METC - Ramaco Resources: Despite Falling Commodity Prices It Remains Appealing

2023-09-28 10:46:08 ET

Summary

- Commodity prices, including metallurgical coal, have fallen steeply in the first half of 2023 compared to 2022.

- Ramaco Resources, Inc. operates low-cost mines and generates strong margins, making it an appealing investment.

- Despite efforts to reduce coal dependence, demand for coal is likely to persist due to ongoing construction projects and the need for steel production.

The prices for a variety of different commodities prices have fallen steeply over the first half of 2023 compared to the same period in 2022. For example, metallurgical coal which is the focus for Ramaco Resources, Inc. ( METC ) the prices has fallen by over 20% as per their last report .

What METC has managed to provide though is that they can run and operate several mines that are low cost and also manage to generate very strong margins. This is the main appeal behind an investment right now, in my opinion. Coal is a resource we are trying to get rid of and be less dependent on, but the fact of the matter remains that we are likely to resume using it for a very long time more, as replacements take time to set up. With the end market being still productions for METC I think that demand will persist as in many key markets significant housing and construction projects are still being developed and introduced all the time. I remain bullish on the company and the coming years and will be rating it a buy as such.

Company Catalyst

As we have gone over, METC is in the coal industry where they supply critical materials and products for steel manufacturers to continue to maintain operations. Currently, with operations in southern West Virginia, southwestern Virginia, and southwestern Pennsylvania, Ramaco Resources develops high-quality, low-cost metallurgical coal. Ramaco discloses 62 million reserve tons and 1,156 million measured and indicated resource tons of high-quality metallurgical coal. The met coal is ignited and used as a heating source in making steel, a market that is still very much alive and well in many regions.

Coal Sales (Investor Presentation)

The company has already managed to build up a decent international presence with sales of coal in 20 different countries. Driving the demand forward comes ultimately from the demand for more steel. There are still a lot of housing shortages across key regions and expectations are that it will continue to be like that for quite some time more.

Margin Profile (Investor Presentation)

Where I think that METC has managed to differentiate itself somewhat efficiently from other miners is the fact they run almost exclusively low-cost and strong-margin mines that are focused on delivering growing FCF over a longer period. The spot prices for coal have been largely down on a YoY basis and this has of course affected the results for METC. However, the most recent report from the company did display some resilience as they did manage to generate a positive $7.6 million in net income for the quarter. I think that despite suppressed coal prices there is stability to METC and their operations. The results for the quarter still showed that METC can deliver a good dividend yield. The management did announce a quarterly dividend of $0.125 for shareholders which is a very good increase from the dividend the company had 12 months ago of $0.09. The payout ratio does look quite low as well at under 30% so I would argue there is room for some more growth without overleveraging themselves as it seems earnings are stabilizing as coal spot prices are finding their bottom.

{kind=link}

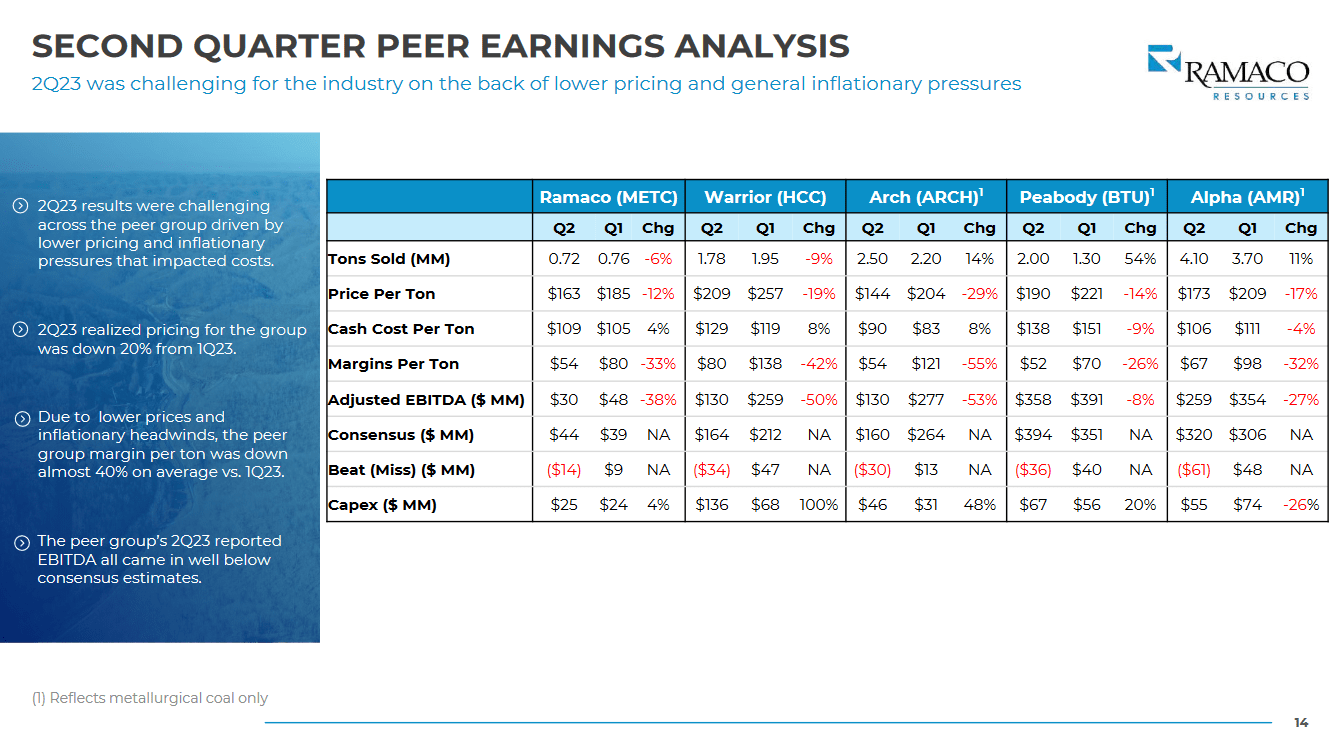

On a peer comparison , it seems that METC continued to perform very well. On a QoQ basis, it was the company that saw the smallest decline in price per ton sold, a decrease of 12%, whilst others saw upwards of 29% instead. The lower and softer pricing environment was tough on a lot of companies in the sector, but seeing METC still able to grow its dividend and have double-digit net margins does limit the downside from here I think. Ultimately, this comes down to strong business fundamentals and good decisions and investments in the mines that they have.

Risks

Mining operations inherently carry risks, and safety concerns are paramount in this industry. A notable incident in 2022 within one of Ramaco's mines involved a methane ignition. Thankfully, no personnel were harmed in this incident. Nevertheless, it's crucial to acknowledge that such occurrences often pique the interest of regulatory authorities, prompting inquiries and investigations.

Furthermore, I think that volatility in the global coal market may exert adverse pressure on the company's cash flow statement. While the firm may sustain its track record of delivering favorable financial outcomes driven by production expansion, it's essential to recognize the potential implications for investors and the stock price. The FCF has been slightly inconsistent over the last few years with 2022 producing a net positive of $6.6 million whilst 2 years earlier it was negative $9 million instead.

Coal Price (tradingeconomics)

Shifts in international coal market conditions can significantly impact investor sentiment and trading behavior. Even if the company continues to demonstrate strong operational performance, heightened market volatility or changes in demand for coal-related products can trigger sell-offs among investors. Such divestments can potentially lead to a decline in the stock price.

Last Pointers

Right now I think that METC is looking like a very strong addition to a portfolio as the dividend continues to go up and the company managed to have double-digit net margins despite the coal prices being already suppressed on a YoY basis. There are clear struggles of lower prices as CAPEX and further investments are difficult to perform because the FCF does take a hit in these market conditions.

{kind=link}

As for the valuation of the company, I think that around the 5 - 6x earnings mark is where I am the most interested. Here it offers a 5% dividend yield at least and still can grow it too. Historically as well, METC has traded nearly twice as high as it is now. Besides that, I think it's somewhat shielded or shouldn't be regarded as threatened by the move towards green energy. Since METC focuses on met coal used in making steel, the shift to green energy doesn't affect it as much. Housing and steel demand will be here for a very very long time and replacing the source of heat is difficult and expensive and unlikely to happen quickly. I like the market fundamentals and think we are heading higher from here on out and will be rating METC a buy as a result.

For further details see:

Ramaco Resources: Despite Falling Commodity Prices, It Remains Appealing