RL - Ralph Lauren: Increased Marketing Spend Could Pay Off

2023-12-30 01:32:49 ET

Summary

- Ralph Lauren's stock has rallied in recent times, likely frontrunning a likely great Q3 holiday performance.

- The brand has had turbulence in the past couple of decades with the brand equity changing with fashion trends.

- A possible return into growth could improve Ralph Lauren as an investment case, but for the time being, I estimate very slight growth implying a slightly overpriced stock.

Founded in 1967, Ralph Lauren (RL) manufactures and sells clothing under many clothing lines within the Ralph Lauren brand, focusing on mostly quite expensive end on the price range. The brand is most well-known for its classic and timeless style.

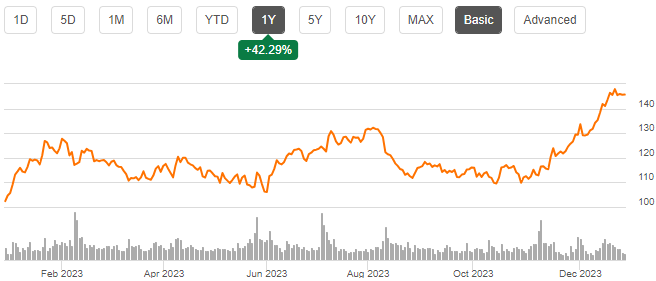

The stock has recently rallied quite well, going from around $110 to a price of $145.70 at the time of writing. Moreover, the one-year return on the stock is 42% after a decade of poor stock performance. The company also returns some capital through dividends, with a current yield of 2.06% .

{kind=link}

Financials – Turbulence in Brand Equity

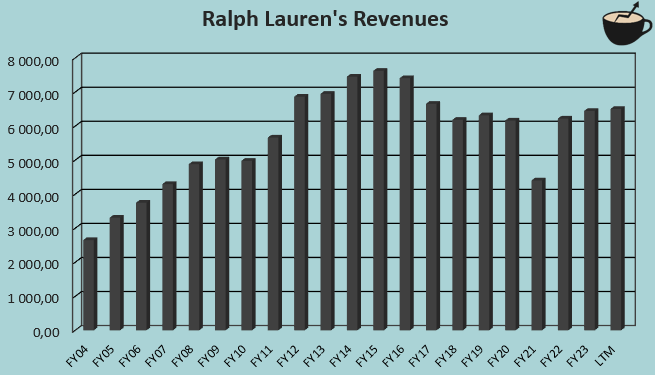

Trends in fashion can clearly be seen from Ralph Lauren’s long-term revenue history. The company’s FY2004-LTM revenue CAGR of 4.7% was mainly achieved in the 2000’s – from FY2004 to FY2015, the CAGR is 10.1%. Since, the brand seems to have fallen out of style, as revenues have fallen into a lower level from the high, with decreases from FY2016 to FY2018. Demand for the brand seems to have since stabilized, excluding the Covid pandemic’s negative effect for revenues in FY2021.

{kind=link}

As a high-end product, Ralph Lauren has decent margins. The company’s gross margin stands high at a current figure of 65.3% , near LVMH Moët Hennessy’s trailing gross margin of 68.7% . Due to high marketing and other SG&A expenses, though, the achieved EBIT margin isn’t very special – prior to the pandemic, and currently, the company has achieved mostly stable low double-digit figures. Currently, the company’s trailing EBIT margin stands at 11.0%.

Possibly Back in Fashion

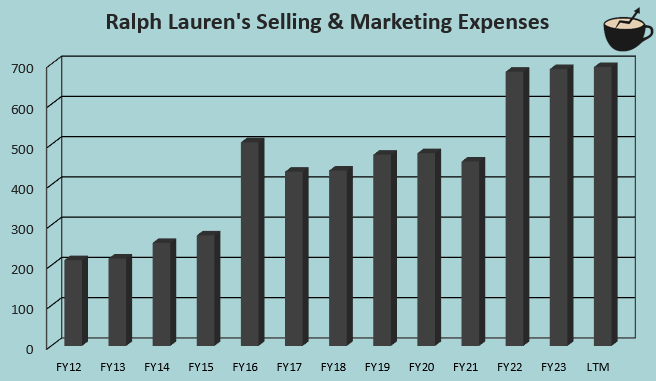

After the brand equity seems to have taken a dive, the brand seems to have stabilized in recent years. I believe that a return to growth could even happen for the company – from FY2022 forward, Ralph Lauren has increased its selling & marketing spend considerably. As is told by CEO Patrice Louvet in the company’s Q2/FY2024 earnings call , Ralph Lauren has recently had sponsorships in notable sports events including the US Open, Wimbledon, and Ryder Cup.

{kind=link}

The spend seems to have started having an effect on the brand. Interest in the brand seems to be on the rise if Google Trends is taken as an indicator. Searches for Ralph Lauren seem to have started increasing , as the indexed holiday season search peak for 2023 is around 19% above the peak achieved in 2022.

{kind=link}

I don’t necessarily think that the search volume is a very clear indicator for better revenues, but the rising interest during the holiday season does signal a possibly great Q3/FY2024 performance. The recent stock rally seems to frontrun the quarter as well; I’d guess that a great performance in Q3 is priced in with the rally, and doesn’t really provide an opportunity for an opportunistic play.

On the other hand, if Ralph Lauren’s better brand visibility rises further even after the holiday season above previous years’ level, the branding could signify a return to a longer-term growth path for the company, a result that the company is striving for. At the moment, I don’t see a long-term extrapolation as reasonable even if the reported Q3 result shows good growth – I would want to see a few quarters of good growth before factoring in a good long-term growth level.

A Reasonable Valuation

Ralph Lauren currently trades at a forward P/E multiple of 14.5, faintly below the ten-year average of 16.5; the small difference can be explained by currently higher interest rates, raising investors’ required rate of return.

{kind=link}

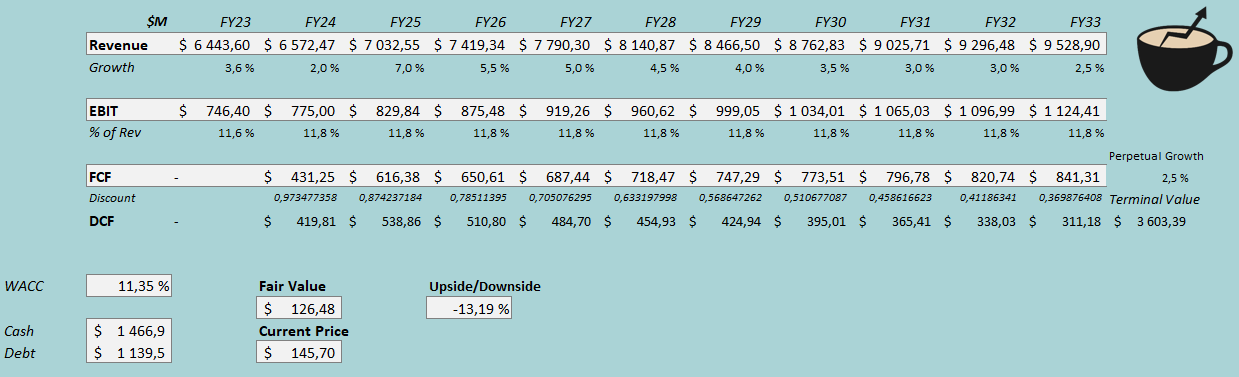

To estimate a rough fair value for the stock, I constructed a discounted cash flow model. In the model, I factor in some growth, but not at a level that Ralph Lauren achieved in the 2000’s – after a FY2024 growth of 2%, I estimate the growth to accelerate into 7% as the macroeconomic situation should improve at some point increasing demand, and as Ralph Lauren’s marketing initiatives could show greater results. Afterwards, I estimate the growth to slow down into a perpetual rate of 2.5%, representing a total revenue CAGR of 4.0% from FY2023 to FY2033.

I don’t see significant factors driving a better profitability for Ralph Lauren. Although an improved marketing could improve same-store sales, increasing margins, I don’t see such a scenario as likely to be significant. For FY2024, I estimate an EBIT margin of 11.8%, that continues into perpetuity. Ralph Lauren does have a plan of increasing the average unit selling price, but the strategy’s contribution to margins should be quite minimal, as higher prices are likely to result in lower sold units.

With the mentioned estimates along with a cost of capital of 11.35%, the DCF model estimates Ralph Lauren’s fair value at $126.48, around 13% below the stock price at the time of writing. The company’s valuation seems to suggest some long-term growth after the recent stock rally, and I believe that the currently priced-in scenario is a very slight overvaluation, but not a terrible gap.

{kind=link}

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In the most recent reported quarter, Ralph Lauren had $10 million in interest expenses. With the company’s current amount of interest-bearing debt, Ralph Lauren’s annualized interest rate comes up to 3.51% - the company seems to have secured low-interest debt. Unfortunately, the company only has quite a modest amount of the cheap debt; I estimate a long-term debt-to-equity ratio of 15%. For the risk-free rate on the cost of equity side, I use the United States’ 10-year bond yield of 3.89% . The equity risk premium of 5.91% is Professor Aswath Damodaran’s latest estimate for the United States, made in July. Yahoo Finance estimates Ralph Lauren’s beta at a figure of 1.45 . Finally, I add a small liquidity premium of 0.2%, crafting a cost of equity of 12.66% and a WACC of 11.35%.

Takeaway

Ralph Lauren has had some long-term revenue turbulence with fashion trends. The recent stock price rally seems to frontrun a great upcoming Q3 result including the holiday season sales, which seems likely in my opinion, as the Google search volume for Ralph Lauren has been great in the period. The company’s increased marketing spend could prove successful with a better long-term growth than the company has achieved in recent years, but for the time being, I am not yet very confident in a great performance with the currently shown financial performance. With slightly accelerated growth, the stock seems very slightly overvalued. As the overvaluation is still quite small, and falls within a margin of safety, I have a hold rating for the time being waiting for potentially geared up growth.

For further details see:

Ralph Lauren: Increased Marketing Spend Could Pay Off