METC - Ramaco Resources: FCF Expected From Production Growth And Undervalued

2023-06-13 06:31:05 ET

Summary

- Ramaco Resources expects to double its coal production by 2026 and recently announced lower capex for 2023 and 2024.

- The company's international sales and expansion plans in the Elk Creek Complex contribute to its potential for growth and increased stock value.

- Despite risks such as debt levels, lower production, and market volatility, Ramaco Resources appears undervalued and could trade higher.

Ramaco Resources, Inc. ( METC ) recently announced that it expects to double coal production by 2026 . Besides, management announced that 2023 capex and 2024 capex could be lower than that in 2022. Taking into account the expected reserve life of close to 19-20 years of the Elk Creek and Berwind assets as well as the expansion plant in the Elk Creek Complex, Ramaco Resources could be worth much more than $7.7-$8.6 per share. Even taking into account risks from the total amount of debt, lower coal prices, or lower production than expected, I believe that METC could trade higher.

Ramaco Resources

Currently with operations in southern West Virginia, southwestern Virginia, and southwestern Pennsylvania, Ramaco Resources develops high-quality, low-cost metallurgical coal. Ramaco discloses 62 million reserve tons and 1,156 million measured and indicated resource tons of high-quality metallurgical coal. After considering the production growth expectations, I believe that the current stock price does not make a lot of sense. For 2023, the company expects to deliver close to 6.5 million ton level with a majority of high quality coal.

Source: Quarterly Presentation

Those analysts running the DCF models would also appreciate having a look at the following production expectations. Ramaco expects to achieve 6.5 million tons by 2026, which means that production could double in the medium term. I believe that more production could lead to FCF growth and stock price increases.

Source: Quarterly Presentation

It is also worth noting that Ramaco Resources appears to receive a lot of demand in the international markets. The company's sales are in Europe, Africa, Latin America, and Asia. With this in mind, I believe that the coal offered and the conditions of Ramaco Resources are top-notch.

The company delivered very beneficial expectations about the expansion plant in the Elk Creek Complex, an option of adding a second section in the Knox Creek Complex, and lower capex in 2024 and 2026.

Source: Quarterly Presentation

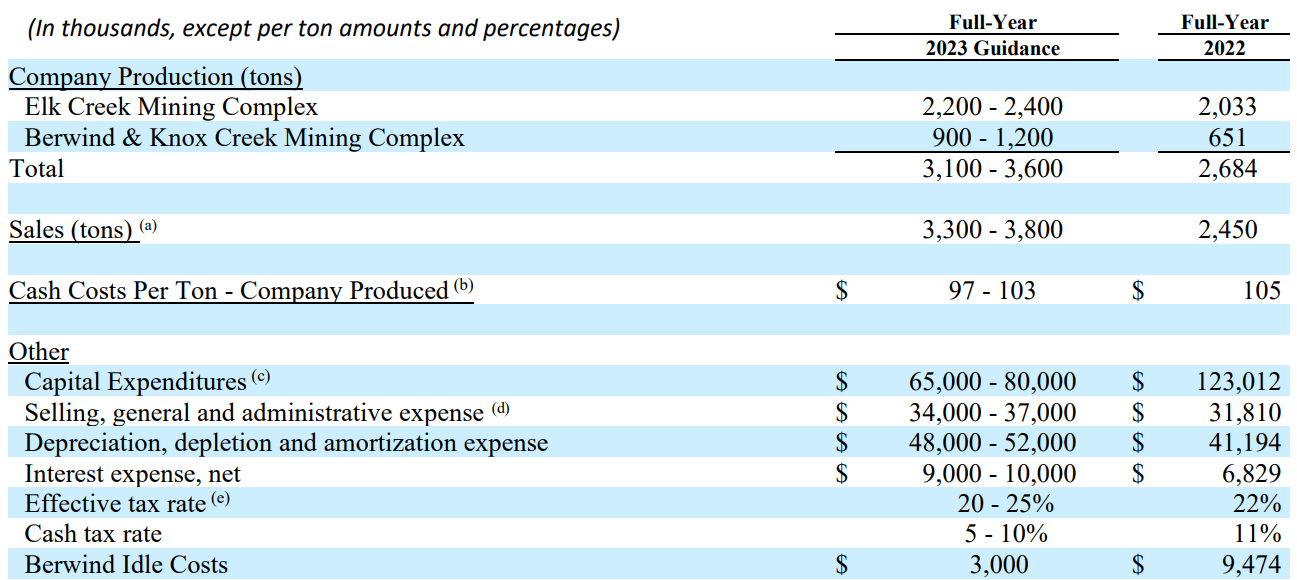

Besides, the guidance given for the full year 2023 was, in my view, optimistic. With total production of close to 3.1-3.6 million tons, which is significantly higher than that in 2022, management also noted capex around $65-$80 million, D&A of $48-$52 million, and SG&A of close to $34-$37 million.

Source: Quarterly Presentation

{kind=link}

Considering the most recent price dynamics, I believe that running a full valuation model makes a lot of sense. The company is currently trading at $7.5-$8.5 per share with a diluted EPS of $2.23. The results of my DCF model implied a valuation that significantly exceeds the current stock price.

Source: Ycharts

The Balance Sheet Looks A Bit Better Than That In 2022

In the first part of 2023, management reported more cash, more accounts receivable, and even more inventories. Recent acquisitions and more long term debt explain the recent increase in assets. However, it is quite beneficial that the total amount of assets increased more than the total amount of liabilities.

As of March 31, 2023, the company reported cash and cash equivalents worth $36 million, accounts receivable around $71 million, inventories of $50 million, and prepaid expenses close to $19 million. Also, with property, plant, and equipment of around $444 million and financing lease right-of-use assets of about $12 million, total assets stand at close to $641 million. Total assets/total liabilities stand at close to 2x, and the net assets are approximately equal to the current market capitalization. Hence, I believe that Ramaco appears undervalued.

Source: 10-Q

The list of liabilities does not seem worrying with accounts payable of $49 million, accrued liabilities worth $33 million, and current portion of long-term debt worth $29 million.

Management also reported asset retirement obligations of about $29 million, long-term debt worth $45 million, long-term financing lease obligations of $3 million, and senior notes worth $32 million. In sum, total liabilities are equal to $304 million.

Source: 10-Q

DCF Model

In the last quarter, we saw how 61% of the total coal produced was sold in countries outside the North American markets. I believe that Ramaco found a way of successfully competing with other international operators with more resources and larger economies of scale. With this in mind, I am quite optimistic about the future performance of Ramaco.

During the first quarter of 2023, we sold 0.8 million tons of coal and recognized $166.4 million of revenue. Of this amount, 24% was sold in North American markets, including Canada, and 76% was sold into export markets. During the same period of 2022, we sold 0.6 million tons of coal and recognized $154.9 million of revenue. Of this amount, 39% of our sales were sold in North American markets, including Canada, with the remaining 61% being sold into the export markets. Source: 10-Q

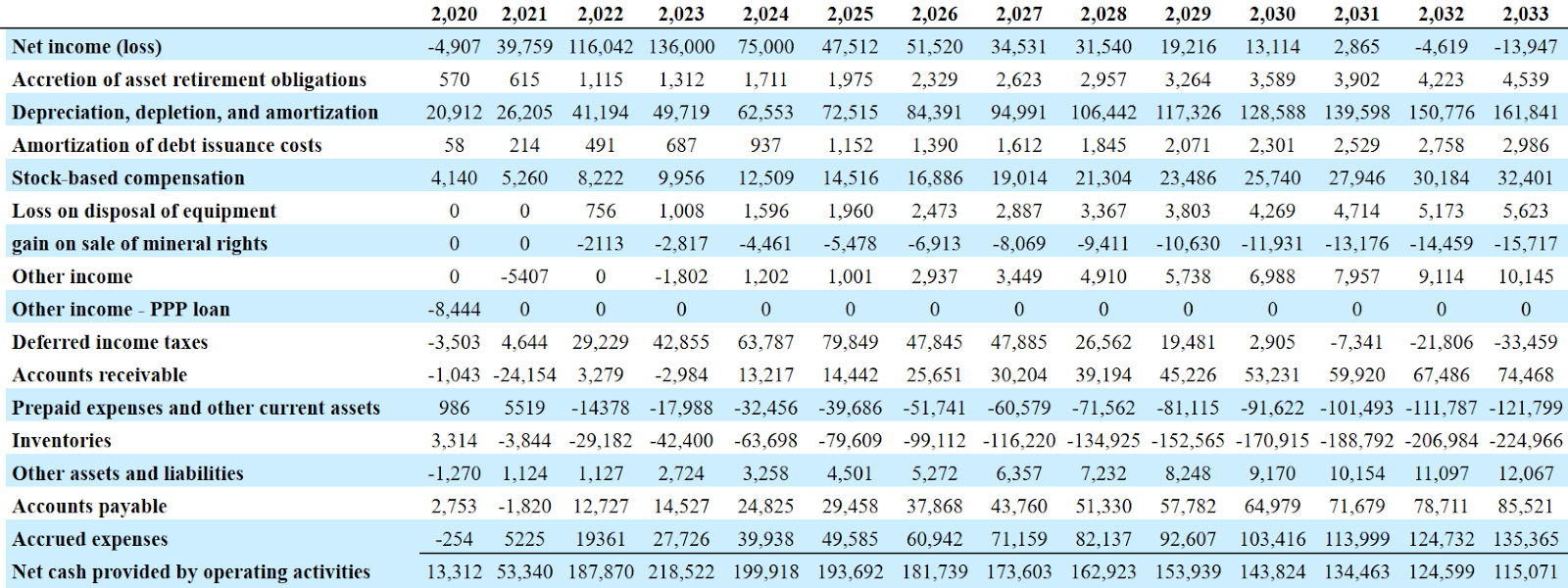

Management reports that it expects to double its production in the coming years. I tried to be a bit more conservative than the company as we also have to consider that the price of coal could lower. Taking into account this fact, I assumed that FCF would trend around $218 and $115 million from 2023 to 2033.

I also assumed that Ramaco Resources will most likely pay less interest expenses as the debt is further reduced. I believe that future FCF would serve to lower the debt received to pay recent acquisitions. Less debt would also interest investors. The cost of equity may lower, which would most likely enhance the stock valuation.

Interest expense, net was approximately $2.3 million during the three months ended March 31, 2023 compared to $1.1 million during the same period in 2022. The increase in interest expense is generally due to higher debt levels, including debt incurred to finance acquisitions in the second and third quarters of 2022. Source: 10-Q

I am really not concerned about the level of debt, but certain investors may not like that the financial debt/equity stands at its maximum level from 2018.

Source: Ycharts

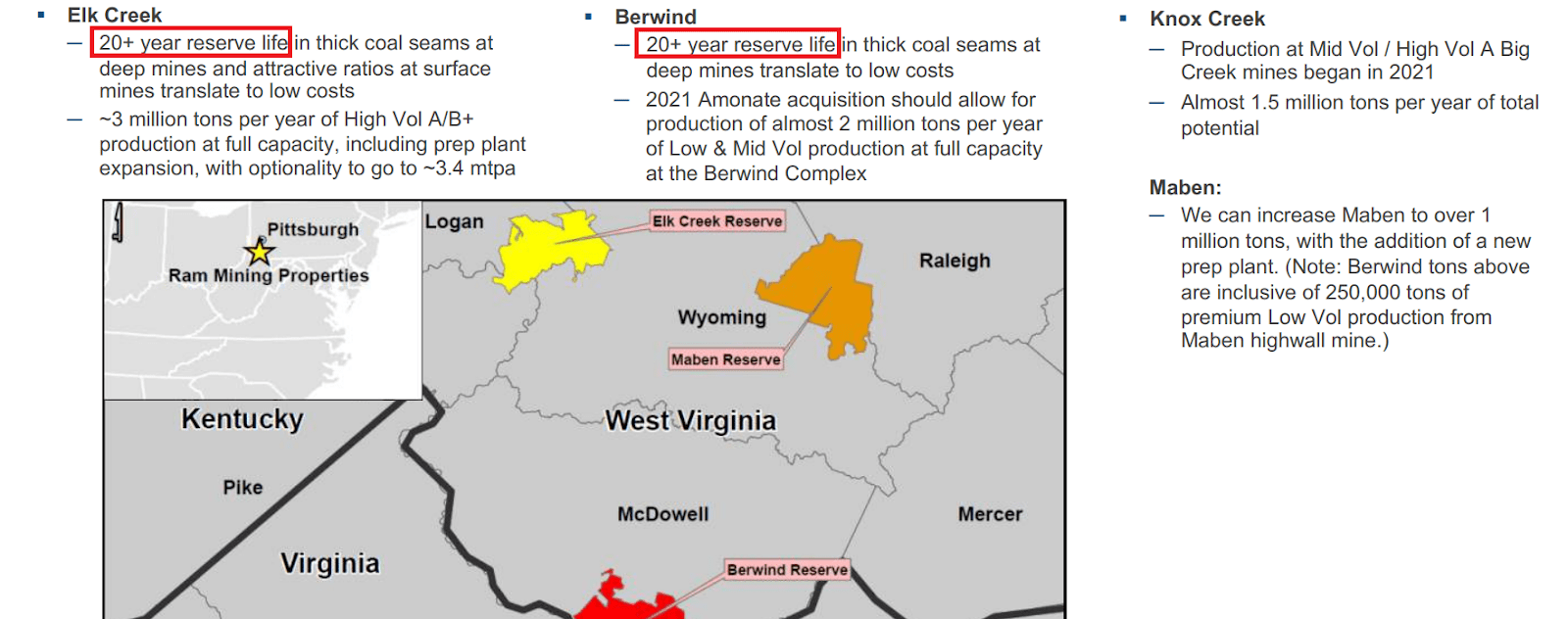

For the assessment of future cash flows, I assumed that Ramaco Resources will be able to operate in Elk Creek and Berwind for at least the next ten years. In this regard, please note that the company, in a recent presentation, noted that the life of these projects are expected to be close to 20 years. I also assumed that further exploration and development will most likely lead to an increase in the economic reserve and capacity.

Source: Quarterly Presentation

{kind=link}

The company is currently making significant efforts to discover REEs, which are critical to power the energy transition. I have not included the discovery of new mineralization. However, investors may be interested in having a look at the work of Ramaco in several target REE zones. In my view, new discoveries could push the stock price up.

The Company continues to assess its potential rare earth element deposit in Wyoming, and core analysis performed to date shows high relative concentrations of heavy rare earth elements such as Terbium and Dysprosium as well as lighter rare earth elements such as Neodymium and Praseodymium. Source: 10-Q

Ramaco has drilled 131 core holes targeting the REE mineralization zone, with 58 of those cores having been scanned by portable x-ray fluorescence ("XRF"), and 965 test samples having been conducted using inductively coupled plasma ("ICP") spectroscopy. Source: Quarterly Presentation

My financial model included 2033 net income of -$14 million, accretion of asset retirement obligations of about $4 million, 2033 depreciation, depletion, and amortization worth $161 million, and stock-based compensation of $32 million.

I also included deferred income taxes of about -$34 million, accounts receivable worth $74 million, prepaid expenses and other current assets worth -$122 million, and inventories of -$225 million.

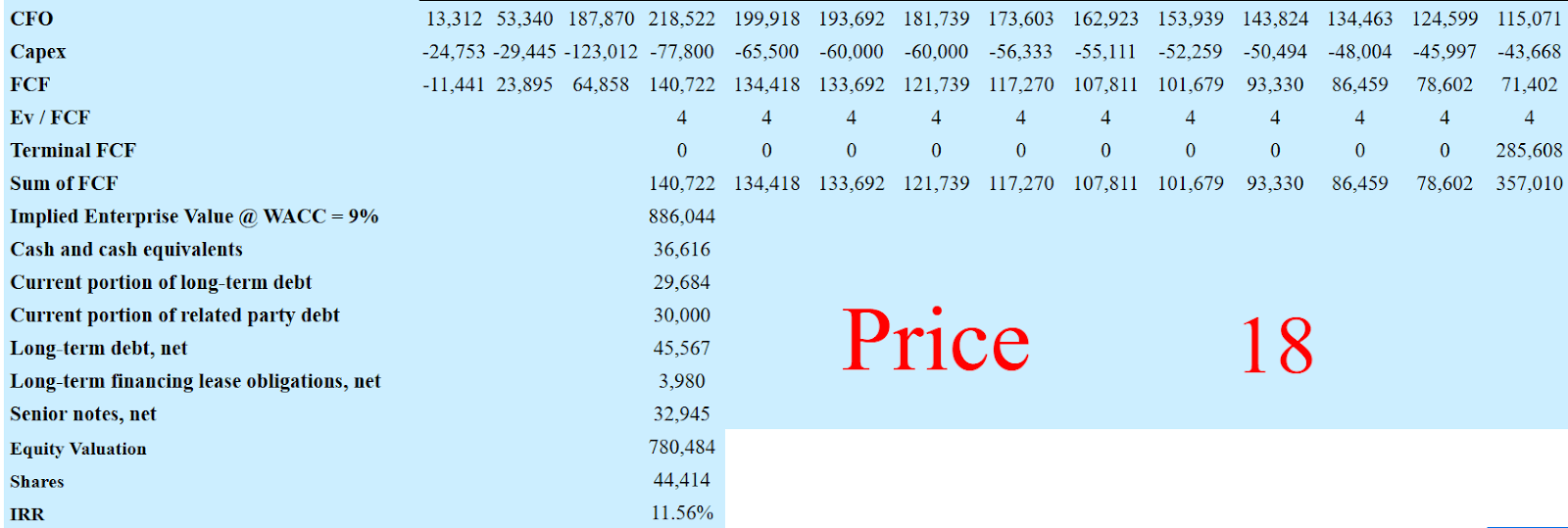

Besides, with 2033 changes in accounts payable of $85 million and accrued expenses close to $135 million, 2033 CFO would be around $115 million. Subtracting capex of -$44 million, 2033 FCF would be $71 million.

{kind=link}

I assumed a terminal EV/FCF of about 4x, which would imply 2033 terminal FCF of $285 million. The implied enterprise value with a WACC of 9% would be around $890 million. If we add cash and cash equivalents worth $36 million, current portion of long-term debt of about $29 million, current portion of related party debt close to $30 million, and long-term debt of $45 million among other debts, the equity valuation would be $780 million. The IRR would be around 11%, and the implied price would be $18 per share.

{kind=link}

Risks

Mining can be dangerous. In 2022, the company reported a methane ignition in one of the mines. No personnel were injured, however authorities may be interested in running a full investigation about the issue. In my view, further issues, explosions, any other fatalities, or detrimental information about the activities of Ramaco could reduce the demand for the stock. As a result, we may see stock price declines.

On July 10, 2022, the Company experienced a methane ignition at the Berwind No. 1 mine, which was one of the active mines at our Berwind mining complex. The other mines resumed production while the Berwind No. 1 mine was idled until a full investigation could be conducted. There were no personnel in the mine at the time of the incident and no injuries or fatalities occurred. Production from the Berwind No. 1 mine restarted in the first quarter of 2023. Source: 10-Q

I also believe that changing conditions in the international coal market could have a detrimental effect on the cash flow statement. Even if the company continues to deliver beneficial results because production increases, investors may sell, which may lead to decrease in the stock price. Management gave full explanation on these matters in the last quarterly report.

This volatility, including market expectations of potential changes in coal prices and inflationary pressures on steel products, has had a significant effect on market prices and may affect overall demand for our coal as well as the cost of supplies and equipment. Source: 10-Q

It is quite beneficial that Ramaco Resources decided to lower its debt obligations in April 2023. However, I believe that changing conditions in the credit markets could have a negative effect on Ramaco. Certain investors may believe that the company may need to pay larger sums of interest expenses, which would lead to lower FCF expectations.

During April 2023, shortly after the balance sheet date, the Company repaid $15.0 million of its outstanding borrowings under the Revolving Credit Facility using funds from current operations. Source: 10-Q

Finally, I believe that lower production than expected in 2025 and 2026 could have a detrimental effect on the credibility of management. If analysts do not trust the guidance given by Ramaco Resources anymore, I would expect lower future FCF and lower stock valuation.

Conclusion

Ramaco Resources expects to double its production of coal in the coming years, and recently delivered 2023 guidance including more production and less capital expenditures than that in 2022. Considering the recent figures and the FCF expectations of other analysts , the stock appears considerably undervalued. We are talking about a company that owns mines with close to 19 years of reserve life, and trades at less than 4x forward EBITDA and even close to 4x forward FCF. Even considering risks from the current debt levels, lower production than expected, or any more methane ignitions, I believe that Ramaco could trade higher.

For further details see:

Ramaco Resources: FCF Expected From Production Growth, And Undervalued