RL - Ralph Lauren: Not Quite The Company Of A Decade Ago

2023-07-13 10:12:55 ET

Summary

- Ralph Lauren has been going through a four-year business transformation, however, top and bottom line fundamentals are weaker than one decade ago.

- The company has rewarded its shareholders with returns of 31.58% over the last year.

- Cautious of increased competition, stagnant top line growth and ongoing market challenges.

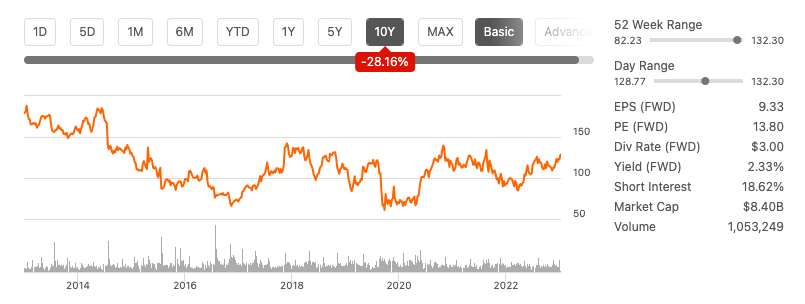

Ralph Lauren Corporation (RL) is considered a high-end consumer discretionary stock. Over the last four years, the company has gone through significant changes, most notably by pulling out of its off-price wholesale and retail revenue, which was considered brand dilutive, increasing digital spending and growing its DTC channel to attract a younger audience and improving margins. It is currently trading below its average price target of $132.32, and over the last year, shareholders have been rewarded with returns of 31.58%. However, we can see that the stock has declined over the previous decade.

Ten-year stock trend (SeekingAlpha.com)

{kind=link}

Despite improvements in operational changes, the company's top line has remained stagnant and cash flow has decreased over the past four years. Fundamentally, the company was stronger ten years ago. Due to ongoing economic market challenges and increased competition it is difficult to foresee major potential for growth in the near future. Therefore, my recommendation is to maintain a hold rating.

Company overview

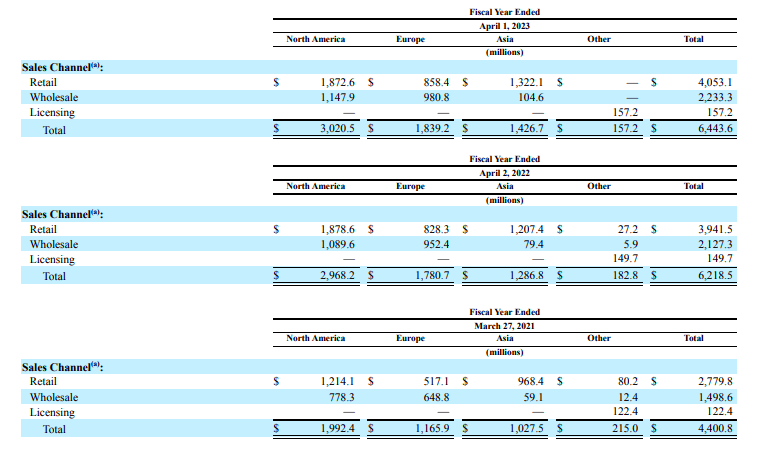

Ralph Lauren is an apparel manufacturer which was founded in 1967. The company has an impressive history of achievements it can be proud of, but equally, a few key hiccups, including brand-diluting licensing agreements, have impacted the brand's strength. Ralph Lauren generates income through retail, wholesale and licensing in North America, Europe and Asia. The company has struggled over the last decade with weakening top and bottom-line fundamentals. Four years ago, the management put a transformation operation in place with a focus on four strategies, namely reducing brand dilution by repositioning its retail, increasing digital presence, returning to the classics, which account for 70% of sales , and increasing customer value through DTC (direct-to-consumer) market strategies.

{kind=link}

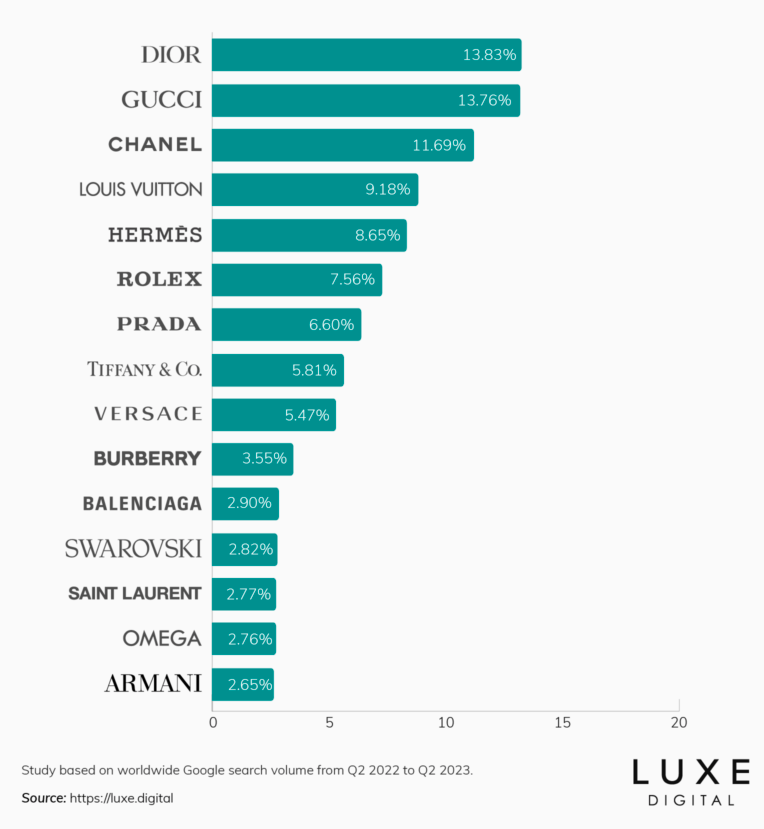

The transformation has positively impacted the business, including a 38% increase in DTC customers since 2019; DTC revenue attributes 63% to total revenue. The company has increased its average order size by 64% by reducing off-price wholesale and retail. It is focused on the growing high-end market in Asia, with a plan to add 200 new stores in the next three years, focusing on China. Furthermore, digital sales now account for 26% of total revenue, with a one-third target by 2025. While these are positive signs of a company focused on value creation, we cannot ignore that it is part of a highly competitive industry. Ralph Lauren failed to make the list of the top fifteen most popular luxury brands based on online search results in 2023.

Top luxury brands online (Lux.digital)

{kind=link}

Financials and valuation

By looking at Ralph Lauren's financials over ten years, we can see that revenue has remained stagnant, income has decreased, and cash flow has dropped. Over the last four years, in line with the business transformation led by CEO Patrice Louvet , we can see a slight increase in YoY sales, and gross profit margins have improved. In FY 2023, the company generated $6.44 billion, a slight increase from FY2020, which generated $6.159 billion.

Annual revenue (SeekingAlpha.com)

Over the past decade, the company has increased its gross profit margin from 57.85% to 64.89% TTM. However, if we examine the earnings from continuing operations, we can observe a decline over the same period, from $702.2 million to $522.7 million.

Annual earnings from continuing operations (SeekingAlpha.com)

Over the past decade, revenue has decreased, which has also led to a decline in net income. However, over the past four years, there has been an improvement in net income, despite a decrease in year-over-year sales from FY 2023 to FY 2022. FY 2021 was an exception, with a negative income of $121.1 million due to reduced sales activity caused by the COVID-19 pandemic.

Annual net income (SeekingAlpha.com)

Ralph Lauren was once known for its impressive ability to generate cash flow, but unfortunately, this strength has dwindled over the past decade and cash flow has become inconsistent. The company's levered free cash flow for FY 2023 has dropped to $112.7 million.

Annual levered free cash flow (SeekingAlpha.com)

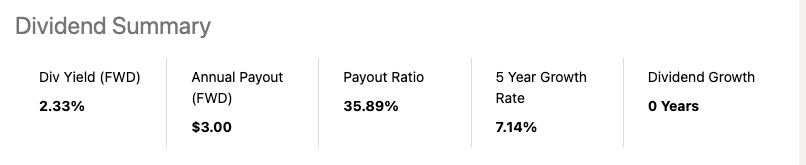

If we look at the company's capital structure, it is made up of 54% of total debt at $2.88 billion and 46% of total equity at $2.430 billion. The company's net debt is $1.3 billion, and $1.57 billion of total cash on the balance sheet. It has a healthy balance sheet with strong liquidity if we see its current ratio at 2.23 and quick ratio at 1.44. The company started paying a dividend in 2003, although it suspended its dividend in 2020 due to COVID-19. It has an FWD dividend yield of 2.33% at a solid payout ratio of 35.89%. The next payout is on 14 July 2023.

Dividend summary (SeekingAlpha.com)

{kind=link}

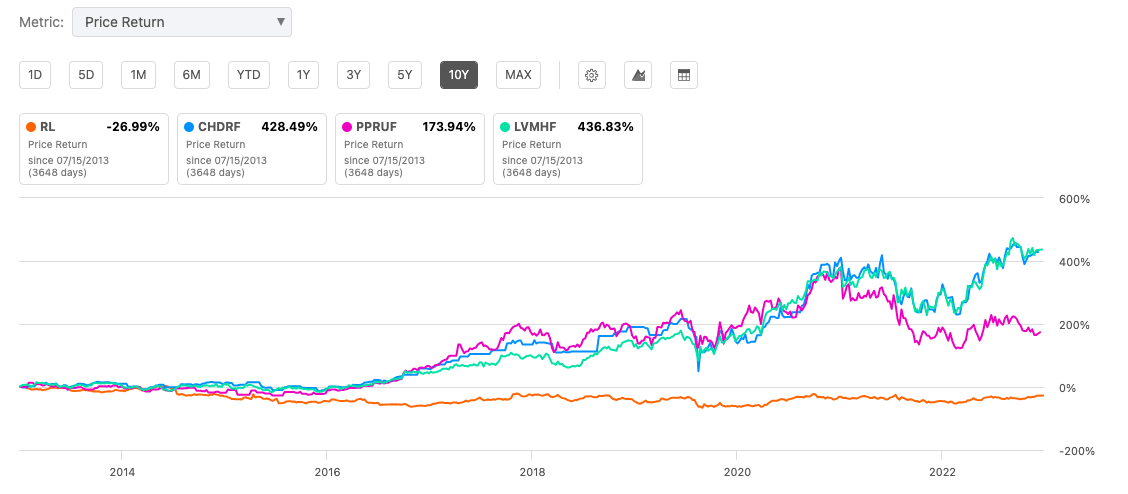

Over the last year, the stock price has increased by 42.54% and is trading near its average target price of $132.32. Investors should be cautious of the high short-interest rate of 18.62%, indicating a negative sentiment towards the stock. If we compare the stock to some of the most popular luxury brands online, namely Christian Dior (CHDRF), Gucci (PPRUF) and Louis Vuitton (LVMHF), we can see that Ralph Lauren has been the least rewarding stock to hold over the last ten years with negative returns of 26.99%.

Ten year stock trend versus peers (SeekingAlpha.com)

{kind=link}

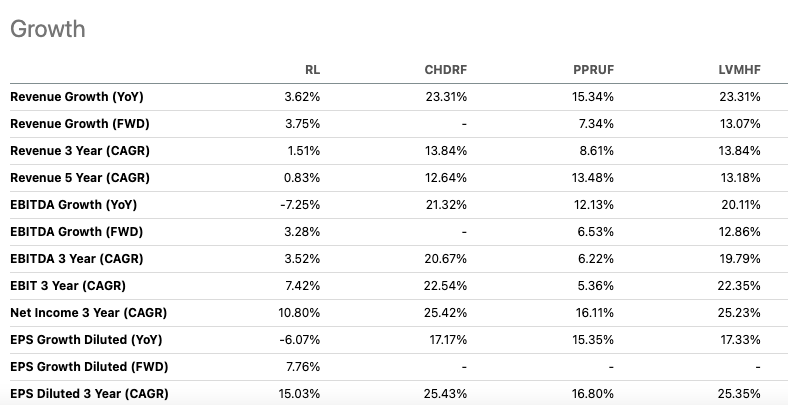

When compared to its competitors, Ralph Lauren's growth has been weaker in both the short and long term. Its revenue growth over the last five years was only 0.83%, while its peers experienced double-digit growth. Additionally, Ralph Lauren's EBITDA has declined year-over-year at 7.25%. It's important to note that some of the revenue slowdown may be attributed to a reduction in off-price revenue.

Relative peer growth comparison (SeekingAlpha.com)

{kind=link}

Although Ralph Lauren has seen an increase in gross profit margins, they still fall short compared to some of the bigger players in the industry.

Relative profitability comparison (SeekingAlpha.com)

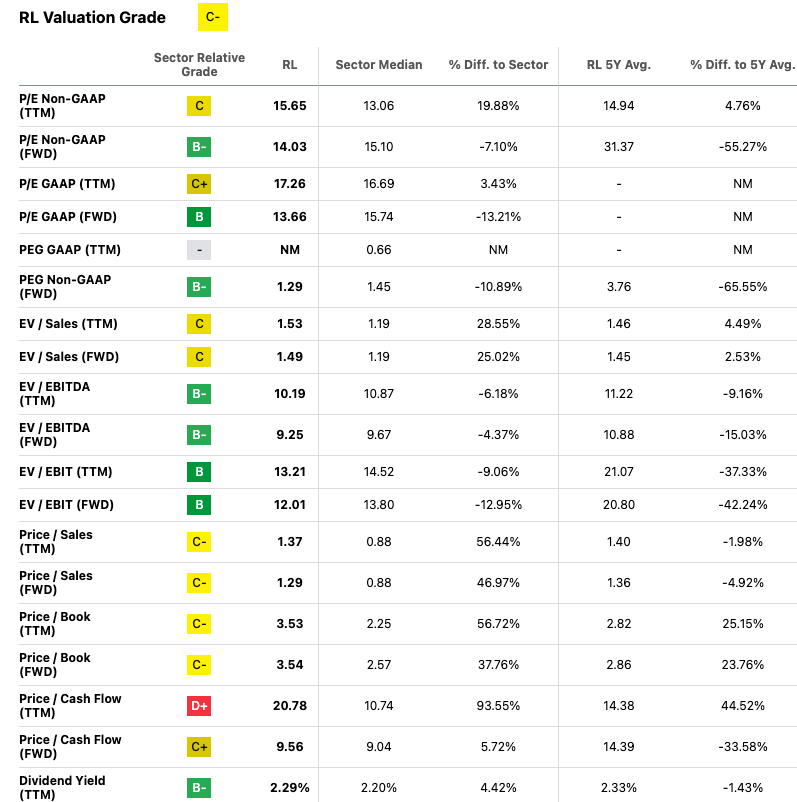

Based on Seeking Alpha's Quant rating system, Ralph Lauren has a C- valuation score compared to other companies in the consumer discretionary sector. The FWD price-to-earnings ratio of 13.66 is lower than the sector median of 15.74, which suggests that the stock may be undervalued. However, when we look at the TTM price-to-earnings ratio of 15.65, we can see that investors are currently paying more for the stock than its five-year average of 14.94.

{kind=link}

Risks

Although a hold rating suggests some level of stability, there is still a chance of financial loss if the stock value declines. The fashion industry is highly unpredictable due to the ever-changing consumer preferences. Moreover, macro-economic factors can also affect its global operations. Ralph Lauren primarily depends on their "classics" for revenue and has shifted their attention towards these enduring clothing pieces, which might offer more stability compared to other fashion stocks.

Final thoughts

Ralph Lauren is a well-known luxury American brand that has been striving to stay competitive by transforming its business. However, over the past decade, we have witnessed a decline in its top and bottom-line fundamentals. Despite a new management team actively implementing changes in the company, the brand, business, and stock have been less attractive than some of its bigger peers in the industry. Given the challenging economic climate and heightened competition, I suggest holding onto the stock for now with a neutral rating.

For further details see:

Ralph Lauren: Not Quite The Company Of A Decade Ago