RL - Ralph Lauren: Strong Top-Line Performance But Poor Free Cash Flows Make It A Hold

Summary

- Ralph Lauren's revenue is surging, up 40% compared to 2022, with 54% of digital sales coming from Asian markets.

- Its P/E and EV/EBITDA are at five-year lows (median).

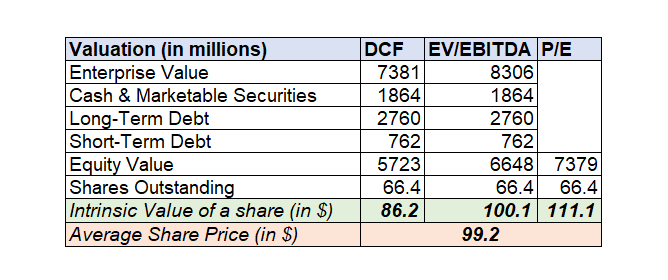

- The company's average intrinsic price per share is about $99 vs. the current market price of $122 - significantly overvalued.

- Negative FCFE and considerable leverage appear to be the primary threats here.

- I rate the stock a hold, but in a volatile market like this one, any hold rating is a tentative one.

Editor's note: Seeking Alpha is proud to welcome Prithvi Vadlamani as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Ralph Lauren Corporation (RL) has a great outlook, post-pandemic. With revenue growth of 41.3% in 2022 compared to that of 2021, top-line revenue is heading back to where it was five years ago. Profit margins are up, because of the uptrend in revenue and a downtrend in COGS (cost of goods sold). According to Statista , the firm has generated 32% of its sales through e-commerce, 12 percentage points up from its previous year's margin. A majority (54%) of those digital sales were driven by Asian markets.

What RL Does

Ralph Lauren is an iconic brand that needs no introduction. However, for the sake of argument let me explain what it does. This New York City headquartered fashion brand (domicile: United States) designs, markets, and distributes apparel, accessories, and fragrances. Ralph Lauren is a seasoned apparel manufacturer in the consumer cyclical sector. Their motto is authenticity and timeless fashion, which is pretty obvious even though they are venturing into new segments of fashion.

Recent Corporate Performance

According to the IMF , Asia is growing at a rate of 4%. According to Macrotrends , the East Asia and Pacific GDP/capita has increased by 13% in 2021. Asia becoming wealthier might provide some tailwinds for Ralph Lauren's already established distribution and e-commerce sales networks outside of the United States. I would watch out for a significant uptrend in the top-line performance in Asian markets for the brand.

The firm has signed deals with Epic Games and Roblox (RBLX) as a digital apparel provider. Although it is a nascent segment right now, I like it because digital apparel needs no skilled artisans, raw materials, or inventory management. Additionally, the need for global distribution and supply chain bottlenecks will be significantly reduced.

Strengths

As mentioned earlier, Ralph Lauren's recent performance has been commendable. Revenue is on an uptrend, toward the levels of five years ago. A 5% increase in gross profit margin in 2021 and 2022 is a source of optimism. This basically reflects the efficiency of the firm in squeezing out the revenue for a given cost of the goods sold.

There is a significant uptrend in accounts receivables and inventory (mainly finished goods) post-pandemic. Together, these constitute 30% of the current assets of the firm in 2022. A quick calculation of the cash ratio (cash and cash equivalents to current liabilities) produces a figure of 0.8, which is still in an acceptable range of 0.5-1.0. So, the liquidity risk of the firm is still in a decent spot.

Although the P/E multiple is higher than the average industry P/E, it is near its lowest level in the past two years.

The firm's P/E multiple has historically been extremely cyclical, with the low point being around 15x and the highest being 105x.

The EV/EBITDA multiple of 8.5x is at its lowest point in the past five years.

However, the multiple has been at that level most of the time, with a sudden surge to 180x in 2021, before dropping back to that familiar area more recently. These multiples, at their lows (lows in the same range as median value) combined with a catalyst like digital sales, might provide a significant value in the long term.

Weaknesses

With a market cap of $8 billion and an average daily trading volume of $4 million, the stock is far from liquid.

Ralph Lauren has a great brand name, yet I do not consider it an industry leader. I do not find it to have a significant moat (i.e., a competitive edge). In an industry where companies do not aim to be cost leaders, a firm might develop a moat either through efficient scale to create a monopoly or through high switching costs for consumers. Ralph Lauren, along with most other firms in the industry, is lacking in terms of both points. The switching costs in the industry are very low. For example, I can buy a Ralph Lauren shirt and pair it with a Michael Kors jacket, or vice versa. Currently, its market share of 5% is not nearly significant enough to achieve a monopoly.

Although the firm's liquidity is in the permissible range, a significant uptrend in debt from 2015 is bothersome. The equity multiplier (total assets to total equity) has grown twofold from 1.5x in 2015 to 3x in 2022. This shows the firm has a lot of leverage on its balance sheet.

Leverage is a double-edged sword. Particularly during recessions, it might prove fatal. And it is already showing up in the financials. The FCFF (free cash flows to the firm) has declined to $104 million TTM (trailing 12 months) from $590 million in the year 2022. The increase in debt and a decrease in the FCFFs led to an FCFE (free cash flow to equity) of -$456 million TTM. A negative FCFE generally means the firm must raise funds (equity or debt) soon. I consider this an ominous sign, particularly with borrowing rates now significantly elevated.

Looking Forward

The intrinsic valuations based on DCF (discounted cash flows), EV/EBITDA (enterprise value to EBITDA), and P/E (price to equity) multiples resulted in an average stock price of around $99 vs. the current stock price of $122. My assumptions based on valuation methods are as follows:

DCF

-

Cost of Equity: 12%

-

Cost of Debt: 6.7%

-

Tax Rate: 20.47%

-

WACC (weighted average cost of capital): 9.73%

EV/EBITDA

-

Average multiple (based on the peer group) of 8.64x compared to 8.4x

P/E

- Average multiple (based on the peer group) of 12.5x compared to 16x

A decline in the FCF to the firm has affected the intrinsic value of the share price (using a DCF valuation).

{kind=link}

Conclusion

Despite the concerns I've noted above, Ralph Lauren is on my watchlist for a handful of reasons. These include the increase in top-line revenue performance, improving profit margins, great online sales (both in the U.S. and other markets), and increased sales in Asian markets. Although I like the idea of digital sales, I still find that to be nascent and would not want to jump on that bandwagon just yet.

Ralph Lauren has attractive P/E and EV/EBITDA multiples, as well as attractive profit margins. However, I rate the stock a hold due to the threat of negative FCFEs and the high leverage on its balance sheet.

For further details see:

Ralph Lauren: Strong Top-Line Performance But Poor Free Cash Flows Make It A Hold