RL - Ralph Lauren: Earnings Growth Not Factored Into Price Yet

2023-08-16 04:31:25 ET

Summary

- Ralph Lauren's stock price has dropped 5% in the past week, coinciding with the release of its Q1 FY24 earnings report.

- The company's revenue growth in Q1 FY24 was slow, but it saw an encouraging margin expansion.

- The outlook for the company indicates both revenue growth and expanded margins from last year, but it doesn't reflect in the price yet.

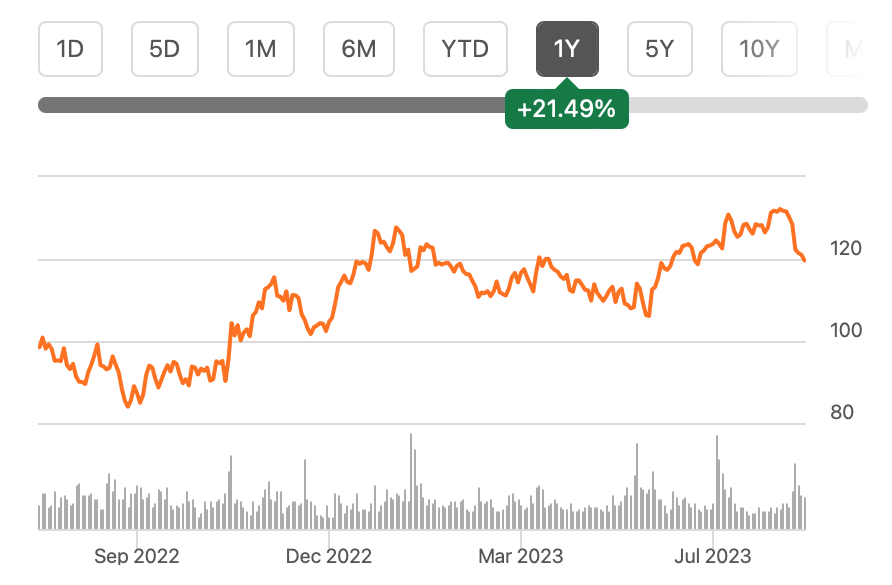

High end fashion brand Ralph Lauren ( RL ) has seen a 5% drop in stock price over the past week, which coincides with the time since the release of its results for the first quarter of fiscal year 2024 (Q1 FY24). In fact, the stock saw its biggest drop of 4.8% in 2023 so far on the release day.

{kind=link}

Here I take a closer look at these numbers to figure out whether there’s now a risk of RL getting derailed after a strong 21.5% over the past year. This is more significant than it might appear on the surface for two reasons.

One, it’s shown far superior performance to the S&P 500 consumer discretionary index, which has basically remained flat over this time, which to my mind puts it at some risk anyway. And two, it marked a break from RL’s dismal historical performance, which saw it lose 9% value over the past five years and over 30% value in the past decade.

The results

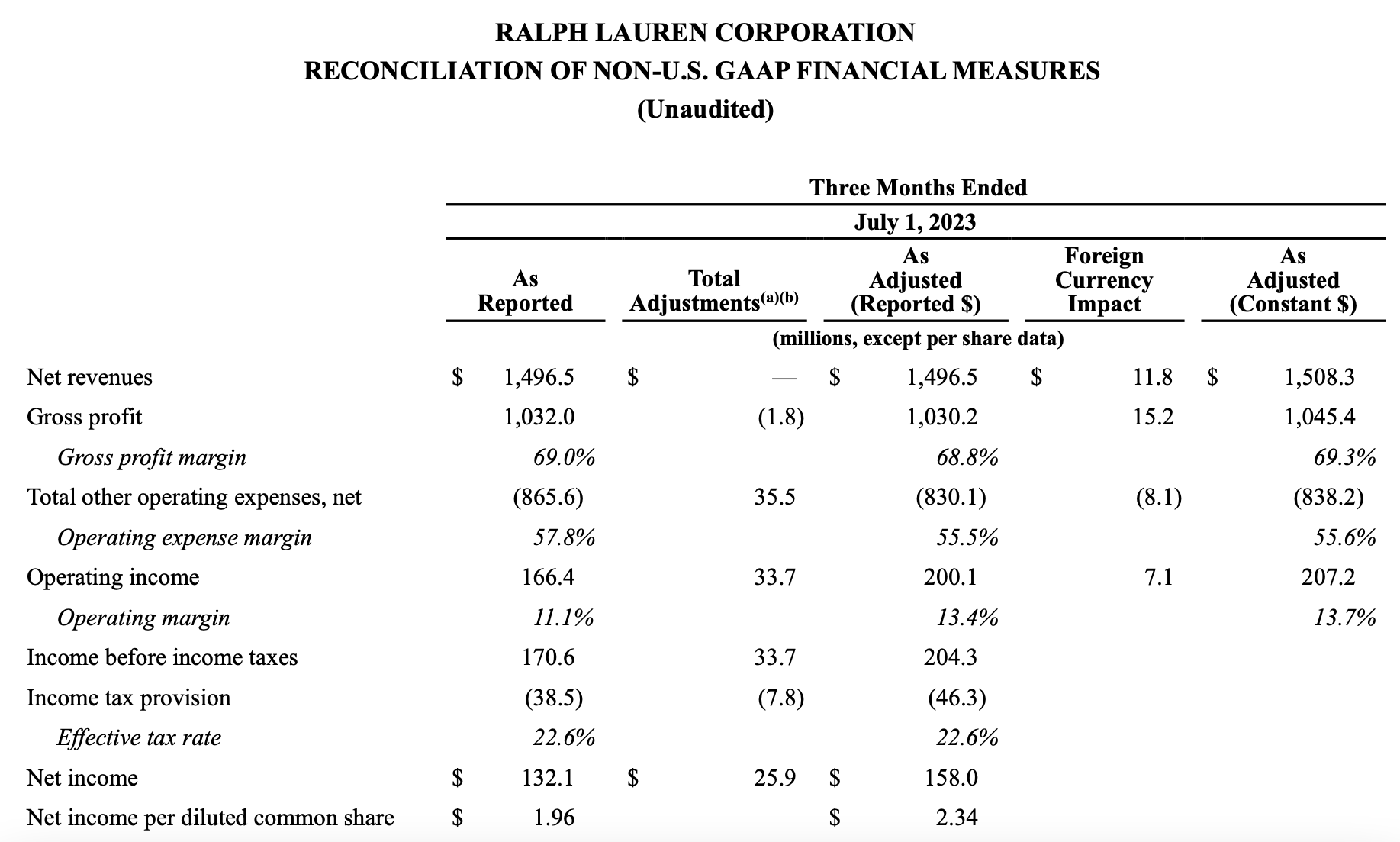

The reason for investor disappointment with the result isn’t hard to find. The company’s revenues grew by just 0.4% year-on-year (YoY) in Q1 FY24 (three months ending July 1, 2023), the slowest growth in 10 quarters. And even before that, revenues had shrunk only because of the pandemic.

It’s not all bad, though. There was a negative foreign exchange impact of 80 basis points on revenues. If there wasn't an impact, the company would have seen revenue growth at the same level as last quarter. Next, at constant currency it has seen a 1% rise, implying that some genuine demand increase.

{kind=link}

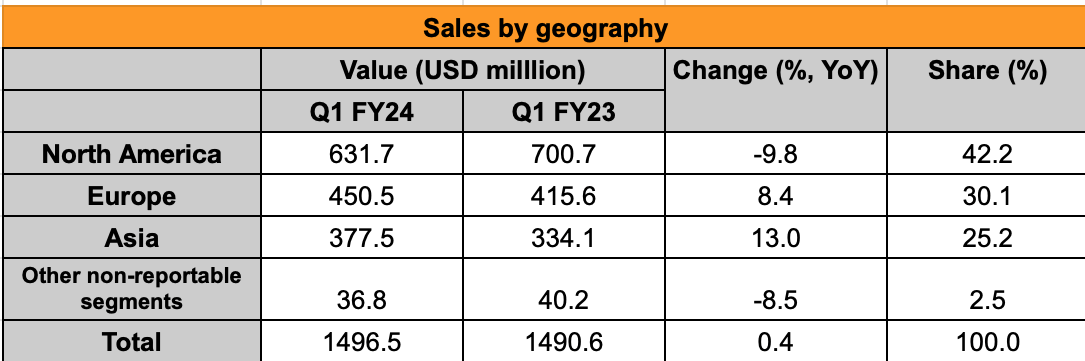

Finally, the big drag on its growth comes from its North American market. It’s not alone in this. Luxury fashion companies like LVMH ( OTCPK:LVMUY ) and Kering ( OTCPK:PPRUF ) too have seen weak demand from the big US market in the last quarter. The challenge for Ralph Lauren though, is that first, the US is its biggest market with an over 42% share as of Q1 FY24.

Second, the drag itself is quite big at 9.8%. The company explains that a 5 percentage point negative impact stems from a shift of Spring product receipts to Q4 FY23, presumably creating a high base effect in the current quarter. And third, the pickup from the Asian market, in particular, isn’t big enough to make up for North America’s weakness (see table below), despite an over 50% increase in sales to China.

{kind=link}

Expanding margins

The big saving grace, however, is the margin expansion, another trend visible across companies’ earnings recently. A broad cooling off in inflation, but in particular the widening gap between producer price inflation and consumer price inflation has worked for margins.

Though in Ralph Lauren’s case, it appears that the company has adjusted well to the inflationary environment as well. It does point to lower freight costs, but also “favorable channel and geographic mix shifts” and the shift in marketing expenses to the next quarter as offsetting higher raw material, compensation and rent costs.

This has resulted in a rise in gross margin to 68.8%, the highest level seen in two years. The adjusted operating margin is the highest in six quarters at 13.4%. In fact, geography wise, the adjusted operating margins are even higher. Asia has the highest margins at 24.7%, followed by Europe at 21.5%, with both markets witnessing a rise in margins from Q1 FY23. Even the US, which saw a drop in margin by 60 basis points is at 19.6%. However, items like unallocated corporate and restructuring expenses proved to be a drag on the overall margins.

Outlook and market multiples

The company’s outlook is unchanged from earlier, and it doesn’t look too bad. It expects revenue growth to be negatively impacted by 20 basis points. For context, last year, the number was at 4% . Even with the impact, though, it looks like an improvement over Q1 FY24’s figures. It also expects the operating margin at constant currency to expand by 30 to 50 basis points this year, from 13.7% last year.

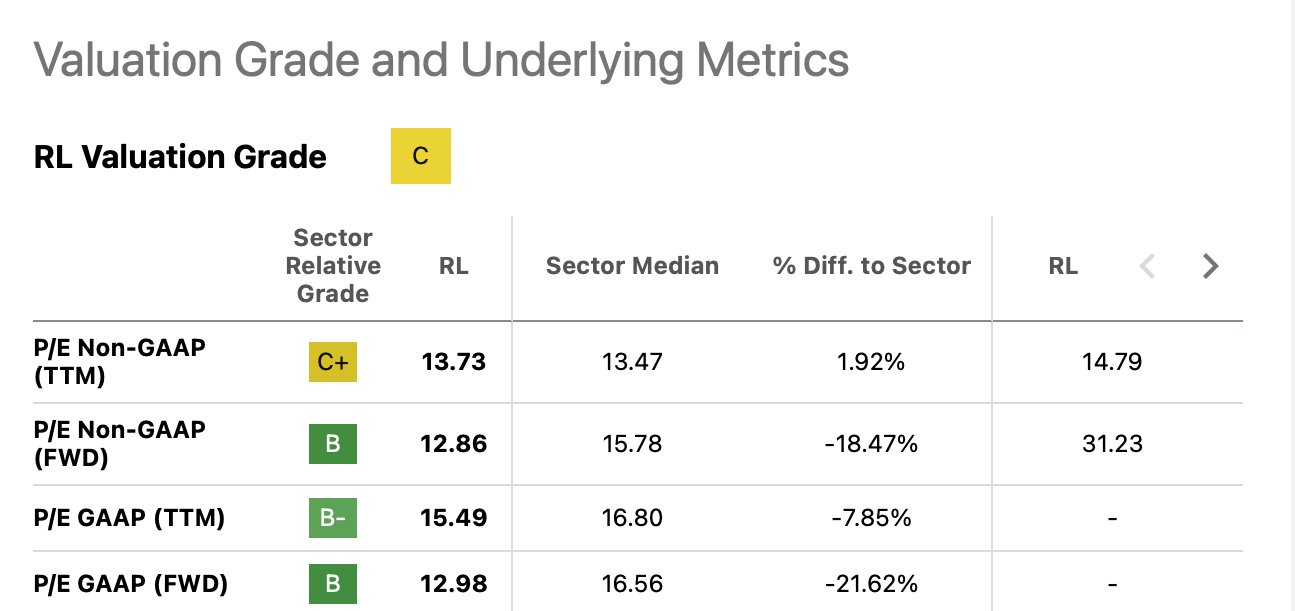

Assuming that the expansion in adjusted operating margin is the same as that for operating margin at constant currency and that net income stays at 75% of operating income as last year, yield a forward non-GAAP price-to-earnings (P/E) ratio of 12.8x for RL. This is close to analysts’ estimates, whose estimates give 12.9x figures. Both estimates are much lower than the 31.2x figure seen on average for the past five years.

The trailing twelve months [TTM] P/E ratio is also lower than the past average, albeit to a lesser degree (see table below). Just based on this ratio, there’s at least a 15% upside to the stock right now.

{kind=link}

It is trading at a higher P/E than peers like Versace and Jimmy Choo owner Capri Holdings ( CPRI ), Tapestry ( TPR ) of brands like Coach and Kate Spade and V.F. Corporation ( VFC ) of North Face and Timberland, but then its recent revenue and net income growth has also been largely superior (see Growth table under link).

What next?

Ralph Lauren’s latest numbers appear more underwhelming than they really are. Revenue growth has been impacted by both exchange rate differences and a change in the timing of receipts. It would have looked relatively healthier otherwise.

Even its operating margins, which have improved in any case, actually look quite impressive when seen from a geographical perspective. They are dragged down only by other costs. Also, the company’s also doing a good job of managing costs, and with some cost pressures declining, this has resulted in margin expansion.

Both gross and operating margins are set to increase for the full year as well, and the net income can be expected to rise too. But this projected increase isn’t yet factored into RL’s share price, which is trading at rather low multiples.

It looks doubtful that the stock can go back to the kind of forward multiples seen in the past few years, but there's nothing in the fundamentals to suggest or multiples a downside. If anything, there's further upside here. I’m going with a Buy on Ralph Lauren stock.

For further details see:

Ralph Lauren: Earnings Growth Not Factored Into Price Yet