METC - Ramaco Resources: Consider The Downward Risk

2023-03-16 11:24:02 ET

Summary

- Although the business performance appears to be improving, any industry-wide price weakness might affect the company's profitability.

- As the coke prices are improving consistently, METC stock price might increase in the upcoming quarters.

- But the risk still persists due to the commoditized nature of the business.

Ramaco Resources ( METC ) is a pure-play metallurgical company that operates high-quality, low-cost coal mines. Having a geological advantage helps the company provide low-cost coal to domestic and international customers. Over the period, management has invested considerable capital in developing these existing mines, which has been bearing fruits for the company; as the company is expanding its reach through acquisition and capacity expansion, in the upcoming years' production is expected to increase from 2.4 million clean ton currently to about 5 million tons annually.

share price (YCHARTS)

After losing over 70% of its value in the 2020 crash, the stock prices started gaining value as the prices of coke started rising; since its crash, the stock returned over 680% in just a single year, which has produced massive value to the shareholders, but from its all-time high price of $19.80 the stock has lost over more than 52% of its value and has been trading for about $8.62.

Although the stock looks cheap as per the current valuation, I believe investors must consider that the significantly higher profits are primarily attributed to higher average selling prices for coke. Such high prices might not last for a longer duration. Any correction in coke prices might affect the profitability of the business.

Historical performance

{kind=link}

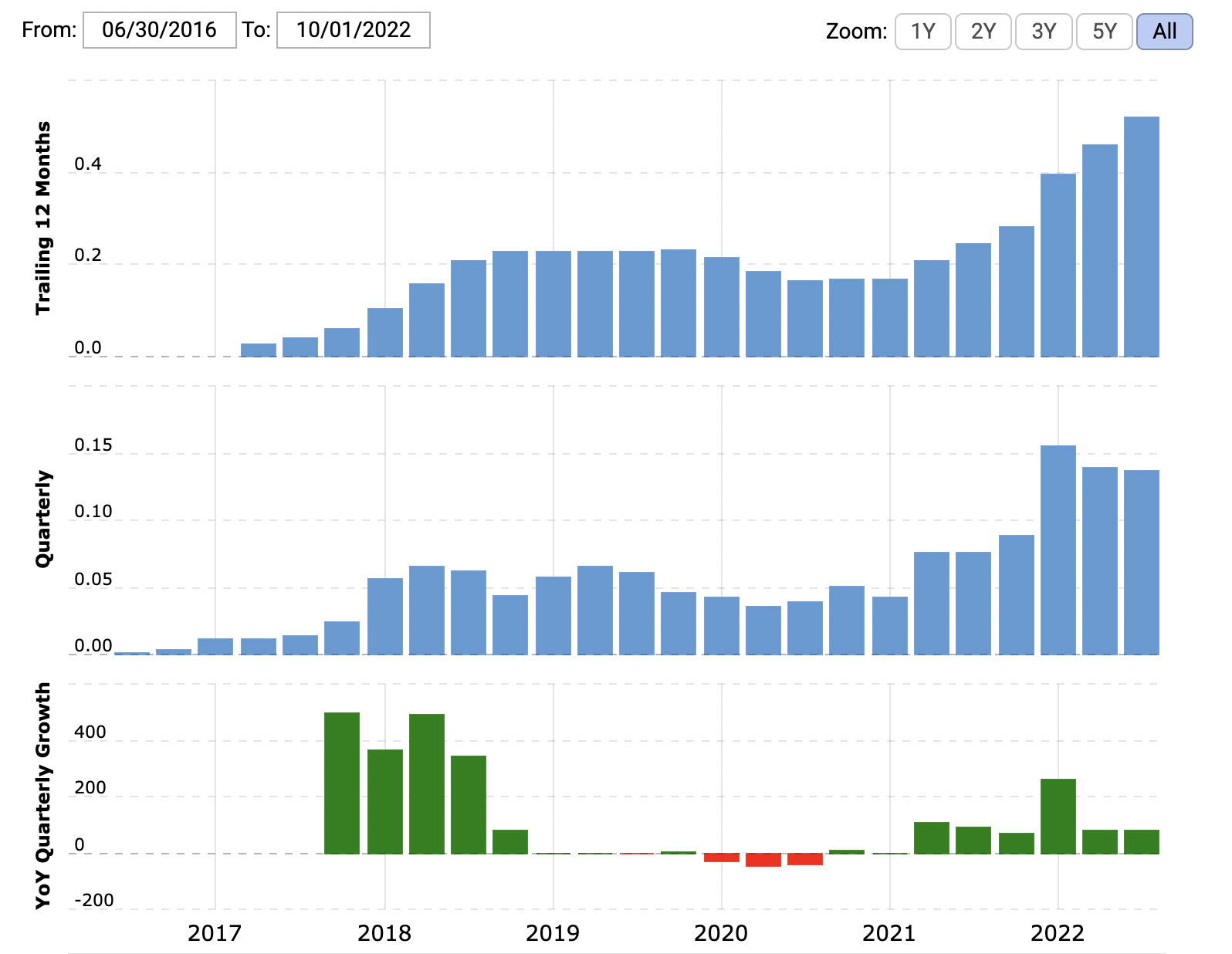

Since its initial public offer, revenue has grown significantly , led by strategic acquisitions and consistent capital expansions. Revenue increased from $61 million in 2016 to about $283 million by 2022. Also, due to its cost-effective business model, where the company enjoys a considerable logistic advantage, Ramaco Resources could turn a highly competitive and commoditized business operation into a profitable business.

{kind=link}

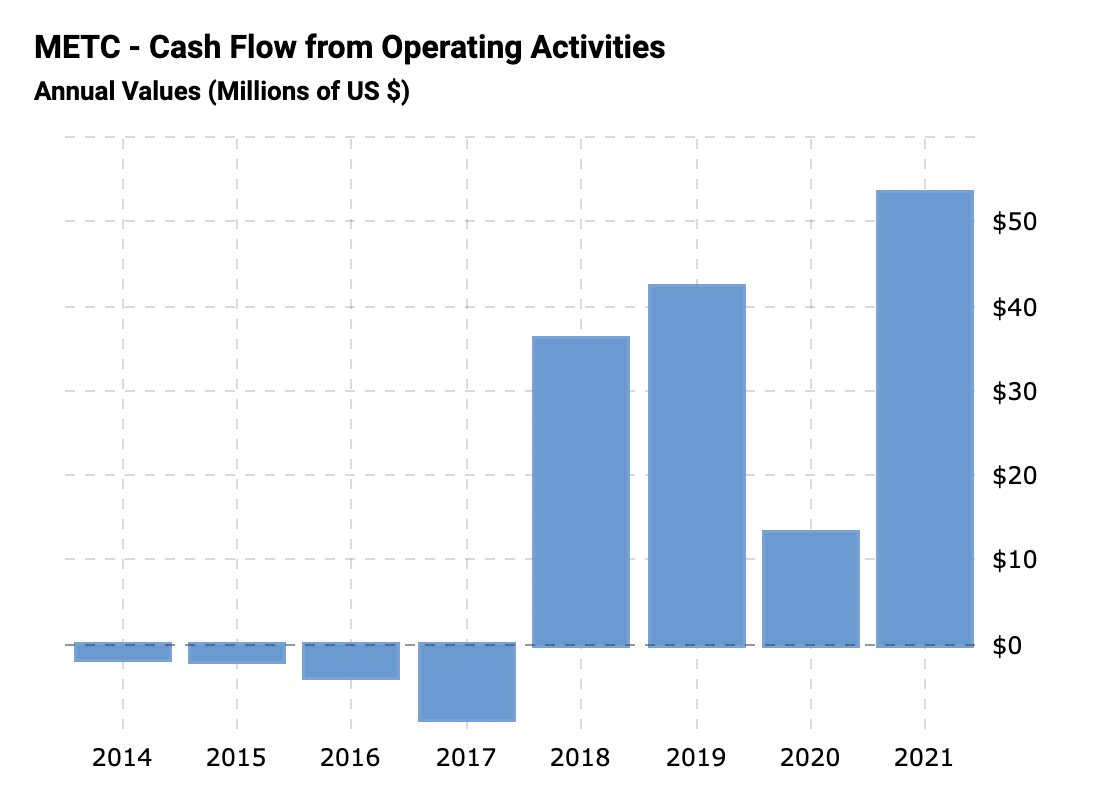

Due to the favorable coke prices in the last few years, the company could post strong cash flow from operations. Such a strong CFO might be a reason for the low debt structure of the company. It should be appreciated that the company has expanded its business reach while keeping its financial position strong.

Strength in the business model

{kind=link}

The company's operations in a metallurgic coal sector give the business model a commoditized nature, where price becomes a significant driving force; In such a case having a business model with a considerable cost advantage provides a substantial competitive advantage over its peers.

In Ramaco's situation, the locations of the mines provide a significant geological advantage, where the company could extract high-quality coal at a very low cost compared to other coal producers. Also, as the management is investing in developing infrastructure to strengthen its price competitiveness and logistic networks, in the upcoming years, Ramaco Resources could enjoy a considerable competitive advantage, which could help the company during industry-wide downturns.

We plan to complete development of our existing properties and increase production from our existing development portfolio to approximately 5 million clean tons of metallurgical coal, subject to market conditions, permitting and additional capital deployment. We may also acquire additional reserves or infrastructure that contribute to our focus on advantaged geology and lower costs.

- Annual report 2022

As the company desires to expand its operations through developing existing properties, in the upcoming years, revenue might increase substantially, which might drive cash flow into a higher range.

Furthermore, the l ong-term debt is considerably low , which provides significant financial strength and operational flexibility to the company; if the company desires to expand its operations, it can raise money through debt at a reasonable cost due to its strong financial position. Also, due to its strong performance over the last two years, overall shareholder's equity has reached a new high of $309 million; It should be appreciated that the management is investing generated money on expanding its business operations which can bear fruit in the distant future.

Risk factors

Although the profits are improving year over year, various risks can hurt the business profitability; historically, prices of coal have been significantly volatile, with significant ups and downs; consider that the recent boom in coal prices is a result of volatility in natural gas prices, any weakness in demand related to coal, can affect the business performance significantly.

As the demand for coal is rising consistently, various producers are increasing their capacities which can cause excess capacity in the market. As seen historically, in such cases, coke prices might suffer a significant correction.

Recent development

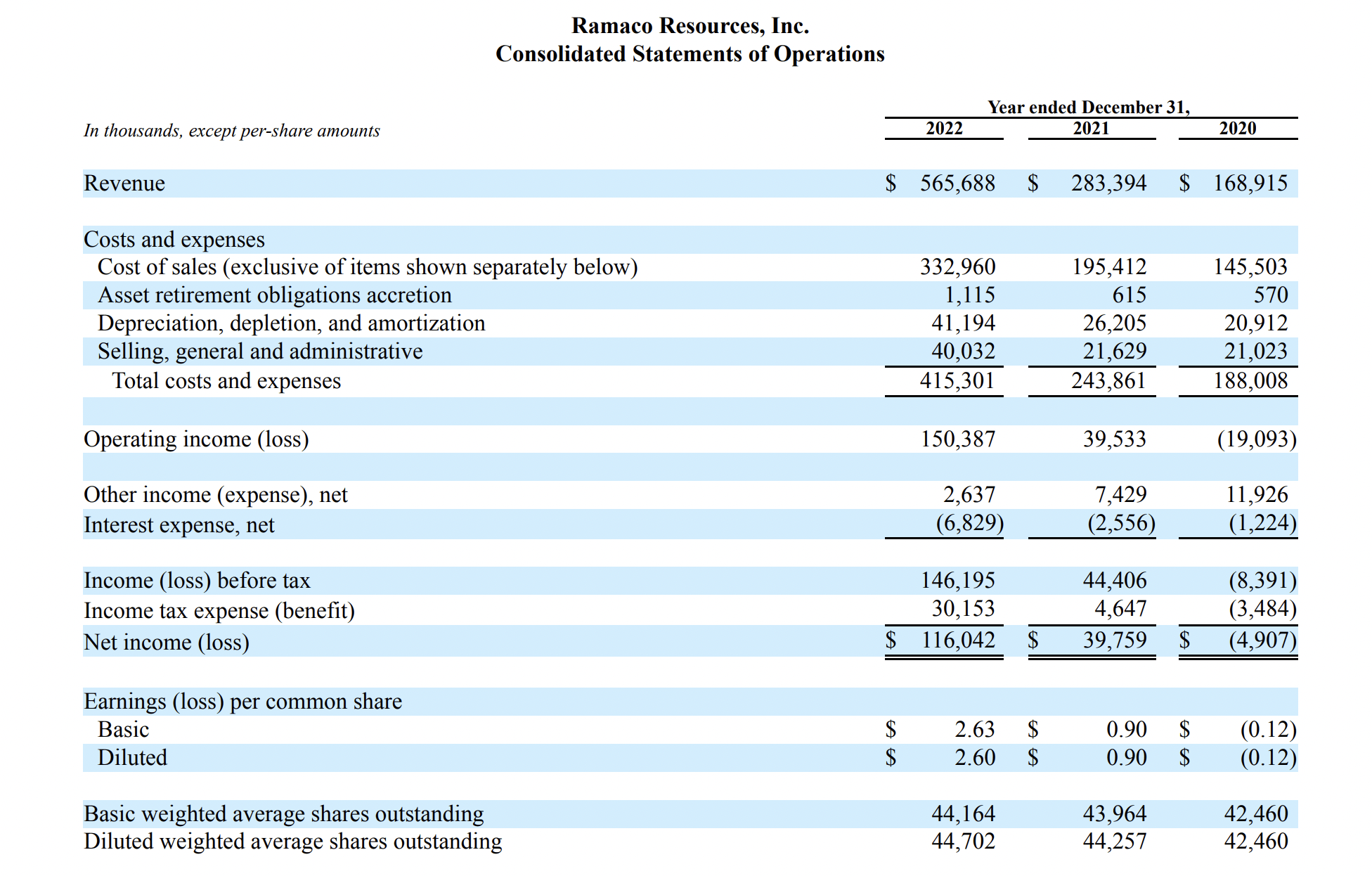

income statement (annual report)

{kind=link}

This week, the company has reported its annual report for FY2022; Revenue has increased from $283 million in 2021 to about $565 million. Such significant growth is primarily attributed to higher prices and consistently high demand for coke in the market.

we had entered into forward sales contracts with certain North American customers for 2023 on a fixed price basis for 1.2 million tons of coal at an average realizable price of $198/ton FOB mine. This level of pricing in 2023 is higher than the average price of $187 per ton FOB mine that was obtained during the previous contracting season for North America.

- Annual report 2022

Also, for the year 2023, the company has already set its prices, which are higher than last year; therefore, profitability might improve in the coming quarters.

Although the business performance appears to be improving, any industry-wide price weakness might affect the company's profitability; in such cases, the stock price might suffer significantly. Currently, the company is trading for about $380 million, whereas it produced over $116 million in FY 2022, which gives it a valuation of about 3 times its earnings. It seems that the stock is trading at a very low valuation, but also consider that such profitability might not sustain at this level.

For further details see:

Ramaco Resources: Consider The Downward Risk