Real estate equities were also under sharp pressure following three weeks of gains. Benchmark interest rates retreated slightly from three-month highs, with the policy-sensitive 2-Year Yield increasing 3 basis points on the week to 4.75% while the 10-Year Yield declined 3 basis points to 3.74%. The Equity REIT Index dipped 4.5% this week, with all 18 property sectors in negative territory, while the Mortgage REIT Index declined 3.8%. Homebuilders and the broader Housing Index remained a bright spot, however, continuing their impressive rebound this year following a strong slate of housing data and homebuilder earnings results throughout the week.

{kind=link}

Hoya Capital

Surprisingly weak economic data in Europe - combined with a surprising "double" rate hike from the Bank of England - renewed recession concerns for the region, as both Europe and Asian economies continue to battle higher levels of food and energy inflation resulting from the Russia/Ukraine war, which took a new turn this weekend with a reported coup attempt against Russian President Putin. Stateside, economic data wasn't much stronger - with the notable exception of the revived housing market - as a pair of PMI readings showed a continued slump in manufacturing activity while initial jobless claims were higher than expected for a third straight week. WTI Crude Oil prices - a key "swing input" in the domestic inflation outlook - dipped 3% on the week to levels that are 40% below the peaks seen last June. Meanwhile, Bitcoin rallied more than 10% following the launch of a new crypto exchange backed by Citadel Securities, Fidelity, and Charles Schwab.

{kind=link}

Hoya Capital

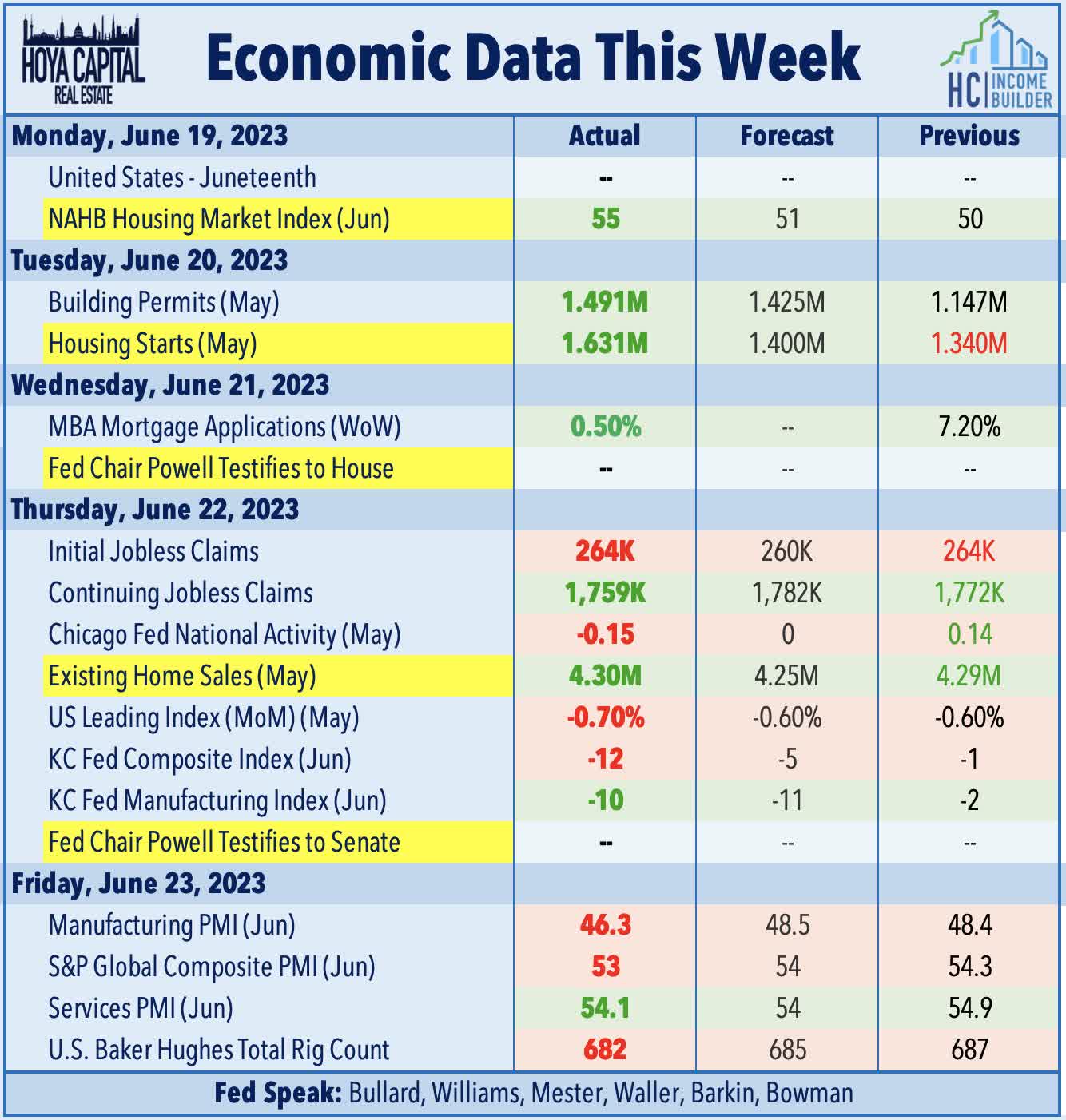

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

Hoya Capital

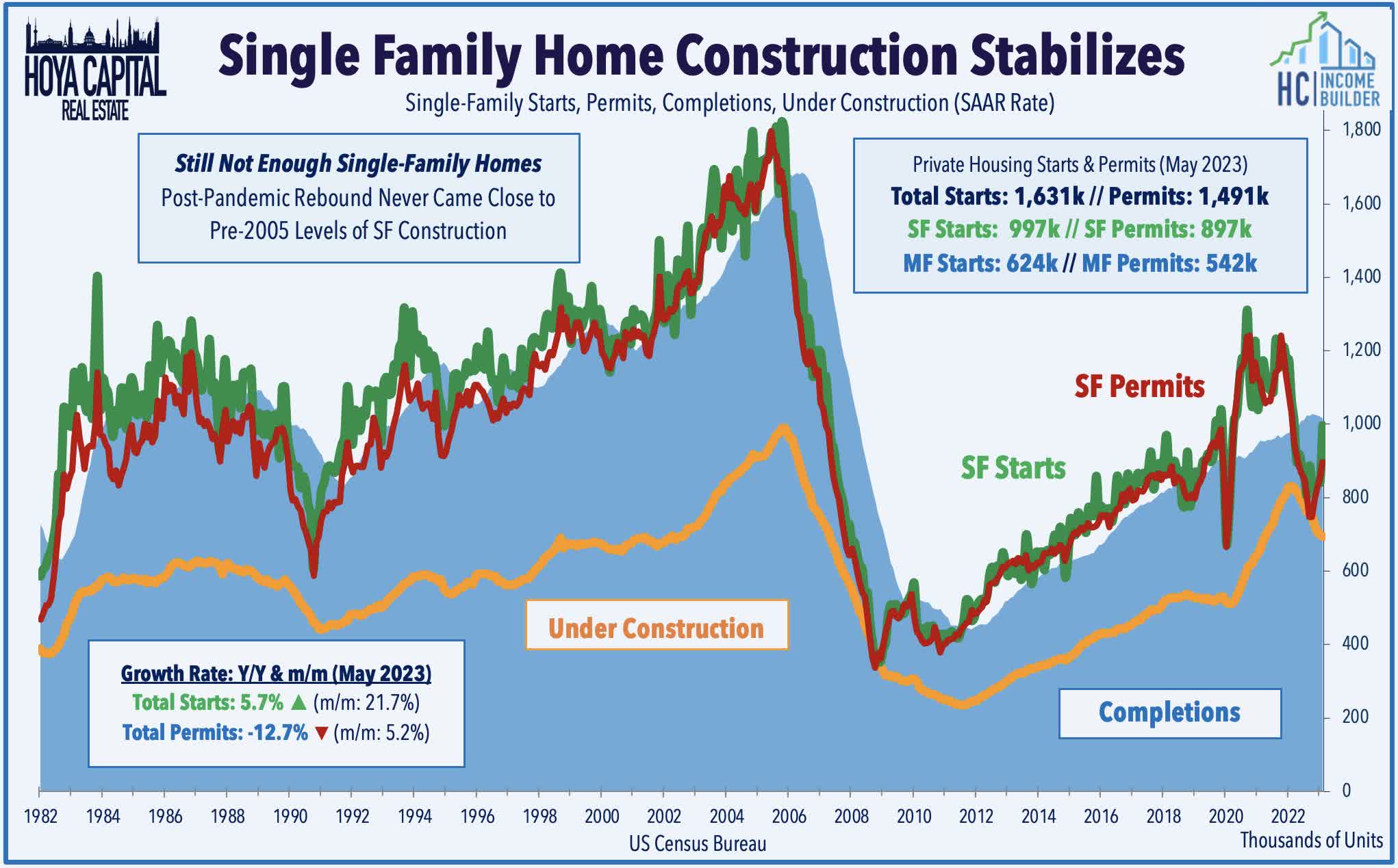

Left for dead at the start of the year, single-family homebuilders added to their impressive year-to-date gains on data showing a rebound in housing activity this Spring following a sharp cooldown in late 2022 and into early 2023. Housing Starts rose to a 1.63 million annual pace in May - up 5.7% from a year earlier - to the highest level since last April. The strong month of May snapped a streak of 11 straight months of year-over-year declines in housing starts beginning in May 2022. Both single and multifamily starts increased in May, while Building Permits also increased to a stronger-than-expected pace of 1.49 million units. Earlier in the week, the NAHB reported that its Homebuilder Sentiment index - a leading indicator of housing market activity - rose for a sixth-straight month in June, which follows a stretch of thirteen straight monthly declines. Existing Home Sales also topped estimates in May as a retreat in home prices has pulled some potential buyers back into the fold, even as inventory levels remain near historic lows.

{kind=link}

Hoya Capital

Equity REIT Week In Review

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

Hoya Capital

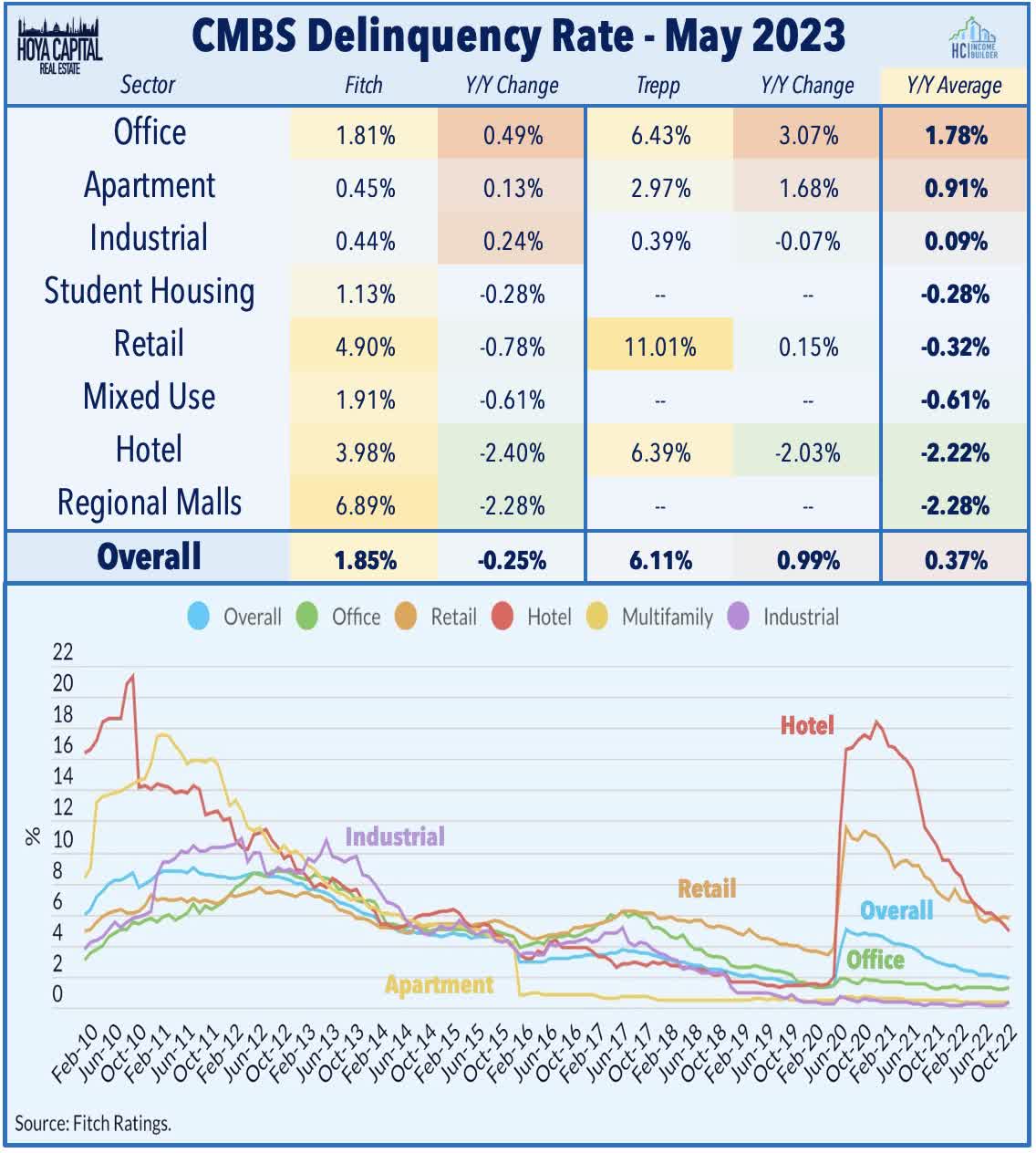

Office : Renewed pressure office REITs this week came after a new report from MSCI Real Assets showing mounting signs of financial distress in the troubled sector - particularly in the coastal urban markets where utilization rates remain at just 50% of pre-pandemic levels. The report estimated that there is roughly $43B in assets that are in "potential distress" - which is the most of any property sector - as maturities come due over the coming years. MSCI defines “distressed” as properties in bankruptcy, default, court administration, liquidation, or that have CMBS loans that have been transferred to a special servicer. Trepp reported earlier this month that the percentage of office loans in distress has nearly doubled over the past year to 6.4%, while Fitch data showed that delinquency rates on office loans increased to 1.8% in May, a year-over-year increase that is twice as large as the next property sector. Not all office REITs are in crisis mode, however, and nuance is required in the analysis. Coastal/Urban office REITs are the source of the real pain, where workers have resisted a return to long daily commutes: leasing volumes were down nearly 40% in Q1 compared to the pre-pandemic averages between 2017-2019. By comparison, Sunbelt/Secondary markets recorded leasing volumes that were only about 15% below pre-pandemic levels.

{kind=link}

Hoya Capital

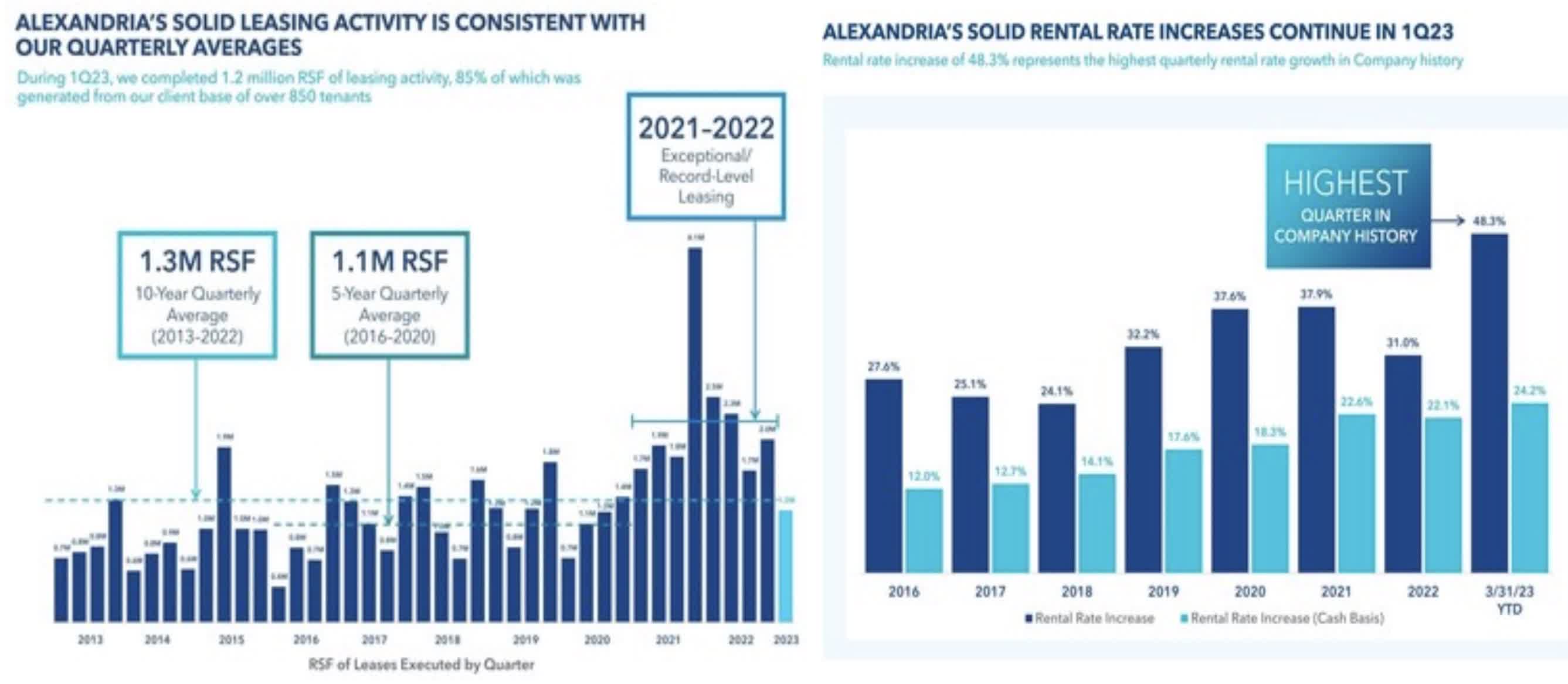

Healthcare : Lab space operator Alexandria Real Estate ( ARE ) slumped about 5% this week after becoming the latest REIT to come into the cross-hairs of short sellers. Activist firm Land and Buildings published a short report focused on the daily utilization rate of ARE's lab space facilities, which L&B says is 50% below pre-pandemic levels based on cell phone data estimated by data firm Placer AI. L&B - which has a short position in ARE - says that combined with the high levels of supply growth, "lab space fundamentals appear set to rapidly deteriorate." ARE pushed back with a business update this week in which it reiterated its full-year outlook calling for FFO per share growth of 6.4%, which would lift its cumulative FFO growth since the end of 2019 to nearly 30%, among the highest in the REIT industry. In its Q1 earnings report in May, ARE reported a ten-quarter low for leasing volumes but achieved record-high rental rate increases of 48.3% GAAP/ 24.2% on these bookings. ARE also announced this week that it sold five non-core properties in the greater Boston market for $365M and at a weighted-average capitalization rate of 5.2% and announced that it completed a recapitalization of an existing joint venture ("JV") for Towne Centre Drive in San Diego at a cap rate of 4.5% in which ARE sold 20% of its ownership interest in the property but retained operational control.

{kind=link}

Hoya Capital

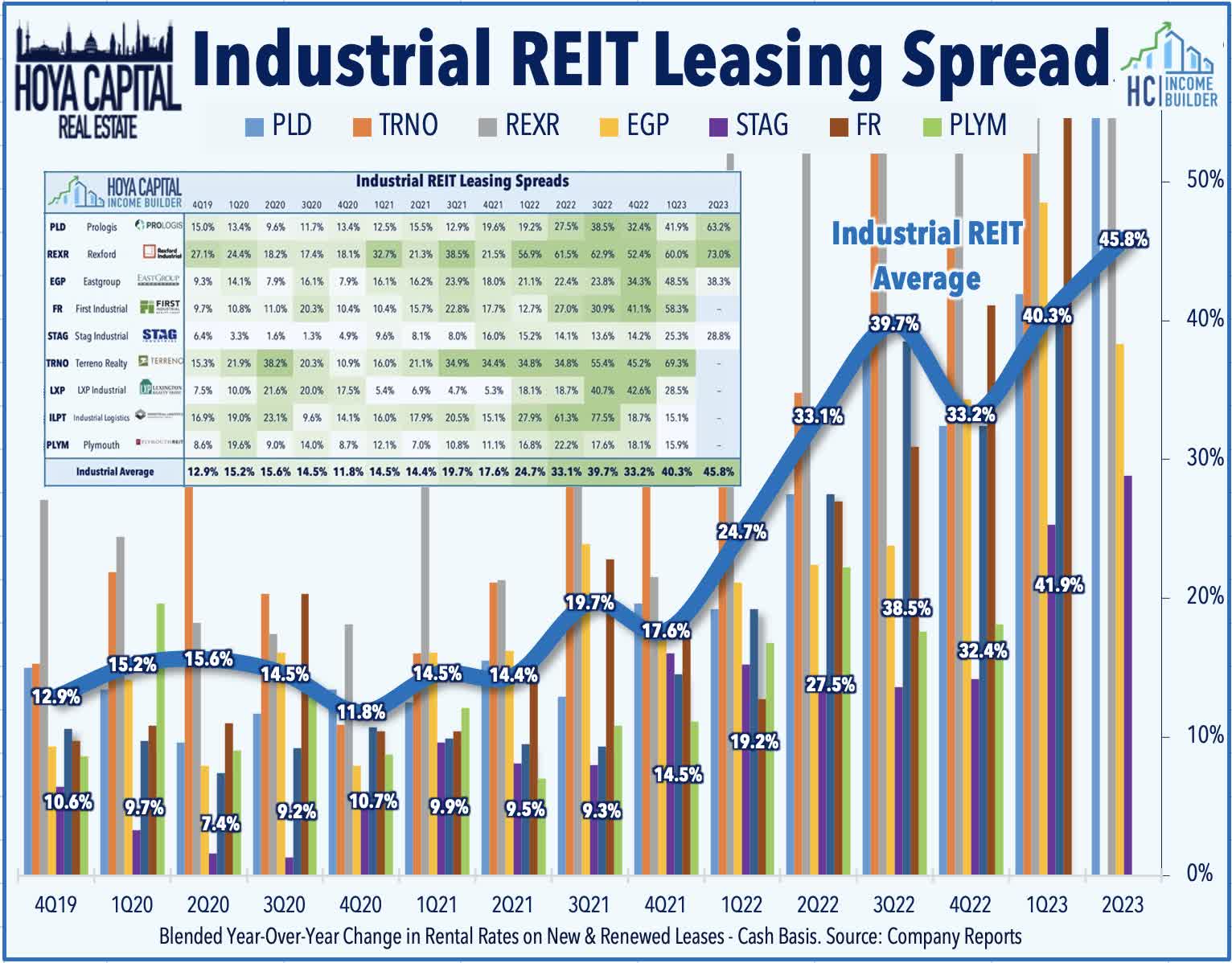

Industrial : Rexford Industrial ( REXR ) is another name that fell into the cross-hairs of the "shorts" this week, dipping more than 6% after it was named a new short idea at research firm Hedgeye, which cited its exposure to a decelerating Southern California market. The firm's recent track record on its public shorts has been hit-and-miss. Medical Properties Trust ( MPW ) has dipped more than 50% since the firm's short call last April, but more recent short calls, including EPR Properties ( EPR ) last December , Arbor Realty ( ABR ) in March , and Digital Realty ( DLR ) in May have each proven less successful thus far with all three REITs outperforming the benchmark by a wide margin since their respective calls. In the prior week, BMO Capital Markets downgraded Rexford with a similar thesis of weakening industrial fundamentals, cutting recent data showing reduced port traffic to L.A. and Long Beach and the potential for further worker disruptions, which has been a chronic headache for California ports over the past decade. Combined with upgrades to the Panama Canal and the more recent slowdown in Asian economic growth, labor issues on the West Coast have resulted in market share declines over the past decade to ports on the Gulf and East Coast.

{kind=link}

Hoya Capital

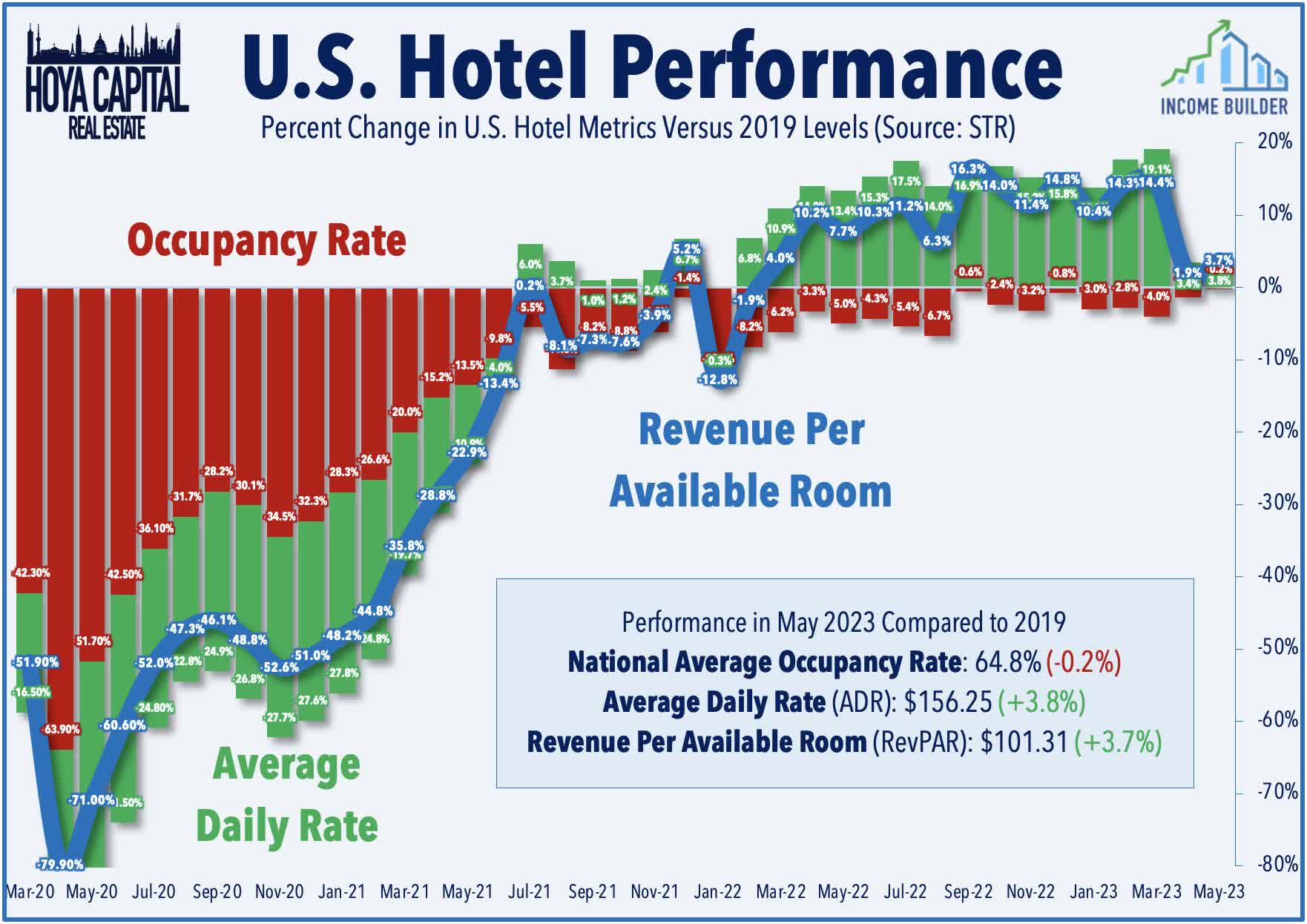

Hotels : Pebblebrook Hotel ( PEB ) was among the better-performers this week after it provided a business update in which it noted that it expects Revenue Per Available Room ("RevPAR") for the second quarter to fall "slightly below expectations," citing softening leisure demand in recent weeks, particularly in its West Coast markets. However, PEB affirmed its Q2 outlook for hotel EBITDA, and adjusted FFO as these weaker leisure trends have been offset by a continued improvement in business and group travel demand. Elsewhere, Ryman Hospitality Properties ( RHP ) announced that it completed the fundraising for its $800M purchase of the JW Marriott San Antonio Resort from Blackstone's ( BX ) BREIT. RHP raised $400M through a private placement of 7.250% senior notes due 2028 and raised another $415M through a public offering of secondary stock at $93.25/share which closed on June 9, 2023. Research firm STR reported this week that the national average RevPAR was about 4% above pre-pandemic levels in May as a recovery in relative occupancy rates has offset a moderation in room rate inflation.

{kind=link}

Hoya Capital

We also saw a continuation of some M&A drama over the past week. Diversified Healthcare ( DHC ) dipped more than 20% this week after affiliates of its external manager, RMR Group , announced an increased ownership position in DHC that may be enough to fend off proxy challenges to its proposed merger with Office Properties ( OPI ). The controversial merger between two struggling REITs that are both externally managed by RMR has faced challenges from several activist firms, including D.E. Shaw and Flat Footed. Elsewhere, Necessity Retail ( RTL ) announced that the 30-day "go-shop" period under its merger agreement with Global Net Lease ( GNL ) has expired without producing a superior acquisition proposal. As a result, it expects the transaction with GNL to close in Q3 2023, if it is approved by the stockholders of both companies. Several activist investors have also challenged this proposed merger between the two REITs, which are both externally managed by AR Global. Elsewhere, INDUS Realty ( INDT ) gained 0.5% this week after it received written notice from the CFIUS (Committee on Foreign Investment in the United States) that it has concluded its review and cleared its planned acquisition by Centerbridge and GIC Real Estate in an all-cash transaction that is now expected to close the Merger on June 29.

{kind=link}

Hoya Capital

Data Center : Sticking with the M&A theme, data center REITs were buoyed by news that asset manager Brookfield Infrastructure ( BIP ) will acquire privately-held Compass Datacenters - which currently operates roughly 16 data centers across the US, Europe, and Israel - in a partnership with Ontario Teachers' Pension Plan and the Azrieli Group. The partnership reportedly outbid former REIT DigitalBridge ( DBRG ) in a deal that values the company at roughly $5.5B, including debt. The transaction is expected to close by year-end and terms of the deal were not disclosed. Last week, we published Data Center REITs: The Epicenter of AI , which noted that Data Center REITs have been among the top-performing property sectors this year in a rebound fueled by reports of "booming" demand for artificial intelligence ("AI") focused data center chips. Even before the Nvidia report, Data Center REITs were on the upswing in early 2023 after an impressive slate of earnings results showed improved pricing power and record-high occupancy rates. Ironically, this AI-wave comes just as Data Center REITs became a trendy “short” idea centered on a thesis of weak pricing power and competition from the "hyperscalers"- Amazon, Google, and Microsoft.

{kind=link}

Hoya Capital

Strip Center : This week, we published Strip Center REITs: Back on Sale . Strip Center REIT fundamentals have improved materially over the past year and continue to be underappreciated in the market as a decade-long “retail apocalypse” narrative has been tough to shake. The combination of near-zero new development and positive net store openings since 2021 has driven occupancy rates to record-highs and allowed Strip Center REITs to enjoy some long-awaited pricing power. These favorable property-level supply/demand fundamentals have translated into impressive double-digit rent growth spreads since mid-2022 and the best earnings “beat rate” of any property sector during that time. Despite several high-profile retail bankruptcies - including Bed Bath & Beyond and Party City - store openings have continued to outpace store closings by 50% so far in 2023, led by demand for space in large-format open-air strip centers. A "higher for longer" monetary environment may be ideal for well-capitalized Strip Center REITs with the balance sheet firepower to accretively consolidate as debt-dependent private owners seek an exit.

{kind=link}

Hoya Capital

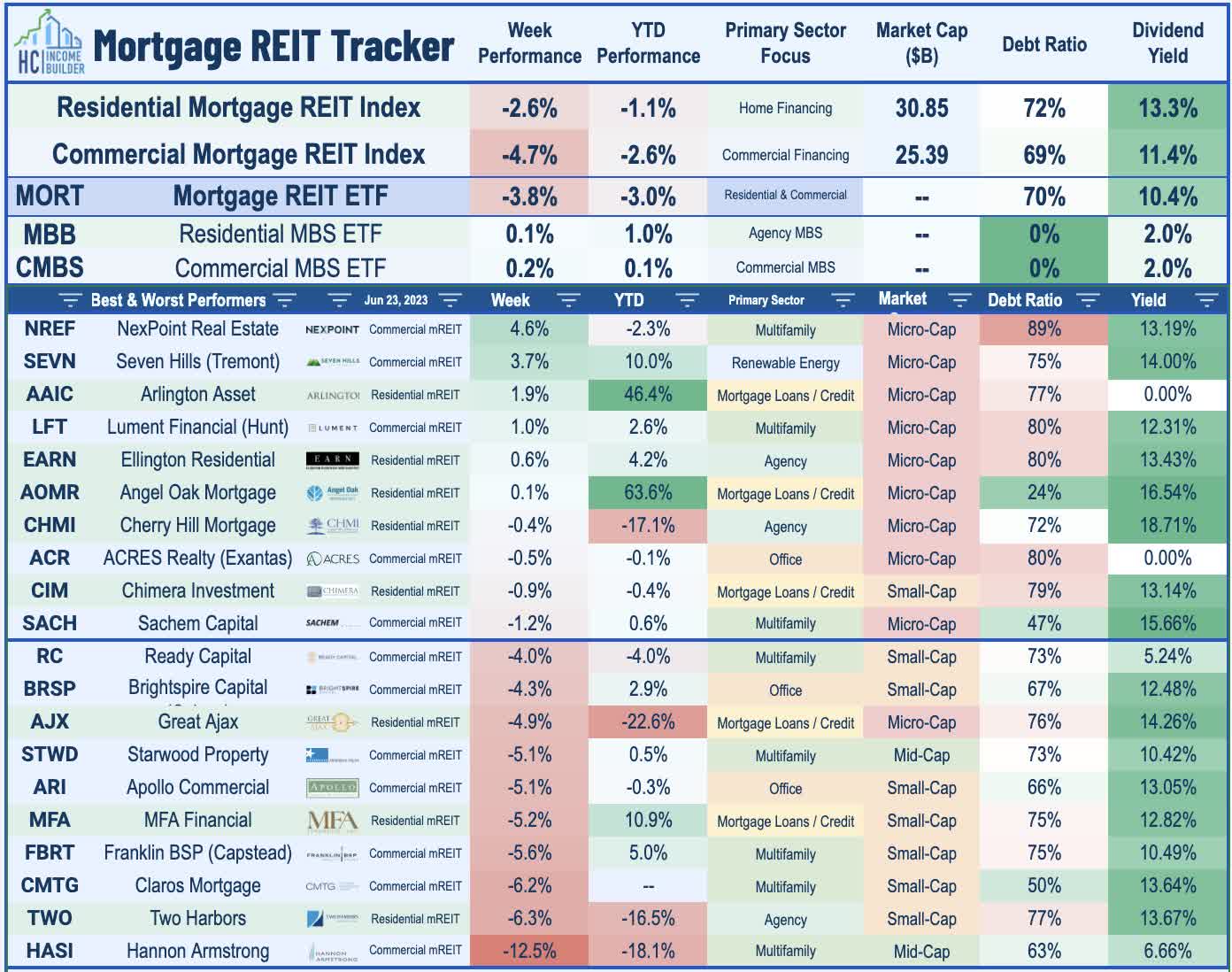

Mortgage REIT Week In Review

Mortgage REITs slumped this week following a three-week rally of over 12% that had pushed the mREIT benchmark into positive territory on the year. The iShares Mortgage REIT ETF ( REM ) slipped 3.8% this week, with particularly sharp pressure on commercial mREITs. Arbor Realty ( ABR ) was among the upside standouts after S&P announced that it would be added to the S&P Small-Cap 600, becoming the fourth commercial mortgage REIT included in one of the three major S&P benchmarks. Arbor has now gained over 30% since early April, a rebound that follows a sell-off earlier in the year sparked by short calls from several firms, including Hedgeye and Ningi Research . On the downside this week, Two Harbors ( TWO ) slumped more than 6% after it trimmed its dividend yield by 25% to $0.45/share , representing a dividend yield of 12.9%. The reduction - which marks the 10th dividend cut within the sector this year - came as somewhat of a surprise given that TWO's payout ratio was 102% in Q1, which at the time the company commented was "reflective of the return potential of the portfolio."

{kind=link}

Hoya Capital

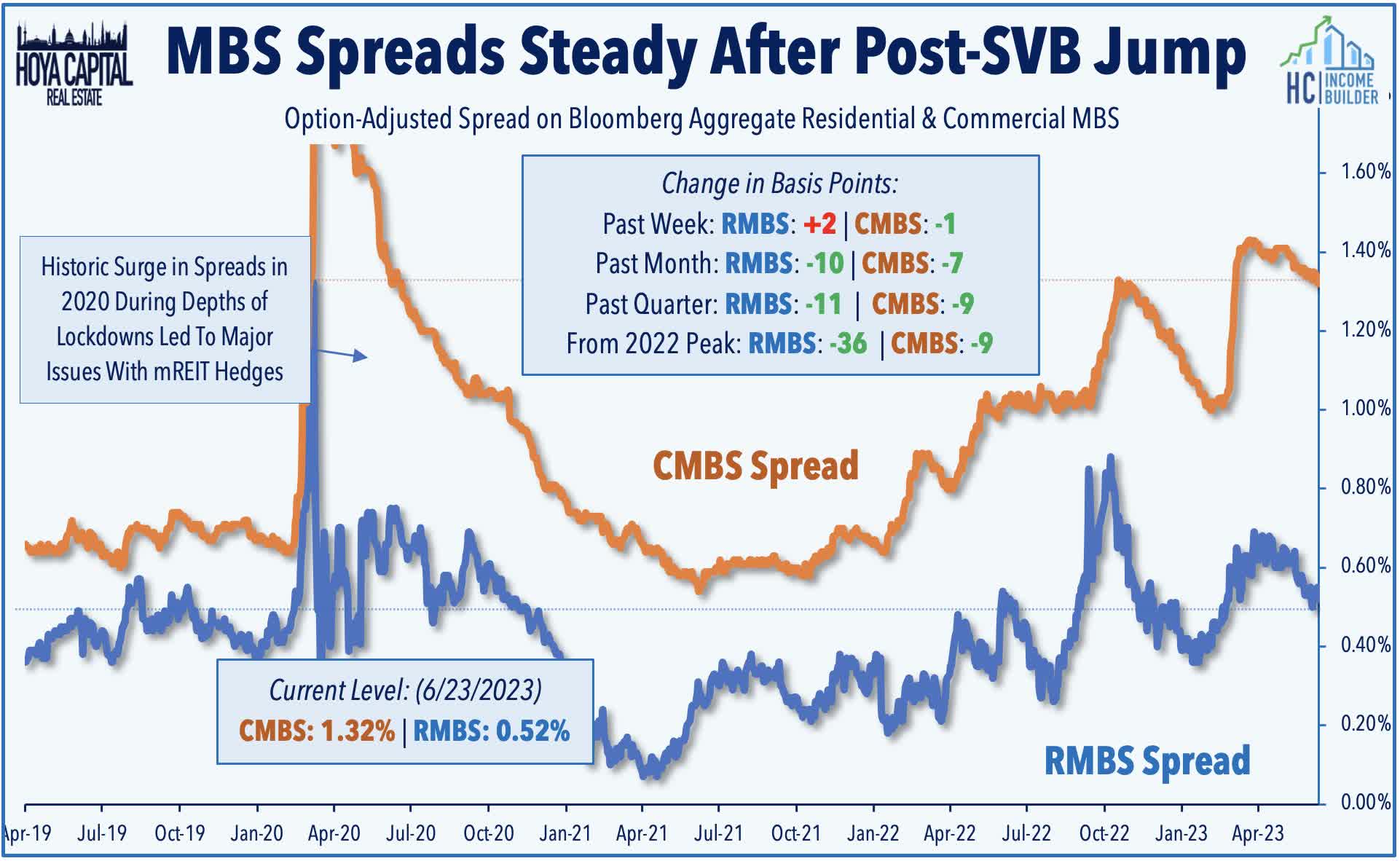

The other half-dozen REITs to declare dividends held their dividends steady: Invesco Mortgage ( IVR ) held its quarterly dividend steady at $0.40/share (13.9% dividend yield), Western Asset ( WMC ) held its quarterly dividend steady at $0.35/share (15.6% yield), Granite Point ( GPMT ) held its dividend steady at $0.20/share (15.4% yield), Franklin BSP Realty ( FBRT ) maintained its quarterly dividend (15.5% yield), and Ellington Financial ( EFC ) held its monthly dividend steady at $0.15/share (13.5% yield). Ellington Financial also reported yesterday at that its estimated book value per share stood at $14.55 as of May 31, which is down about 3.6% from the $15.10 level at the end of Q1. Spreads on mortgage-backed bonds ("MBS spreads") have narrowed following the surge in the wake of the Silicon Valley Bank collapse in early March. At 0.52%, Residential MBS spreads have tightened by about 10 basis points since the end of Q1. Commercial MBS spreads are still relatively elevated at levels that are roughly even with their 2022 highs at 1.32%, but down about 10 basis points since the end of Q1.

{kind=link}

Hoya Capital

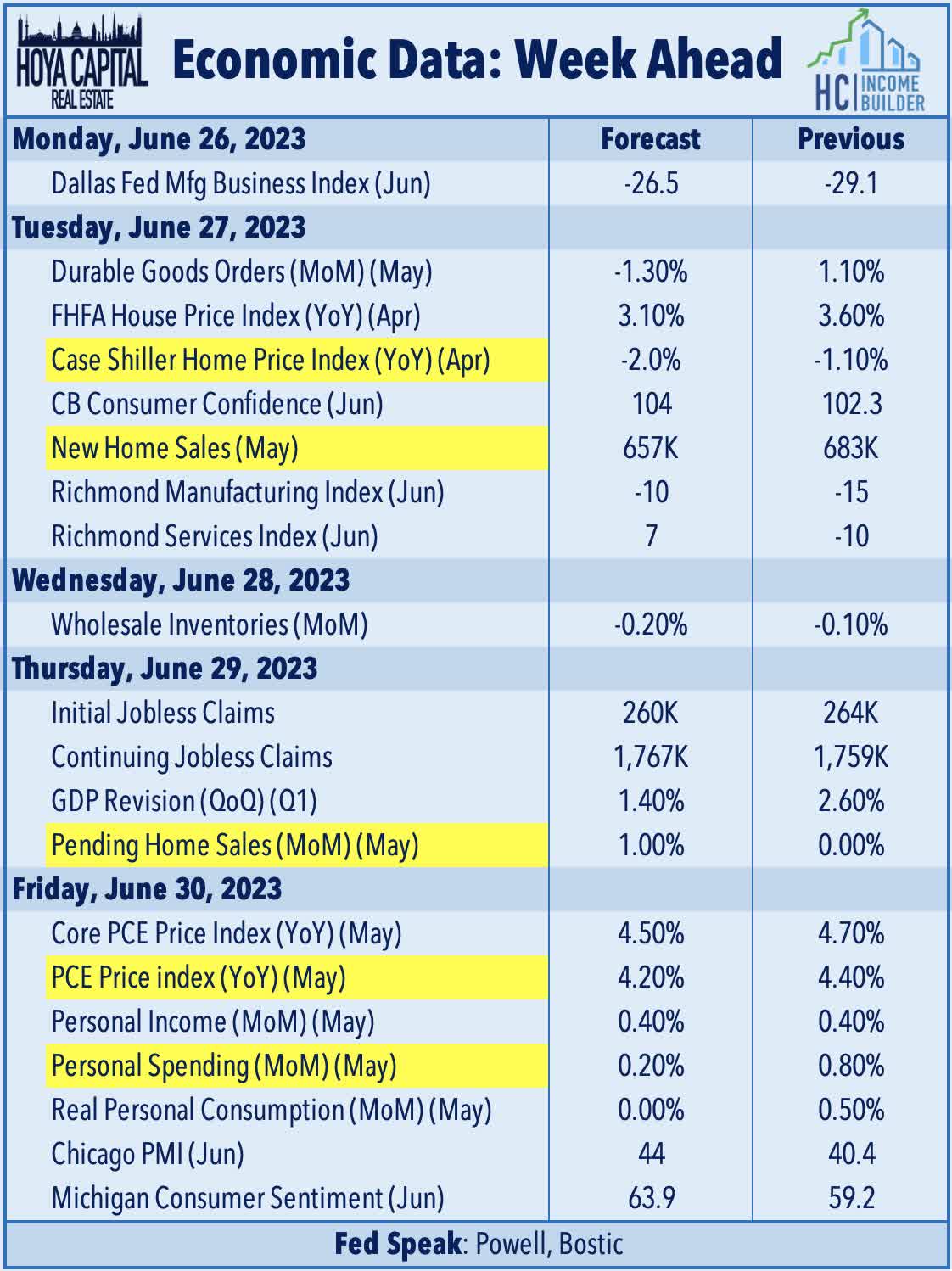

Economic Calendar In The Week Ahead

We'll see another fairly busy week of economic data in the week ahead. The state of the U.S. housing market remains in focus early in the week. On Tuesday, we'll see New Home Sales data for May, which last month posted the first year-over-year increase in two years. We'll also see home price data with the Case Shiller and FHFA releasing data for April, which are both expected to show a modest year-over-year decline in home values as downward pressure from higher mortgage rates has been partly offset by the effects of historically low housing supply levels. We'll see some more housing data on Thursday with Pending Home Sales data, which is expected to increase for the fifth month out of the past six following a stretch of thirteen straight monthly declines. The most important report of the week comes on Friday with the PCE Price Index - the Fed's preferred gauge of inflation - which is expected to show a continued moderation in price pressures. In the same report, we'll also be looking at Personal Income and Personal Spending data for May, a key read on the state of the U.S. consumer.

{kind=link}

Hoya Capital

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

Hoya Capital

For further details see:

Rally Fades After Fed Warning