RL - Ralph Lauren: Poised To Benefit From An Eventual Recovery In Demand

2023-08-20 20:52:37 ET

Summary

- Ralph Lauren has seen strong revenue growth in Europe and Asia, offsetting lower sales in North America.

- The company continues to show an attractive quick ratio and P/E ratio.

- The stock is in a good position to see a rebound if the appetite for North American luxury spending recovers.

Investment Thesis: In spite of lower North American sales, I see upside potential for Ralph Lauren based on strong Europe and Asia performance, as well as a strong balance sheet and an attractive P/E ratio.

In a previous article back in January, I made the argument that Ralph Lauren ( RL ) could see further upside going forward, on the basis of an attractive P/E ratio, strong revenue growth and favorable balance sheet metrics.

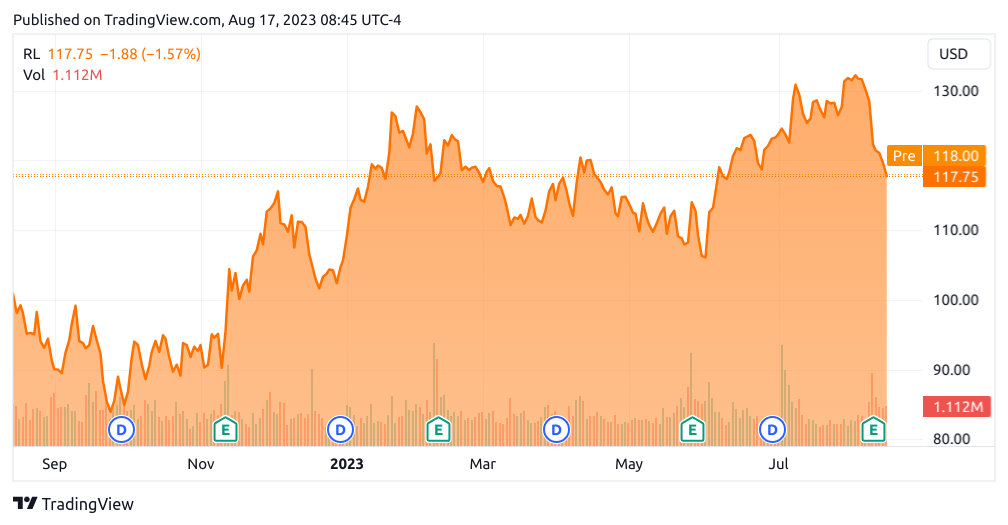

Since then, the stock has descended to a price of $117.75 at the time of writing:

{kind=link}

The purpose of this article is to assess whether Ralph Lauren has the ability to see continued growth from here taking recent performance into consideration.

Performance

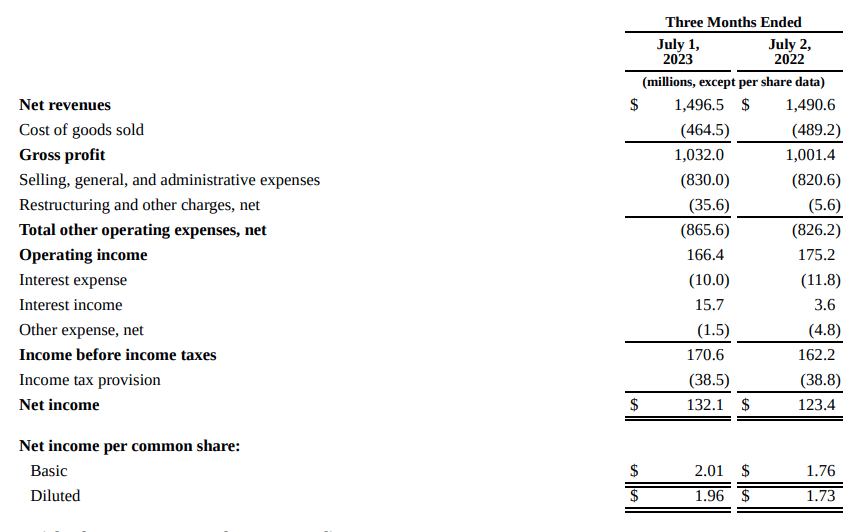

When looking at the most recent earnings results for Ralph Lauren, we can see that the company has seen modest growth in net revenues, with diluted net income per share up by 13% since the same quarter last year:

Ralph Lauren: First Quarter Fiscal 2024 Results

{kind=link}

From a five-year standpoint, it is notable that when comparing net revenue by region for Q1 2019 versus Q1 2024, the contributions of Europe and Asia to net revenue have been increasing, while that of North America has been decreasing:

Figures sourced from Ralph Lauren Q1 2019 and Q1 2024 Earnings Releases. Figures provided in millions of U.S. dollars. Heatmap generated by author using Python's seaborn library.

Additionally, when looking at digital commerce versus brick and mortar sales across these regions, we can see that both showed a decline across North America - while digital commerce far outpaced that of brick and mortar sales in Europe. Asia showed strong growth across both sales channels.

Ralph Lauren: First Quarter Fiscal 2024 Results

Including other non-reportable segments, Europe and Asia now account for 55% of total net revenues, whereas both regions accounted for 43% of total net revenue in Q1 2019.

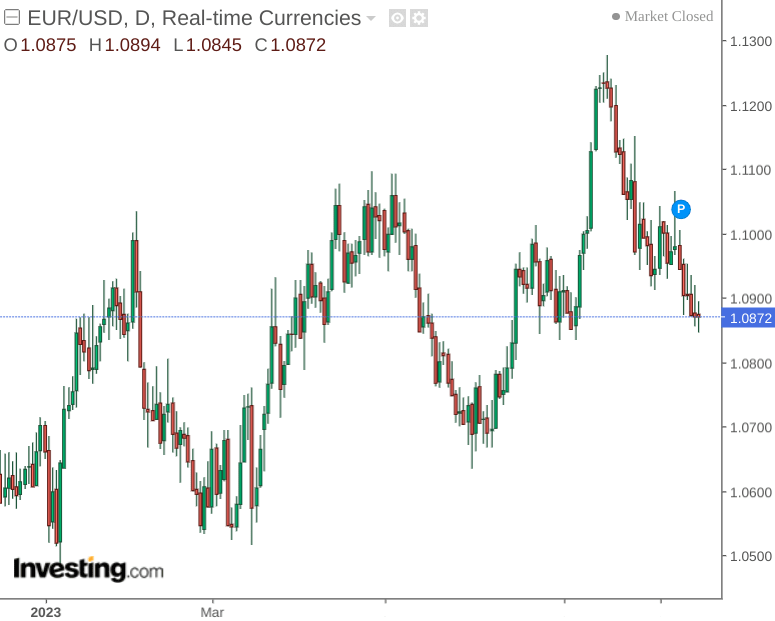

For this quarter, foreign currency fluctuations had negatively affected revenue growth by an estimated 80 basis points. We can see that the euro has gained significant strength against the U.S. dollar since the start of this year.

{kind=link}

A weaker dollar negatively affected the company's adjusted operating margin rate across Europe and Asia - down by 40 and 70 basis points across these regions, respectively.

With that being said, operating margin (as adjusted) is up from 12.7% from the three months ended July 2022 to 13.7% (as adjusted constant $) for the three months ended July 2023 - with operating income up from $190 million to $207.2 million over the same period.

With regards to short-term liquidity, we can see that the quick ratio of Ralph Lauren (calculated as total current assets less inventories all over total current liabilities) has remained above 1 since last year - indicating that the company has more than sufficient liquid assets to meet its current liabilities.

| Jul 2022 |

| Apr 2023 |

| Jul 2023 |

| Total current assets |

| 3577.5 |

| 3324.1 |

| 3473.1 |

| Prepaid expenses and other current assets |

| 217.2 |

| 188.7 |

| 208 |

| Inventories |

| 1178.2 |

| 1071.3 |

| 1187.8 |

| Total current liabilities |

| 1745.4 |

| 1493.5 |

| 1593.7 |

| Quick ratio |

| 1.25 |

| 1.38 |

| 1.30 |

Source: Figures sourced from Ralph Lauren First Quarter Fiscal 2024 Results. Quick ratio calculated by author.

Additionally, cash and cash equivalents were up from $1.464 billion for the three months ended July 2022 to $1.614 billion for the three months ended July 2023. The company's cash ratio, or cash and cash equivalents relative to total liabilities, has increased slightly from 0.32 to 0.36 - indicating that Ralph Lauren has been seeing a marginal improvement in cash flow.

| Jul 2022 |

| Jul 2023 |

| Cash, cash equivalents, and restricted cash at end of period |

| 1464.3 |

| 1614.2 |

| Total liabilities |

| 4587 |

| 4427.4 |

| Cash ratio |

| 0.32 |

| 0.36 |

Source: Figures sourced from Ralph Lauren First Quarter Fiscal 2023 and Fiscal 2024 Results. Cash ratio calculated by author.

That said, the fact that the quick ratio remains above 1 indicates that the company has sufficient cash reserves to meet its current liabilities.

My Perspective

As regards my take on the above results and the implications for the growth trajectory of the stock going forward, the strong growth that we have been seeing across digital commerce for Europe and Asia has been encouraging. However, we have seen that the slowdown in North American revenue resulted in modest revenue growth overall - 1.2% from that of the same quarter last year.

From an earnings standpoint, we can see that earnings per share are trading near a five-year high along with the P/E ratio trading at the lower end of the five-year trend.

ycharts.com

Additionally, we can see that Ralph Lauren also has a lower P/E ratio than that of competitors PVH Corp (PVH) and Hugo Boss (OTCPK: BOSSY ).

ycharts.com

From this standpoint, my view is that the stock could have scope for a rebound in upside from here, but this will hinge significantly on a rebound in North American performance lifting overall revenue. As it stands, a decline in luxury spending across North America more generally has been a significant cause behind the lower sales, with companies such as LVMH ( LVMHF ) and Kering (PPRUF) also having seen weaker demand.

However, given that the industry across North America has been seeing a slowdown more generally due to macroeconomic conditions, I take the view that Ralph Lauren stands to benefit from an eventual rebound in consumer spending more broadly and is in a good position to see upside upon realising this.

Risks

In terms of the potential risks to Ralph Lauren at this time, there is a possibility that the slowdown we have been seeing across North America could also affect Europe and Asia - depending on economic conditions. While growth across Asia has been encouraging, this in significant part reflects the post-COVID rebound in demand across China following the lifting of lockdowns. Eventually, growth can be expected to moderate across this region and without a recovery in North American sales to counterbalance this - we could see a situation where downward pressure on net revenue increases.

Conclusion

To conclude, Ralph Lauren has seen strong revenue growth across Europe and Asia, whereas the same has been more muted across North America.

However, I take the view that the company is in a good position to benefit from an eventual recovery in demand once consumer confidence returns - and the company's strong balance sheet and attractive P/E ratio means that upside potential still exists. I continue to take a bullish view on Ralph Lauren.

For further details see:

Ralph Lauren: Poised To Benefit From An Eventual Recovery In Demand