METCL - Ramaco Resources: From Market Expansion To Market Realities

2023-12-24 08:13:26 ET

Summary

- METC's stock soared by 157% YTD, driven by increased production capacity and new mining developments.

- The company is transitioning from aggressive expansion to focusing on maximizing existing capacity, with reduced growth Capex.

- METC's current valuation, while fair, requires cautious consideration in light of declining growth, rising mining costs, and declining average selling prices.

Investment Thesis: A Growth Narrative

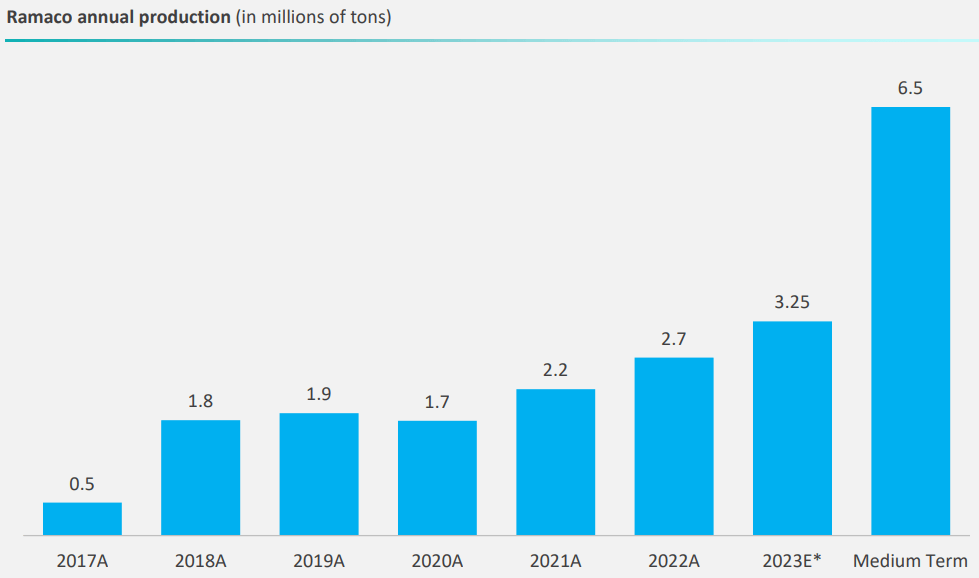

Ramaco Resources ( METC ), the coal mining start-up, has delivered an exceptional stock performance this year, soaring by an impressive 157% year-to-date 'YTD,' outperforming all but one of its industry peers. The key driver behind this surge is the company's increased production capacity, largely fueled by the development of new mining sites. Notably, the Berwind and Big Creek mines at Knox Creek complex have been instrumental in this expansion, adding more than 1 million tons of production capacity. This represents a significant jump of nearly 40% above 2022 production levels.

Nonetheless, the company's growth trajectory in the short term appears less certain. METC has announced a slowdown in capacity expansion going into 2024, obscuring the growth narrative that has been integral to its past performance and one of the pillars of its high Quant Score rating.

Seeking Alpha

Beyond 2024, METC anticipates an increase in production in the medium term, a factor that reinforces our 'Hold' rating. However, we see a consistent rise in the cost per ton, which might reflect the lower quality of the newly-opened mines, suggesting an initial focus on higher-quality assets and undermining the marginal benefits of management's medium-term growth initiatives.

{kind=link}

In terms of valuation, while the company's pricing appears reasonable when considered independently, it's important to note that it is trading at a valuation similar to its industry peers.

The Growth Factor is Abating

METC's impressive stock performance can be credited to its increased sales and production capacity, effectively offsetting the coal price correction from 2022's record highs, many of which have been described as unsustainable. In the nine months ending September, the company's expansion efforts resulted in 2.5 million tons of coal, a notable rise from 1.8 million tons in the same period last year.

The increase in production stems from expansion initiatives at the Berwind and Big Creek mines, which contributed to an additional 1 million tons of capacity. This expansion has boosted METC's total production rate to about 4 million tons, a significant increase from 2.7 million tons last year and 2.2 million tons in 2021. This steady and robust growth has reinforced investor confidence, spurring a surge in the company's share price.

METC is now focusing on maximizing the potential of its new operating capacity, transitioning from its prior aggressive growth capex strategy. Management anticipates a 50% reduction in capex for FY 2024, projecting it to fall between $45 million and $55 million, down from the estimated $96 million in 2023 and $134 million in 2022. This reallocation of funds towards maintenance rather than expansion signals a shift in METC's investment focus and suggests moderation in the rapid growth trend it has experienced up to this year.

Costs are Rising, and Unit Revenue is Declining

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Cash Cost |

| $73 |

| $63 |

| $73 |

| $72 |

| $70 |

| $107 |

METC's management has progressively raised its cash cost per ton estimates over the past year. The initial March forecast was between $97 and $103 per ton, which was revised up to $102 - $108 per ton in August and then again to $108 - $112 per ton in December. This upward trend in costs suggests that METC may have ventured into newer mines with higher operational expenses after initially leveraging more cost-effective mines. Management attributes the cost increase to broader inflationary trends. However, the recent cost rises in recent months contradict the broader inflationary trends, which have been subsiding.

{kind=link}

Simultaneously, there's been a decrease in the realized price of coal sales. In November, management announced it contracted 1.3 million tons (30% of 2024 expected production) at $167 per ton. By the same period last year, the company had already committed nearly half the output estimate at $201 per ton. This reduction in price and customer commitments reflects the marketing challenges METC faces as it seeks to sell the increased capacity resulting from its recent mine expansions.

Fairly Valued

METC currently trades at a compelling fair value with a Forward PE ratio of 9x. This valuation, considered on a standalone basis, fairly compensates for the variability of returns throughout economic cycles. This state of fair value implies stability in valuation multiples at 9x.

In comparison to industry peers, METC's valuation aligns with the upper range of the sector's average, possibly reflecting its historical growth and potential opportunity in the Brook Mine, which the company believes might contain significant Rare Earth Elements 'REE' reserves, which are more valuable than coal.

The valuations of leading mining companies set the upper-range benchmark for evaluating smaller peers in the industry. These major players, known for their strong operations track records, set a standard in a sector that is highly regulated and fraught with hazardous accidents, impacting both ESG and financial risks.

Larger mining companies typically control higher-quality assets, as reflected in their Average Selling Price 'ASP' and cash costs of mined commodities, including Metallurgic coal. In Q3 2023, for instance, METC achieved $188 per short ton for its coal products (including transport), whereas BHP Group realized $218 per ton (a mix of FOB and transport revenue). This price difference reflects BHP's strategic focus on superior mines and its ongoing divestiture of lesser-quality ones. This strategic shift towards premium mines justifies a higher valuation. METC's valuation at 9x PE, compared to BHP's average of around 13x, suggests that METC is fairly valued, considering its operational context and asset quality. METC's valuation is thus aligned with industry averages and seems reasonable when considering its market position in the metallurgical coal sector.

Risk

Our 'Hold' rating on METC is based on the expectations that the company's performance will align with broader market trends. The key driver behind this assessment is the management's plan to reduce growth Capex in the near term, a shift from the previous growth strategy that had driven share appreciation.

Although management has indicated a capacity for flexible production increases, the source and magnitude of this flexibility remain uncertain. We speculate it could stem from improved operational effectiveness and mine utilization, potentially leading to a modest uptick in production capacity if market conditions necessitate such a move. However, should this flexibility prove greater than anticipated, it could lead to increased production and sales, especially in accommodative market demand conditions, potentially resulting in share price growth exceeding that of the broader sector.

On the other hand, the rapidly evolving technology in coal alternatives for steel production presents a significant risk. With predictions like the Yale University white paper suggesting that 53% of global steel will soon be produced using Electric Arch Furnaces 'EAF' instead of coke coal, demand for metallurgical coal could see a sharp decline. This shift not only threatens to reduce coal demand, but may also accelerate regulatory changes targeting lower-tier metallurgical coal. This looming technological shift in steel manufacturing is a critical factor that could negatively impact METC's performance in the short term if attention to these long-term risks comes to the surface at any time next year, potentially leading to METC's underperformance relative to companies with higher coal quality.

Summary

Although METC has demonstrated robust growth and remarkable stock performance, driven primarily by increased production and sales, several factors temper our outlook going into 2024. The company's strategy shift towards reduced growth Capex and increased focus on operational efficiency signals a transition from aggressive growth to consolidation. Rising costs and declining unit revenue amid a fluctuating market for metallurgical coal pose valuation challenges. These factors, combined with METC's current valuation at the higher end of industry averages, underpin our 'Hold' rating.

For further details see:

Ramaco Resources: From Market Expansion To Market Realities