RL - Ralph Lauren Corporation: Favored By Strong Tailwinds

2023-04-26 17:19:33 ET

Summary

- Ralph Lauren Corporation has benefited from a strong brand, steady demand, and channel development.

- Ralph Lauren also possesses attractive attributes that, when considered alongside the company's growth drivers, I think can excite investors.

- An adverse economic situation is a significant risk to the company's prosperity; therefore, potential Ralph Lauren Corporation investors should keep an eye on that.

Investment Thesis

Ralph Lauren Corporation ( RL ) creates, markets, and distributes clothes, footwear and accessories, home goods, fragrances, and hospitality products. RL has benefited from a strong brand, steady demand, and channel development. Good AUR (average unit retail) growth and a solid online show portend well for the company's future expansion.

In addition to these potent development levers, RL possesses attractive attributes that, when considered alongside the company's growth drivers, can excite investors. These appealing qualities are its outstanding results and the ROE trend. In light of these elements, I find that the company has solid fundamentals, which prompts me to be bullish on the stock.

RL Growth Drivers: Very Solid And Reassuring

Growth is crucial for cutthroat businesses, and companies like RL compete. Given this context, it is encouraging to see that this business is taking advantage of solid growth levers, which are, in my opinion, very efficient and rewarding and supported by its performance. Below are its major growth levers.

1. Solid Online Show

Ralph Lauren has invested in mobile, omni-channel, and fulfillment to advance its digital and omni-channel capabilities significantly. Digital business remained a major growth engine in the second quarter of fiscal 2023, increasing digital sales in all regions.

{kind=link}

The worldwide digital economy has kept expanding, with sales up by the mid-teens over the previous year. This includes expansion in the mid-single digits across all Ralph Lauren-owned digital properties, which follows expansion of over 30% in just the prior year.

In the second quarter of the fiscal year, the corporation launched new digital properties in strategic countries like Korea and Australia. Strong full-price selling, resulting from a favorable product mix, investments in AI-powered targeting, and consumer acquisition, all contributed to a year-over-year revenue increase for the company's owned digital sites in the mid-single digits. More than 50 million people around the world are connected to it through social media, and its internet search has grown by low double digits annually.

Ralph Lauren's linked retail capabilities, such as virtual selling appointments, "buy online, pick up in store," and unlimited aisle product availability, continue to grow at an impressive rate. The company released its first-ever full catalog Ralph Lauren mobile app, effectively using its connected retail capabilities to provide the most individualized and content-rich platform.

2. AUR Growth

One of the most important growth drivers is the steady increase in AUR. For the second quarter of fiscal 2023, the AUR rose by 18%, making it 22 consecutive quarters of growth. With a robust product mix and pricing power, the company has been able to weather the prolonged inflationary climate. It anticipates exceeding its long-term target of annual AUR growth in the low to middle single digits through fiscal 2023, which will assist offset cost inflation in the middle to high single digits.

Its long-term AUR growth is projected to be supported by its strategy of product elevation, acquisition of full-priced consumers, advantageous channel and geographic mix, and ramping up of targeting and customization activities. This is expected to continue fostering the expansion of the gross margin. For fiscal 2023, good AUR growth and a positive product mix are expected to cause the gross margin (at cc) to expand by 30-50 bps on a 52-week comparative basis. This is anticipated to mitigate the effects of rising freight and product costs significantly.

Considering all of these variables makes it easy to see why I'm optimistic about the company's future. RL has launched the second phase of its Next Great Chapter : Accelerate plan, which will streamline the company's global operations and introduce new technological capabilities to boost its growth pillars.

Its portfolio realignment announced last year has been finalized with the completion of the first step of the strategy, which involved the transition of Chaps to a licensed firm. As part of its aim to elevate itself for its Next Great Chapter, this shift will allow it to concentrate on its most influential brands.

On a 52-week comparable basis, RL expected fiscal 2023 revenue growth in the upper single digits, or 8% (cc). The firm anticipates year-over-year sales growth in the low to mid-single digits at cc for the third quarter of fiscal 2023.

What Do The Numbers Say?

Given the aforementioned strong and promising growth levers, we can only estimate their output by extrapolating from the company's performance. These variables have caused RL to experience a strong surprise trend, which persisted in the second quarter of fiscal 2023. In the second quarter of its fiscal year, the company posted its ninth consecutive earnings beat and seventh consecutive revenue surprise. To $1,579.9 million, net revenues increased 5% from the previous year. Constant-currency [cc] revenue growth over the same quarter last year was 13%. The indicator saw a strong rise in every region. Guided by this data, I am justified to assert that the company's future growth is bestowed in safe havens.

The ROE-Earnings Interplay

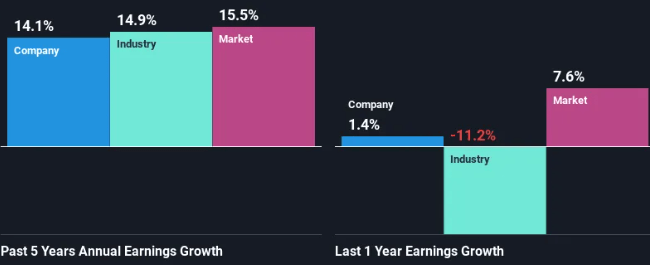

Return on equity [ROE] quantifies a firm's profitability. The extent to which a company's profits are reinvested (or "retained") for future expansion is a crucial indicator of such growth's potential. If everything else is equal, a company with a higher ROE and stronger profit retention will outperform competitors that lack these features.

To begin with, its 21% ROE seems reasonable. When compared to the average ROE in its industry of 16%, the company's returns look even better. This was likely the seed that sprouted the moderate net income growth of 14% experienced by Ralph Lauren over the past five years.

Earnings growth is a primary factor in determining a company's value. RL has a healthy mix of a moderate three-year median payout ratio of 33% (or a retention ratio of 67%) and a decent amount of growth in earnings, as shown below. This means that the company has been making good use of its profits.

{kind=link}

Overall, I'm satisfied with Ralph Lauren's performance. I appreciate the strong return rate the company is getting from its reinvestment efforts. This has resulted in rising profits.

Risk

RL appears to be an attractive opportunity, but economic conditions on their major consumers, suppliers, vendors, and lenders, including the COVID-19 epidemic, and their capacity to access global financing markets cannot be forecast. Major manufacturers may fail to meet customer delivery dates if they can't ship. Deterioration in global financial or capital markets could affect its ability to access liquidity to meet future cash needs, increase the cost of future financing, or prevent its lenders from meeting their funding commitments under their credit and overdraft facilities. A disruption in the ability of its significant customers to access liquidity could cause serious disruptions or an overall deterioration of their businesses, which could lead to a significant reduction in their future orders of our products and the inability or failure to meet their payment obligations to them, all of which could have a material adverse effect on their business.

Conclusion

Despite unfavorable economic conditions, Ralph Lauren Corporation's brand strength, high demand, solid online show, and significant AUR growth position the company well for long-term success. Therefore, I recommend Ralph Lauren Corporation stock to growth investors as a buy.

For further details see:

Ralph Lauren Corporation: Favored By Strong Tailwinds